SUMMARY

RIL’s recent acquisition of majority stake in Urban Ladder may look unfavourable for investors, but for the founders and the brand itself, it was a fire sale

Urban Ladder’s management gave up more than half of its valuation after the acquisition by RIL, but the retail behemoth was not the only suitor in the fray

Urban Ladder’s exit story is another example of inflated valuation and the consequent erosion of investor wealth. Will it impact online retail startups?

The deal market is awash with news in spite of the Covid-19 slowdown. And the latest to hit the headlines is the acquisition of Bengaluru-based online furniture retailer Urban Ladder Home Decor Solutions. On November 14, Reliance Retail Venture Ltd (RRVL), a subsidiary of Reliance Industry Ltd (RIL), announced an all-cash buyout of 96% stake in the company for a little over $24.5 Mn (INR 182.12 Cr). The RIL unit may also acquire the rest of the stake by December 2023 for another INR 75 Cr. But all that is history now unless we are ready to take a deep dive into the buyout and analyse the outcomes.

Let us not beat around the bush. Unlike other exits in the consumer internet space in 2020, this is no run-of-the-mill acquisition. Think, for a moment, how a billion-dollar edtech startup shelled out $300 Mn to acquire a smaller company within 18 months of its launch. In contrast, Urban Ladder, which has been around since 2012 and built a much-coveted private label, took a 75% cut in its paper valuation when the Mukesh Ambani-led retail behemoth acquired it.

A closer look at its funding history and past valuations are bound to make both entrepreneurs and investors slightly jittery.

