SUMMARY

Set up in 2017, Paytm Payments Bank is the top payments bank in India, a leading mobile banking platform and an e-wallet services provider

However, PPBL has been barred by the RBI from onboarding new customers since March 2022 due to ‘material supervisory concerns’

Profitable since FY19, PPBL, in its latest filing, claimed to have complied with most of the RBI mandates, but approvals are pending

Time and again, Paytm founder Vijay Shekhar Sharma has been vocal about his ambitious vision of building India’s first $100 Bn technology company.

Building a groundbreaking technology startup in India is no easy task. But One97 Communications, the parent company of the Paytm mobile payment and financial services group, and its thriving digital banking platform, Paytm Payments Bank Ltd (PPBL), have managed to keep this dream alive, even when the going got tough.

For instance, One97 Communications clocked impressive growth numbers in the financial year that ended in March 2023, posting a 61% YoY revenue growth while reducing losses by 25%, from INR 2,396 Cr in FY22 to INR 1,776 Cr in FY23. It also capped its expense growth to 18% and reached its target for operational profitability.

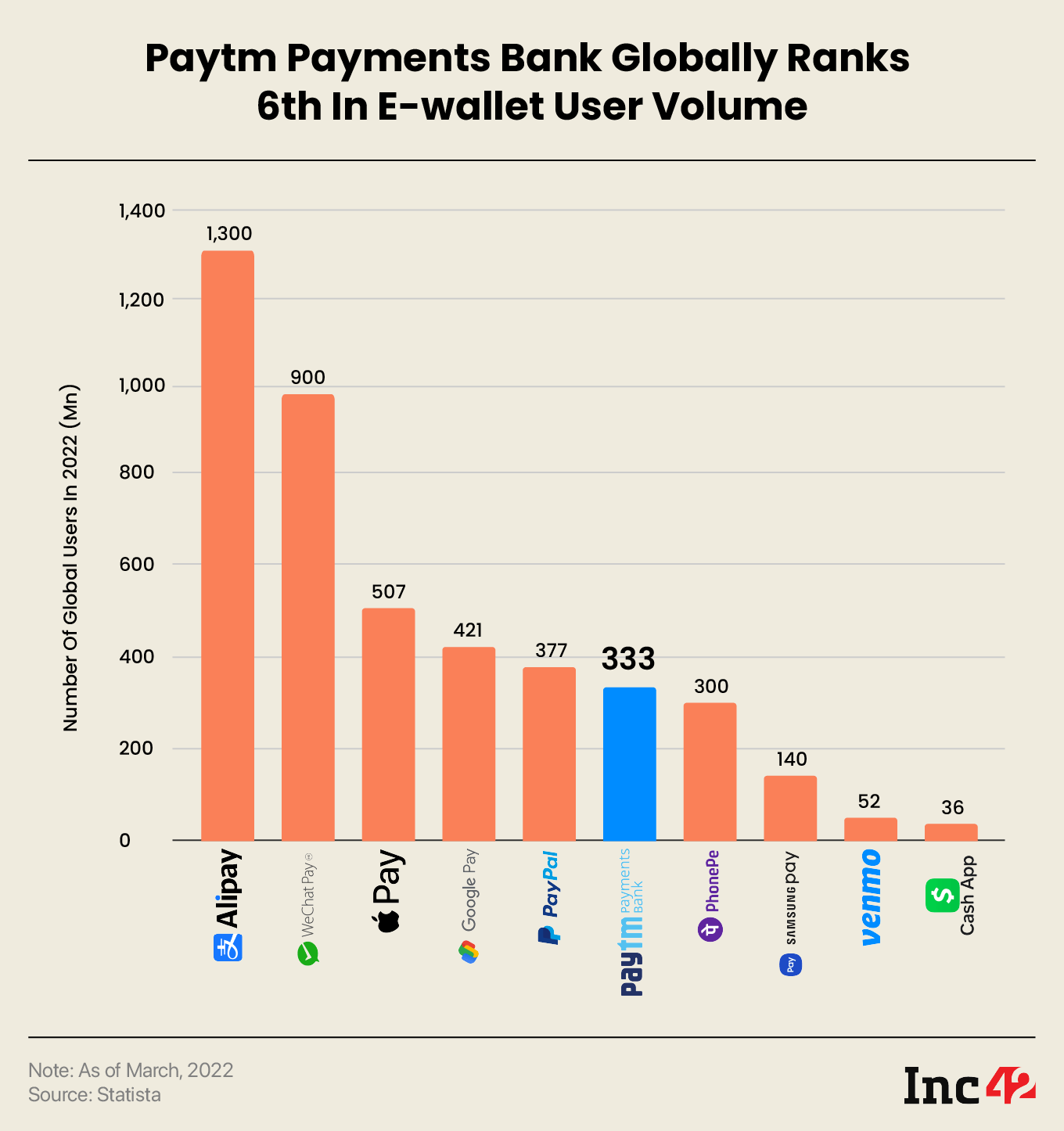

On the other hand, Paytm Payments Bank has been profitable since FY19 (FY23 financials are not filed yet). It emerged as one of the top mobile banking service providers in India and ranked sixth globally in 2022 in terms of e-wallet users.

