Even though startups such as BigBasket have experimented with the dark stores in the past, the model never gained wide traction in India, unlike the West

But the Covid-19 pandemic and the increased focus on on-demand hyperlocal capabilities in the essentials space has made dark stores more viable for startups despite the relatively higher costs

Will India’s hyperlocal delivery players and consumer brands gravitate towards dark stores despite some of the drawbacks to meet consumer demand or will kiranas step in to bridge the gap?

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

The years between 2014 and 2018, can be considered the worst for India’s hyperlocal delivery and logistics startups. The consumer demand for fast and on-demand deliveries had already eaten into the thin margins, and even deep-pocketed players like Grofers, Shadowfax, Peppertap (the B2C business), Local Banya, TownRush, Paytm Zip, Ola Store, Flipkart’s Nearby were retreating from major cities, pivoting to the B2B model or closing the operations.

This was the time when BigBasket first experimented with the dark store model, a concept pioneered by British retail giant and the world’s third-largest retail company Tescos when it started online deliveries. Simply speaking, a dark store is a small neighbourhood warehouse where consumers cannot enter directly and can only order online for a home delivery. Players like Walmart, JCPenney among others have further made it popular in the US with the advent of ecommerce in these regions.

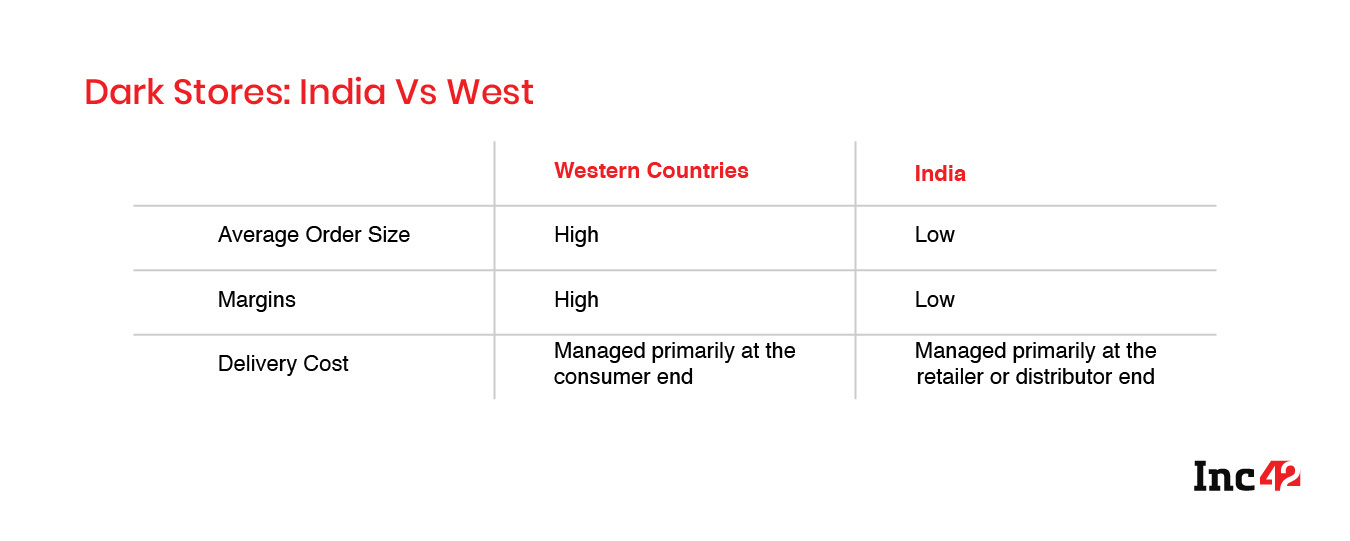

But dark stores need to be seen in a totally different light in India, unlike western markets. As Kushal Nahata, CEO and cofounder of logistics startup FarEye explained, in the west, the supermarkets and department stores at-large serve in a semi-warehouse or dark store for daily order fulfilment. In high-density areas, with high-frequency orders, separate dark store facilities have been installed for faster deliveries.

