SUMMARY

In 2017, Indian Fintech Startup Raised A Whopping $2.59 Bn In Funding

This article is part of Inc42’s Startup Watchlist annual series where we list the top startups to watch for 2018 from industries like Blockchain, Logistics, Fintech etc. Explore all the stories from ‘Startup Watchlist’ series here.

“Digital technology provides a low-cost way for people in developing countries to send money to each other, buy and sell goods, borrow and save as long as the financial-regulation environment is supportive.” – Microsoft co-founder and former CEO Bill Gates.

In India, the need for technological disruption in the banking sector is all the more acute, given that over 19% of the country’s population still remains unbanked. This is where fintech startups come in.

Touted as the year of financial technology services, 2017 saw the emergence of a legion of promising fintech startups that are working to bring innovation and disruption to the otherwise conservative Indian banking sector.

Forecasted to cross $2.4 Bn by 2020, as per a report by KPMG India and NASSCOM, India is currently home to more than 500 fintech startups, whose collective aim is to attain financial inclusion. Since early 2015, the fintech sector has undergone massive changes, chief among them being the move towards a cashless economy.

The government’s enthusiastic promotion of cashless technologies – digital wallets, Internet banking, the mobile-driven point of sale (POS) and others – as well as the launch of IndiaStack including Aadhaar, eKYC, UPI and BHIM have also managed to restructure the financial sector, disrupting the long-held monopoly of traditional institutions like banks.

The Explosive Growth Of Indian Fintech Sector

Home to more than 462 Mn Internet users, the number of mobile users in India is expected to reach 1 Bn by the year 2020. In fact, it has the greatest market potential in the entire world, as determined by the Harvard Business Review (HBR) in its latest edition of Digital Evolution Index 2017.

Increased access to the Internet and social media, coupled with the explosion of smartphones, tablets and computers, have helped usher in swift, automated and efficient financial services solutions. Another factor that has played an integral part in the rise of the fintech industry was demonetisation (November 8, 2016).

Post the ban on INR 500 and INR 1,000 notes, India witnessed an acute dearth of cash, which in turn caused Internet-enabled cashless transactions to sky-rocket. As reported by Inc42, digital transactions increased 22% almost immediately after the ban came into effect.

In less than 24 hours after the embargo was announced by PM Narendra Modi-led government, Paytm saw an overwhelming 435% increase in overall traffic. Other digital wallets like PayU India witnessed a staggering 80% jump in transactions, while FreeCharge claimed that the average wallet balance on its platform increased 12 times. MobiKwik meanwhile reported an over 40% increase in app downloads within less than 18 hours of the announcement.

Digital wallets weren’t the only beneficiaries of demonetisation., Bengaluru-based mPoS solution provider Ezetap, which makes its own point-of-sale devices to enable merchants to receive digital payments, saw a 25% spike in transactions.

With the entry of big players like Amazon, Google, PayPal and Uber, India’s digital payments space has morphed into a $500 Bn behemoth in the making, according to a report by Google and Boston Consulting Group.

Simultaneously, a brigade of related startups has also emerged in different sub-sectors of fintech, such as in loan and insurance. For instance, there is BankBazaar as well as Gurugram-based insurance comparison platforms like Policybazaar, and financial services companies like IFMR Holdings.

Then there are companies like Mumbai-headquartered BillDesk, Instamojo and mobile-based Point of Sale (POS) providers Mswipe that have helped bridge the gap between the common man and the small retailers.

In segments such as alternative lending, including SME lending and P2P lending, startups also took the centre stage this year with players like ZestMoney, Capital Float, Lendingkart, CashCare, Indifi, Rubique, Faircent cashing in on the opportunity.

Fundings Aplenty In The Indian Fintech Sector

According to Inc42 DataLabs, the Indian fintech sector reported 102 funding deals this year till November, worth $2.59 Bn. As per data available, fintech startups grew by 31% Year-on-Year (YoY) to almost to 360 in 2017, with almost $200 Mn funding received in H1 of this year, recording a growth of 135% since H1-2016. In the sector, sub-segments like digital payments and lending are maturing, while wealth management and insur-tech emerging as growth areas.

Almost 33% of funding raised by fintech startups was in the areas of artificial intelligence and analytics.

This year, maximum investments took place in this segment at the late stage, with Paytm topping the charts with a staggering $1.4 Bn funding, followed by Flipkart-owned PhonePe, which reportedly secured $500 Mn from its parent entity. Then there was US-headquartered Ebix Inc that made headlines when it poured $123 Mn (INR 800 Cr) in Mumbai-based payments solution firm ItzCash, against an 80% stake in the company.

If we are talking about acquisitions, how can we forget Hyderabad-based Payswiff, earlier known as Paynear which after expanding routes in Indian cities is now eyeing international markets? In October this year, Payswiff acquired Singapore-based GoSwiff in a deal reportedly valued at around $100 Mn. With this deal, this Indian startup now has an access to 20 new markets in South East Asian, Middle East, Commonwealth of Independent States and Eastern European markets. With all this, Payswiff is aiming to clock $16.8 Mn (INR 110 Cr) in revenues with marginal profits.

Well, it seems that fintech is going to be a sector to watch in 2018 too with so much going on around the clock.

Before we embark on an equally eventful journey in 2018, let’s take a look at the top nine fintech startups (which have raised less than $25 Mn in funding) that are a must watch in 2018.