PPBL is the country’s largest (UPI) merchant-acquiring bank, enjoying 40% of the market share and generating revenue through government incentives, merchant subscriptions and upselling of financial products. Paytm has also onboarded more than 71 Lakh merchants who pay subscription fees to use its PoS devices like Soundbox, surpassing the combined number of subscribers serviced by other payments companies.

Interestingly, Walmart-owned PhonePe still holds an edge over Paytm in UPI transaction volume. But it is a relatively new entrant in the Soundbox market (that’s where the money is) and has only managed to onboard 20 Lakh+ merchants since 2022.

However, all is not hunky-dory with Sharma’s core businesses. The market cap of One97 Communications went south from $19 Bn (INR 1.56 Lakh Cr) to $5.5 Bn (INR 45K Cr), including a 70% free fall in its listing price three months after its INR 18,300 Cr IPO in November 2021. The stock market crash might have been caused by many foreign investors exiting amid concerns over sustained losses and the subsequent price downgrading by several brokerages.

Furthermore, Paytm Mall, an ecommerce venture set up by Sharma, saw a 99% valuation plunge from $3 Bn (INR 24.7K Cr) to $13 Mn (about INR 100 Cr) after Alibaba and Ant Financial offloaded their entire 43% stake at a meagre INR 42 Cr.

Another incident also shook One97 Communications’ associate company Paytm Payments Bank in March last year. On the 11th of that month, the Reserve Bank of India barred PPBL from onboarding new customers, citing “certain material supervisory concerns observed in the bank” (more on that later).

Among all the subsidiaries, Paytm Payments Bank, however has got a number of factors in its favour including its mobile-first services, a large consumer base of digital users, and a strong brand value. The range of products and revenue streams will increase manifold, once the company acquires a small finance bank’s license. However, for the long-term benefits, it must overcome the financial and regulatory challenges in the short term, believe experts.

Can Paytm Payments Bank be the entity, Sharma could bet on? Let’s take a look at the Payments Bank.

Paytm Payments Bank: Born With A Silver Spoon & Clocking Profits

Before we delve deeper into Paytm Payments Bank, the obstacles hindering its growth and the opportunities it can leverage to help Sharma realise his $100 Bn tech dream, let us take a quick look at the formation of payments banks in India and their unique role.

Following the RBI guidelines on payments bank licensing published on November 27, 2014, more than 40 applicants contended for the same. In 2015, the central bank gave in-principle approval to 11, including Dilip Shantilal Shanghvi of Sun Pharma and Vijay Shekhar Sharma of Paytm, among others.