On the other hand, in India, dark stores have primarily been small warehouses or neighbourhood fulfilment centres serving the objective of on-demand fast deliveries primarily in a D2C (direct to consumer) model.

“At the same time, there is a large network of retail stores across the country, which can actually be used as a dark store facility, rather than creating a parallel supply chain like west,” he added.

The Shift After Covid-19

Dark stores are synonymous with fast and timely deliveries. However, the cost of quick 2-hour or 4-hour delivery through dark stores comes at almost 40% higher cost than traditional slot-based warehouse retail model in India. This makes dark stores difficult to scale for the price-sensitive Indian consumer and business, said Rhitiman Majumder, cofounder and CEO, Pickrr, an end to end tech-enablement service provider for logistics and last-mile delivery players.

The Covid-19 pandemic has created a positive momentum for hyperlocal delivery players serving the essentials segment. While several non-hyperlocal and offline players like Snapdeal, Uber, Domino’s, Quikr, PerPule among others marked their entry in the grocery delivery segment, Dunzo even claimed a 33% higher weekly orders, 2X surge in ticket size when every other player was gasping for revenue.

In line with BigBasket, recently Swiggy launched its dark store pilot ‘Urban Kirana’. The food delivery major has partnered with a number of manufacturers, retailers and B2B grocery players to enable its fulfilment services. It already had Swiggy Stores, which aggregated deliveries from local kirana and department stores.

Then why the move to dark stores? B2B e-commerce platform MaxWholeSale’ founder and CEO Samarth Agrawal says it’s simply because more consumers are looking for options that are not available at the nearest kirana store. In order to take control of inventory, Swiggy is now showcasing its ‘dark store’ warehouse as a store which consumers can directly access on the app for placing orders.

“This way order fulfilment goes up. The purchase orders are raised with the partners on the basis of the last 7 days’ sale, which then refills the dark stores’ inventory on a weekly basis,” Agrawal added.

Also, the timing couldn’t have been better for Swiggy. Due to Covid-19, there has been an aggravated impact on home delivery demand, and consumer behaviour has evolved to look for grocery and essentials rather than cooked meals.

Considering these factors, the delivery costs for dark stores are expected to reduce in proportion to the increasing scale, on the expectation that more and more consumers will be looking for online grocery and quick hyperlocal deliveries.

“This is the most opportunistic time for anyone considering dark stores expansion. We are also expecting the service cost per delivery to be reduced further with deeper penetration of dar stores in the near future,” added Pickrr’s Majumder.

Decoding Dark Stores Viability in India

It would be remiss to assess the long-term viability of dark stores without answering the questions around ownership, maintaining margins, the unit economics, and assessing how they compare to the longstanding traditional warehouse model as well as the kirana stores, which are the lifeblood of hyperlocal retail.

Supply Chain Links

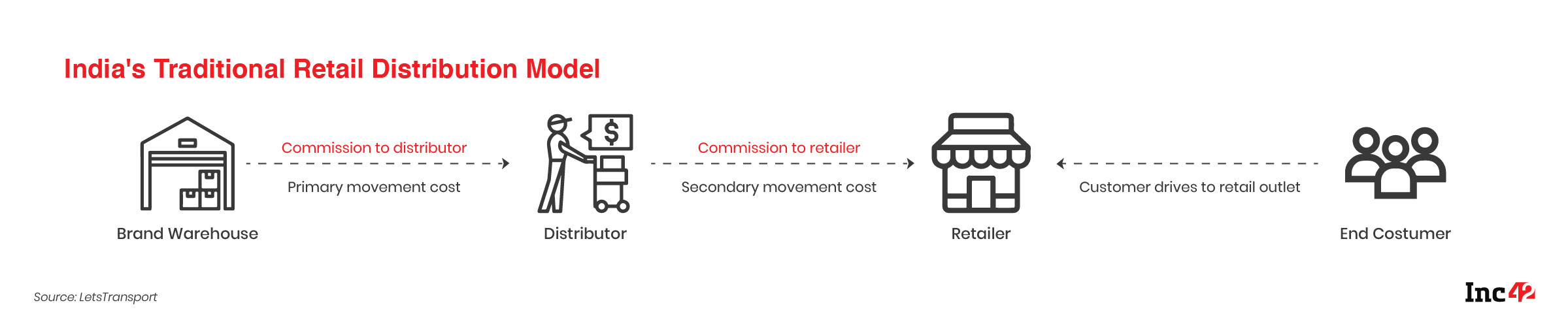

A typical supply chain including traditional warehouse hubs has lower last mile delivery cost, which is assumed by the consumer.