Indian FinTech Startups To Watch Out In 2018

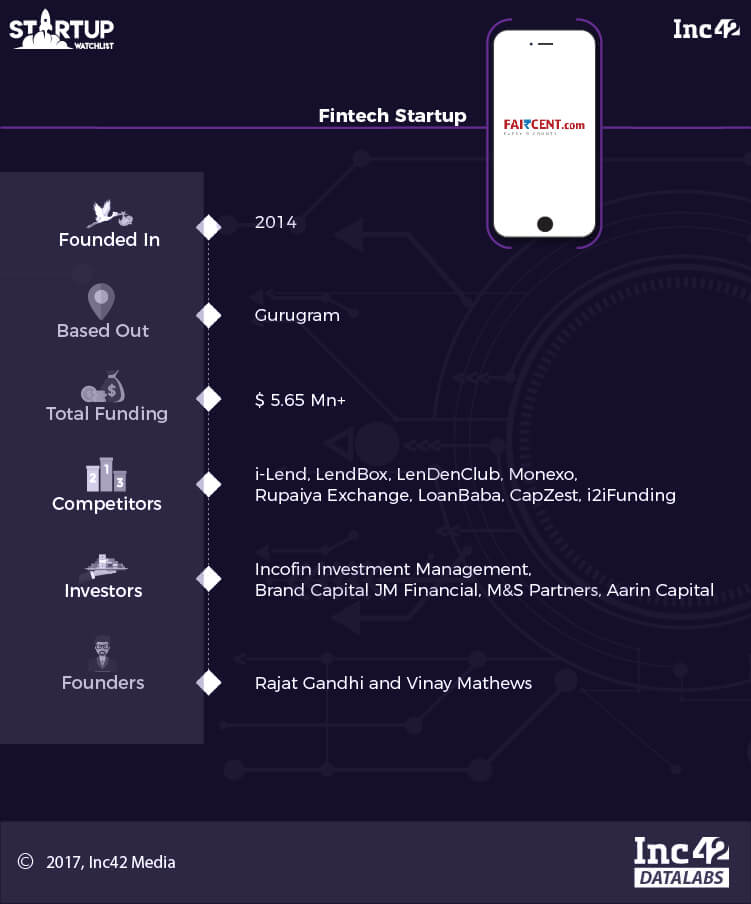

Faircent

Gurugram-based Faircent is a peer-to-peer lending startup that connects lenders with borrowers. Launched in 2014, the startup offers a variety of tools such as Auto Invest, which is a fully-automated feature that matches a lender’s investment criteria with the borrower’s requirements and automatically sends proposals to the borrower on behalf of the lender, based on pre-selected lending criteria such as loan tenure, amount, and risk profile.

Recently, the startup, under the trusteeship of IDBI, created an Escrow account for its lenders to help in faster and smoother flow of funds enabling them to make greater returns on their investments.

As part of a move aimed at diversification, Faircent introduced a semi-secure loan product in collaboration with Bengaluru-based micro-lending startups. The initiative was aimed at helping students avail fast and easy personal loans at a reasonable cost.

Till date, lenders on the platform have committed to lend over $4.8 Mn (INR 31 Cr), while borrowers have sought up to $3.5 Mn (INR 23 Cr) in loans. At present, Faircent claims to receive over 225K loan requests per month, with most of them being used for funding businesses, family events, appliance purchases, debt consolidation, among others.

Earlier, Faircent was showcased as one of the top startups at Start Up India, selected for the first batch of NASSCOM 10,000 and was also part of the Microsoft Accelerator Winter Cohort and BizSpark programme.

The Indian P2P lending industry has undergone a massive boom this past year, thanks in part to the RBI’s decision to regulate the space. Expected to hit the $4 Bn-$5 Bn mark by 2023, the P2P lending space is inhabited by some 30 players, namely i-Lend, LendBox, LenDenClub, IndiaMoneyMart, Monexo, Rupaiya Exchange, LoanBaba, CapZest and i2iFunding.

Riding on the ongoing fintech revolution, Faircent is gearing up to reach a larger group of people and businesses seeking capital that they can borrow online, without having to rely on an official financial institution as an intermediary.

Unlike most other players in the sector, the Rajat Gandhi-led startup has attracted substantial investor attention. Armed with a war chest of more than $5.65 Mn, how Faircent fares in 2018 will be interesting to watch.

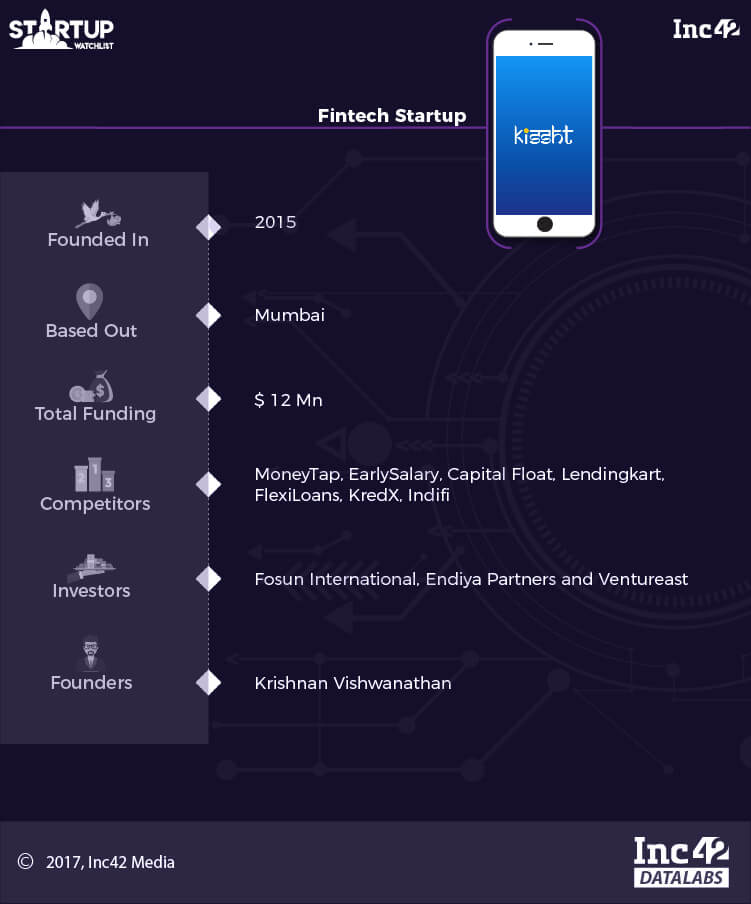

Kissht

Conceived in 2015, Mumbai-based Kissht is a fintech startup that provides instant credit to consumers for making purchases at digital points of sale (both offline and online). Through its app, users can buy various items including mobiles, laptops, jewellery, and electronics by opting for flexible EMIs even without a credit card.

