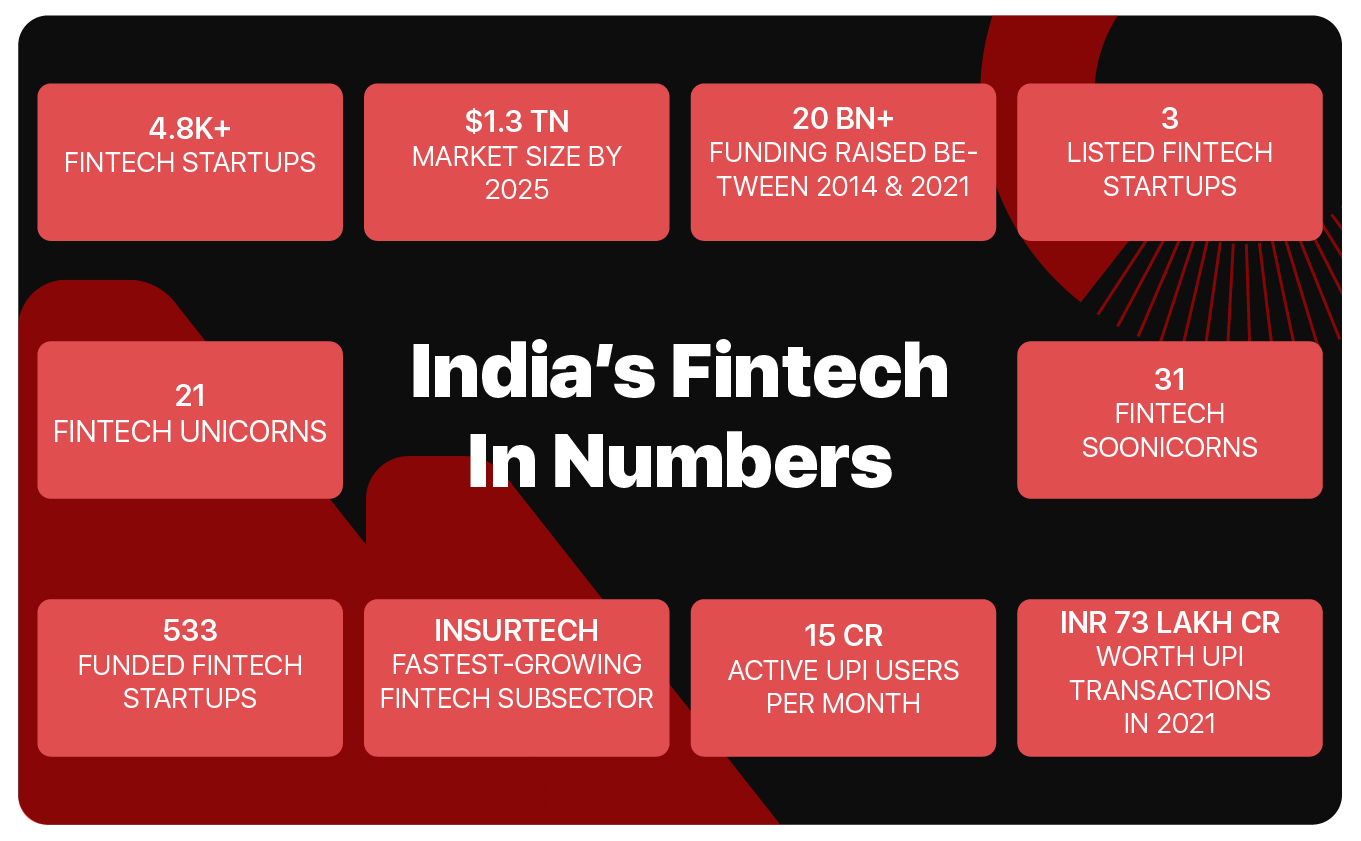

India’s fintech market is estimated to reach $1.3 Tn by 2025, calling for a systematic discussion about the ecosystem, the opportunities and the speed bumps

In this 29th edition, published ahead of Inc42’s Fintech Summit 2022, we take the opportunity to explore fintech and blockchain startups that will reimagine all aspects of finance and realign new-age tech to create innovative products

In spite of the RBI’s latest mandate that will affect the payment and lending segments, Inc42 has shortlisted four payment and seven lending tech startups, which are on their way to disrupt the ecosystem

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

Businesses are bound to experience a mix of good and bad phases, and the current scenario proves it again. The fintech ecosystem in India is firmly in the regulatory crosshairs, and there is no immediate respite in sight if one considers the latest RBI mandate. But that does not deter fintech enthusiasts or overthrow the fact that the ecosystem is estimated to reach a market size of $1.3 Tn by 2025.

