Ola Electric has pivoted to become a full-stack electric scooter OEM, but a recent acquisition in the Netherlands comes back to haunt it

Netherlands-based Etergo, which was acquired by Ola in a distress sale to give wings to the Indian company’s EV dream, has angered its minority investors due to discriminatory share buyback

European investors are crying foul and preparing to take Etergo and its parent company Ola to court; did Ola’s due diligence team fail to deliver?

When Ola Electric, the EV arm of the ride-sharing unicorn Ola (ANI Technologies), announced in May 2020 that it would start operating as a full-stack manufacturer of electric two-wheelers (2W), the euphoria was palpable. News reports claim that Ola Electric is deliberating with electric vehicle (EV) equipment manufacturers and also holding talks with several state governments to set up a 100-acre manufacturing unit, with a production capacity of 1 million scooters a year. Initially, these two-wheelers are expected to be manufactured in the Netherlands. And Ola is reportedly planning to ship these to European markets and India in the early months of 2021.

These developments at Ola Electric may seem promising, but behind it lies an acquisition it made recently in the Netherlands, which is a tale of multiple hits and misses, an erosion of (minority) investors’ wealth and trust, and an alleged charge of defrauding that may soon reach a court of law. Did Ola conduct its due diligence before grabbing the EV firm? But before we go into that, let us look at the beginning of the whole saga. (more on this later).

It all started with Ola’s acquisition of the Amsterdam-based EV startup Etergo BV, which had to undergo a fire sale or face bankruptcy. In May 2020, Ola Electric announced the buyout for an undisclosed amount. Now the Indian unicorn plans to utilise Etergo’s App Scooter design and engineering capabilities to build a smart electric two-wheeler.

The backstory, however, is quite grim. Lauded as the ‘Tesla of e-scooters’ by the European and Dutch media, Etergo was a crowdfunded initiative that raised millions of euros in two crowdfunding rounds. But after raising around €21 Mn ($24.8 Mn) in equity financing from more than 6,000 individual investors (most of them were carried away by the e-scooter craze), the company got sold to Ola Electric for €3.75 Mn ($4.44 Mn) valuation, according to internal emails and multiple Etergo investors who spoke to Inc42.

