SUMMARY

Is NPCI's growing presence across fintech segments also a potential threat to startups?

This December, the NPCI will celebrate its 15 year anniversary, but for the most part, many of us only became familiar with NPCI because of fintech and UPI. And that’s only in the last 7-8 years.

But today it’s much more than UPI. It might as well be the backbone of fintech in India and in many ways, the gatekeeper of fintech innovation. And this was on full display at the 2023 Global Fintech Festival (GFF) in Mumbai this past week.

The slew of product launches at the GFF showed just how much innovation is waiting in the wings. Startups are viewing NPCI’s role with a dual lens — not just as an enabler but also a large corporation, as its name suggests, which has its own revenue interests to follow.

We’ll look at this dual-edged role shortly, but after these top stories from our newsroom this week:

- EV Ownership Hurdles: EVs are here to stay but electric vehicle financing is still grappling with teething issues that have slowed adoption. What needs to change? Read in our World EV Day special

- Clipping The Flip: Can GIFT IFSC’s special provisions be the answer for startups looking to reverse flip to India? Here’s the answer

- Inc42 Financial Tracker: With profitability of startups under the microscope, this latest addition to Inc42 tracks the FY23 performance of startups and tech giants. Bookmark this for updates as and when financials are released

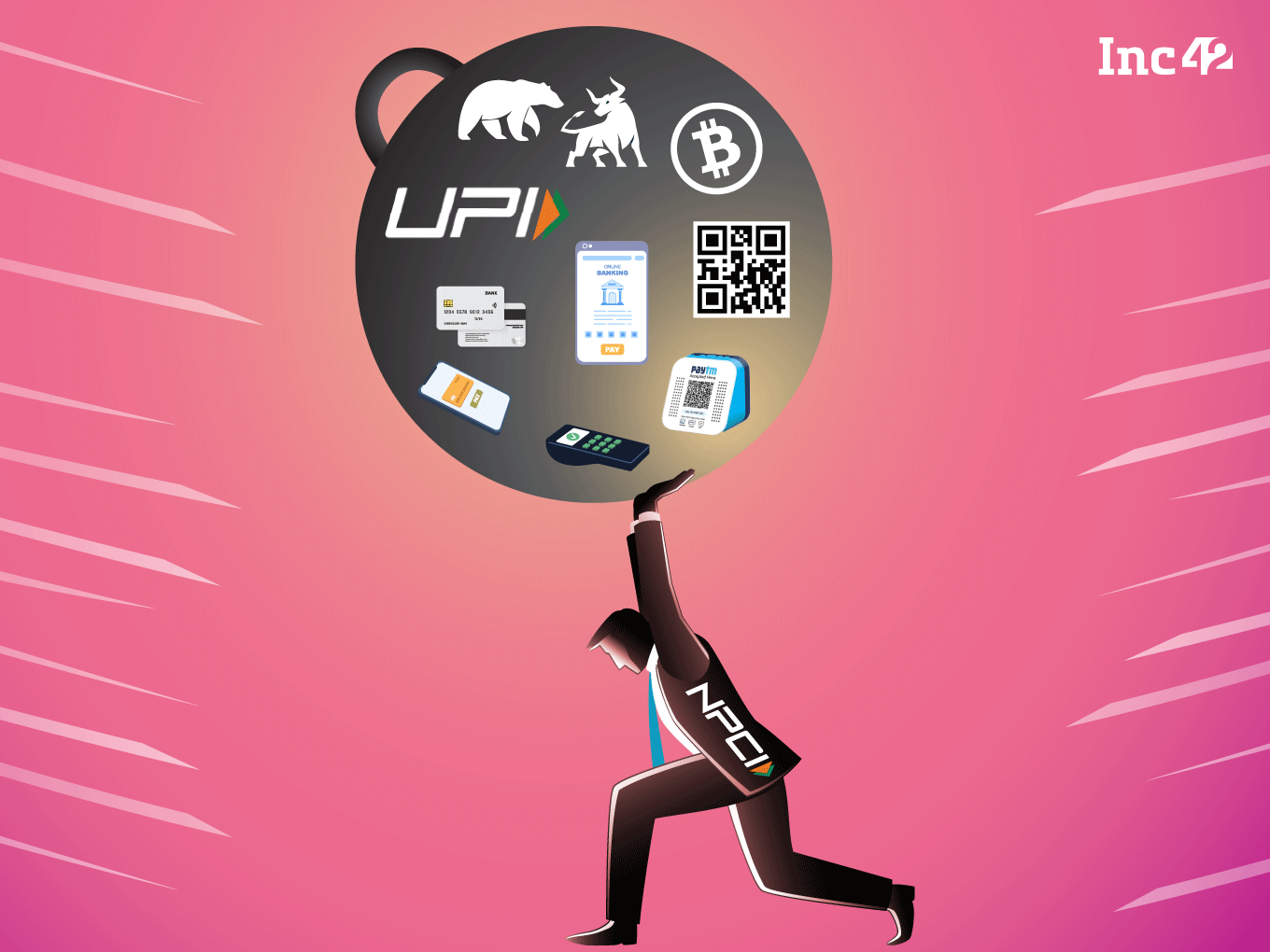

NPCI’s Fintech Universe

Pretty much all the major attractions at GFF in Mumbai were from the payments segment, even though there was a heavy presence of lending tech and embedded fintech or API products as well. But when it comes to payments, NPCI was everywhere.

With a lot of fanfare, it announced tie-ups with PepperMoney, FamX and PineLabs for prepaid cards, LivQuik for a payments ring, a forex card launched in association with CARD91, showed off its work in conversational payments with Amazon Alexa, and also took the first steps towards taking UPI to the US and the UK.

There was also a partnership to launch EV charging payments on the FASTag platform, and a cross-border bill payments service for NRIs. UPI also got upgrades, including conversational payments, NFC-based offline payment offerings, UPI Tap & Pay and, arguably the biggest game-changer, credit line on UPI. NPCI was the talk of the town online and offline.