Once logged in to the app, users can see in-app merchant partners or choose to buy items from the Kissht store. A user can upload documents and make the down payment and pay the processing fees.

For customers with ongoing loans, Kissht provides an option to check the available line of credit. Also, users can make an early payment or view upcoming EMIs and invoices for the same. The fintech startup also provides cash loans that can be used for house renovation, holidays, purchase of consumer durables, education, short-term loan for equipment purchase, etc.

As claimed on the Kissht’s official website, loan approvals on the platform take anywhere between 90 to 120 seconds. The company claims to have a fixed rate of interest which is charged on a monthly reducing basis. Users can avail flexible return tenures of up to 60 months and repay loans in installments. Last month, Kissht raised $10 Mn (INR 67 Cr) in a round led by Chinese investment conglomerate, Fosun International.

At the time, it was reported that the consumer lending startup was keen on expanding its presence across 15 to 20 tier II and tier III cities in India such as Amravati, Vijayawada and Satara, among others.

According to a report by brokerage firm Credit Suisse, the Indian consumer finance market is expected to touch $1.2 Tn by 2020, expanding at a compound growth rate of 18%.

With the advent of ecommerce, consumers are increasingly looking for easy credit to make online purchases. Kissht is feeding this demand through swift loan approvals and a growing presence in tier II and tier III cities across the country.

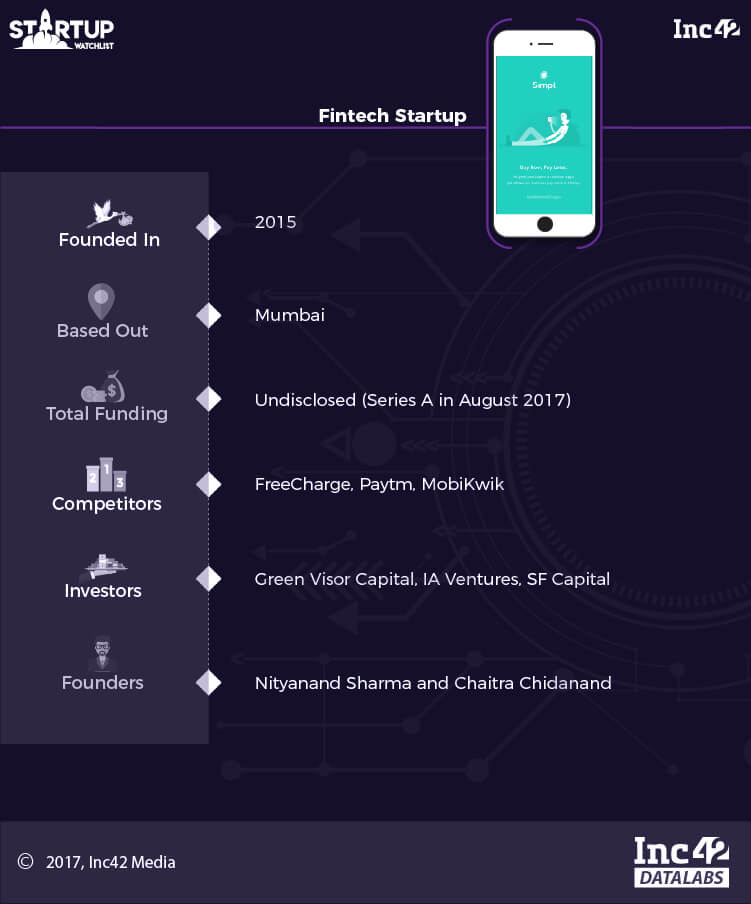

Simpl

Launched in 2015, Simpl is an online payment instrument that allows customers to make purchases and settle payments online. It is a data-driven, mobile-first platform that works by reducing the payment flow to a single tap, therefore improving the client’s product experience, and giving users a payment model that’s faster and more convenient than wallets or cards.

Instead of having the make payments individually, customers can choose to pay just one bill, with all the online purchases added up. Among the merchants that currently work with Simpl include BookMyShow, FreshMenu, Faasos, Nykaa, Licious, Grofers, DocsApp, Drivezy, Dunzo and others. At present, the spending limit of customers on Simpl ranges between $11.7 (INR 750) and $78 (INR 5,000).

In August this year, the Mumbai-based payments startup reportedly raised an undisclosed amount in a Series A round led by US-based venture fund Green Visor Capital LP II. The round also saw the participation of other investors, including IA Venture Strategies Fund II LP, Boillot Family Trust, Russell M Byrne, The Oliver R. Grace Jr. Millennium Trust, SF Capital Investments LP and DIA Investments LLC.

As claimed by the company’s spokesperson, Simpl boasts a customer retention of around 85% overall, which is growing at 50% monthly. During a media interaction last year, co-founder and CEO Nityanand Sharma stated that the company had already achieved positive unit economics on every transaction.

To bolster its product portfolio, the company has also partnered with a number of banks and NBFCs.

