Cofounder and CEO Byju Raveendran said that around 40% of the revenue collected in FY21 got deferred to future fiscal years

The deferred revenue seems to have a deep impact on its numbers and BYJU'S has also capitalized some of its costs which has also raised some eyebrows

BYJU'S claimed that in FY22, it clocked INR 10,000 Cr in gross revenue, but did not say whether this led to a profit overall in the most recent fiscal year

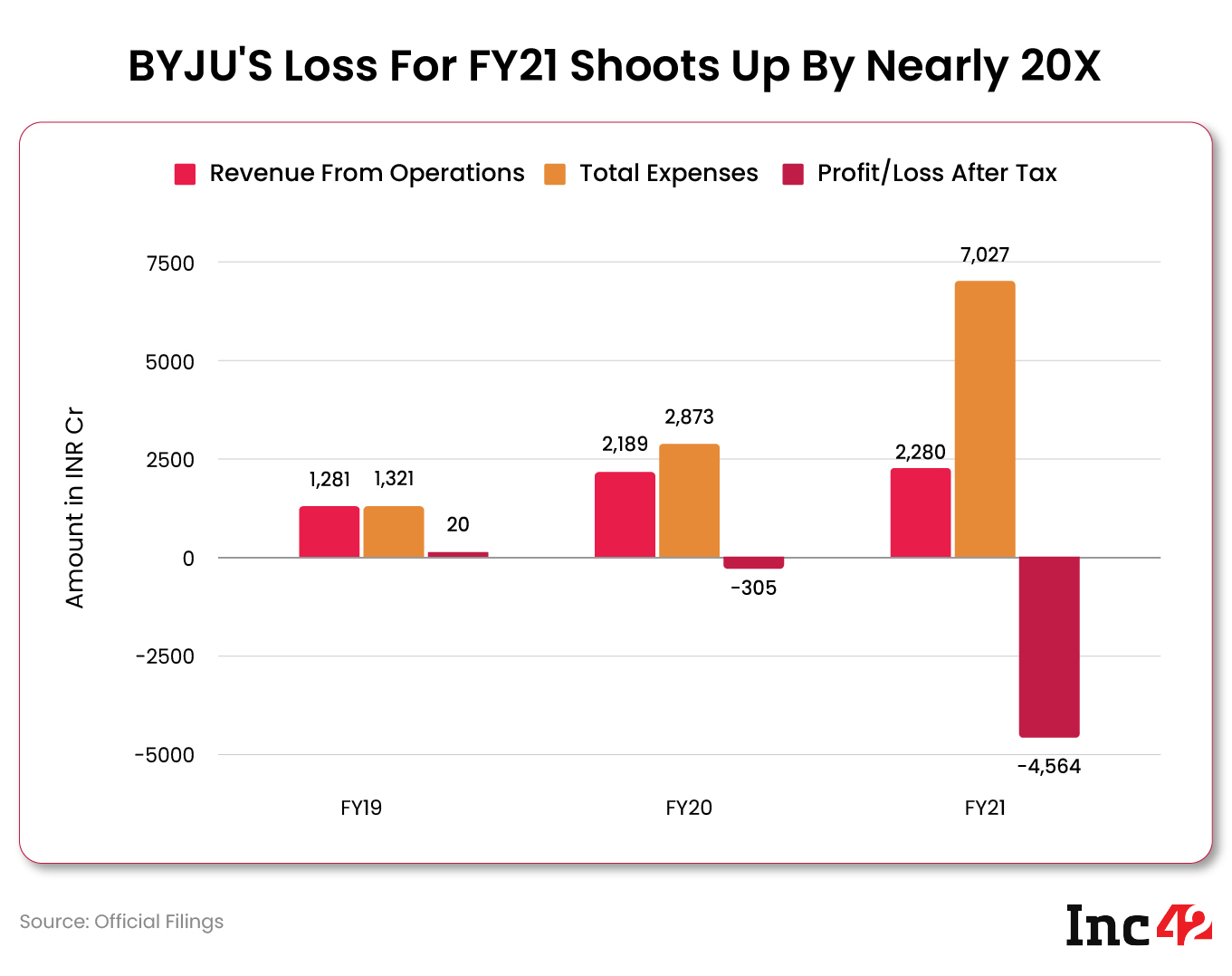

All eyes have been on edtech giant BYJU’S this past week as it reported a massive surge in losses for FY21 after months of delays around its financials. With a total loss of INR 4,588 Cr for FY21, a massive 1,880% or 19.8X jump from FY20, all headlines are pointing towards how BYJU’S has failed to capitalise on the edtech momentum seen during the pandemic.