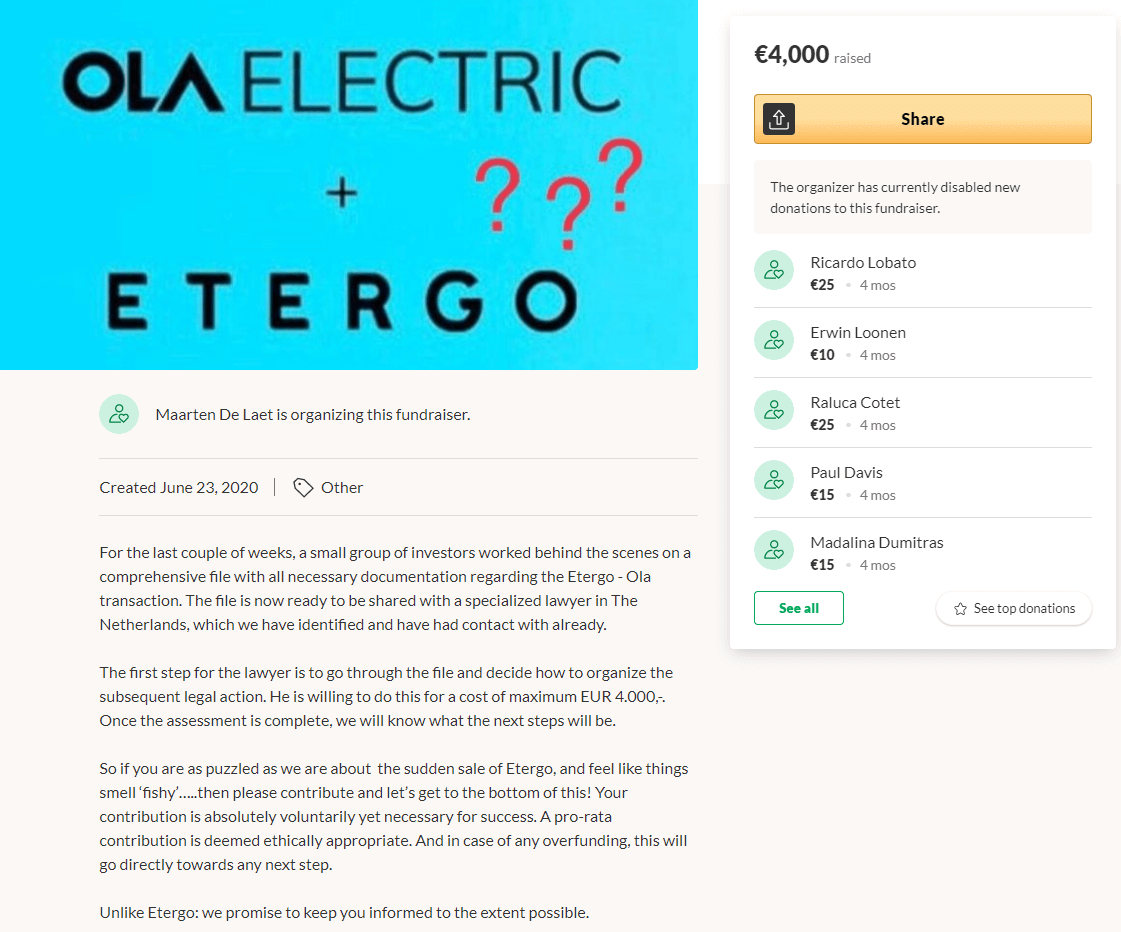

More than 900 investors who put their money into Etergo through crowdfunding campaigns are now in the process of filing a lawsuit in a European court to recover their money from Etergo and its current owner Ola Electric. Inc42 spoke to at least five such investors who have invested €2,000-5,000, but now getting back barely 10% of their original investments. Many of them have held onto their shares since 2017, hoping to get their hands on the swanky App Scooters promised by Etergo.

Angered by the breach of promise, some of these investors have started their own crowdfunding campaign on GoFundMe to pay for a lawsuit that might be filed before the end of the current calendar year. Also, some of them have joined a Facebook group that keeps buzzing with ideas and legal suggestions on how to recover their money.