Speaking at that launch, Infosys cofounder and non-executive chairman as well as former UIDAI chief Nandan Nilekani said that NPCI ecosystem has been transformational for India in its journey to a digital-first economy.

“As they use additional credit, get access to capital and build businesses, we are going to see a huge formalisation of the country over the next 20 years. This is only possible because of the digital public infrastructure,” he told the audience.

The new feature launches are part of the NPCI’s quest to take UPI to 10,000 Cr monthly transactions. With UPI recently achieving the milestone of 1,000 Cr monthly transactions in August 2023, all eyes are now on how the payments network scales up going forward. The addition of credit to UPI is likely to supercharge this growth.

NPCI Comes For Lending Pie

Credit line on UPI is the biggest elephant in the room when it comes to fintech startups.

Credit on UPI will essentially allow consumers to pay for transactions through credit but using the UPI interface. This works by connecting pre-sanctioned digital credit lines from banks through UPI apps and payments products.

The payment flow and UX will be the same as UPI right now, so familiarity is expected to drive customer acquisition and could also tackle the problem of low trust in loan products. This is a major disruption within the fintech ecosystem as payment apps can now leverage bank partnerships to enable credit lines on UPI.

This also allows many payment apps such as Google Pay and Paytm to enter the space that was vacated by prepaid payment instruments or PPI-based lending players, which also offered credit line products, last year. Indeed, Paytm and Google Pay are among the first to launch the ‘credit line on UPI’ service. We can expect UPI market leader PhonePe to join the duo soon.

NPCI is also said to be working with HDFC Bank and ICICI Bank for full digital onboarding for sachet credit products, which could further disrupt BNPL players. At present, UPI is used by 350 Mn individuals, according to the corporation. “There is opportunity to make credit available real time and we are working on a service layer to empower customers to manage and use credit,” NPCI’s chief Dilip Asbe said in a media statement.