For its part, the company has claimed that much of the losses are due to changes in the way it recognises multi-year revenue such as that earned from its streaming services for recorded classes.

Cofounder and CEO Byju Raveendran said that around 40% of the revenue collected in FY21 got deferred, which would have otherwise seen revenue growth in the region of 60%-65%. Instead, BYJU’S revenue from operations grew only marginally and stood at INR 2,280 Cr during the year, a slight increase from INR 2,188.9 Cr in FY20.

We took a look at the numbers and decided to analyse exactly where BYJU’S has spent the billions it has raised and why its revenue growth does not infuse too much confidence. In particular, the deferred revenue seems to have a deep impact on its numbers, but even after this measure, we can see that BYJU’S has also capitalised some of its costs, which might have actually increased the losses further. Read on to see our analysis.

Marginal Revenue Growth In FY21

While the higher losses are definitely alarming, the biggest reason for worry would be the marginal growth in revenue.

In fact, total income on a consolidated basis declined 3.3% to INR 2,428.3 Cr in FY21 from INR 2,511.7 Cr in the previous year. So overall, BYJU’S has seen a degrowth in FY21.

It must be noted that the consolidated statement comprises financial details of WhiteHat Jr, Specadel Technologies, Tangible Play Inc (Osmo), Span Thoughtworks Private Limited (Vidyartha), BYJU’s Inc, and BYJU’s Pte Ltd.

Of these, WhiteHat Jr contributed the most to the loss among the subsidiaries, as we outlined. In fact, Raveendran called WhiteHat Jr the under-performer within BYJU’S portfolio of products and claimed it is likely to involve high cash burn due to the very nature of the segment.

With a total loss of INR 1,118.25 Cr in FY21, WhiteHat Jr contributed 26.73% to the total loss of INR INR 4,588 Cr. This is the second largest contributor to the overall loss after the parent company.

Besides this, there has been a serious decline in BYJU’S revenue from India. India contributed INR 1600 Cr to the revenue in FY20, but this fell by nearly 40% to INR 987 Cr.

Clearly, BYJU’S was not able to capitalise on the edtech boom amid the pandemic in 2020 and 2021, and if it did, that revenue has been deferred to either FY22 or future years, for which we do not have the pertinent filings. This does not, however, mean that BYJU’S will turn a profit in FY22 or FY23. That still depends on how much it has controlled its expenses.

This could be said to be a key reason for why the company has not been able to show higher revenue in FY21. However, Raveendran insisted that this is largely due to how revenue is now recognised by the company — more on this later.

