Is India’s national digital health ID programme enough to solve the healthcare access hurdles?

Hey,

Looking back at 2020 a few years down the line (and let’s face it, there will be a lot of looking back at this watershed year), one may remember Covid-19 as a life-changing moment. For many, it has brought on realisations and epiphanies about the uncertainty in life. What seemed like a year that could kickstart the next phase of Indian tech has turned out to be a year full of introspection, tough calls and adjusting visions.

In this (future) nostalgia, one might be forgiven for overlooking something that is likely to become an ubiquitous part of everyday lives in India in the next half a decade. On August 15, 2020 — India’s 74th Independence Day — Prime Minister Narendra Modi launched digital health IDs for all Indians, which is envisioned as a single touchpoint to access healthcare services in India in the future.

The digital health IDs can be best understood as UPI for healthcare — digitally encapsulating all records and history of an individual’s health and wellness. This includes prescriptions, treatment, diagnostic reports and discharge summaries. These digital records can then be shared by individuals with doctors and healthcare providers in hospitals or clinics. It is an utopian image of holistic healthcare, success of which will depend on various factors such as proper implementation and coordination between all stakeholders.

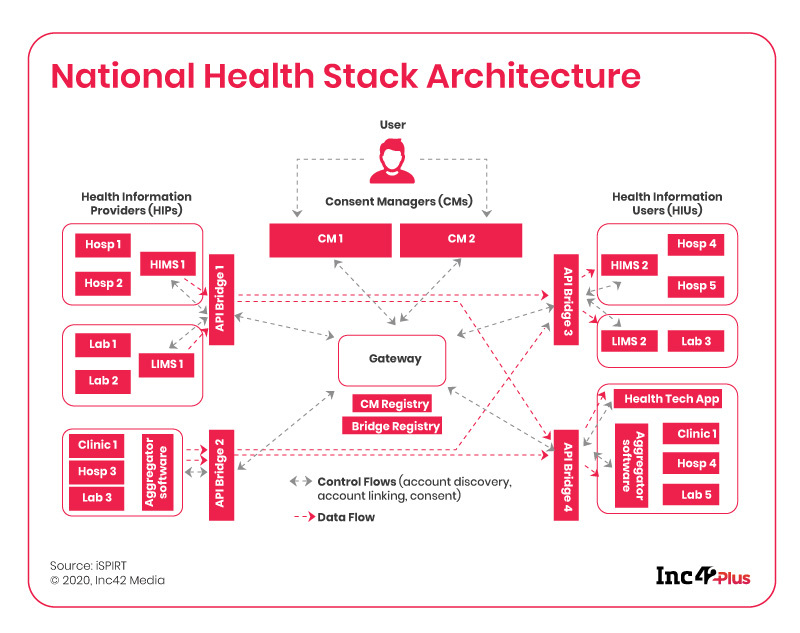

To create this health ID, Indians will have to provide personal and demographic data as well as contact information to a healthcare consent manager. These consent managers will be the facilitators of data flowing between patients and other entities like hospitals, doctors, labs or insurance companies. Multiple consent managers are expected to be available for patients, similar to how payment platforms such as Google Pay, PhonePe and BharatPe manage UPI transactions.

Closely linked to the National Health Stack, which is considered to be the consent layer for healthtech, the National Digital Health Mission (NDHM) already has over a dozen companies and organisations working together, including 1mg, Practo, mfine, National Cancer Grid, LiveHealth, DRiefcase etc.

Further, the NDHM envisions a health registry as a master repository of all the entities in the healthcare ecosystem, including doctors, hospitals, clinics, laboratories, pharmacies, and insurance companies. A pilot was launched earlier this week in select union territories, and startups are already working within the framework to come up with products and services.

The Dream That Is Digital Health

While the NDHM is undoubtedly going to help improve healthcare infrastructure and penetration, one of the biggest impacts will be seen in the emergence of new models within the healthtech ecosystem. Building a teleconsultation service is no longer a novel idea, but onboarding specialist doctors and healthcare providers is a major challenge for healthtech companies.

Every startup has devised their innovative way to crack this acquisition formula — while some have collaborated with hospital chains, others depend on a network of pharmacies and specialised hardware as key differentiation. With the launch of NDHM, healthtech startups expect cross-functional collaborations to become easier and automated.