In an already-saturated digital payments market, Simpl comes armed with biggies like BookMyShow, Grofers, Nykaa, FreshMenu and others as clients. The company’s chief selling point is its convenience.

By offering users the convenience of settling payments through a single bill, the tech-enabled startup is aiming to reach 100 Mn over the next few years.

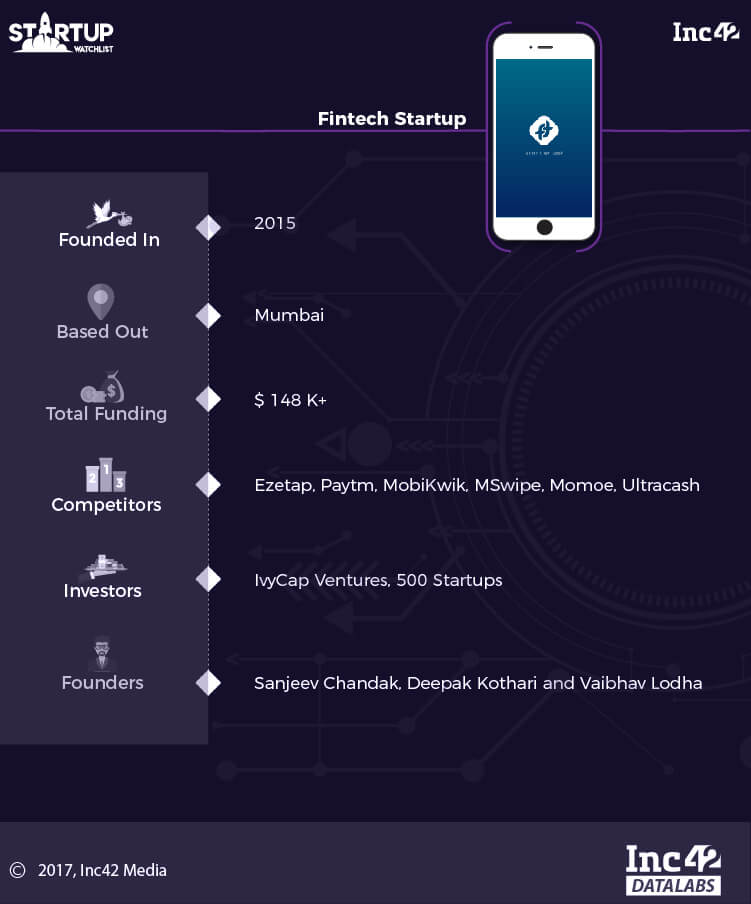

FTCash

Founded in June 2015, Mumbai-headquartered FTCash provides seamless solutions for micro-merchants to accept payments through multiple payment instruments including debit cards, credit cards, and mobile wallets. It additionally also provides short-term loans to these merchants.

FTCash was part of PayPal’s Start Tank Incubator Challenge in Chennai and was also one of the six winners of the UK Trade and Investment (UKTI) India and iSPIRT-organised Great Tech Rocketships Initiative 2016 (GTRS). In August 2016, the fintech startup was named as one of the 12 finalists of IBM Smartcamp for Fintech challenge.

The platform also empowers micro-merchants and SMEs by offering easy access to credit. Loans disbursed by FTCash usually range from $1000 to $20,000, with interest rates somewhere between 18 and 30%. It is currently participating in the MasterCard Start Path programme, which is aimed at supporting later-stage fintech and tech companies with the aim of shaping the future of commerce.

At TechCrunch’s recently-held Startup Battlefield, FTCash co-founder Vaibhav Lodha stated that the company currently facilitates digital payments of up to 25,000 merchants and is growing at 30% month-over-month for the past 18 months. It plans to scale to $233 Mn (INR 1,500 Cr) worth of annual transactions.

The digital payments industry in India is projected to reach $500 Bn by 2020, as a per a report by Google and Boston Consulting Group. Over the last 12 months, thanks in part to demonetisation and the government’s enthusiastic promotion of IndiaStack, FTCash has witnessed a dramatic increase in transactions, which has, in turn, catapulted its revenue to more than $1 Mn.

With thousands of micro-merchants, including neighbourhood Kirana stores, utilising the platform to offer digital payment solutions to customers, the fintech startup is slowly emerging as a strong player in the country’s digital payments sector.

One of the company’s biggest selling points lies in its founders’ strong banking and financial services background. Harvard-educated Vaibhav Lodha, for instance, worked as a consultant at The World Bank prior to starting FTCash. While Deepak Kothari has worked at the world’s top five accounting firms, Grant Thornton.

FTCash co-founder and CEO Sanjeev Chandak, on the other hand, completed an MBA Finance degree at the prestigious Wharton School of the University of Pennsylvania. Before starting his own venture, Chandak served as the Deputy CFO of Deutsche Bank and was also the Director of US-headquartered bank holding company, Capital One.