What Went Wrong At Etergo

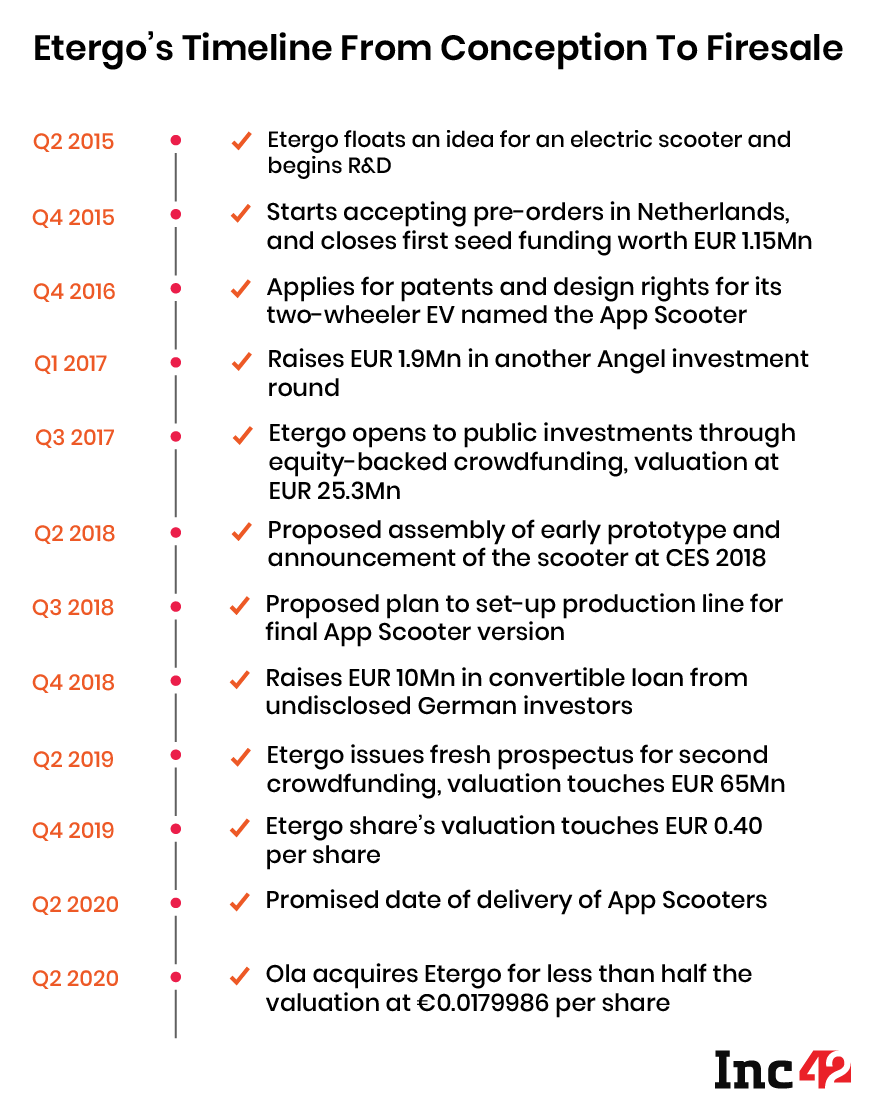

Founded in 2014 by Bart Jacobsz Rosier and Marijn Flipse, Etergo had conceptualised an all-electric state-of-the-art AppScooter that depends on battery-swapping for a quick recharge and an increased run time. Unveiled in 2018, the AppScooter claims to use high-power energy density batteries to deliver a range up to 240 km and quick acceleration. But according to two investors aware of Etergo’s operations in the Netherlands, even after three years of research and development since 2015, not a single scooter was delivered to people who purchased actual shares in the company via a pseudo-public offering. This fundraising vehicle can be used by any private company in Europe.

In the Netherlands, the government allows private firms to set up STAKs (Stichting Administratiekantoor) or an Administration Office Foundation to help companies raise equity funding by issuing shares. Etergo BV diluted around 10% equity stake in September 2017 and set up a STAK with targeted funding of €1.5 Mn ($1.7Mn), which was also its first publicly raised money. Etergo used Seedrs, a platform that allows European retail investors to buy shares in private companies.

In fact, it is similar to GoFundMe, but only startups can use the platform to raise money from investors, and the latter will own an equity stake in the company. The Seedrs page for Etergo is still live and indicates that the scooter was supposed to go into production by Q2 2018. The Seedrs crowdfunding campaign was a massive success for the founders as it seemingly overshot the original target and amassed a total of €3.2 Mn, valuing the company at more than €25 Mn.

“Although the first public funding (crowdfunding) happened via Seedrs, the owners of the company later used their own website to gather and raise funds, as they started getting momentum for their brand… Everything was fine until late 2019, and I got some email from the (investor relations) team promising that the scooter would be delivered by March 2020, and then suddenly it was sold to an Indian company by May 2020, and none of us got any such heads, and I learnt from the news itself,” says an Amsterdam-based investor who picked up shares worth €5,000 in Etergo in 2017. The investor does not wish to be identified.

A copy of the prospectus issued by the company and reviewed by Inc42 reveals that Etergo was valued at north of €65 Mn in March 2019. This was more than double the valuation the company had in 2017, during its first crowdfunding campaign. Before the end of 2019, its share was reportedly priced at €0.40. But after the buyout, the per-share price came down to €0.0179986, according to emails sent to Etergo investors in May 2020. It essentially means investors lost nearly 90% of their original investments.

The email also mentioned that they might redeem their shares at €0.0179986 per unit, which according to Inc42’s estimates, values Etergo at around €3.75 Mn after the Ola buyout. The shareholders with whom Inc42 spoke also point out that they are now being forced to redeem their shares, and they do not have an option to renegotiate the price.