While delivery of goods from warehouse to distributor to retailer might be slow, it’s reasonable to expect a next-day or two-day fulfillment cycle. The same supply chain is applicable for kirana stores too, which receive goods from nearby wholesalers or distributors. Although quick home deliveries are possible through kiranas, this varies from city to city and neighbourhood to neighbourhood.

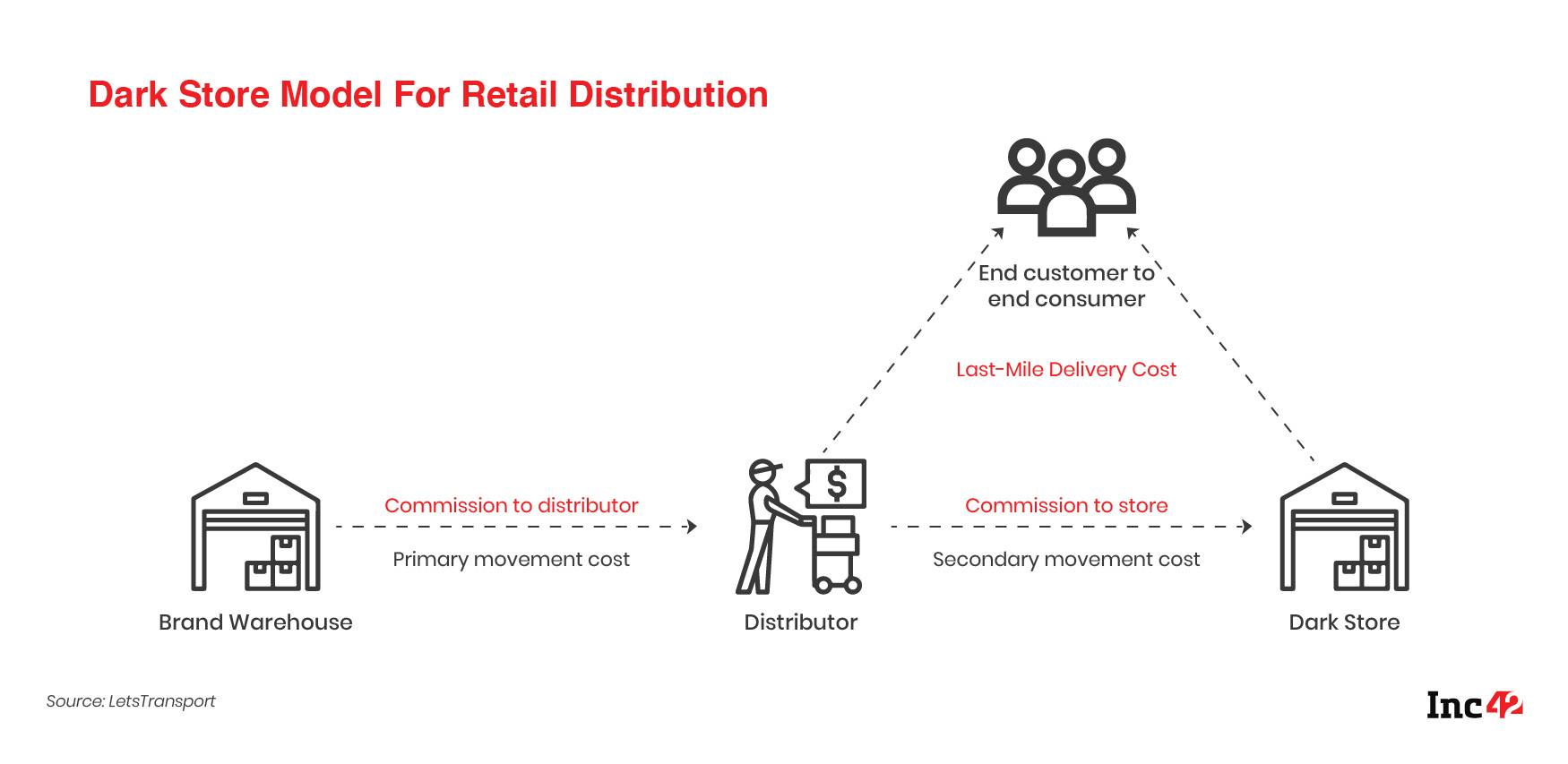

In comparison, the dark store supply chain gets aggregated at the fulfilment centre and there is no retailer link here. But here, the last-mile delivery costs tend to be much higher than traditional warehouse models, as fast and door-to-door delivery is the basic premise.

Ownership, Product Categories And Profitability

The concept of dark stores changes on the basis of product categories and the nature of urgency or demand from the consumer’s end. In food and grocery, for instance, the availability and delivery of the product is expected within 2-3 hours.

Platforms like Bigbasket which have fulfilment centres and dark stores facilitate on-demand delivery in many cities. On the contrary, companies like Swiggy and Dunzo onboard stores in each neighbourhood and their delivery agents pick products from these stores to deliver to customers.

According to Gautam Kapoor, COO and cofounder of Shiprocket, the likes of Dunzo, Swiggy, Zomato and others that have retail store networks can come up with concept stores where businesses and FMCG brands can store inventories to expand their distribution capabilities. When an end-consumer places an order for these products, they can be picked up from these concept stores and delivered to the consumer.

Third-party logistics (3PL) or warehousing companies can also offer dark store capabilities in the middlemen layer for a wider retail network in Tier 2 and Tier 3 cities. One can also expect to see commercial real estate growth for warehousing and enabling fulfillment from such locations.

On the other end of the spectrum, for apparel and electronics retail, products may not be needed in 2-3 hours — the expectation is to get the order in 24 hours. The concept is evolving and this is where omnichannel presence comes into play — combining online discovery and checkout with fulfilment through warehouses in the vicinity.