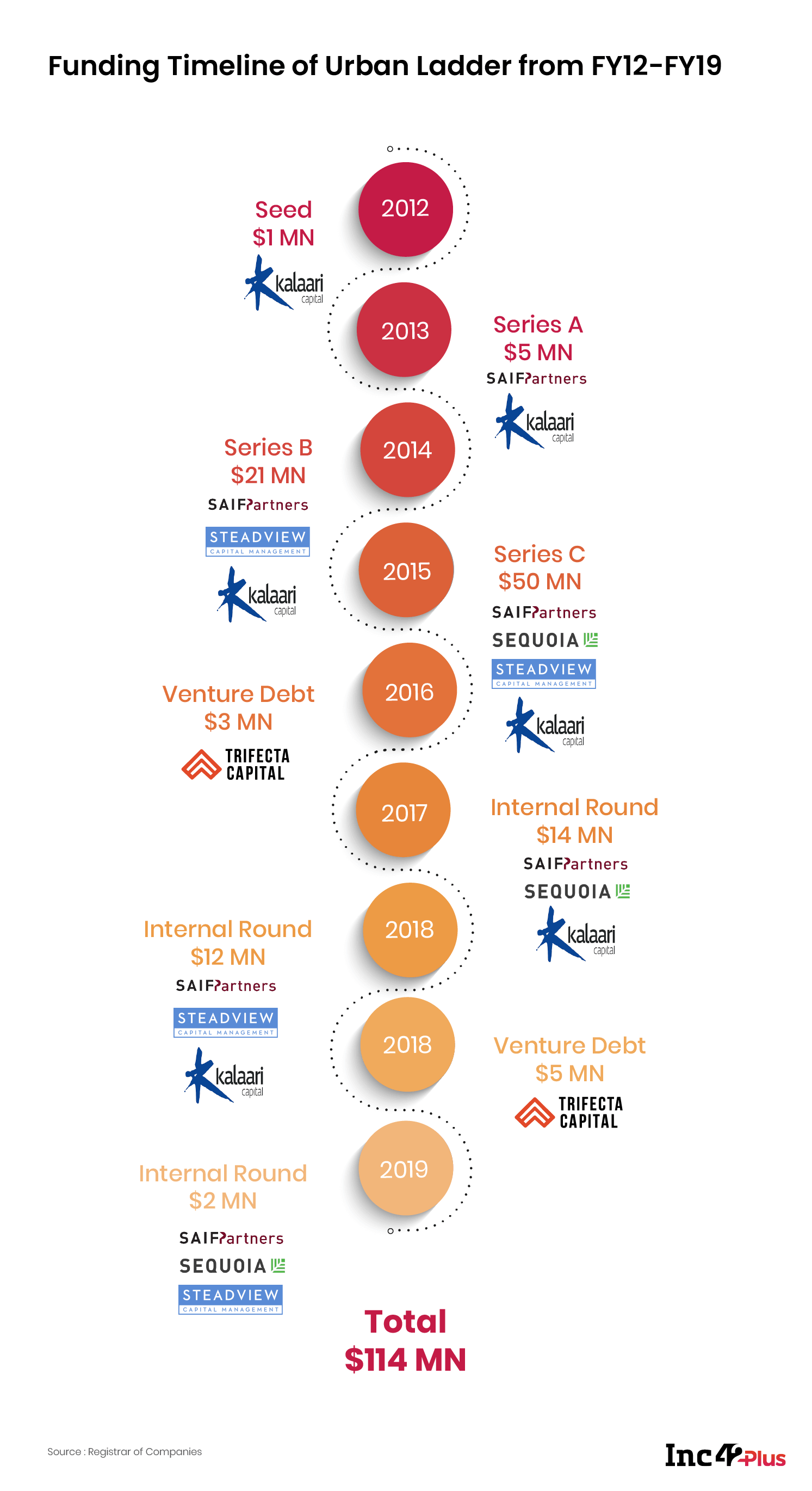

Founded in February 2012 by IIM-Bangalore graduates Ashish Goel and Rajiv Srivatsa, the company raised around $120 Mn from top venture capital funds such as Sequoia Capital, SAIF Partners, Kalaari Capital, Ratan Tata’s VC fund, and a hedge fund called Steadview Capital. The company closed its Series E round two years ago but struggled to get funding after that. In November 2019, it managed to raise INR 15 Cr although some of its existing investors did not participate in the round.

In fact, the furniture e-retailer went through a sticky patch throughout 2019. Several cracks started to appear in the firm’s business, including layoffs, and the exit of its cofounder Rajiv Srivatsa. In October last year, just months before a devastating pandemic swept the world, Srivatsa said in a press statement that his eight-year journey with Urban Ladder would come to an end. His exit came a day after Kalaari Capital’s Vani Kola resigned from the board of the company.

The financials and the change in post-money valuations over the years would further explain the scenario.

On paper, the online furniture retailer had a valuation of INR 780 Cr at the time of its equity fundraising in September 2018. This was slightly higher than its approximate valuation of INR 750 Cr, reached during the earlier funding round in February 2017. However, much of this valuation started to erode towards FY2019, way before the company entered into talks with RIL.

Two industry executives, directly aware of Urban Ladder’s acquisition talks, have told Inc42 the startup was looking for a buyer for the past one year and a half.

“Internally most of the investors knew this, especially as the company was not able to raise more funding than its direct competitor Pepperfry,” says one of them, requesting not to be named. By the end of CY2019, Pepperfry secured more than $200 Mn while Urban Ladder only crossed the $100 Mn mark.

According to him, when Urban Ladder started looking for a buyer in 2019, it targeted a deal value of INR 300 Cr or so, to be mostly paid in cash. This was already significantly lower than the INR 780 Cr valuation it had in the beginning of 2018. But by early 2020, the company brought its pricing down to around INR 200 Cr, especially after it started negotiating with RIL, both executives confirm.

