While paper valuations of Indian startups continue to rise, why are these companies not chasing IPOs?

Dear Reader,

If you are reading this, there is a good chance that you follow startups closely and you would agree that a majority of the news about startups is related to funding announcements. Indian startup ecosystem is peculiar that way, we hear more about investments than exits. While the ecosystem has expanded by a magnitude in the past decade (55K startups launched till date), multi-billion dollar startup exits are a rare sight — highest being Flipkart’s $16 Bn.

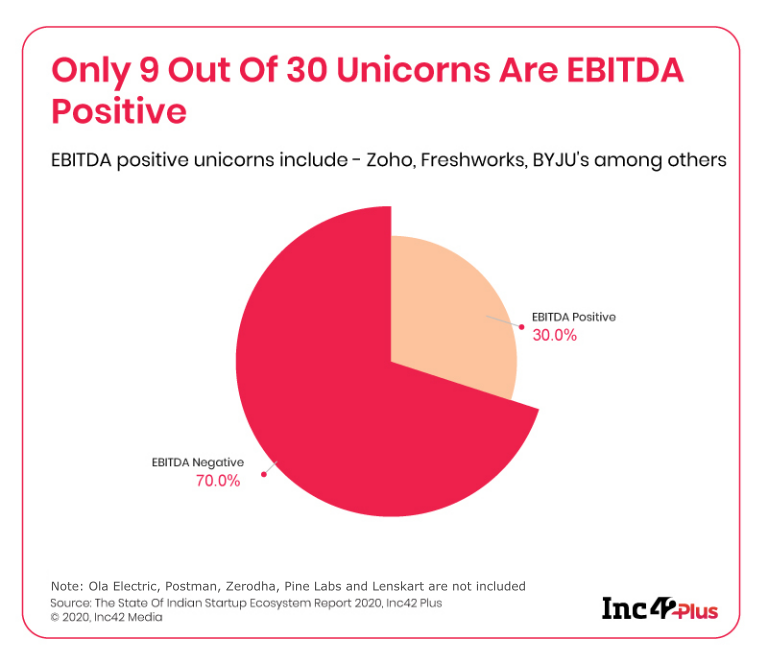

There are about 35 startup unicorns in India and just a handful of them are chasing IPOs. What’s more pressing is that for many, the losses still run in millions of dollars. Out of the 30 major unicorns in India, only nine are EBITDA positive. These include ReNew Power, Zoho, Info Edge, Mu Sigma, BillDesk, BYJU’S, Freshworks, Icertis, and Druva.

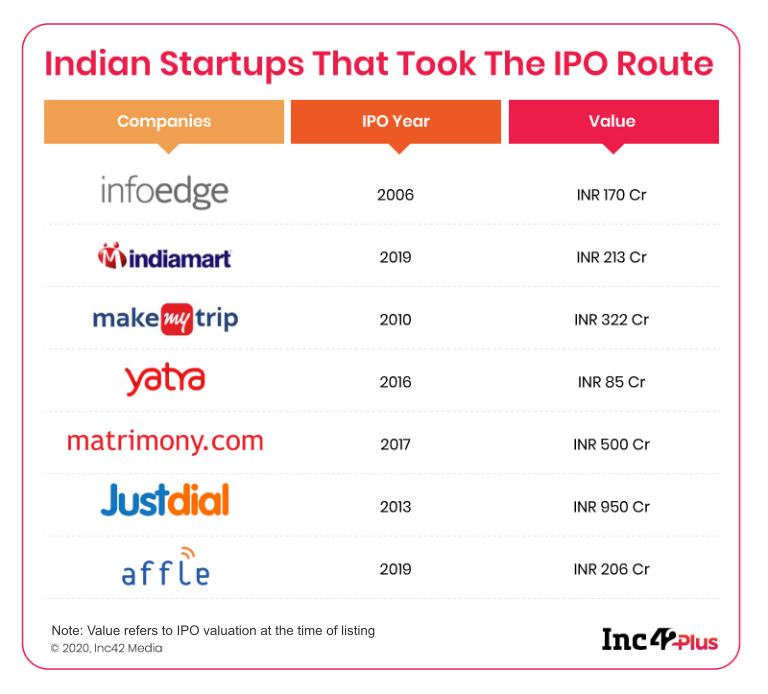

Further, even among the listed tech companies, the list of public startups is short and includes MakeMyTrip, Infoedge, JustDial, InfiBeam, Bharat Matrimony, IndiaMART and Yatra among others. The number of mergers and acquisitions have also hit a record low with 35 M&As reported in the first half of 2020, as compared to 59 M&As in H1 2019 and 52 in H1 2018.