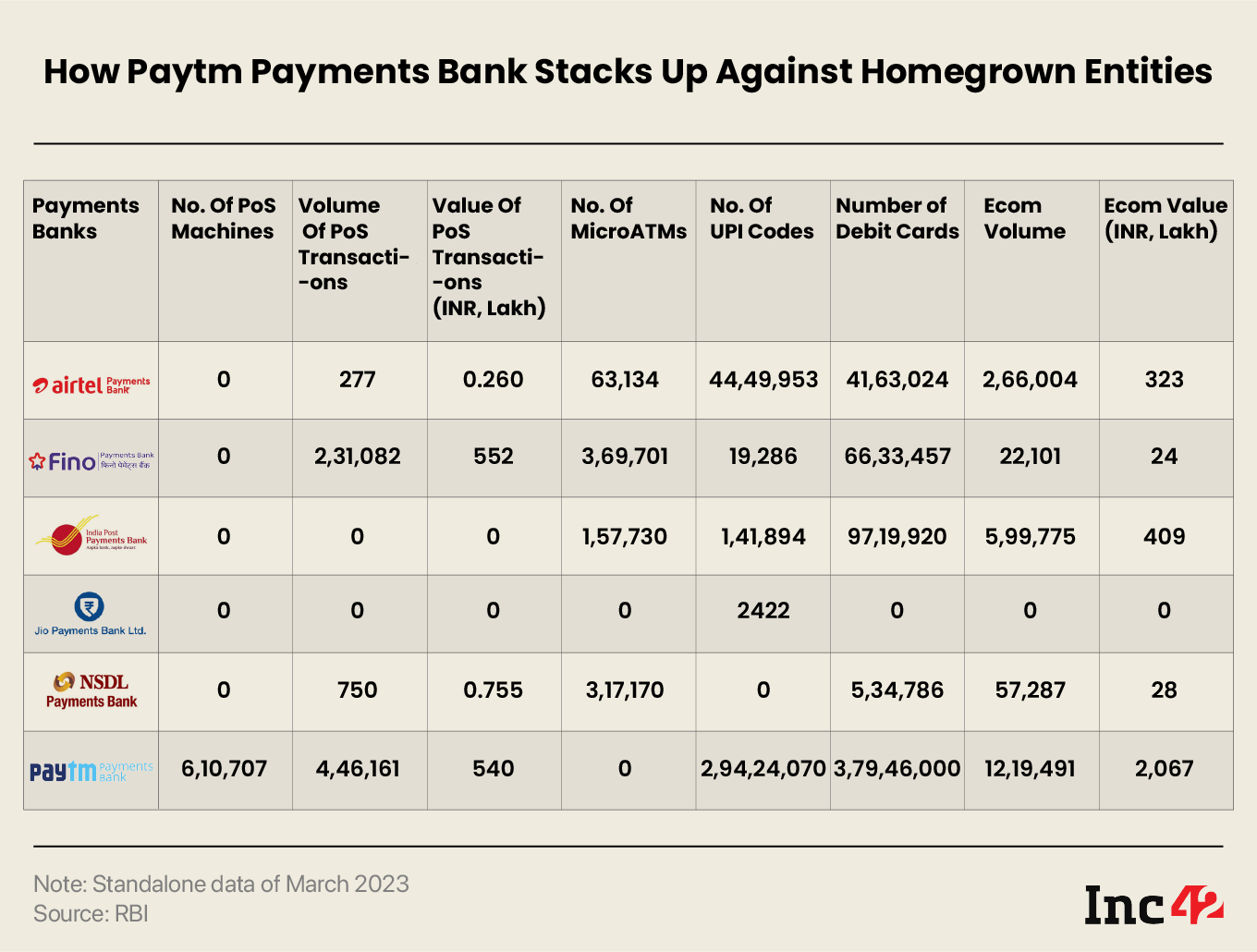

While Shanghvi, Tech Mahindra and Cholamandalam dropped out of the race a year later, the RBI revoked its in-principle approval for Vodafone. With Aditya Birla Nuvo ceasing its payments bank operations in 2019, only six entities currently operate in this space. These include Airtel, Fino, India Post, NSDL, Jio and Paytm Payments Bank.

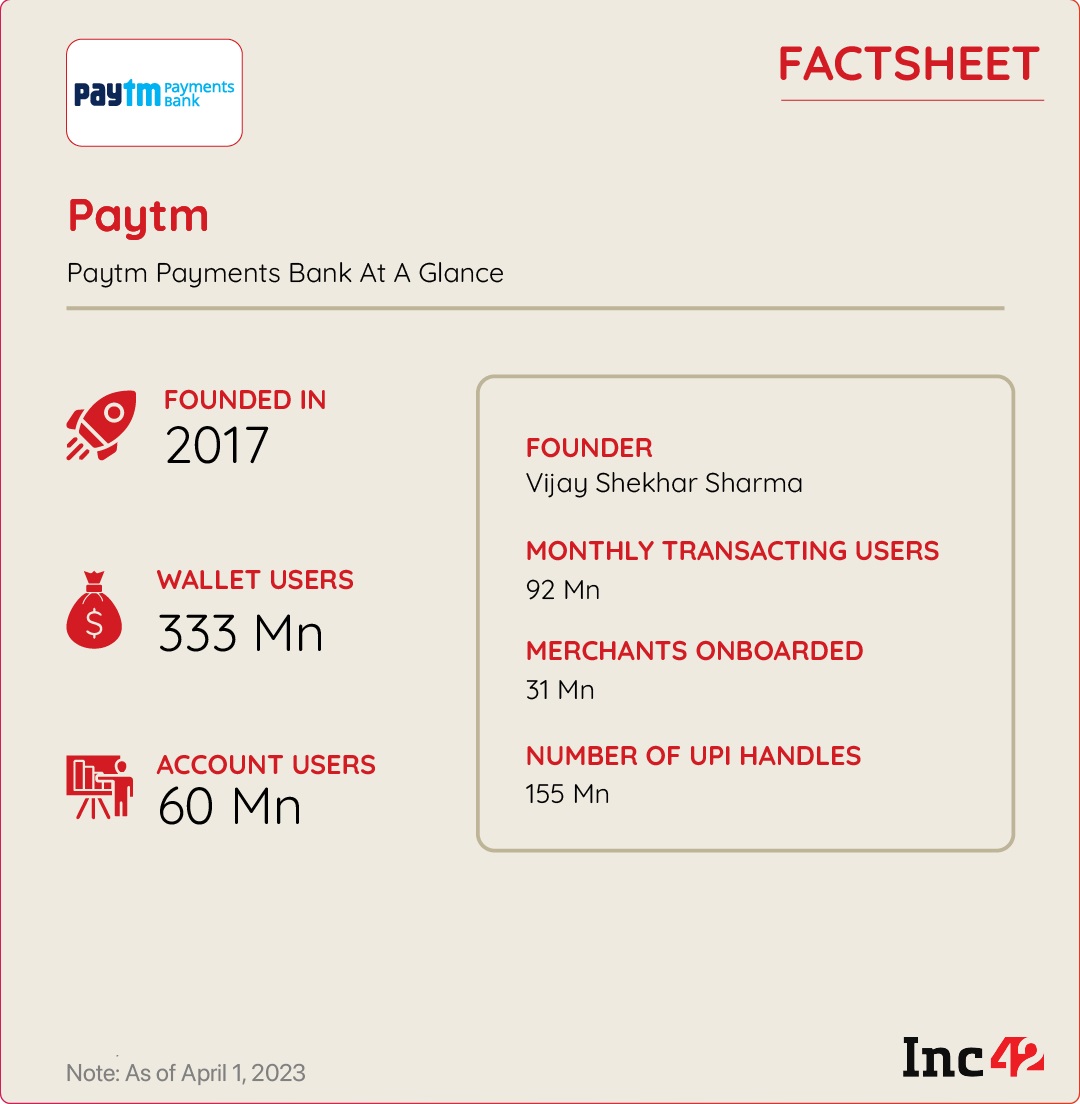

Unlike its peers, most of which started from scratch and struggled to grow, PPBL enjoyed a unique advantage. When it was launched in May 2017, Paytm, the digital payments business of the group, had more than 200 Mn wallet users. So, the parent company merged its wallet services with the newly introduced payments bank to give it a substantial head start in user volume.