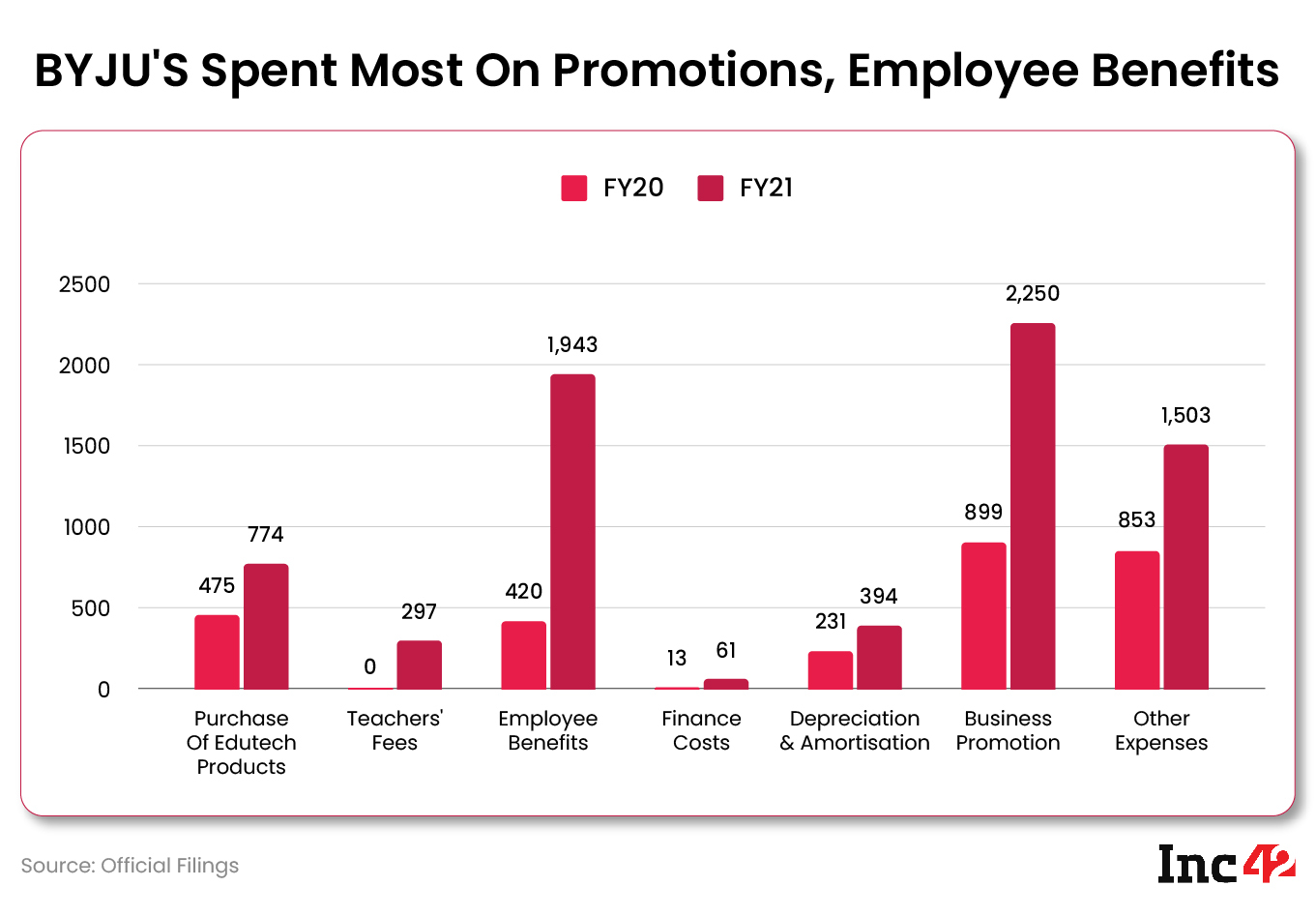

Employee Costs Surge To Touch Nearly INR 2K Cr

Interestingly, the company’s primary expenses are related to business promotions, for which it spent INR 2,250 Cr or half its total loss for the year. The next biggest expense is employee benefits cost, which came up to INR 1,943 Cr. These two expenses together accounted for a whopping 93% of the company’s fiscal year losses.

BYJU’S has a no-holds-barred approach when it comes to spending on marketing. Be it being the title sponsor of the Indian national cricket team or roping in one of the highest paid Indian actors, Shah Rukh Khan, as an official brand ambassador, BYJU’S has spent a hefty amount over the years to become a household brand.

The combined marketing expenses of Unacademy, Vedantu, and upGrad stood at INR 793.5 Cr in FY21. In comparison, BYJU’S consolidated marketing expenses for FY21 were nearly three times more than the combined marketing expenses of the three edtech unicorns.

BYJU’S also hired aggressively during 2020 and 2021, which was reflected in its employee benefit expenses.

In fact, BYJU’S has accounted for some costs related to employees and teachers separately in FY21. For instance, it says teachers have been paid INR 300 Cr in FY21, which was not a line item in FY20. It would seem the company has taken this portion out of the employee benefit expenses, presumably because this amount was spent on part-time teachers who were not on its payroll. It is not clear whether this practice will continue in FY22 and beyond.

Interestingly, some of the expenses related to employees have been recognised as capital expenses rather than operational costs.

For instance, from the total salary outlay of INR 900 Cr in FY20, INR 526 Cr was capitalised as expenses towards intangible assets in the balance sheet. As only INR 420 Cr was recorded as a direct expense in the profit and loss account, more than 60% of the employee expense was capitalised.

Essentially, this meant employee costs were spread across multiple fiscal years for tangible assets. Typically, costs incurred on building intellectual property, software are capitalized, instead of being added as a straight expense, since this IP will be treated as assets in the future.

Similarly, INR 376 Cr has been capitalized from the INR 1,943 Cr as salary, bonus and wages under the employee benefits expense head. Further, in FY20, BYJU’S capitalised INR 551 Cr of expenses under intangible assets, while in FY21 the number was INR 409 Cr.