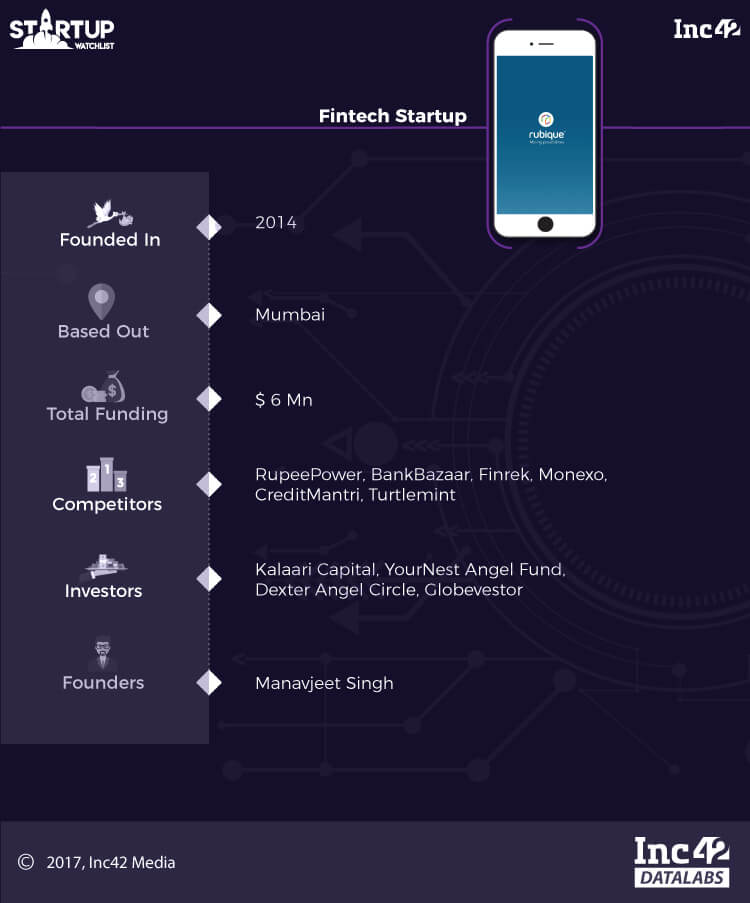

Rubique

Launched in 2014 as Bestdealfinance, Rubique is an online marketplace for financial products offering a wide range of loan products and end-to-end loan fulfilment to individuals and MSMEs.

The fintech startup has introduced a tech-led lending solution whose model is focused on disbursement rather than mere lead generation allowing the customer to get the best deal in the quickest possible time while lowering the cost of customer acquisition for the financial institution.

With the help of unique algorithm, machine learning and AI, the online portal facilitates the disbursal of up to 235+ products such as personal loans, car loans, home loans, business loans, loans against property, credit cards, healthcare and construction equipment financing, among others.

Working to bridge the gap between lenders and borrowers through a wide range of capital financing options, Rubique currently has two verticals. First, it provides the users with a well-aggregated, curated and digitised collection of products with partner financial institutions. Second, after comparing and selecting the required product the user can instantly apply online.

The company has also developed its own credit score – Rubique’s Magic Score – that can be integrated with the bank’s lending system.

The fintech startup is also part of the year-long 42 Fellowship by Inc42. Prior to that, in August 2016, it was crowned as one of the 12 finalists of the IBM Smartcamp for Fintech.

The Indian fintech startup space has seen the emergence and growth of startups that have disrupted the traditional ways of how businesses have been conducted. Lending and payments industry has been revolutionised, but at the same time, the space has become saturated now.

In a space where Capital Float offers tailored products, Lendingkart offers instant loans, BankBazaar offers instant paperless solutions, Rubique focusses on disbursements, with a neutral business model and aims to become the go-to solution for loans, insurance and other financial products.

For Rubique, the real game changer has been customer procurement, end-to-end satisfaction and technology. This could also explain how, in just three years of operations, the fintech startup has clocked annual revenue of over $2.6 Mn (INR 17.5 Cr).

With the startup looking to tap into the largely unstructured market of alternative financing, there is tremendous opportunity for it to scale. How far will it be able to carve a niche for itself amidst the competition in 2018 remains to be seen.

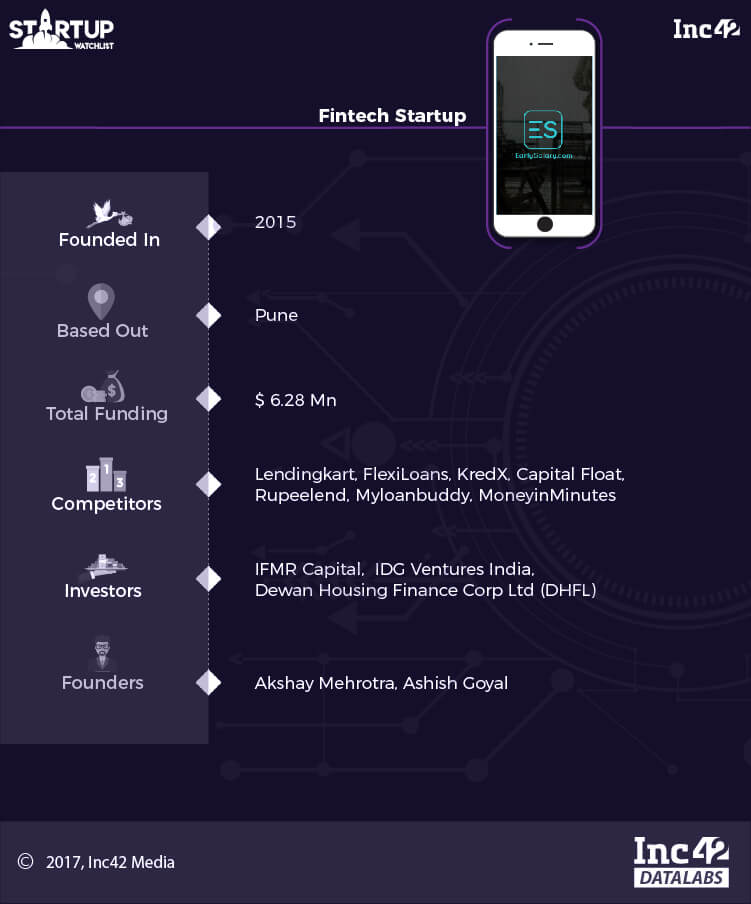

EarlySalary

Founded in 2015 by Akshay Mehrotra and Ashish Goyal, Pune-based EarlySalary is a mobile-first lending platform. It provides salary advances and instant cash loans and provides a smart risk scoring system.

