Over the past few years, the payments landscape in India has shown some major shifts with digital payments witnessing an exponential growth. The digital payments industry in India is projected to reach $500 Bn by 2020, contributing 15% to India’s GDP, as a per a recent report by Google and Boston Consulting Group.

The report is based on Nielsen’s qualitative and quantitative research with over 3,500 respondents (digital consumers – 1,516, remittance users – 917 and merchants – 917), across nine geographies – Delhi, Mumbai, Bangalore, Ludhiana, Lucknow, Indore, Surat, Visakhapatnam and Coimbatore.

As revealed by the report, by 2020, non-cash (includes cheques, demand drafts, net-banking, credit/debit cards, mobile wallets and UPI) contribution in the consumer payments segment will double to 40%. Already 81% of existing digital payment users prefer it to any other non-cash payment methods. Indian consumers, are 90% as likely, to use digital payments for both online as well as offline transactions. Over 60% of digital payments value will be contributed by offline points of sale such as unorganised retail, eateries, transport etc.

Other Major Highlights Of The Report

- Online, shopping, payment of utility bills and buying movie tickets have emerged as the three top things that an Indian user primarily interacts with.

- Convenience has emerged as the most important factor that is driving the growth of digital payments in India. This is followed by availability of offers while opting for digital payment methods.

- Micro-transactions will form a substantial portion of the industry, with over 50% of person-to-merchant transactions expected to be under INR 100.

- The value of remittances and money transfer that will pass through alternate digital payment instruments will double to 30% by 2020 in the Indian market.

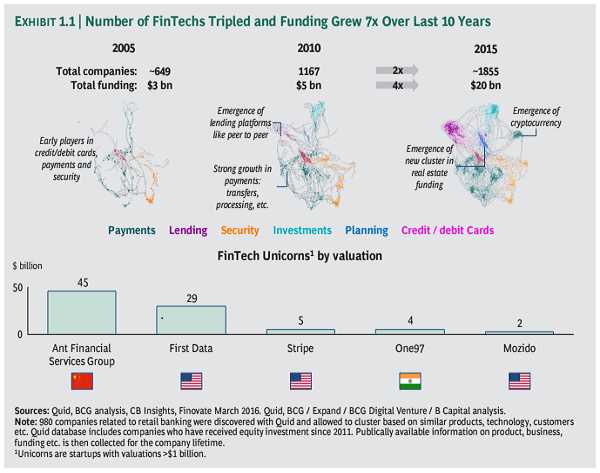

- Globally, the number of FinTech startups has doubled to 1,000 in approximately 5 years with funding growing 6X to reach $11 Bn in 2015

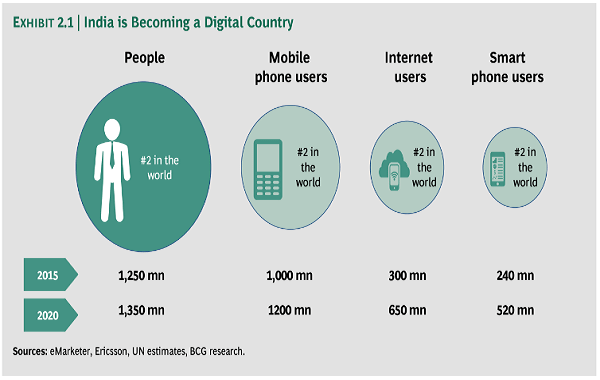

- India currently ranks #2 in the world with over 1 Bn mobile subscriptions. Of this, approximately 240 Mn consumers use smartphones and this base is projected to increase to over 520 Mn by 2020.

- 75 percent of merchants believe that using digital payments would accelerate future sales.

Expectations From Payment Ecosystem In The Next 5 Years

Technology will make digital payments simpler

Smartphone penetration, ubiquitous connectivity, biometrics, tokenisation, cloud computing and the Internet of Things are a few trends that will shape the way consumers transact in the future.

Merchant acceptance network to grow 10X by 2020

Mobile-based payment solutions and proprietary payment networks will drive merchant acquisition by offering low-investment solutions that will make economics more attractive for merchants and acquirers, resulting in over 10 million merchant establishments that will accept digital/mobile payments.

Payments will drive consumption—and not the other way around

Payments will provide access to customer transaction data, enabling payment service providers (PSPs) to offer relevant deals, offers and coupons to consumers, thereby influencing their consumption decisions.

Consolidation will drive ubiquity

Customers prefer fewer, ubiquitous payment solutions. Niche or limited use solutions will be forced to merge to offer near-universal solutions.

Modified UPI will be a game changer

Unified Payments Interface (UPI) provides a great platform for seamless interoperability of PSPs. Modified to overcome current challenges, it can drive large-scale adoption of digital payments.

Digital identity to accelerate customer acquisition

Using Aadhar for online authentication and confirmation of KYC data will boost the growth of digital payment systems.

Cash to non-cash ratio will invert over the next ten years

Digitisation of cash will accelerate over the next few years. Non-cash payment transactions, which today constitute 22 percent of all consumer payments, will overtake cash transactions by 2023. Digital payments instruments will drive the growth in non-cash payments.

Challenges

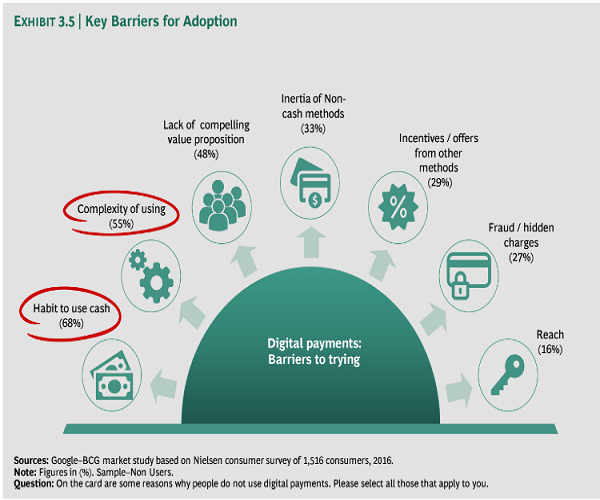

The research has shown that 1 out of 2 non-users haven’t used digital payments because they found the product too complicated to understand and 61% of non-user merchants find it complex to use. Additionally, the universal acceptance of digital payment methods and merchant concerns around the speed of transactions during peak hours, have emerged as other inhibitors to usage.

In order to accelerate the evolution of a successful and economically viable payments play in India, one must focus on building simplified products for users, addressing true customer needs. The stress should be laid on building an ecosystem exploiting next generation technologies to build low-cost and scalable solutions.

Finally, in a market like India, where regulations are still evolving, it is imperative that the Government and regulators take a long-term view to building a sustainable digital payments market. Regulators need to emphasise awareness on the cost of cash and incentivise the use of non-cash instruments, while the Government needs to shape policy that simplifies KYC requirements, making digital payment transactions more user-friendly.