It also calls for a systematic conversation among stakeholders keen to explore the future. Inc42’s Fintech Summit 2022 will do just that, bringing the industry together for a deep dive into the opportunities and challenges and analysing the insights that will emerge from this meaningful meeting of minds.

The premier fintech conference, to be held on July 1 and 2, will bring in disruptive financial products and their makers under one virtual roof for a dialogue on how fintech and blockchain will shape India’s new economy.

With the advent of a financial internet that digitises all traditional assets, products and services, the ecosystem is rapidly changing and catering to the evolving needs of tech-savvy consumers. Therefore, at the Fintech Summit, Inc42 will take a close look at how to build a scalable business from the product lens.

Through a mix of fireside chats and panel discussions, the summit will help decode high-growth financial products, understand new business models like BNPL and fintech SaaS and examine the infrastructural innovations like DeFi and DAOs, powering these business models.

The stage is set, and we want to contribute to the cause as much as possible. Naturally, when we sat down to shortlist the startups for the June edition, we were keen to highlight how the internet impacted people’s finances in India and opened things up for new business models.

30 Startups To Watch: June 2022

This month’s list includes only 25 fintech startups, unlike our usual 30 companies solving unique challenges and developing innovative products across sectors. In the 29th edition of the series, we have listed companies working on long-standing challenges within the fintech sub-sectors – from insurtech and new-age lending to warehouse financing, cap table management, fintech infra and more.

This list gets more interesting every month, but this time, we have a single focus, bringing forth the fintech startups that are growing well despite market pullback and regulatory uncertainties.

Editor’s Note: The list below is not meant to be a ranking of any kind. We have listed the startups in alphabetical order.

BridgeUp

Why BridgeUp Made It To The List

The funding winter has set in as equity financing continues to drop quarter on quarter. Even when the world did not face a downturn, raising funds from venture capital and private equity companies, one of the most popular methods among startups for capital raising, took time and effort, along with stake dilution. But there is a way out.

Now that most new-age companies are eyeing a recurring revenue model via subscription, startup funding is changing. Set up in 2021, Mumbai-based BridgeUp was launched as a subscription revenue-focussed financing platform that would revolutionise equity and debt funding.

In simple terms, BridgeUp is a sector-agnostic marketplace that connects startups (earning monthly/quarterly recurring revenues) with investors who bid to purchase the revenue contracts for their annual value. The fundraising process is not complicated, though. To begin with, a startup needs to sign up and sync its payment system with BridgeUp. After that, a trade limit [maximum funding amount] is assigned to the company, and a tradable anonymous contract is drawn up depending on the revenue data. Based on this contract, potential investors can place their bids, and the money is raised from the most suitable investor. BridgeUp’s clients, mainly from SaaS, OTT and D2C sectors, directly forward their subscription amounts to investors as repayments according to their agreed timelines.

BridgeUp charges a service fee of 1-2% from the startups on all transactions, while the platform is free for investors, primarily NBFCs and banks, at this point. The investment tech startup aims to onboard international lenders by FY23 and disburse more than INR 500 Cr to 200+ companies.

Credlix

Why Credlix Made It To The List

In the wake of the global pandemic, businesses badly needed a resilient supply chain that could withstand major disruptions like the Corona crisis. Therefore, the launch of Credlix, a supply chain financing platform, turned out to be a welcome initiative. Launched in 2021 as part of the offering from SaaS unicorn Moglix, Credlix is operational in India and Southeast Asia.

The Noida-based B2B finance facilitator provides five working capital solutions for enterprises/suppliers and exporters, including early-payment programmes, vendor financing, supply chain financing, invoice discounting and purchase order financing.

Here’s how the process works. Enterprises/suppliers can integrate their invoicing process or manually upload invoices on the Credlix web platform so that its analytics engine can recommend financing solutions from NBFCs, banks and companies willing to finance them. It also functions as a lending platform for exporters after its recent acquisition of NuPhi, an EXIM financing startup. The company provides up to $3 Mn in credit or 90% of the consignment value (whichever is lower) and charges annual interest of 7-11% or monthly interest of 0.6-0.9%.

The startup has disbursed loans worth $100 Mn+ in FY22 to finance more than 2,500 MSMEs. It aims to increase its credit disbursal by 3x by 2025.