These loans are similar to salary/cash advances or credit card cash withdrawal. The startup currently has operations in eleven cities including Mumbai, Pune, Chennai, Bengaluru, Hyderabad, New Delhi, Jaipur, among others.

The fintech startup provides salary advance up to 50% of monthly salary to its users. The company claims that 70% loans are given in under 10 minutes. Apart from this, salary advance/cash loans are transferred to bank instantly.

To that end, the company has also partnered with corporates as well as SMEs across the country to give salary advances to employees. Over the past year, the company has developed its ‘Underwriting System’ which is a self-learning, algorithm-based decision-making system. The system reviews social media in real-time as well as Credit Bureau data of customers and helps approve the loan.

The ticket size of loans ranges between $125-$1,561.8 (INR 8,000 to INR 1 Lakh) for a period of up to 30 days. The money is lent at a cost as low as $0.14 (INR 9) per $156.1 (INR 10,000), per day.

The app has received nearly 1 Mn downloads on Android and iOS mobile app platforms. As claimed by the company’s spokesperson, EarlySalary has disbursed 42,000 loans to customers till date worth $9.3 Mn (INR 60 Cr).

According to some market research agencies, the Indian payday loan market currently stands at $10.27 Bn (INR 70,000 Cr). Growing at a rate of 14% yearly, the sector is expected to touch $14 Bn by the end of 2017.

The space has seen the emergence of a number of innovative startups that are using technology to make short-term loans more accessible to young Indians. Given that credit card penetration in India is still relatively low at 24.5 Mn as of March 2016, alternative lending startups like EarlySalary are working to bridge the gap in credit card usage.

Armed with a strong team and sufficient funding from big investors like IFMR Capital and IDG Ventures India, the fintech startup is riding the digital wave to expand its footprints across tier II and tier III cities in the country.

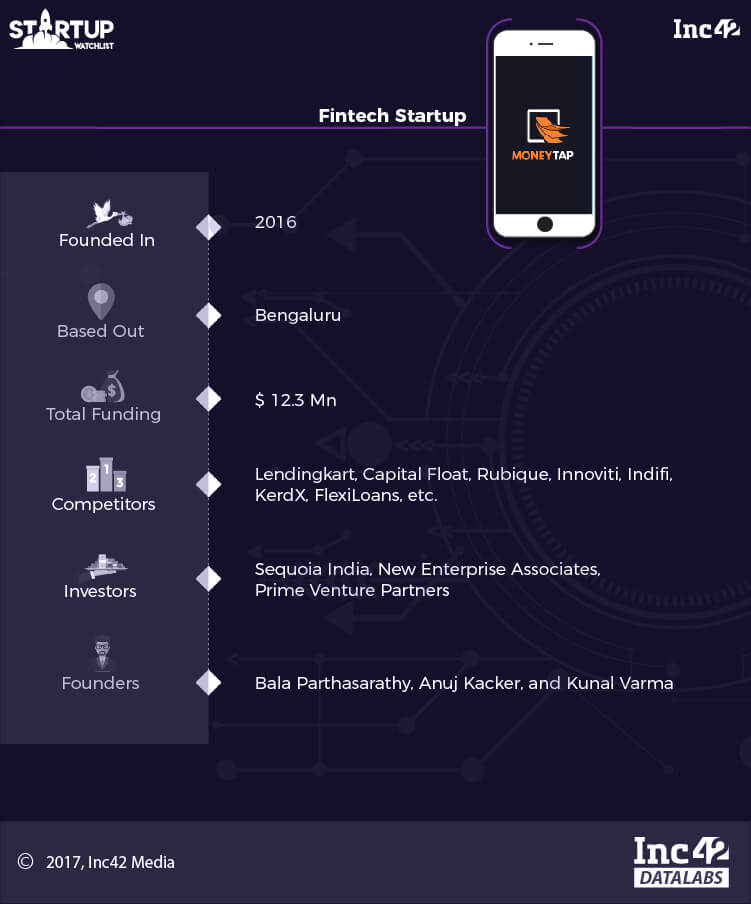

MoneyTap

Touted as India’s first app-based credit line, MoneyTap is a Bengaluru-based consumer lending startup that is working to democratise credit by providing flexible loans for personal use. The fintech firm currently caters to customers with monthly income ranging between $308-$1,080 (INR 20,000-INR 70,000).

MoneyTap’s proprietary technology strives to solve this problem of insufficient consumer credit line by targeting the country’s fast-growing middle-income group who needs money for shopping, paying school fees, rent, weddings, sending money to family and so on.

On the MoneyTap platform, consumers can borrow anywhere between $46-$7,715 (INR 3,000 to INR 5 Lakh) with an option to choose the repayment duration from as little as two months up to three years. Unlike other consumer lending platforms, credit assessment on MoneyTap happens in real time.

As claimed by MoneyTap co-founder and CEO Bala Parthasarathy, the entire process of credit evaluation takes around 3 to 7 minutes, depending on how fast the customer types. Since its launch in September 2016, MoneyTap has grown by leaps and bounds.

The platform has gone from zero to 300K registered users across 14 cities in India. With a small office in Mumbai and a head office in Bengaluru, MoneyTap’s present workforce comprises 30 people. The consumer lending company is currently working with seven banking/NBFC partners at different stages of integration, including the RBL Bank.

Armed with more than $12.3 Mn funding, the fintech startup has an average default rate much below 1%. Furthermore, compared to credit card interest rates which typically range somewhere between 3% and 4% per month, the interest rates charged by the MoneyTap app are just over 1.5%.