Telemedicine and healthcare content startup myUpchar cofounder and CEO Rajat Garg believes the biggest gap is patient medical history, which NDHM will solve at the grassroot level.

“Most of the time, users do not provide that history completely. So by having such a system in place, you suddenly have the ability to fetch the patient’s medical history from wherever and that’s a very big plus in our view,” Garg told Inc42.

According to Medcords cofounder Shreyans Mehta, the announcement of NDHM alone will inspire a 5X-10X growth in its business. Pune-based Medcords is a telemedicine startup which is also digitising pharmacies in Tier 2 and Tier 3 markets. Other companies also expect the digital health policy to create collaboration opportunities in spaces such as health insurance and advanced healthcare.

Of course, with so much data at stake, there’s always the question of data privacy and security breaches. Indian government systems have not been known to be the most robust in terms of cybersecurity and with healthcare data, the threat is much more critical. The Internet Freedom Foundation’s (IFF) Apar Gupta cautioned that business collaborations with health insurance companies in the absence of clear legal regulation or data protection law can result in function or feature creep. The term is used to define a situation where data is collected for one purpose but is eventually used for a completely different use case.

Hence, it is necessary for the upcoming personal and non-personal data protection laws (pending before parliamentary committees) to provide for appropriate protection through legislation. IFF’s Gupta added that these business collaborations and opportunities will have a more ideal outcome if they are done in a sandbox model where there is a clear legal regulation. This will enable startups to forge real trust between the service provider and consumers.

Maturity Moment For Healthtech

“Better adoption of digital practises will help us to make faster inroads on the supply side and with the patient’s data being easily accessible will significantly improve triaging capabilities of our AI system,” mfine cofounder Ashutosh Lawania.

Even before the NDHM was announced, the buzz around healthtech in the light of the Covid-19 pandemic had brought in tech giants such as Reliance Jio and Amazon into the healthtech space. But it’s hundreds of Indian startups that stand to benefit the most from this data-forward healthcare ecosystem.

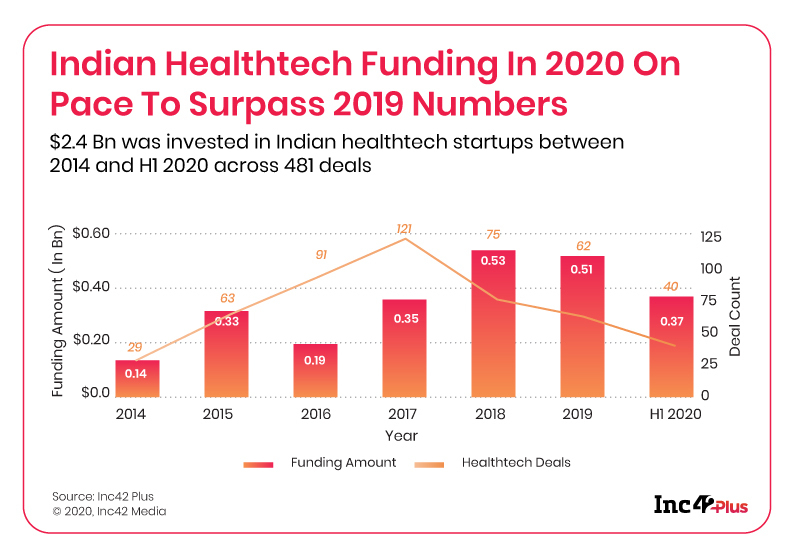

Inc42 Plus estimates that there are 311 funded healthtech startups in India, but so far, due to the peculiar nature of the Indian market, these startups have primarily been in telemedicine, doctor discovery or epharmacy space. With the NDHM, newer and more innovative models are expected to get encouragement through policy, if not through market demand.

Startups such as Blume-backed BeatO were already differentiating themselves in the teleconsultation space by closely integrating hardware solutions to provide advanced healthcare services. The Delhi-based startup’s Made-in-India blood glucose monitor collects and transmits real-time health data to smartphones. It is working on similar innovation for blood pressure and more vital stats. Having centralised data to create treatment plans for patients will be critical for these solutions.