Sharma aimed to onboard 500 Mn wallet users for PPBL by 2020 but could only reach 333 Mn by March, 2022. The onboarding of new customers has been halted since then.

Compared to the Paytm group, Airtel enjoyed a distinct advantage in 2017, with more than 285 Mn customers in India. But soon enough, the RBI-UIDAI found that the telco violated eKYC norms while signing up its subscribers for e-wallets. The central bank imposed a fine of INR 5 crore in 2018 and barred Airtel Payments Bank from enrolling new customers for nearly 10 months. Moreover, as a pure-play telco, the company found it difficult to position itself as a payments/fintech specialist.

Paytm Bank: New Avenues Of Revenue

As payments banks cannot directly offer loans or other credit products, lending and wealth management solutions remain out of bounds for PPBL. However, it has developed multiple channels to diversify its revenue scope. These include:

UPI incentives: This programme encourages acquirer banks to promote RuPay debit cards and low-value BHIM-UPI (P2M) transactions. As PPBL serves as an issuer, payment service provider (PSP) and acquirer, it benefits significantly from the scheme and received INR 133 Cr in FY23.

Transaction charges: A 4.35% commission is charged on every transaction from a credit card to the wallet. Transactional charges are also levied for IMPS, NEFT and RTGS fund transfers.

Government deposits: The bank invests customer deposits in government bonds and earns better interest rates than what it offers on savings and business accounts, as well as fixed deposits.

Subscriptions for Paytm Soundbox, PoS machines: One 97 claims to have onboarded 7.1 Mn merchants. These Sounboxes have been integrated with Paytm Payments Bank wallets, UPI QR codes with merchant accounts. To set up a Soundbox, a merchant has to pay a one-time charge of INR 299 and a monthly fee of INR 125.