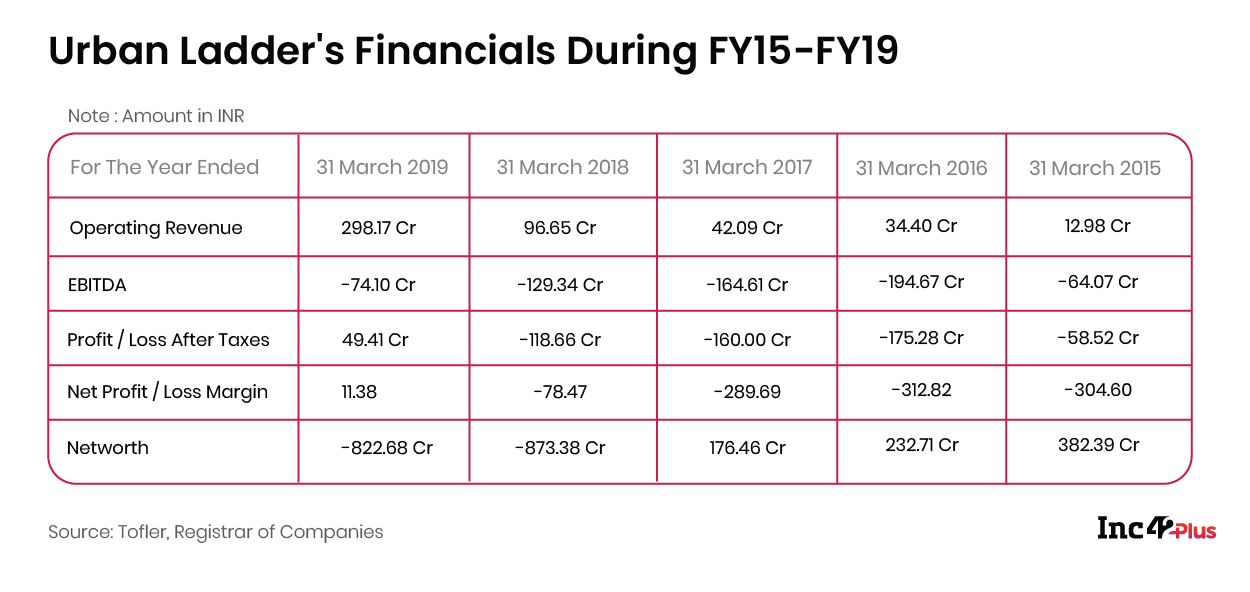

Meanwhile, the company’s financials have a different story to tell. According to its RoC filings, Urban Ladder reported a net profit of INR 49.41 Cr in FY2019, a huge improvement from the INR 118 Cr loss it posted in the previous financial year. It also recorded total revenue of INR 434 Cr in FY2019, a whopping 187% year-on-year jump compared to FY2018.

However, several industry experts and investors point out that the improvement was largely due to the company shifting from Generally Accepted Accounting Principles (GAAP) to Indian Accounting Standards (Ind AS) notified in 2013.

Urban Ladder shifting its accounting reporting standards to Ind AS played a significant role in marking up the company’s profit inFY2019. Apart from the INR 298 Cr revenue from actual sales of products, the company had a non-operating revenue to the tune of INR 136 Cr, which primarily came from furniture exchange deals, and other provisional income from unsold assets, as per FY2019 filings in the Registrar of Companies (RoC). Under Ind AS accounting standards, the exchange value of these assets is classified as non-operating income.

The startup’s FY2019 RoC filings, also show that while its operational revenue stood at INR 298 Cr (excluding INR 136 Cr in other non-operating income), the actual EBITDA loss was INR 74 Cr.

A Stellar Start And After

When Urban Ladder started its journey, the startup had a front-row seat to make it big in organised furniture e-retail. For instance, it began with 35 design categories and grew its portfolio to more than 5,000 types by 2019. By October 2016, it took another bold step and pivoted from a pure-play ecommerce platform to an omnichannel furniture brand, setting up its offline stores, or experience centres for that much-needed touch and feel. The pivot, however, came a little late. Its closest competitor and the biggest industry player Pepperfry had already gone ahead and launched its first ‘offline experience centre’ in Hyderabad’s high-street location Banjara Hills in June that year. By 2020, Pepperfry has around 40 offline stores while Urban ladder has just 10.

“The company (Urban Ladder) focussed on a private label business model, which was not a bad idea, and it also got them a good brand recall. But the furniture retail space is a tough market and everything depends on strategy execution,” says a venture capitalist requesting anonymity. He has portfolios in direct-to-consumer (D2C) space and online retail.