Credochain

Why Credochain Made It To The List

Although MSMEs in India roughly account for 30% of the GDP, they still belong to the unorganised sector, affected by limited operations, unstructured business processes and few-to-none financial footprints. So, these companies find it difficult to raise loans from banks and traditional FIs. Aware of how this widening credit gap is crippling growth, Credochain launched its operations in 2021 to build an alternative credit assessment approach to help MSMEs join the formal credit economy. The startup also provides a line of credit to these businesses.

New Delhi-based Credochain offers a cluster-based profiling service, post which lenders can come up with geography-specific loans. Based on the MSMEs’ business transactions (sales, purchase of goods, cash flows and more) and a host of other parameters, the startup assesses their loan eligibility and offers solutions for working capital management. It is now building a credit line for MSMEs and has dubbed the feature Pemant. This will work like a bank, providing payments directly to suppliers and repaying existing creditors via e-mandates.

While Credochain functions as a loan assessment platform, Pemant will act as a credit provider in compliance with all regulatory guidelines. In 2021, the fintech SaaS firm onboarded 600+ MSMEs for loan assessment and disbursed small-ticket loans (INR 25K-2 Lakh) through partner banks and other financial institutions, earning commissions on interests. It aims to reach out to 28K+ MSMEs and disburse loans worth INR 50 Cr by 2022.

Deciml

Why Deciml Made It To The List

Micro-savings and micro-investments are all the buzz now as the desi gullak (piggy bank) gets a digital makeover. Although Indians are thrifty by nature and would rather save money for the future, smart investments to grow their wealth are often avoided due to a risk-averse mindset. The outcome: Investment penetration, especially in mutual funds, remains abysmally low at 17% compared to the world average of 75%. To help people become more disciplined investors with a twist of nostalgia, second-time entrepreneur Satyajeet Kunjeer launched Deciml in 2020.

The Pune-based investment tech firm allows people to auto-invest loose change from every online transaction into MF or fixed-return funds. For example, if a registered user buys a T-shirt worth INR 492, Deciml’s Android app will read the transaction SMS on the user’s phone, round it off to INR 500, and the balance – a very tiny portion of the total spend – will be secured for investment. Users can also put in a lump sum amount or make a fixed payment at a regular interval.

Deciml gets a commission on the total AUM from financial institutions where funds are invested. To date, 50K+users have come on board and invested INR 35 Lakh via this platform. The startup aims to introduce micro-investments in cryptocurrencies, build a consumer base of 2 Mn and earn $1 Mn in revenue by FY23.

Drona Pay

Why Drona Pay Made It To The List

Fintech in India is a $1.3 Tn opportunity, with digital payments and online lending accounting for $800 Bn. But here is the glitch. Frauds and scams have also grown with the rapid spread of digital services. Between April and September 2021, Indians lost more than $5 Bn to financial frauds, and this fast-growing pain point is bound to affect fintech and banking CX. Therefore, Drona Pay was launched in 2021 to help reduce delinquency, bust-offs, scams and merchant frauds across the UPI, BNPL, payment processing and debit and credit card space.

The Mumbai-based fintech SaaS startup provides three solutions: Transactional fraud tracking via an ML-based dashboard to find common compromise points and system vulnerabilities; a behavioural biometrics solution, basically an SDK, to ensure user biometrics are updated while institutions monitor cognitive behavioural patterns, and credit decision-making, where a dashboard helps fintech companies make lending decisions and manage onboarding risk.

Drona Pay offers subscription-based customisable API integrations based on the size of the organisation. The startup plans to go deeper into the fintech ecosystem by building an extensive team in 2022.