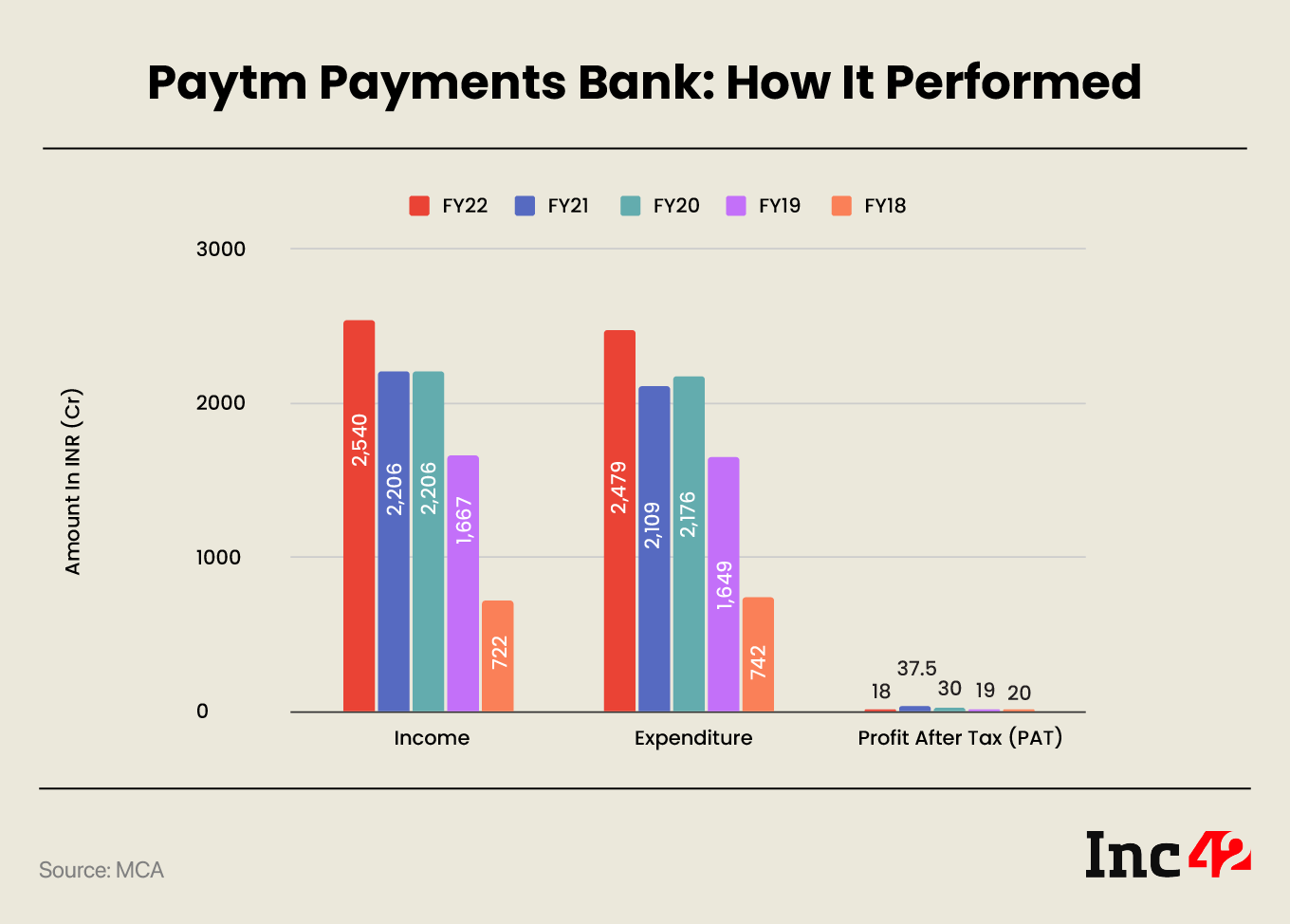

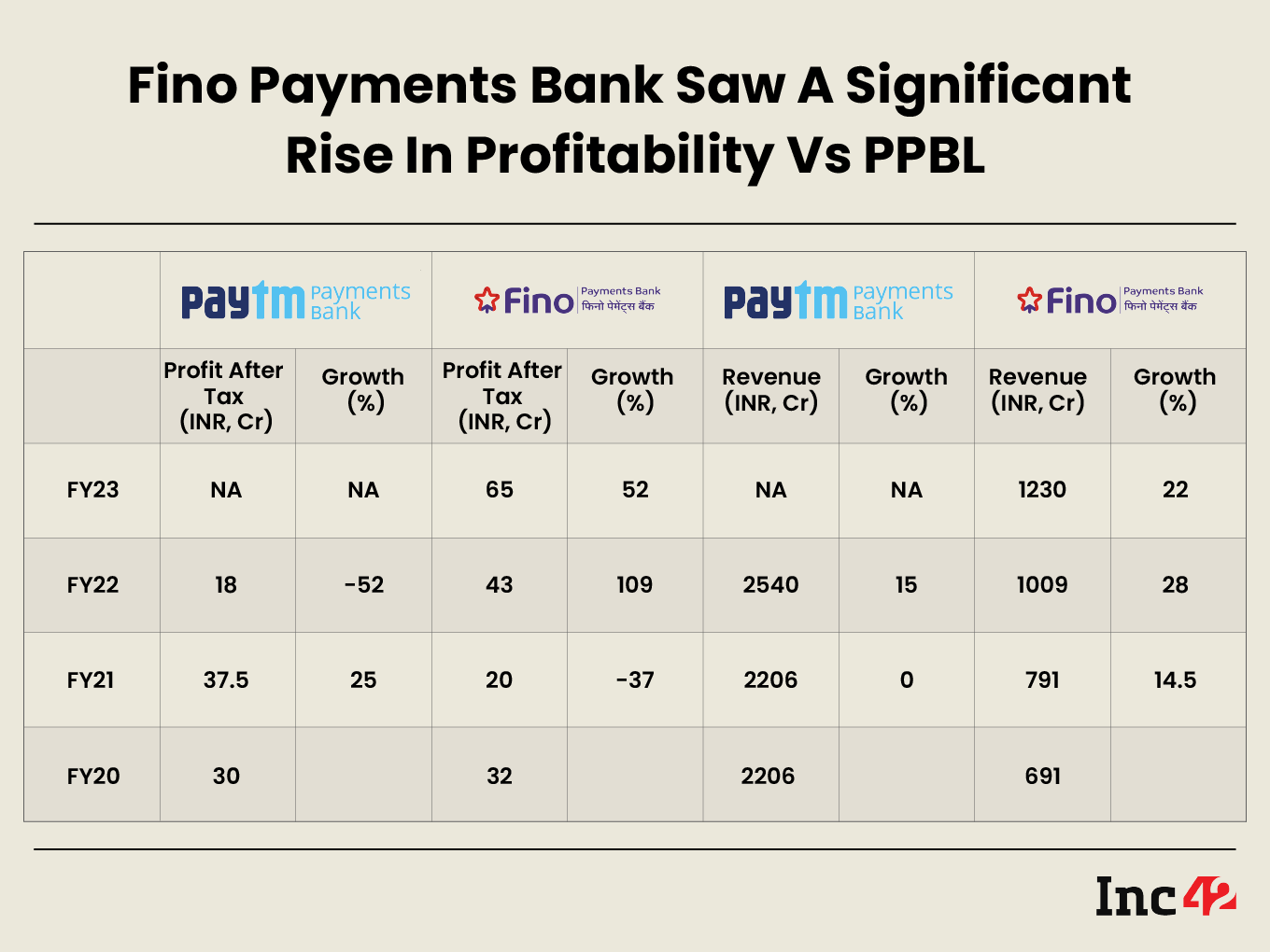

Here is a look at its financial report card since FY19.

For PPBL, The Devil Is In Compliance

That PPBL was not in the red for four years in a row makes it reasonable to expect significant improvements in the revenue trajectory. However, a quick SWOT analysis reveals two critical concerns.

For one, mastering the digital payments space remains challenging, and nothing short of an intense diversification across real-money channels can make companies sustainable. Think of how PhonePe and Google Pay, still ruling the UPI transaction landscape, need to catch up with the Paytm group’s extensive range of payment and banking products for long-term success. Similarly, PPBL’s value proposition will remain severely restricted until it moves to the next growth stage and acquires the licence of a small finance bank (SFB).

This brings us to the second and more critical area – the RBI’s role as a stringent regulator and the impact of its directives on fintechs.