Disrupting Startups?

Of course, NPCI’s feature creep into areas beyond payments has some players worried. It’s the source of the one big complaint from the fintech industry.

Some players say NPCI is concerned about its primary source of revenue which comes from the expansion of its network and penetration into startup-led fintech models. Speaking at the GFF, RBI Governor Shaktikanta Das claimed Indian fintech will touch $200 Bn in generated revenue by 2030.

NPCI is also a big part of this opportunity, and unlike most fintech startups, it is a profitable entity. In FY22, NPCI logged over INR 720 Cr in net profit on an operating revenue base of INR 1,620 Cr. Income from payment services constituted 96% of this income.

As per its filings, NPCI primarily earns revenue from operating retail payment systems for its members through cheque truncation, National Financial Switch (NFS), IMPS, RuPay card network, National Automated Clearing House or NACH, Aadhaar-enabled payments, UPI, electronic toll collection (FASTag), and more.

It also charges its members product and membership fees (non-refundable) for being part of the network, details of which were not readily available. But NPCI has increased the membership fees for banks in the past (from INR 75K to INR 3 Lakh in 2017, for instance).

In private, founders were unhappy about the entry of NPCI into the credit space with a product that resembles PPI-led credit line products such as the ones offered by Slice, OneCard, Uni, Jupiter, LazyPay among others.

The RBI barred existing products and mandated PPI players to use banks to offer credit ‘directly’ to customer’s bank accounts rather than through the PPI product. The reasoning was that PPI was never meant to be a lending instrument, but players had used loopholes to circumvent the regulations.

But it did disrupt operations industry-wide even in cases where startups had followed regulations.

And now NPCI is doubling down on the bank-first approach with the credit line on UPI, allowing larger players such as Google Pay and Paytm the opportunity to flex their scale.

The other launch of prepaid cards also impacts fintech startups that partner with PPI issuers to offer UPI-based services. Indeed, in June, NPCI had asked PPI issuers to stop all cobranding arrangements and now it has launched prepaid cards directly with some startups.

Startups know that working with NPCI gives them some advantages on the regulatory side, but on the other hand, many feel that they have little choice in this matter. At the moment, there is only minor discontent among a handful of startups, but it is certainly brewing quietly, even amid the overall enthusiasm for NPCI’s role in propelling Indian fintech.

Startup Spotlight: Attero’s E-Waste Playbook

Not many startups can turn ‘trash’ into gold, but Noida-based Attero logged INR 300 Cr in revenue in FY23 doing this and profits in FY22.

Leveraging the booming consumer electronics products market, Attero started recovering gold, silver, aluminium, and copper from e-waste such as discarded laptops, mobile phones, televisions, and refrigerators.

Today, its efforts are in the area of Li-ion battery recycling to create a sustainable future for the EV generation. 85% of its business comes from e-waste recycling while Li-ion battery recycling accounts for 15% of the total revenue today, which the company is certain will change in the future.