Investor exits through public issues or large buyouts by public companies (also rare) are important analogues for the maturity of a startup ecosystem and also serve as a way for investors to validate their investment decisions.

Analysts say the lack of profitability for many of the biggest startups in the Indian market is a major constraint, which stops them from going public. It is not because startups don’t want to go public — the situation is quite contrary to that.

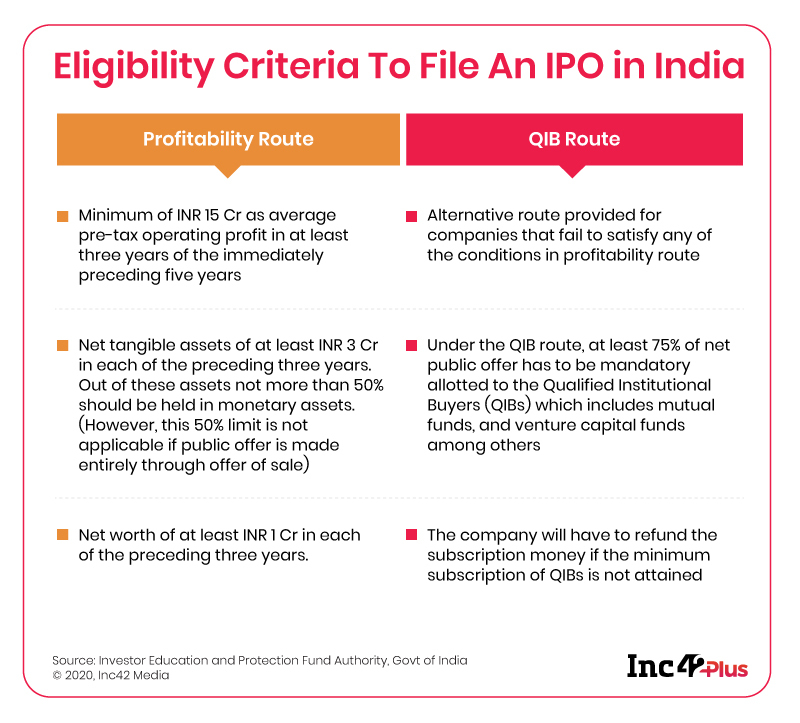

A 2019 survey of Indian startups by the Reserve Bank of India (RBI) concluded that about 58% of 1,246 surveyed startups have plans to get listed on Indian stock exchanges in the next five years. But less than one-fifth (around 250) of the survey respondents had turnovers exceeding INR 1 Cr and a whopping 70% of the respondents were early stage in terms of revenue generation or younger than three years. Which means, only a fraction of the startups would meet the profitability route criteria.

The other option is SEBI’s QIB (Qualified Institutional Buyers) route for companies that don’t meet the profitability criterion. It had capped the public offering to 25%, mandating 75% shares for institutional investors such as mutual funds and SEBI-registered venture capital funds, which can be accessed through other routes as well.

Why IPO When There’s VC?

“Even if startups take the QIB route, the valuation that they get through private investments are much higher than what they would get in an IPO. Because Indian stock market investors are not used to paying high premiums to loss-making entities whereas the startup ecosystem is used to that,” believes Pranjal Kamra, founder of legal and financial services startup Finology.

He added that once these companies are in the public domain, their high valuations would be very hard to sustain. The cautionary tales of WeWork’s IPO are a testament to this sentiment and why public market investors have been largely sceptical of investing big in internet companies.

Even Apple, which is the gold standard for a stock market success story from the tech industry, only took off after 2013, growing from $59 to over $500 today, after the company reached an incredible $2 Tn market cap. Having gone public in 1980, Apple showed 33 years of steady growth and maturity before an incredible rocket growth in the latter part of this century.