“Now the value is to convert these channels into ecommerce channels. Instead of going to the main warehouse located in a remote location, these channels can be used. 3PL companies are offering warehousing and fulfilment capabilities for people who do not have distribution capability,” added Kapoor.

For instance, recently, Shiprocket launched ‘Fulfilled by Shiprocket’ where retailers can store goods for consumers. This is focused on retail businesses and allows same-day or next-day delivery for consumers.

Cost Burden Of Dark Stores

A big part of why the concept of dark stores has not caught on in India is the relatively higher cost component in comparison to traditional large hubs and smaller kirana stores. In a price-sensitive market, this cost may just be too much to bear for startups, especially one which does not have high margins to play with.

Manpower Costs Rise With Fulfilment Capacity

In dark stores, workers would be needed for a minimum of two shifts to enable 24×7 delivery, thus adding to the manpower cost. On the other hand, the traditional warehouse with its fixed working hours can function with workers in a single shift.

In kirana stores, the owner manages the shop every day of the week and there is perhaps an employee (helper) or two at most. Kiranas have prospered on philosophy of being a small family-owned business, where profits are usually invested back in the shop.

City Presence Drives Up Rent

Traditional hubs are based in city outskirts which means cheap real estate costs while kirana stores are primarily owned or taken on lease at low rents deep within local neighbourhoods. Dark stores on the other hand, require 2000 sq ft to 4000 sq ft of real estate in prime high-population areas in the city, thereby increasing the rent cost manifold.

Unit Economics And Minimum Order Size

Given that dark stores primarily need to fulfil quick two-hour or four-hour delivery, industry experts estimate the cost per delivery to be INR 50 – INR 60. With an estimate of 10% commission earned per order, a dark store operator would need an estimated minimum order size of INR 800 – INR 1,000 to get a profit in hand.