According to the email exchanges between Etergo and two different shareholders, which have been reviewed by Inc42, the Dutch startup has also stated that investors do not have an option to hold onto their shares or convert those into equity shareholding in Ola Electric.

“The company (Etergo) let itself be tied into a negotiation with a potential investor that waited until the cash ran out to pick up the pieces out of the rubble for near to nothing. And (the) management is retained and properly incentivised for the next run. So, early investors lost nearly all,” says one of the early investors mentioned above.

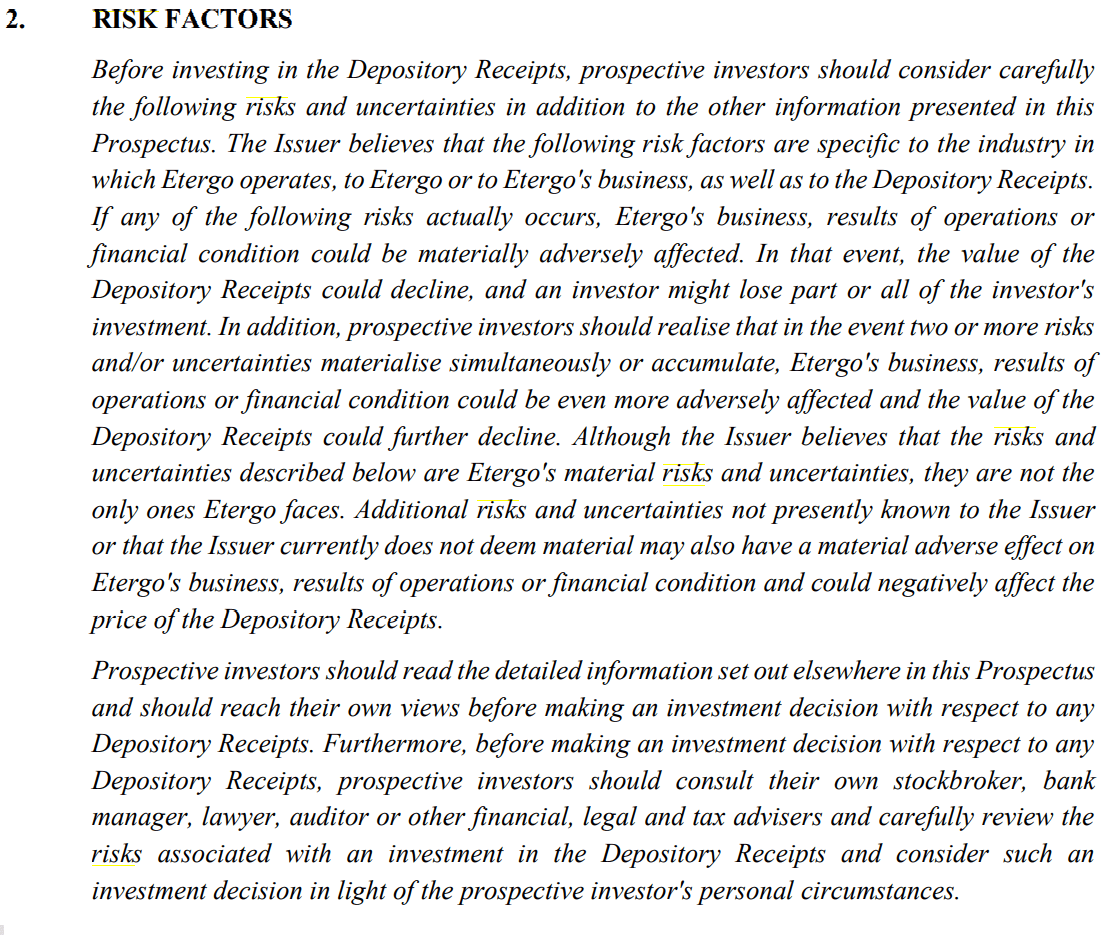

Before Etergo conducted its second crowdfunding campaign in March 2019, its investment prospectus clearly laid at least 10 pages of “risk factors” due to which the share price could be affected leading to erosion of the original investment value. These included market, financial, and technological risks. However, the 6,000 lot of investors who placed their trust on the Etergo brand probably didn’t expect an acquisition to wipe out their share value.