There are examples galore. When non-banks were directed not to load credit lines on pre-paid wallets and cards in 2022, many fintech players offering those services in association with banking and NBFC partners had to suspend their operations. According to Macquarie, such a step might have also affected the volume of loans disbursed by Paytm.

Again, in December 2022, the RBI asked Razorpay and Cashfree to pause onboarding new merchants as they must undergo systematic upgrades and make operational changes before obtaining their final payment aggregator (PA) licences. Therefore, it is not surprising that PPBL came under the RBI lens just before completing its five-year tenure as a payments bank post which it could have applied for an SFB licence.

Even if fintechs claim such scrutiny and time-consuming process improvements do not have any long-term impact on their businesses or growth plans, more often than not, such mandates may escalate into more critical issues. Here is a look at real-time and potential consequences that may arise if Paytm Payments Bank fails to cut through the current regulatory maze.

Zero user growth: After barring PPBL from onboarding new customers on March 11, 2022, the RBI directed the company to appoint an audit firm to conduct a comprehensive audit of its IT system, saying that “the action is based on certain material supervisory concerns observed in the bank”.

According to sources close to the development, the RBI is wary of how Paytm Payments Bank has been functioning in conjugation with One97 Communications’ subsidiaries.

“Whether the Bank has been managing its users’ data separately or it is transacted with other Paytm businesses frequently…since the bank is fully integrated with the Paytm platform, the entire transaction of Paytm Payments Bank is coming from One97 Communications. The RBI does not see this as a healthy practice and that’s why the IT audit. The Chinese funding issue is the other,” he added.

Onboarding of new customers by Paytm Payments Bank would be subject to specific permission to be granted by [the] RBI after reviewing reports of the IT auditors, the central bank notified.

But PPBL sat on the issue. By April 2022, the RBI sent another reminder, and IT auditors were approved and appointed in July. In November, the PPBL management received the auditors’ report and the central bank’s observations, which focussed on improving IT outsourcing processes and managing operational risks.

In its Q4 FY23 financial statements, One97 Communications stated, “Our associate company, PPBL, continues to work towards implementing various recommendations of [the] RBI as part of the IT review undertaken earlier during FY23. A significant part of implementation has been completed and submitted further for validation.”

But the net-net is far from heartening. Due to its failure to close the issue at the earliest, the company has been unable to add a single user since the RBI mandate came into effect last year.

Alleged data leaks raised the spectre of Chinese intervention: Rumours had it that the RBI halted customer onboarding due to PPBL’s possible violation of data rules. According to a Bloomberg report, the central bank could probe whether the payments bank sent data to overseas servers to share it with Chinese entities with an indirect stake in the bank.

The bank, however, immediately and categorically denied these allegations. “Paytm Payments Bank is proud to be a completely homegrown bank, fully compliant with [the] RBI’s directions on data localisation. All of the bank’s data resides in India,” it said.