“Setting up offline stores was, in fact, an unavoidable strategy for Urban Ladder and Pepperfry. But furniture e-retail is still a very niche segment and historically speaking, such niche segments in India usually have a single winner. In cosmetics, Nykaa is emerging a winner; in fashion, it is Myntra; in the eyewear and accessories space, Lenskart seems to be winning. Similarly, Pepperfry seems to be winning in the furniture space, but this is being challenged by IKEA now,” he adds.

Add to that the low-cost products sold by local players in nearby markets and things get tougher for organised players. High customer acquisition cost (CAC) and low purchasing frequency further pose a strategic challenge to most startups in this segment. According to estimates from a founder in the ecommerce space, the CAC in online furniture retail ranges anywhere between INR 3,000 and INR 7,000, depending on customer location. Moreover, the average order value should be within this price range to realise some value even from a single transaction, experts point out.

“Furniture retailing itself is a unique space compared to other niche retail categories (like fashion, cosmetics or accessories). It is impossible to build a recurring customer base in this segment, and one has to recover the CAC at the first sale itself. Then there is the high logistics cost as multiple orders cannot be clubbed in a single delivery run as you do in other categories,” says an investment banker who advises consumer internet startups and asks not to be identified.

War Of Woods Intensifies

By August 2018, the segment lost its niche label when the Swedish furniture giant IKEA entered India with a 400,000 sq. ft outlet in Hyderabad, which saw an initial investment of INR 1,000 Cr by the company. The global player with more than $27.3 Bn in annual revenues (INR 20,200Cr), worldwide reach and decades of experience rang a warning bell of sorts and compelled the VC-funded Indian startups to ramp up their competitive advantage. In 2018, just months before the build-up to IKEA’s launch, Pepperfry announced a $35 Mn Series E funding, while Urban Ladder picked up $12 Mn. But the latter failed to attract any large investment after that.

By 2019, it was clear to Goel and Srivatsa that the company would have to find an exit as stagnation was building around the late-stage deal ecosystem. The number of late-stage deals dropped significantly after a steep rise in 2017, as pointed out in Inc42 Plus analysis.

A trouble-torn Urban Ladder started to explore an acquisition opportunity from rival Pepperfry in 2019. But it never went beyond the initial talks as there were differences over valuation, two people aware of the development have told Inc42 on condition of anonymity. According to one of them, Urban Ladder had vehemently pushed for an all-cash deal, but Pepperfry’s founders and investors opposed it.

Pepperfry’s cofounder and CEO Ambareesh Murty declined to comment on the story when we reached out. Urban Ladder’s CEO Ashish Goel is yet to respond to an email seeking comments.

In April 2020, the company found a fresh suitor in RIL and began its six-month-long talks, again pushing for an all-cash buyout, both people quoted above confirmed. At the time, RIL was looking to purchase stakes in several tech startups, especially those who had run out of money or were on the verge of bankruptcy.

“RIL even offered cash to purchase a majority stake in (online grocery) Milkbasket when it was in advanced talks with Urban Ladder, but the Milkbasket deal fell through. Nevertheless, it does seem that RIL is buying out the least-valued companies in the consumer Internet space. Powered by these acquisitions, it may venture into those areas,” says the VC quoted earlier in the story.

Interestingly, RIL or its subsidiaries made quite a few acquisitions in the consumer internet segment before buying Urban Ladder. These included Saavn in the music streaming space, Fynd in fashion and Netmeds in online pharmacy. Urban Ladder is the fourth Kalaari-backed startup which got acquired by RIL apart from Embibe, Zivame and Haptik. But when it came to grocery, RIL said it would build its own brand with JioMart as grocery accounts for nearly 70 per cent of the retail market in India, as pointed out by several analysts in the past.