Inc42 has also reviewed several email exchanges between retail investors and an email by Etergo. The latter clearly states that the shareholders who purchased equity in Etergo via the STAK structure are minority shareholders. Hence, they do not have any say on the acquisition.

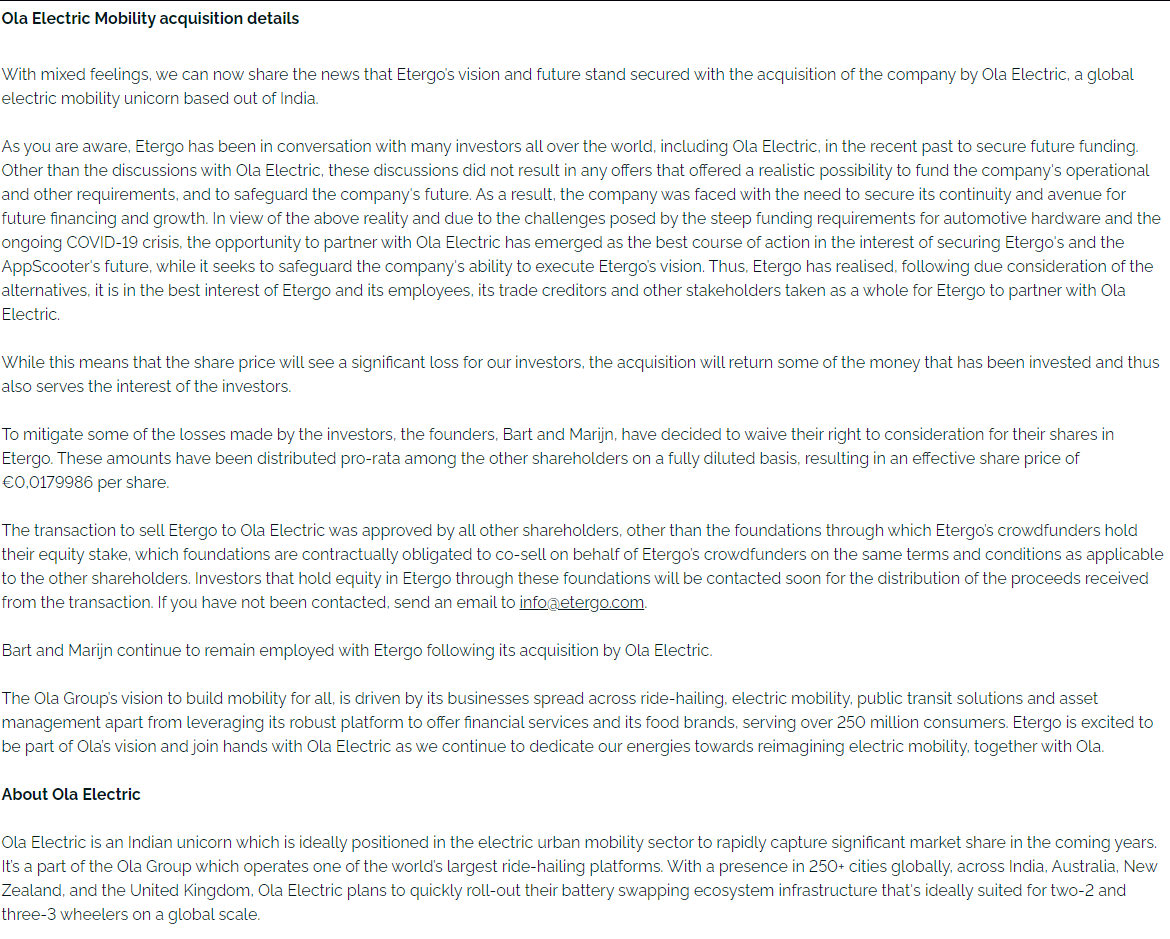

“…It is important to note that Stichting Administratiekantoor Eterrgo II (STAK), as a minority shareholder, was not in a position to help negotiate a higher purchase price. It is OLA who made the final offer which was formally approved by the shareholders to prevent bankruptcy. The STAK had no other option but to participate in the transaction…The shares have been transferred to OLA. It is OLA who paid the STAK and other shareholders the purchase price of €0 .0179986 per share,” reads another email sent to one of the investors who purchased shares in Etergo through crowdfunding.

The email further mentions that cofounders Rosier and Flipse have decided to waive their right to consideration for their shares in Etergo. It means the cofounders have waived their shares in Etergo and distributed those in the STAK pool — the entity that holds the stake of the minority shareholders.

“To mitigate some of the losses made by the investors, the founders, Rosier and Flipse, have decided to waive their right to consideration for their shares in Etergo. These amounts have been distributed pro-rata among other shareholders on a fully diluted basis, resulting in an effective share price of €0.0179986 per share,” states the earlier May 2020 email sent to investors.

Will Etergo’s Investors Weigh Heavily On Ola?

Even as Etergo is at loggerheads with its minority investors, it is important to ask: Who wins this game? A Dutch startup that spent three years of engineering and development efforts and marketing and sold its entire shareholding to Ola Electric for 6% of its original valuation of €65 Mn? Or is it Ola that had gone window-shopping in Europe and returned to India with a cheap deal?

The Bhavish Aggarwal-led company has just been handed over an e-scooter prototype ready to go for manufacturing on a boilerplate, and according to its statements to the Press, Etergo founders, Rosier and Flipse, will continue to work under Ola’s management. However, it is still not clear if an actual e-scooter will hit the market within the stipulated time frame. Ola declined to comment on a questionnaire sent by Inc42.