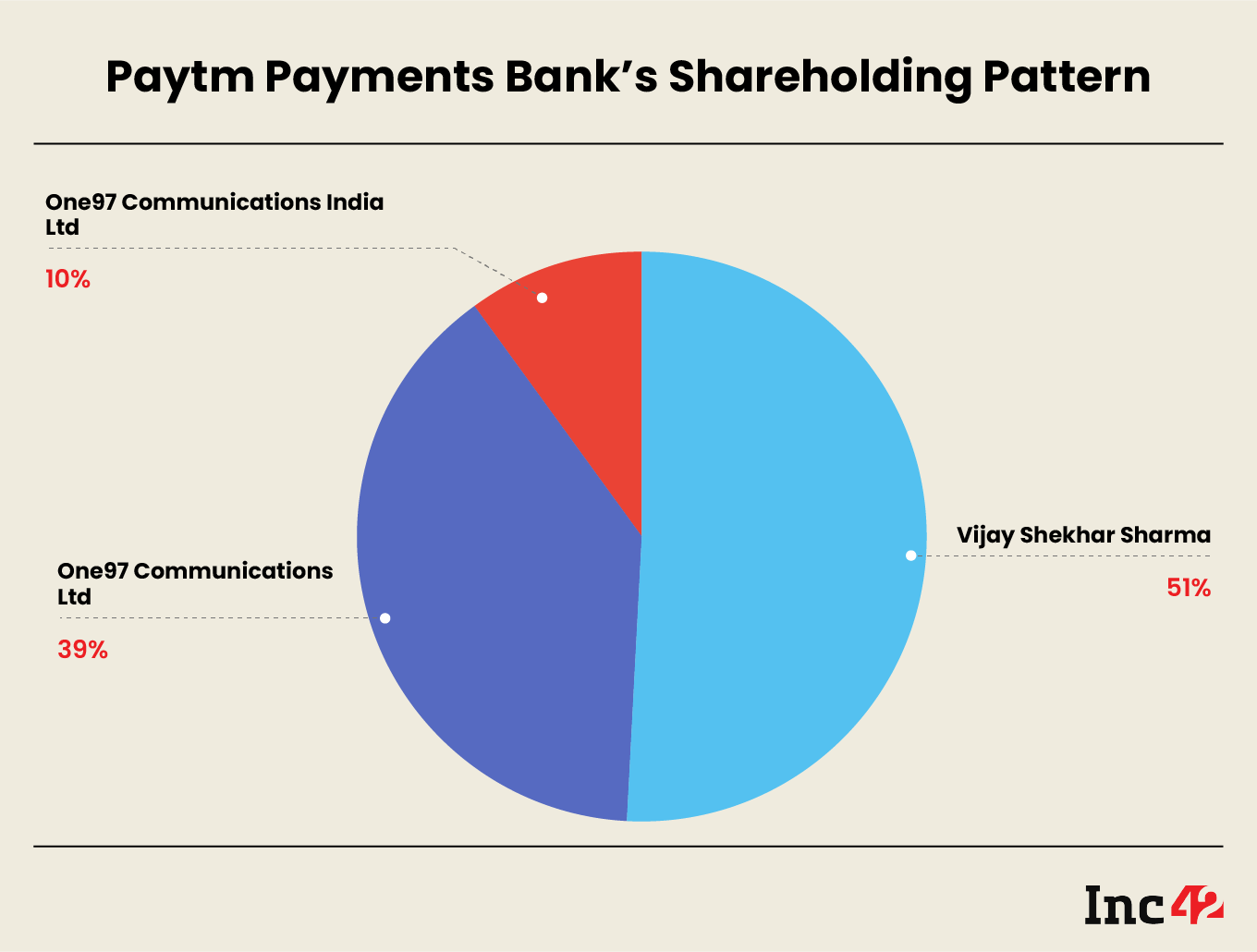

A look at the company’s shareholding pattern also reveals how keen Sharma is to avoid such controversies. He owns 51% in PPBL and has been its promoter from Day 1. But One97 Communications, the parent entity of the group that holds the remaining 49% (39%+10%), was never designated so.

The reason?

A former NPCI official explained, requesting anonymity. “Among the lead investors of One97 are Alibaba, SAIF Mauritius and SVF India Holding (Cayman). If Chinese investors back a company’s promoter, it will not be in the good books of the RBI.”

Alibaba recently offloaded its shares in One97.

Application for SFB licence on hold: After finishing its five-year term as a payments bank, the company intended to apply for an SFB licence in May 2022. But it has postponed its plans.

“Our top priority is obtaining the RBI’s approval to onboard new customers. Currently, there are no plans to apply for the SFB licence,” said a company official who did not want to be named.

According to the former NPCI official, there is another reason for this move. “One97 Communications has a 49% stake in PPBL, and FIIs own 70% of One97. Also, China’s Ant Financials owns more than 25% of One97, meaning 12% of the PPBL funding is under Chinese control. This won’t gain brownie points if the payments bank applies for an SFB licence,” he told Inc42.

One97 may offload its Chinese funds before applying for the licence. This might take a couple of years to keep the transactions smooth without impacting the company’s shares, he added.