In India, retail investors do not have similar patience with tech startups and nor have startups been convincing enough with their financial performance to garner such long-term support, even though this is in many ways the golden period for startups.

Given the fact that unicorn startups are able to easily raise funds through prominent VCs, is there even an incentive for these startups to list?

Paytm CEO Vijay Shekhar Sharma famously referred to the company’s SoftBank fundraise as its very own IPO — a “Masa Public Offering or MPO”.

Not Enough Bait To Reel In The Whales

To make it more attractive for startups to pursue a public listing, regulators have made their fair share of effort in easing the listing norms. There are startup-focused NSE and BSE platforms, which also have an option for the companies to shift to the main trading board after one year. But, only six companies have chosen to list themselves on the BSE Startups platform since December 2018 and the total amount of the money raised by these six listed companies is just INR 22.4 Cr or under $3 Mn. In case of NSE Emerge, 200 entities have been listed including SMEs and have raised INR 3,136 Cr (roughly $43 Mn) collectively.

“Even if a startup is listed there, there are hardly any retail investors who would bother taking that route and actually invest, unless it is available on platforms like Zerodha, Groww and others. I think the options offered by both NSE and BSE would need to mature and integrate with these trading platforms, only then it will become a viable option,” Kamra said.

In terms of HNIs investing in startup IPOs, Rajmohan Krishnan, principal founder and MD of Entrust Family Office reckons that 90% HNIs don’t prefer to invest in listed startups. He added that there is a need for more startup exits to increase the HNI confidence in the startup ecosystem.

The Lure Of A Foreign IPO

While existing laws in India do not allow direct listing of Indian companies in overseas stock exchanges, many companies have set up parent entities in Singapore, Mauritius, the US and other countries to be eligible for a foreign listing. There is also the option of accessing foreign capital through the American Depository Receipts (ADR)/Global Depository Receipts (GDR) route, which has been used by companies like Reliance Industries and Infosys.

But in March this year, amendments to the Companies Act proposed allowing direct overseas listing of Indian companies among other changes. This is the green signal for many startups in India that may not have registered entities overseas.

Sequoia Capital India Managing Director Rajan Anandan believes the proposed legislation to permit tech startups to list on overseas exchanges would be a gamechanger, as it will put many Indian companies on the global map. They will have access to deeper and more diversified pools of capital.

“It should not be mandatory for companies to also list in India. That would make the scheme a non-starter because of the way different exchanges value companies, putting Indian companies at a disadvantage vs offshore companies and creating a non-level playing field,” Sequoia MD Anandan told Inc42.

Further, Inc42 Plus analysis shows that Indian tech startups prefer countries with technologically-advanced markets as well as tech-aware investors such as the US or Singapore over India for listing. Being the biggest tech hub in the world and home to Silicon Valley, the US stock market brings them more visibility and a bigger chance of winning international markets.

Even among the few Indian startups who chose the IPO route, companies like MakeMyTrip and Yatra are listed in the US on the NASDAQ. Auto rental platform Drivezy has shared plans to list on the New York Stock Exchange or Tokyo Stock Exchange.

PolicyBazaar cofounder Yashish Dahiya has also indicated interest in going for a dual listing if the rules regarding overseas listing are ratified. The company has shared plans to issue its initial public offering (IPO) in September 2021 and is preferring Mumbai as its listing location.

Rachit Chawla, CEO of lending platform Finway and a SEBI-registered financial advisor, argued that overseas listing gives startups access to global investors and also makes exits easier for the existing investors who are usually from these global markets. Drivezy also said that since most of their investors are from the US and Japan, listing in India is not attractive enough.

While there are obvious benefits of listing overseas, the argument in favour of an Indian IPO is that Indian retail investors are already familiar with homegrown startups as consumers. For example, a company like Matrimoney.com will have a hard time convincing US investors the importance of matchmaking services and arranged marriage — try as Netflix might. But Indian retail investors already know it and understand its value.

“It’s a big benefit to list in a geography that understands your business model rather than going to another country and trying to explain to them what you do,” said Sreedhar Prasad of KPMG India.