Similarly, Bengaluru-based mfine is also working on integrating innovations like digital collection of vitals, deciphering the type of infection based on cough sounds, blood sugar readings and more. BeatO cofounder Gautam Chopra agreed that connected hardware innovations is the next level of innovations to happen in the healthtech sector. Once India solves the problem of access to authentic and reliable health data, advancement in AI triaging and machine-aided diagnosis will be possible.

He also noted that the success of these innovations will depend on how closely they are integrated with the AI driven app ecosystem because the real value of any such system lies in the real-time delivery of care. Other AI-based innovations like predictive analytics in diagnosis are also expected to grow in the sector. For instance, myUpchar is working on an AI algorithm to fast-track teleconsultations.

Healthcare being a service-intensive space, companies are also betting on their established network and customer trust to distinguish themselves in the crowded market. So, even though the user data will become interoperable, ultimately factors like service quality, speed of delivery, pricing will drive the user adoption of a platform. It is unlikely that doctors will collaborate with 50 different apps and platforms, and thus the quality of the product and the revenue-sharing potential will be a major differentiator for startups.

But before we look at such mature questions, the policy has to be successfully deployed. The major portion of the healthcare ecosystem still consists of aging hospitals, offline labs, pharmacies and small clinics. It is no small feat to be able to digitise the myriad of healthcare providers in the country. Startups also noted that health is a state subject and there is a possibility that the central government could face trouble in encouraging people to adopt a digital mechanism.

Aayush Rathi, policy officer at the Centre for Internet and Society (CIS), agreed that the National Health Authority will be tasked with coordination efforts.

“The NDHM is a little different from previous health initiatives as centralisation of data is a core element of the mission. Most successful welfare initiatives tend to accord state greater agency in their adoption implementation,” Rathi told Inc42.

Is Digitisation The Only Answer?

“The National Digital Health Mission aims to liberate citizens from the challenges of finding the right doctors, seeking an appointment with them, payment of consultation fee, making several rounds of hospitals for prescription sheets,” National Health Authority said in a statement. But can digitisation alone fill the infrastructure and funding gaps in the Indian healthcare system?

CIS’s Rathi added that such health digitisation efforts tend to internalise the ideologies of tech-centricity, which is assuming that the mere use of technological tools will solve underlying structural issues.

“With an already underfunded and overworked public health system such as in India, it is entirely possible that resources spent on these systems could set us several steps back. The now-discontinued National Programme for IT (NPfIT) in the UK is a great example of similar global efforts,” he added.

BeatO’s Chopra added that it’s a vital first step, but the overall spending needs to be ramped up. “It is a good development that India is thinking about building a National Health Stack but still investment in healthcare infrastructure is key. Covid has been an eye opener and we need to start thinking of investing much more in healthcare. We can’t remain at a total public (centre and state) expenditure on healthcare of just 1.29% of GDP,” Chopra said.

While there is tremendous excitement around building digital infrastructure and local innovations, we cannot lose sight of the core issues in Indian healthcare sector — underfunding and lack of capacity. The government healthcare expenditure (GHE) of India was a little over 1% of the total GDP, according to the National Health Account (2015-16), one of the lowest in the world.