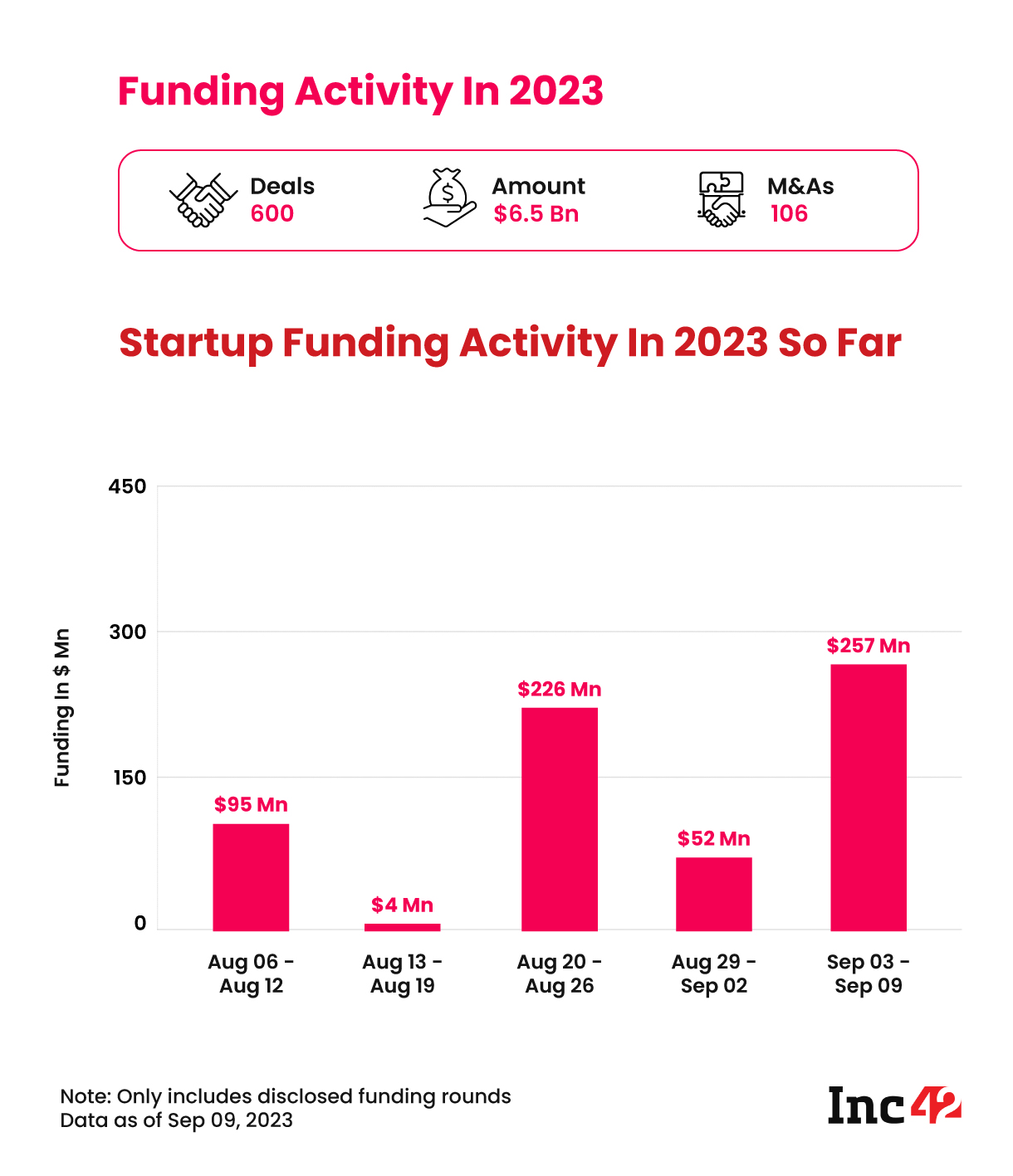

Sunday Roundup: Startup Funding, Tech Stocks & More

- Startup Funding Surges: After barely cracking the $50 Mn mark in the previous week, this past week’s startup funding tally saw some improvement. Overall, $257 Mn was raised by Indian startups and tech companies, including listed entities such as Nazara.

- Reliance Eyes Chip Gold: RIL is reportedly in talks with international chipmakers to partner up for semiconductor manufacturing in India

- Bull Case For Zomato: Platform fees on Zomato could add INR 40 Cr to the company’s overall contribution margin, bullish brokerages claimed

- Power Struggle At Rario: Investors in Rario are said to have pushed founders Ankit Wadhwa and Sunny Bhanot out of the company in a bid to exert more control over operations

That’s all for this week. We will see you next Sunday with another weekly roundup, and till then, you can follow Inc42 on Instagram, X (Twitter) and LinkedIn for the latest news as it happens.