[Note: This article is part of The Junction Series. We will be covering the FinTech sector in detail at The Junction 2017 in Jaipur. Learn more about The Junction here!]

The demonetisation drive by the government, however, cynical it may seem, has actually opened the floodgates for India becoming a cashless economy. Not only, have we seen true innovation (and some jugaads too) coming out of this initiative, but also there has been seen a sudden surge in the usage of digital products such as e-wallets, mPOS solutions, and more. In time, we can expect regulatory authorities to revisit their operating models and policies in the fintech segment of the country.

With the stats being all positive, the global fintech software and services sector is expected to boom into a $45 Bn opportunity by 2020, growing at a compounded annual growth rate of 7.1% as per Nasscom.

The Indian fintech market is forecasted to touch $2.4 Bn by 2020, a two-fold increase from the market size currently standing at $1.2 Bn. Lending and payments, in particular, have also paved the path for this unprecedented growth.

This report is the second in our three-part Indian fintech funding series. In the previous article, we discussed how the fintech sector has been performing over the last few years. In the current version, Inc42 looks back at the funding numbers of fintech sector to help our readers understand how fintech has grown as a sector since 2014. You can read more about the sector in the next part of our fintech funding series – the top 5 fintech fundings of 2014-2016.

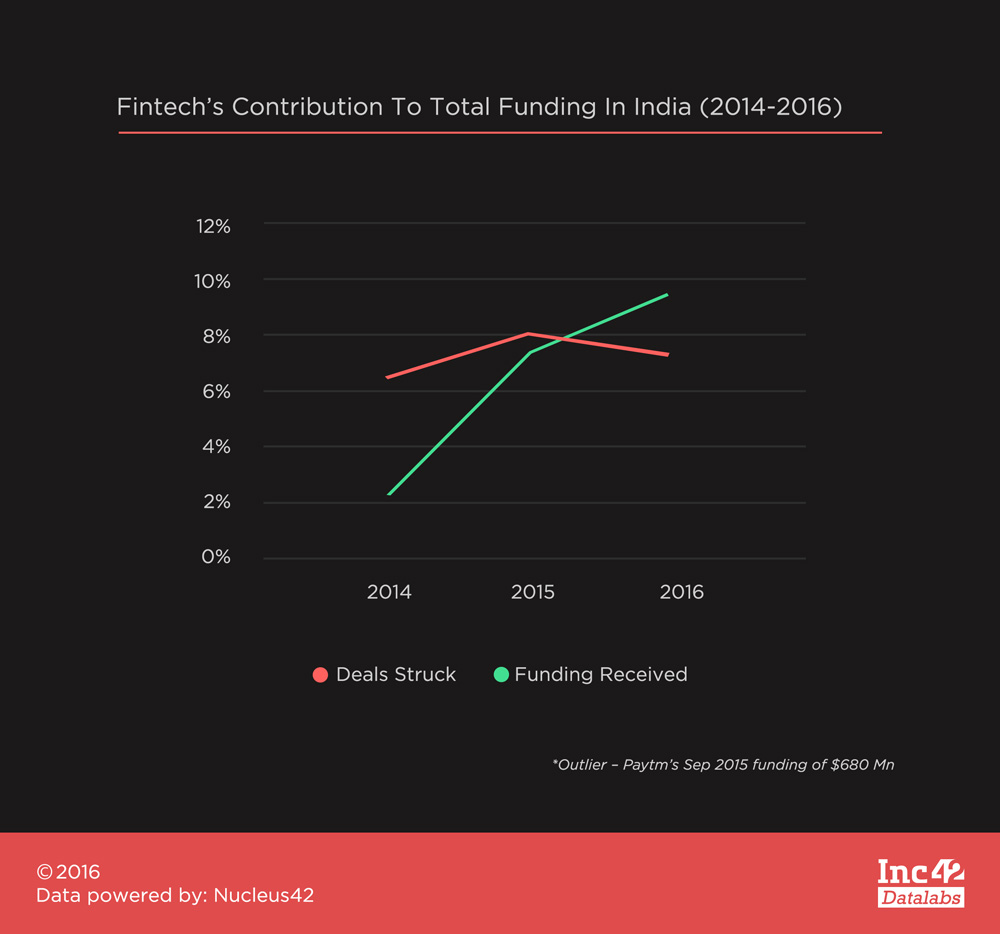

Fintech In Proportion To Overall Funding In India

In 2014, out of the total 308 deals, only 20 funding deals amounting to about $114 Mn were from the fintech sector. This only constituted only 2% of the total overall deal size of $5 Bn. However, 2015 saw a manifold increase in the amount of funding raised by fintech startups. In total, 72 deals in the fintech sector amounted to $1.2 Bn. Out of which about $680 Mn was the funding raised by Paytm during the entire year.

In 2015, fintech saw a major boost as compared to the number of fintech deals in 2014, but it was offset by the total increase in the overall startup ecosystem, which saw about 885 deals amounting to $8.1 Bn. It constituted about 15% of the total deals as compared to a mere 2% in 2014. Even if we remove the huge chunk of investment on one particular entity, Paytm, the total funding still constituted to about 7% of the total funding.

Changes In 2016: More Deals, Demonetisation, Going Cashless

2016 is projected to end with more number of deals than 2015. Things will definitely change to increase the demand of fintech players with the changing economic scenario because of change in regulations.

Demonetisation, the introduction of the UPI by the NPCI, is bound to revolutionise the digital payments and take India a step closer to a cashless economy, approvals for setting up Payments Bank pilot projects being deployed etc. have cemented the position of fintech inclusion and have paved the way towards a better framework in India.

As of October 31, 2016, fintech witnessed a total of 67 deals with $367.89 Mn in funding. It constituted approx. 10% of the total deals as compared to a mere 15% in 2015.

The transaction value for the Indian fintech sector is estimated to be approximately $33 Bn in 2016 and is forecasted to reach $73 Bn in 2020 growing at a five-year CAGR of 22%.

The cash-driven Indian economy has responded well to fintech innovation, primarily triggered by an increase in smartphone penetration and the upsurge of ecommerce. The demonetisation policy introduced by the government has provided an impetus to digital wallets and startups offering mPOS solutions.

Bipin Preet Singh, co-founder MobiKwik opines, “There is a short-term pain, in trying to implement demonetisation, but we should not become overconfident, that our country is going to turn into a cashless economy overnight. We’ve only taken one step today. We have a long way to go and we need to work really hard, with an attitude of humility. We need to make people aware, there have to be major changes on the policy side. The government also needs to adopt cashless payments across all channels.”

The current situation of the Indian market offers an opportunity to exponentially increase demand in almost every category – consumer lending, digital payments, insurance, trade finance, banking tech, etc. Therefore the right streak would be to not give in to merely reallocating the existent market share to current players, but to unlock the true potential of fintech to establish a much larger market.