The startup is aiming to disburse credit line worth about $46.2 Mn (INR 300 Cr) by the end of the current fiscal year. As part of its immediate goal, MoneyTap intends to hit unit economics profitability within the next six to 12 months. Over the next three years, MoneyTap is gearing up to lend more than $1 Bn worth of credit line and is also looking to expand operations across 100 cities.

In a country where 19% of the population is still unbanked, MoneyTap is working to provide consumers with a personal line of credit to be used whenever and however they want. Since the cost of evaluating and issuing a credit line/loan/credit card for a bank is extremely high, they usually prefer to give big-ticket loans to few people rather than small ticket loans for a large group of people.

The average loan ticket size in this country is between $4,629 – $7,715 (INR 3 Lakh-INR 5 Lakh). This also means that banks focus on only around 12 to 15 Mn customers at the top of the pyramid. With an innovative business model, Sequoia-backed MoneyTap is aiming to serve people in need of credit lower than the above-mentioned bracket.

In recent times, with consumer Internet companies like Flipkart, Amazon and Reliance Retail entering the Indian market, the consumer has become more demanding. Consumer credit, therefore, has become an attractive space for promising tech startups like MoneyTap.

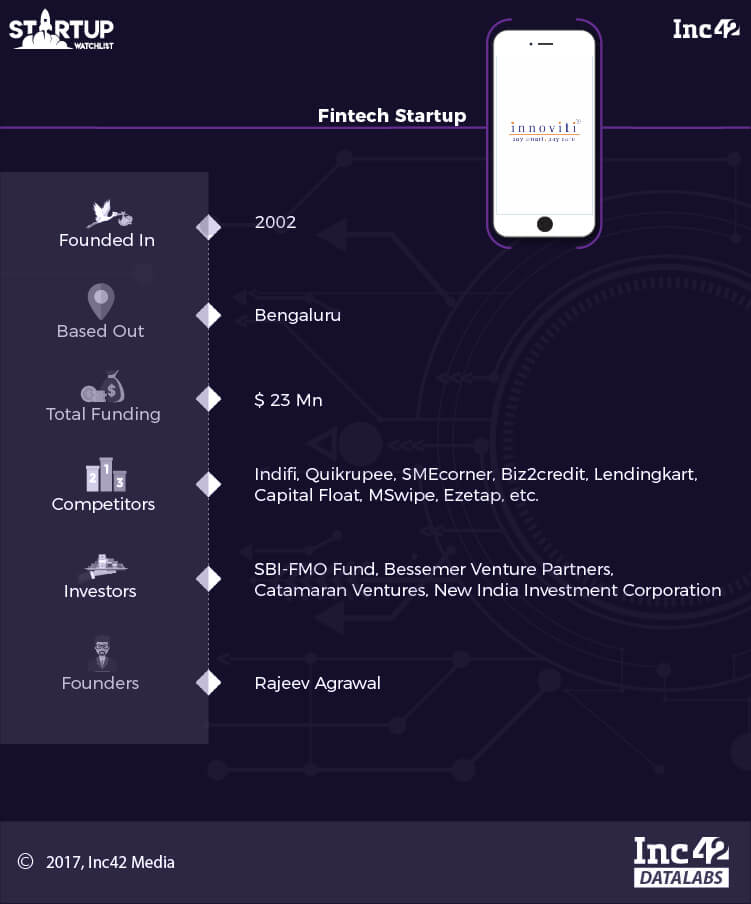

Innoviti

Started by IIT Bombay alumnus Rajeev Agrawal as a wireless hardware systems manufacturers in 2002, Innoviti has since forayed into digital payments and SME lending.

On one hand, the company’s solutions help businesses in reducing the cost of processing digital payments by automating the manual processes used by them. On the other, it facilitates the growth of small businesses by supplying hassle-free working capital.

Today, Innoviti’s flagship product UniPAY processes close to one-fifth of all digital payments made at large retail stores in the country, amounting to a staggering $3 Bn transactions annually. Operating in about 700 cities across India, the UniPAY platform has undergone a near 100% growth between March 2016 and March 2017.

Innoviti’s payment platform clientele includes Reliance Retail, Titan, Indigo, Walmart, and several others. Banks such as HDFC, ICICI, Axis, use the platform to access customers for processing their payments and loans distribution.

Since its launch in 2016, Innoviti’s SME lending product has disbursed between about 160K loans to over 30,000 small merchants in different parts of India. The yearly disbursement volume of SME lending ranges from $62.3 Mn (INR 400 Cr)–$78 Mn (INR 500 Cr), with the average ticket size of loans being around $312 (INR 20,000) and payback duration of not more than 15 days.

Despite cut-throat competition in the digital payments space, Bengaluru headquartered Innoviti seems to be right on track. Fifteen years after it took its first step, the company has blossomed into a formidable enterprise with of a workforce of more than 150 people across offices in Mumbai, Chennai, Delhi, and Hyderabad.

The company’s main selling points have been its focus on building technologies that facilitate speed, reliability, and flexibility. During an earlier interaction with Inc42, Innoviti founder and CEO Rajeev Agrawal talked about the importance of frugality when it comes to creating a successful business.

With its eyes set on hitting profitability within the next 12 to 18 months, Innoviti is aggressively banking on the increasing popularity of digital transactions in the retail segment, which is slated to reach 30% in the coming five to seven years.