If these costs were counted as a direct expense, the total loss for the year would have breached the INR 5,000 Cr mark. While these accounting practices are not uncommon and certainly legal, what they do is hide the full picture of the costs and loss for BYJU’S in FY21. It remains to be seen whether this changes in FY22.

Raveendran added that just as BYJU’S has deferred some of its revenue for future years, it is looking to improve its track record when it comes to other disclosures. He claimed the company is looking to ensure that there is no repeat of the delay in reporting, which led to plenty of questions this year.

Given some of these questions being asked now about the revenue deferment, BYJU’S might well change its revenue and expense recognition in the future as well.

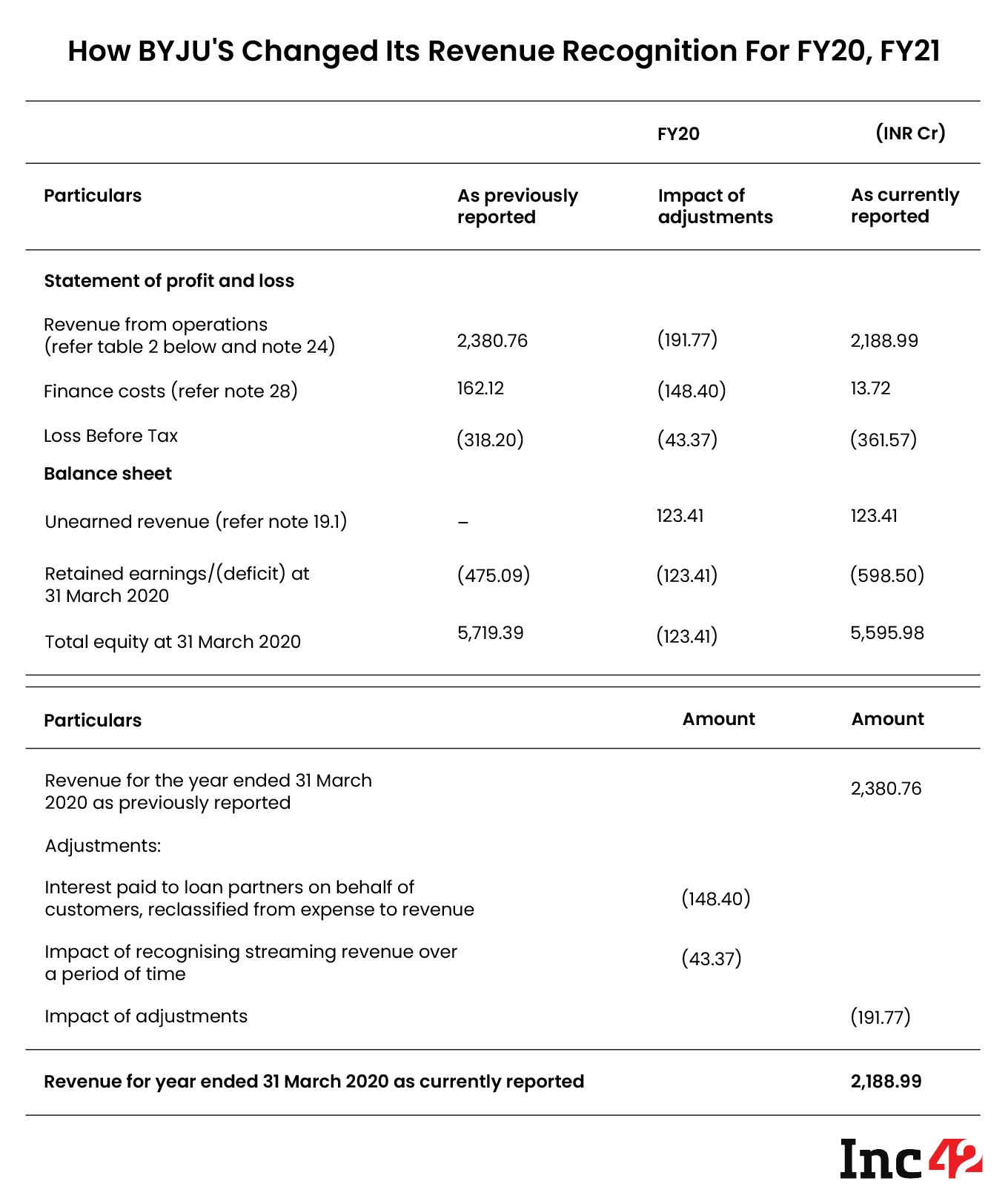

How BYJU’S Deferred Its Revenue

The company’s reasoning is that along with the revenue that got deferred from FY21 to future years (including FY22), the expenses have been accounted for during the fiscal period, resulting in higher losses.