For the same reason, traditional large hubs do not make much sense for small orders. The cost of warehousing added to the cost of delivery makes smaller orders less profitable, so warehouses need retailers for high volume orders with larger ticket sizes. However, in the case of kirana stores, the delivery cost is very low — often it’s possible to walk over for a delivery — so it can even deliver orders for INR 200 – INR 300 profitably.

Logistics And Maintenance Cost Eat Into Margins

A traditional large hub is equivalent to at least five dark stores in terms of real estate occupied. Thus replicating the same SKU and cold storage structure in each dark store is pocket heavy. The tech-enablement costs for online inventory mapping, route optimisation, logistics between several dark stores is an added cost further for dark stores.

Kirana stores, on the other hand, need small infrastructure as they work on daily demands and less stock has to be maintained in comparison. Plus on the technology front, kiranas are currently largely using either a PoS solution or a software-based ledger for transactions — very few have tech capabilities beyond that.

So Why Is The Industry Bullish On Dark Stores?

Given some of the cost deficiencies of dark stores, the model should not ideally find large traction in India but industry leaders are optimistic that a change in consumer behaviour initiated during Covid-19 times will accelerate the adoption of faster deliveries even in less urbanised areas and neighbourhoods. Hence, consumers may be more inclined to bear the higher delivery costs that dark stores come with.

According to LetsTransport CEO Pushkar Singh, cities have high order densities resulting in positive unit economics capable of undertaking the costs of delivery boys. Typical retail outlets have significant real estate costs, which can be substituted by much cheaper options in case of dark stores – enabling further cost benefits. And as more consumers from Tier 3 cities and beyond order groceries online, dark stores might become profitable in these markets as well.

Further, there are more savings in case of dark stores as frontline staff is replaced by tech and inventory management and invoicing gets automated. As a result the addition of delivery cost in the case of the dark store model now is getting absorbed through these savings.

“In case, a small portion of added delivery cost is still not covered in these savings, there is potential to charge the same to consumers a slight premium in the form of delivery charges to offer this service, making the unit economics viable,” Singh added.

Are Kiranas Leading India’s Dark Stores Drive?

For a country like India, which already has a decades-old dark store network in the form of kirana stores, the concept may not seem new. It’s also perhaps why it’s been used so sparingly.

As FarEye’s Nahata highlighted, during Covid-19, there are probably some retail stores who have shut down completely, which could turn into dark stores. “But those who are still operating, have the bandwidth to convert their frontend to a dark store or a delivery centre where it partners directly with a FMCG maker or get listed on aggregator hyperlocal delivery apps, acting as a dark store for them,” he added.

But not every deep-pocketed player is expected to run its own network of dark stores. ShipRocket’s Kapoor believes a dark store concept will only work where there are intermediary parties trying to bring goods together. “There are startups like Swiggy, Zomato, Dunzo, Bigbasket that will bring the demand to dark stores directly. No retailer can create this individually, it needs to be aggregated,” he added.

At the same time, it’s tough for a tech-driven dark store segment to compete with the scale of the network and familiarity of local kirana stores across the country. Where dark stores are purely technology-driven, kirana stores are more capable of doing personalised curation.

“In terms of delivery cost also, dark stores need high ticket size orders while Kirana can operate at a lower end as well. In crux, where the kirana store is not able to deliver, a dark store might not be able to deliver as well,” added Maxwholesale’s Agrawal.

Further, given India’s housing complex structures and G+2 model for independent houses, it will be difficult for dark stores to achieve good unit economics. Dark stores would be better positioned from a cost point of view for deliveries to multiple consumers in a single location, rather than spread out deliveries, which is the reality in India. This has proven expensive even for the likes of Milkbasket and here too the kirana store is at an advantage.

All this network of stores needs is the added tech-capability for modernisation, which many startups such as PeelWorks as well as retail giants such as Walmart, Kishore Biyani’s Future Group and others are working towards.

There is a demand from the urban consumer side for such dark stores, said LetsTransport’s Singh. “This monetisation potential is what makes the model viable and more attractive. I think consumers would be willing to bear the cost associated with it,” he said. But when and how are the big questions.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.