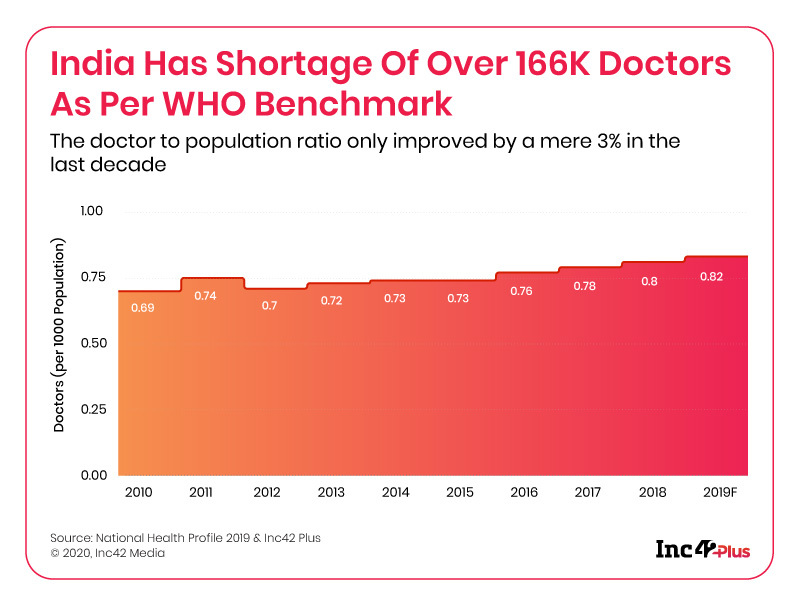

Further, the number of doctors per 1,000 population in India increased from 0.69 in 2010 to 0.82 in 2019, but it is still lower than WHO’s recommendation of one doctor for every 1,000 people. Even in terms of infrastructure, India only has 0.56 beds available for every 1,000 people, as compared to the recommended five beds per 1,000 people.

Digitisation definitely has the potential to serve as a good supplement for lack of access in healthcare and data repositories might help in optimising resources to an extent but all these tech innovations cannot replace the need for infrastructure and healthcare professionals.

Big Tech’s Healthcare Moment

Ever since the Covid-19 pandemic broke out, healthtech has earned its spot as an essential sector in the Indian tech industry. 1mg’s Prashant Tandon has even called Covid-19 and the ensuing investments the demonetisation moment for healthtech in India. When heavyweight players like Reliance and Amazon decide to enter the sector, the writing is on the wall.

Just this week, Reliance Retail acquired a 60% stake in epharmacy startup Netmeds for $83 Mn and Amazon launched its pharmacy delivery service. Further, Flipkart is also looking to enter the epharmacy space through a potential partnership or investment in PharmEasy. The moves by these tech giants indicates that India may soon release the much-awaited epharmacy guidelines to bring sector clarity.

Meanwhile, global social media giants continue to face scrutiny in India. A recent report by Wall Street Journal alleged Facebook of preventing takedowns of hate speech content posted by members of India’s ruling BJP, even if it conflicted with the company’s community guidelines on hate speech.

Facebook has now been summoned by the parliamentary standing committee on information technology to discuss on the subject of “safeguarding citizens” rights and prevention of misuse of social/online news media platforms. The Shashi Tharoor-led panel has set September 2 as the date for this hearing.

And on the topic of tech controversies, the anti-China sentiment in India rages on Chinese smartphone brand Vivo was replaced by Indian fantasy sports platform Dream11 as the title sponsor for the Indian Premier League’s (IPL) 2020 edition. But given Dream11’s investors (Tencent from China) does this mean brand IPL is beyond the call to curb Chinese tech investments in India?

India’s Digitisation Moment

As Reliance makes another startup acquisition, here’s taking a look at the company’s ever-expanding ecosystem. Reliance ventured into tech-dominant businesses with the acquisition of startups such as Haptik, Embibe, C-Square, Fynd, Grab, Netradyne, Tesseract and others.

After the company’s 43rd virtual AGM, we had noted that Jio might not tick-off requirements for being a startup, but it definitely is a kingmaker for startups. Clearly, Jio apps have made their footprints in several categories but there is a long journey to travel.

Jio Platforms is bringing a lot of drastic changes in the sectors where it has entered and is looking to change the cost dynamics of entire industries with its free offerings. In that sense, it is relying on the playbook that earned Jio its success and growing revenue.

It’s not just Reliance, the digitisation wave in India has changed things for many traditional businesses in India. And so has been there attempts to capture larger audiences. After the pandemic, 100% offline brands such as Havells, Cornitos, Kiehl’s have strengthened their online presence, embraced the latest engagement solutions and UI/UX standards to drive sales and loyalty.

From retail presence and traditional distribution, direct-to-consumer (D2C) is fast becoming the new buzzword for brands in India’s storied consumer products and goods market. Over the past few years, even traditional businesses have had to rethink their approach to selling. And if many brands were on the fence in the past, the pandemic has well and truly pushed them on to the D2C corner.

For most brands, pursuing an ecommerce strategy was not just an option, but absolutely crucial. Will the entry of valuable primarily-offline brands with huge capital be a threat to D2C startups?

The movement of heavyweight players in the startup space is not specific to just D2C segment, healthcare too is seeing a major interest from traditional and deep pocketed players. And the answer to the growing competition will eventually be found in how clearly startups differentiate themselves in terms of service quality.

Stay Safe, Stay Healthy

Yatti Soni