According to a senior partner at a Netherlands-based venture capital firm, who is aware of Etergo’s operations, the startup was looking for a buyer since the beginning of 2020, especially after the App Scooter’s certification from automobile regulators was delayed. “The firm spent most of its money on getting its prototype right. But it fell short of cash when it was production time, and hence, had to shop for a buyer. By then (early 2020), the Covid-19 pandemic was sweeping through Europe and selling the company at the right price turned out to be an impossible task,” he tells Inc42, requesting anonymity. His VC firm has also made several investments in the mobility sector across the European Union.

“What has happened at Etergo mostly happens when too many investors put in their money via crowdfunding,” he adds. “These investors did not understand all the business risks involved and only hoped they would be the first ones to get the App Scooters. But with the ‘upcoming’ lawsuit in Europe, Ola may not want to deal with the regulators there. So, the company has rushed to pay the money back to investors, especially as the deal looks like a sale to prevent bankruptcy,” he said.

Etergo already had a pre-money valuation during its two crowdfunding rounds. But when Ola acquired the company, the same retail investors who took part in the crowdfunding rounds were forced to sell back their shares at a lower price. It has happened because the people who purchased shares via the STAK system do not have voting rights. Hence, the decision made by the majority shareholders – founders and promoters – becomes final.

“These investors (who purchased shares via crowdfunding) are basically minority shareholders, making up less than 25% of the company. Usually, in a buyout, to prevent bankruptcy as seen in the Ola-Etergo case, the minority shareholders directly follow the decisions of majority shareholders and have no say in the acquisition. It also means these minority shareholders cannot block the Ola-Etergo transaction or negotiate a new price, unlike the public stock market. As Etergo could not deliver a single scooter in the past three years, the value of the company is going down. So, the value of its shares is also erased,” the VC mentioned above adds.

“If you are making an acquisition where there are minority shareholders, they should get the same price per share just like the majority shareholders even under the STAK model. However, this crowdfunding feature can be misused as STAK shareholders have no voting rights. Whether or not Ola-Etergo misused this clause is subject to a debate,” says a Bengaluru-based lawyer who advises companies on funding and mergers and acquisitions, and does not want to be named.