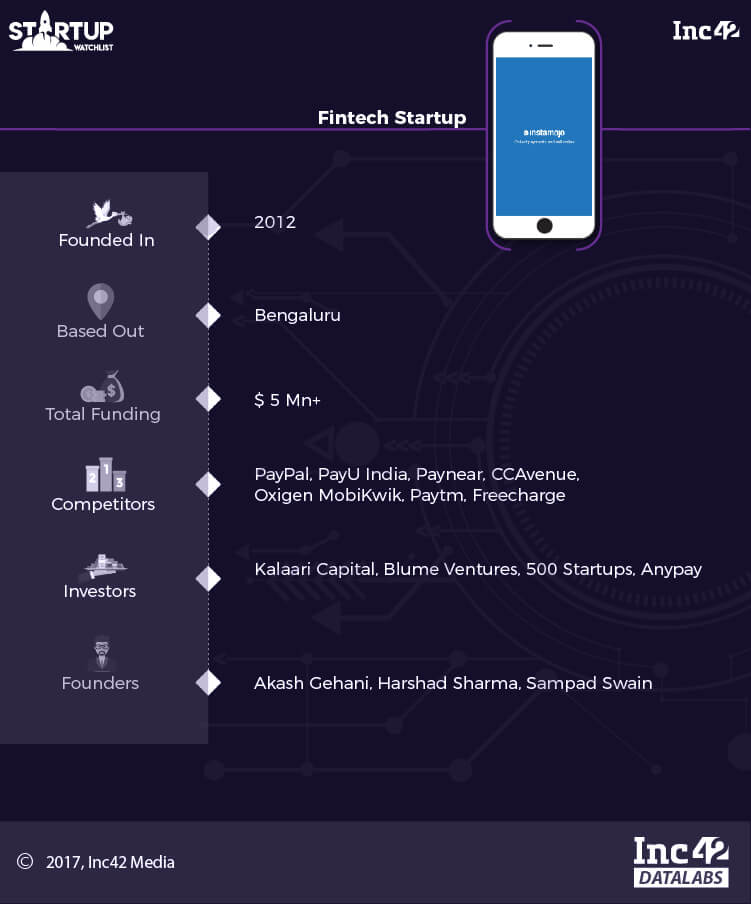

Instamojo

The brainchild of Akash Gehani, Harshad Sharma and Sampad Swain, Bengaluru-based Instamojo is a micro product and digital payments platform for SMEs. It allows users with a mobile device and a bank account to accept payments using credit and debit cards, e-wallets and via UPI.

The startup helps merchants build their online identity and sell, manage and grow their businesses online. It provides a suite of tools, including an online store where merchants can showcase their products and services. Merchants can also connect to a marketplace which allows business owners to connect with sellers offering services such as digital marketing, content, logistics, SMS marketing, etc.

Post demonetisation, the digital payments company witnessed an increase in the number of merchant registrations by 106% as well as a 150% growth in new merchant activations over the last financial year. Digital transactions performed on Instamojo’s platform have also surged by over 178%, in the last year alone.

Currently catering to over 300K registered merchants, Instamojo claims to have acquired 10% of the digitally-active small businesses in India and controls 30% of their annual turnover. In July this year, the fintech company turned EBITDA positive and has since witnessed a 10-15% month-on-month growth.

In 2012, Instamojo was one of the first Indian startups to join the Silicon Valley-based 500 Startups’ Accelerator Programme.

Aiming to extend its share in the Indian digital payments space to 70% by 2019, Instamojo is currently working to expand its footprints among the country’s merchant community. As stated by its spokesperson, the fintech startup is looking to increase its reach by 400% to around 1 Mn SMEs and MSMEs by 2018.

Currently, there are about 50 Mn MSMEs in India of which only 30% have gone digital in some form or the other. However, only about 5% of the entire MSME population uses computers or smartphones to trade a total turnover of $60 Bn.

Despite the challenges associated with it, Instamojo is working to bring offline merchants to the online realm. Instead of focussing on one solution, the fintech startup Instamojo is shaping up to become a complete business solution with a vertically integrated approach of providing various core services like payments, ecommerce enabling services, compliance, lending and other services like logistics and promotions.

Editor’s Note

Banking activities in India can be traced backed to the 18th century around the time that the Bank of Hindustan was created. Since then, the Indian banking sector has undergone several phases of evolution to transfigure into a $1.54 Tn mammoth by FY17.

Over the years, the country’s banking industry has weathered many storms. Quite surprisingly, it managed to remain relatively unscathed during the global financial crisis of 2007-08, which kicked the economies of even developed nations like the US off their feet.

In fact, according to one report, by 2025, India could be a $5 Tn economy, adding $1 Tn to its worth every 18 months thereon! Much of the nation’s recent economic growth has been driven by progress in the banking segment. Apart from an unshakable resilience, the sector has witnessed strong growth in saving and rising disposable income levels.

Furthermore, in recent years, access to the banking system has also improved significantly, thanks largely to the government’s efforts to integrate technologies into the other conservative sector as well as facilitate expansion in unbanked and non-metro regions across the country.

Despite the huge strides that the Indian banking sector has made in the last couple of years, it continues to be riddled with inefficiencies and latencies. For instance, in a country with a population of over 1.31 Bn, only 220 Mn people have PAN cards. Other forms of KYC (know your customer), including voter ID, Aadhaar and ration cards, are also not widely used.

Due to these challenges, financial inclusion still remains an elusive dream in India. Fintech startups, unlike traditional financial institutions, bring with them a myriad of advanced technologies for both consumers (through digital payment, POS, and wallet solutions) as well as banks and NBFCs (in the form of Big Data analytics, credit assessment, hassle-free KYC, etc.)

As prophesied by co-founder and CEO of 11:FS David Brear, “Technological innovations will be the heart and blood of the banking industry for many years to come and if big banks do not make the most of it, the new players from fintech and large technology companies surely will.

While these were the Indian fintech startups to watch out for in 2018, stay tuned for next edition of Startup Watchlist, where we will be featuring agritech startups to watch out for in 2018, click here for more stories!

[The startups mentioned above have been selected on editorial discretion, our interactions with the startups and other industry veterans.]