Balancing overseas listings with the prevalent nationalist sentiment in India is like a tightrope walk. Companies and even celebrities are being increasingly criticised for connections with international investors. Ever since the Chinese app ban, people have begun questioning the Indianness of companies by looking at the cap table and there’s already several lists of such ‘pariah’ companies being circulated on WhatsApp, Facebook and Twitter.

So what happens when these companies actually go and list in the US, which just might resume trade with China if a new administration is voted in in November this year. Will India’s Atmanirbhar brigade (aka the retail investors) support such startups in the market?

The Economic Riddle

India’s changing market sentiments towards China and its new foreign direct investment rules could not have come at a worse time. Given the current economic climate, these rules have started to impact deal flow in Indian startups as many feared. Chinese tech giant Alibaba Group is reportedly planning to pause further investments into Indian startups and businesses. The Chinese conglomerate and its subsidiaries have invested more than $2 Bn in India backing startups such as Zomato, Paytm, Snapdeal, Bigbasket, Xpressbees and others.

Alibaba, which is incidentally in the process of filing its IPO, said in the prospectus this week that it holds 30.33% (nearly a third) stake in Paytm and 25% stake in food delivery unicorn Zomato through its subsidiaries. If Alibaba pauses investments in the Indian market, it would set a precedent for smaller investors to follow suit with one of the largest startup investors in China. It could prove to be a major — and in many cases, fatal — blow for Indian startups.

If the international investor pool shrinks, it would only make matters worse for companies who are already going through the worst economic cycle ever. Previously high-flying mobility startups are reeling from the impact. Around 2 Lakh Ola and Uber drivers are now planning to go on strike from September 1 over fare hikes, increase in commissions charged by the aggregators and seeking extension on the moratorium for repayment of loans.

The D2C Riddle

We don’t know yet how the current situation and the anti-China rhetoric will pan out over the next couple of months, but when it comes to homegrown alternatives in the consumer market, Indians are spoilt for choice these days. The direct-to-consumer (D2C) revolution has brought unique products with strong brand narratives, born out of vertical integration and the adoption has also been quite promising. The average revenue surge between 2018 and 2019 for 11 prominent D2C startups including The Man Company, Yoga Bar, NUA, The Moms Co and others was 213%.

Amid the pandemic, even brands that have traditionally been retail-focussed such as Havells, Cornitos, Kiehl’s, LG and even Apple have strengthened their online presence — native as well as marketplace — and embraced the latest engagement solutions and UI/UX standards to drive sales and loyalty.

Innovative and personalised marketing, discounts and quick delivery are the critical factors that drive the ecommerce industry today and that’s exactly what D2C brands are riding on. In particular, food brands have tied up with high-visibility online grocery apps such as Bigbasket or Grofers, and even hyperlocal players such as Dunzo, while for beauty and grooming products Nykaa, Myntra, Flipkart and Amazon help extend reach.

Further, integrating influencer marketing into the overall digital marketing strategy has helped many D2C brands build credibility, target wider audiences and improve brand recall. With millennials demanding brands rooted in purpose, the new-age brands are also going beyond marketing gimmicks and focus on delivering a product with a purpose and conveying the same in its overall marketing strategy.

Despite the long-term vision of most brands being autonomy in operations and vertical integration, success as a pure-play D2C brand remains elusive given the peculiarities of the Indian market — take a tour of the vibrant D2C segment covering almost every aspect of the ongoing D2C Rush in India.

More than anything India’s D2C brands are showing that there is a way to win the Indian market without heavy cash burn. It’s not uncommon for businesses that are just starting out to unearth creative ways of being sustainable. When startups grow big and achieve the scale that many of India’s largest unicorns operate on, this creativity is often focussed on aspects other than sustainability. But it’s time for many of India’s unicorns to revisit their early days and revive the creative fire to take the logical next step of IPOs (in the Indian market) in their journey.

Until The Markets Close Next Week,

Yatti Soni

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/featured.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/academy.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/reports.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/perks5.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/perks6.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/perks4.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/perks3.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/perks2.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/perks1.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/readers-svg.svg)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/twitter5.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/twitter4.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/twitter3.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/twitter2.png)

![[The Outline By Inc42 Plus] Indian Startup IPOs – Still A Pipe Dream?-Inc42 Media](https://asset.inc42.com/2023/09/twitter1.png)