The Road Ahead For Ola Electric

Although reports in the Indian media claim that Ola Electric is prepared to ship the much-awaited App Scooters to Europe and India by early next year, Etergo’s retail investors, who spoke with Inc42, say the company has not communicated any such plans. In fact, the last email communication (November 2019) to investors mentions that “with the production line being set up, the goal is to manufacture the first batch of early Dutch investor editions in February and then deliver these in March 2020”. But just months after this timeline passed, Etergo became an Ola company.

EV industry experts and analysts further point out that regulatory certification is not the only hurdle Ola will have to face when it sets up its manufacturing unit in India. The company will have to find a way to source Lithium-Ion batteries without depending too heavily on Chinese manufacturers, who are now facing pushback from Indian businesses. Due to the current geopolitical situation, the Indian company is in talks with battery cell manufacturers such as Bosch and Samsung so that it can locally assemble these batteries, according to a Mint report published in September 2020.

“It is true that China governs the majority of the lithium-ion reserves, just like it does in the solar cell segment. But the supply of cells may soon come from places like Taiwan, Japan, Canada, the US, Chile and even Australia. Moreover, Indian companies like Tata Chemicals and Adani are also coming up as cell manufacturers,” says Chinmoy Mallick, Head, M&A and Strategic Alliances, at VSL Ventures that funds startups in the IoT (Internet of Things) and EV segments.

However, Ola Electric is a company that has puzzled many experts and investors. Launched in 2017, it has raised more than $300 Mn and become a unicorn, thanks to two rounds of funding. But as of now, there is no tangible product on the ground. The EV arm started with a pilot in Nagpur in late 2017 with e-rickshaws and their charging points. But the project came to a grinding halt in 2018 due to multiple delays and the drivers concerned returned the vehicles. Despite these issues, the startup has raised equity funding from top investors, including Japanese conglomerate SoftBank, parent company ANI Technologies, Hyundai Kia and Ratan Tata, among others.

However, the steady exodus of cofounders and senior executives does not bode well for the company.

Ankit Jain, a cofounder of Ola Electric, stepped down in August 2020, three months after Ola laid off 1,400 employees as revenues were badly hit by the coronavirus-induced crisis. Another co-founder, Anand Shah, also resigned from Ola Electric in August last year, according to an Economic Times report. Ola Electric’s chief business officer Sanjay Bhan also left in July this year.

Moreover, this is not the first time when Ola has acquired a company for cheap and tried to turn around its operations. In January 2018, Ola acquired Foodpanda India from Germany-based Delivery Hero Group for about $31.7 Mn. The acquisition, which took place in late December 2017, marked Ola’s return to India’s online food aggregation and delivery space after its first attempt Ola Cafe was shut down in March 2016. But after many failed attempts to break into the food delivery and take on UberEats, Foodpanda India was laid to rest just 18 months after the acquisition. And hundreds were laid off.

Etergo’s App Scooter may seem like a done deal. But the target company’s blemished history of fundraising and the upcoming lawsuit by (minority) shareholders in a European court may weigh heavily on the Indian company. In fact, tougher questions must be asked right now before Ola lands into a legal quagmire and loses its reputation globally.

To start with, is Ola aware of Etergo’s handling of its early investors and the discriminatory share pricing to which they are subjected? Did it conduct its due diligence well before lapping up the steal deal? Has the Indian company played any role in the erosion of Etergo shareholders’ wealth? Can it ensure that they get their justified dues as well as the EV two-wheelers promised by the Dutch company? It sounds like a tall order, but a local company’s global dream must live up to global expectations not only in terms of the products it sells but also in terms of business ethics.

Maybe Ola saw this coming, but clearly, there is a lot at stake with this acquisition. The Etergo buyout is probably the only chance for Ola Electric to justify its billion-dollar valuation and deliver to the world. The only caveat here: If success is a journey that is achieved by taking small steps over a period of time, failure, too, is an outcome of small oversights in the wild pursuit of one’s dreams.