RIL has, however, retained all the brands it had previously acquired. So, VCs and industry experts believe that the retail behemoth would do the same with Urban Ladder. “Based on what has happened before, these (acquired) companies would operate independently until a future date, after which they will be assimilated into the parent entity,” says Anirudh Damani, Managing Partner at Artha Venture Fund.

According to Anup Jain, Managing Partner at Orios Venture Partners, Urban Ladder does have a brand recall value although the exit to RIL is a consolidation exercise. “Consumers usually buy home appliances and furniture together, and thus, it has a synergy with Reliance digital. One could see a co-location for home appliances and the furniture business to get the best acquisition cost and increase the sale value to recover it faster,” he adds.

What The Distress Sale Means For Dealmakers

Despite the valuation-pricing gap, the acquisition of a startup brand like Urban Ladder by a large retailer is unlikely to affect future dealmaking. Understandably, the startup has sold a majority stake (96 per cent) for a full-cash consideration, signalling that the buyout was solely meant for liquidation and paying back its investors.

“This deal (with RIL) should not become a reference point for the online furniture space. Let us not forget that this deal came at a 75% markdown to the total investment that Urban Ladder raised – not a great advertisement for the segment as the company was widely considered No. 2 in the space (after Pepperfry),” says Damani.

According to the VC quoted first in the story, Urban Ladder’s investors made an average return of around $0.20-0.25 per dollar invested into the company, which is an erosion of their money. But it is highly unlikely to deter future investors in the space in spite of a loss in this case. This is definitely a growing segment and according to market research firm Euromonitor International, India’s indoor furniture market is set to reach $10.7 Bn in 2022.

Going by Urban Ladder’s FY2019 cap table, the promoters (Goel and Srivatsa) currently own 14.2% stake in the company. The rest of the equity is held by its investors, including SAIF Partners, Kalaari Capital, Sequoia Capital and Steadview Capital. They also own the top four slots on the cap table and are likely to get the biggest chunk of the $24.5 Mn exit. Even though these top VCs have seen most of their investments erode, for the founders – Goel and Srivatsa – the exit is still a favourable outcome.

According to Apoorva Ranjan Sharma, cofounder and president of Venture Catalysts, RIL’s acquisition of Urban Ladder does reinforce a potential for growth in the consumer internet space and, more significantly, in the furniture e-retailing segment. “The startup followed the model of converting its sellers into contract manufacturers. There is a lot of scope for growth as India has so many skilled and semi-skilled workers involved in furniture making. Moreover, there is a lot of scope for regional or even specialised players (for office/home/commercial furniture) to grow in this sector,” he adds.

Also, given the fact that a global giant like IKEA has already entered India, RIL’s acquisition of Urban Ladder might well be the first step to take on bigger brands. It may still take some time, though, as RIL has a retail presence in multiple segments instead of a single and more focussed exposure. But furniture retail could be a different ball game as RIL already has indirect control over HomeTown, a home furnishing brand owned by the Future Retail group.

RIL has already acquired a stake worth INR 25,000 Cr in Kishore Biyani-owned Future Retail in August 2020. HomeTown contains the remains of the online retail startup FabFurnish, which was once controlled by Rocket Internet. Biyani’s Future Group acquired FabFurnish for INR 20 Cr in February 2016, but shut it down and merged the brand and the entity with HomeTown in the same year. This does not necessarily mean that ‘Brand Urban Ladder’ will have the same fate as FabFurnish. To start with, the integration of FabFurnish with HomeTown was not a successful strategy. Moreover, Urban Ladder is a familiar name among consumers and, hence, the brand is likely to be retained.

“Reliance is banking on the twin power of its Jio reach and WhatsApp partnership to become the lowest-cost marketing vehicle and thus target consumers in every category of retail – grocery, home appliances, furniture, pharmacy or others. So, it has been buying distressed startups in many sectors,” observes Jain of Orios.

“But there is a big challenge when it comes to integrating multiple companies, all at the same time, and hoping to make behemoths out of them. It will require very powerful execution to beat the best players in each vertical, be it Amazon, Pharmeasy, Pepperfry, IKEA, Flipkart, Croma or Big Basket.”