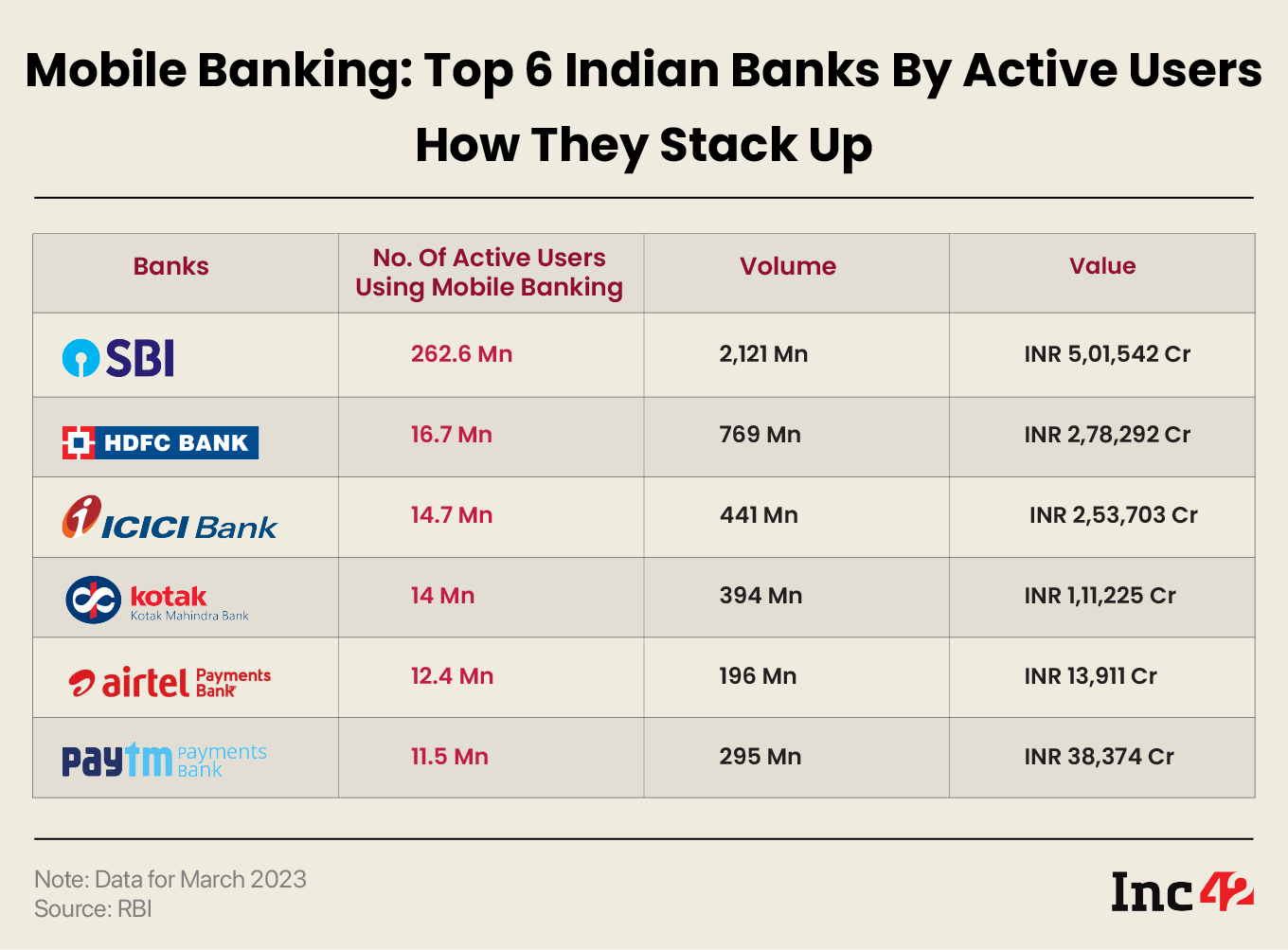

Amid restrictions, PPBL may lose its top position: Although PPBL has been profitable for years, the numbers are rarely impressive, with its PAT ranging between INR 19 Cr and INR 37 Cr. Moreover, other payments banks like Airtel and Fino grew significantly in the last fiscal when PPBL was struggling to cope with regulatory issues.

For instance, Fino opened 29.7 Lakh accounts in FY23, but Paytm could not onboard a single user. Airtel, too, added 28.9 Mn users in FY22 and is expected to add more than 35 Mn users in FY23.

Will Paytm Payments Bank Hit The Jackpot?

Despite many challenges, Paytm Payments Bank has the potential to be a game changer if its founder plays his cards right. Consider this. As of September 2022, Sharma and his Axis Trustee Services owned 8.91% and 4.77% of One97, respectively. This makes him a minority shareholder instead of the company’s promoter, although he is the company’s founder and a non-retiring director.

As the Indian government is reportedly putting pressure on the group to divest its Chinese investments due to the ongoing geopolitical conflict, Sharma’s minimum involvement, at least on the outside, is likely to help. After all, walking this tightrope means coping with the regulatory burden at every step while obtaining the board’s approval to make important decisions and secure funding.

In contrast, he holds a majority stake in the payments bank and remains the sole promoter, free to lead the company up any suitable growth path that can fulfil his billion-dollar tech dream.

Asked whether PPBL is on track to outshine the parent entity (One97), a banker (for two decades)-turned-VC told Inc42, “There are very few companies that ‘own’ their customers. Paytm is one of them. It has successfully retained its user base and consistently increased the number of repeat transactions, despite the emergence of new fintech apps like Google Pay, PhonePe, BharatPe, Amazon Pay, WhatsApp Pay, and more.”

The way its products gain traction is also impressive. For instance, Paytm UPI Lite, the latest from its stable, has more than 4.3 Mn users since its launch on February 22, 2023, and recorded 10 Mn transactions within the first 45 days. Paytm UPI and UPI Light will pave the way for the payments bank to acquire more customers once the RBI permission is fully restored.

Moreover, when retail banking (with its bells and whistles) becomes fully operational on mobile platforms, leading digital banks like PPBL are bound to attract more customers. In that scenario, legacy players may lose their competitive edge as they still lack inclusivity and a super-app-like experience that will bring banking to one’s fingertips.

Experts also think when PPBL acquires a small finance bank licence and subsequently gets the RBI nod for universal banking, all related business units of the group, including banking, Paytm Insurance, Paytm Money and Paytm First Games, will join forces to provide a more extensive range of services and a richer experience, surpassing what has been envisioned by Sachin Bansal’s Navi.

As a former Paytm KMP (key managerial personnel) said, “Barring regulatory compliances, the group has already cleared the road for the bank. And what it did with the wallets, it will also accomplish in the lending space.

When PPBL became operational, it had more than 200 Mn wallet users. It will be the same with lending. The company disbursed more than INR 23K Cr of loans in FY23. But it was only the distribution part of the business. When it acquires an SFB licence, the entire lending business would be transferred there,” he added.

The only glitch: Can it withstand the RBI’s regulatory whip, the typical growth throes most fintechs have suffered? The central bank has a rigorous approach to regulatory compliance. It not only investigates past violations by banks and financial institutions but also evaluates potential risks before granting approvals, especially when it is about 360-degree customer protection and convenience.

“It is nothing new,” said the former KMP quoted above. “The RBI barred Airtel Payments Bank from onboarding new consumers in 2018. And the company took 10 months to become compliant. Again, in 2020, it barred HDFC Bank from onboarding new credit card customers. And this time, the bank needed 15 months to meet all the requirements directed by the RBI. The ban was fully lifted by March 2022. It was the same with Mastercard, and the ban was lifted after a year.”

To grow big, the Paytm Payments Bank needs to align with the regulatory requirements, say the experts tracking the Indian fintech space.

However, nothing will fructify until the payments bank gets the RBI approval at every stage, opening the high growth road. If that happens, Sharma’s dream of a $100 Bn tech company may not elude him for long.

Edited by Sanghamitra Mandal