“The Sale of Edutech products (which includes the sale of tablets) are recognised at a point in time. In the case of sale of educational content in the form of Streaming services, revenue is recognised over the period of time the services are rendered to the customers.

But this seems to be a bit of an exaggeration once you dive into the financial statements that have been shared by the company. Even though they are unqualified financials, the numbers show that expenses related to the deferred revenue amounted only to INR 109 Cr in FY21, which is a drop in the bucket considering the overall loss of INR 4,564 Cr.

Besides deferred revenue, some portion of the deferred due payments — INR 1,156.27 Cr to be precise — has not been recognised because the company is unlikely “to collect the consideration to which it is entitled.”

Here’s a breakdown of how the revenue deferment has been accounted for.

Revenues from streaming services, which were previously recognised fully on commencement of contract, have been adjusted to be recognised on a pro-rata basis over the period of the contract.

Further, the interest paid to loan partners on behalf of customers in respect of loans granted directly to customers have been reclassified from finance cost and adjusted against revenues, the filings shared by BYJU’S state.

Clearing The Murky Acquisition Picture

According to BYJU’S unqualified financials for FY21, seen by Inc42, the edtech major has INR 1,983.49 Cr ($249.6 Mn) pending in cash payments to clear the $1 Bn Aakash deal. Notably, the pending amount accounts for a quarter of the total deal amount.

Apart from the cash payments, the edtech decacorn also has to pay INR 2,007.74 Cr in equity after the merger of the two entities is completed.

Thirty-three-year-old Aakash (AESL) was acquired by the edtech giant in a deal worth nearly $1 Bn in April 2021 to enter the offline space and the test prep space. Blackstone, the largest stakeholder in AESL, which holds a 37.5% stake in the edtech giant, is reportedly due $180 Mn.

Amid the months-long delay in its financial reporting, BYJU’S was under great public scrutiny over the uncertainty in payments due to stakeholders in transactions such as Aakash.

In FY21, the edtech major made three major acquisitions — WhiteHat Jr for $300 Mn, Scholr for $180 Mn and LabinApp for an undisclosed amount.

Then in FY22, besides Aakash, it acquired Singapore-based Great Learning for $600 Mn, Toppr for $150 Mn, US startup Epic for $500 Mn, Tynker for $100 Mn and Whodat, GradeUp, HashLearn and Austria-based GeoGebra for an undisclosed sum.

One reason being cited for the delays is that the company is in talks to raise funds to wrap up this deal and other transactions. Abu Dhabi sovereign wealth funds are reportedly in active negotiations with BYJU’S for a $500 Mn round.

What Next For BYJU’S?

BYJU’S claimed that in FY22, it clocked INR 10,000 Cr in gross revenue, but the CEO added that at least one subsidiary — WhiteHat Jr — will continue to remain in losses.

However, these are unaudited results and there’s no clarity on whether this would be the final revenue for FY22. Inc42 could not verify the claims made by the company for FY22 revenue. Besides this, there was also no indication about the loss in FY22.

In terms of cost-cutting, we know that in FY23 i.e after March 2022, WhiteHat Jr downsized its workforce by more than 800 employees. This could have a positive impact on the P&L in FY23.

With a sharper focus on unit economics and sustainability, Raveendran said the company would be looking to capitalise on products that are growing and showing profitability. WhiteHat Jr, however, is one of the subsidiaries that will not show profits, the CEO admitted.

But he was confident that the growth within its core edtech business and other verticals such as Great Learning and Aakash will be able to fuel the cash burn that WhiteHat Jr would require.

As for plans for its IPO, Raveendran said the current macroeconomic conditions have forced most companies to reassess their listing plans. BYJU’S is likely to come back to the drawing board when it comes to the IPO by next year.

“Whether it is a SPAC, a US listing or an India listing — we have left that call open for later. At a consolidated level, we will be on track for profitability at the end of the next two quarters, with the growth we are seeing in BYJU’S and Great Learning,” the CEO added.