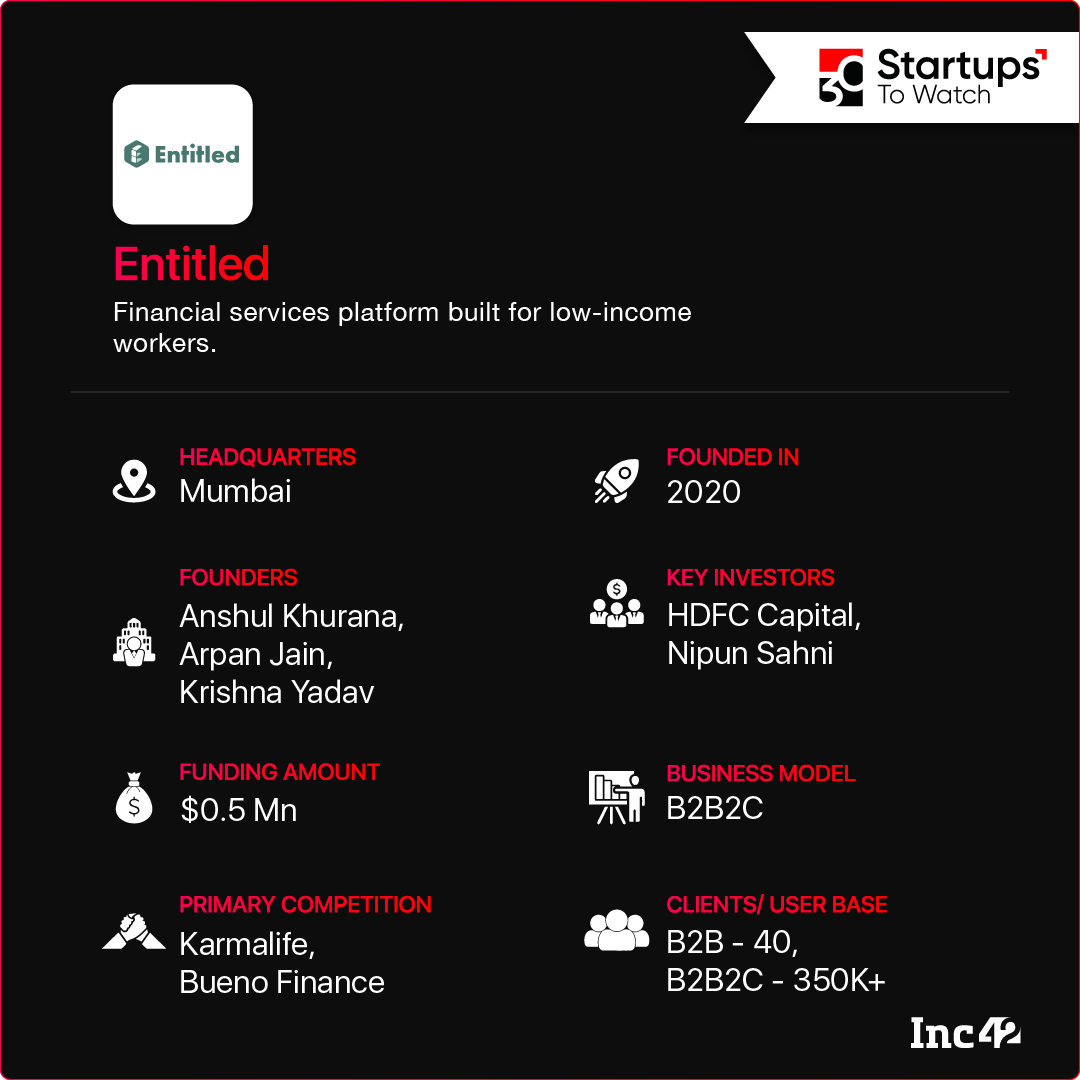

Entitled

Why Entitled Made It To The List

Fintech’s potential reach in India is limited to the top 53% who own a bank account and may have a credit history. This means a huge opportunity around financial inclusion of the middle- and lower-income segments. Mumbai-based Entitled decided to leverage this and launched operations in 2020 to cater to low-income workers.

The B2B2C lending tech firm builds financial profiles of low-income workers (income under INR 2 Lakh per annum) using alternate behavioural data points (expense history, social circles, intent for repayments and more) and provides small-ticket fintech products like loans, insurance and savings schemes.

To enter its target market, Entitled has partnered with companies like Swiggy, Quess, LetsTransport and NIYO and provides their gig workers with useful financial products and services. These include salary advances, personal, medical and consumer loans, digital gold schemes and primary health insurance in tune with their lifestyle and requirements. The startup also helps blue-collar workers reap the benefits of government schemes like PF, Employees’ State Insurance (ESIS), Ayushman Bharat and Atal Pension Yojana by assisting them to check eligibility criteria and enrol for the same.

The platform does not charge employers who provide these services as part of their employee benefits programme. However, it earns a commission on the financial transactions carried out by partner institutions and charges a fixed fee on non-financial services. Entitled claims a 26% MoM revenue growth and eyes an ARR of INR 7.8 Cr in FY23 by catering to 2 Mn+ gig workers. By 2025, it plans to go beyond blue-collar workers to other LMI segments.

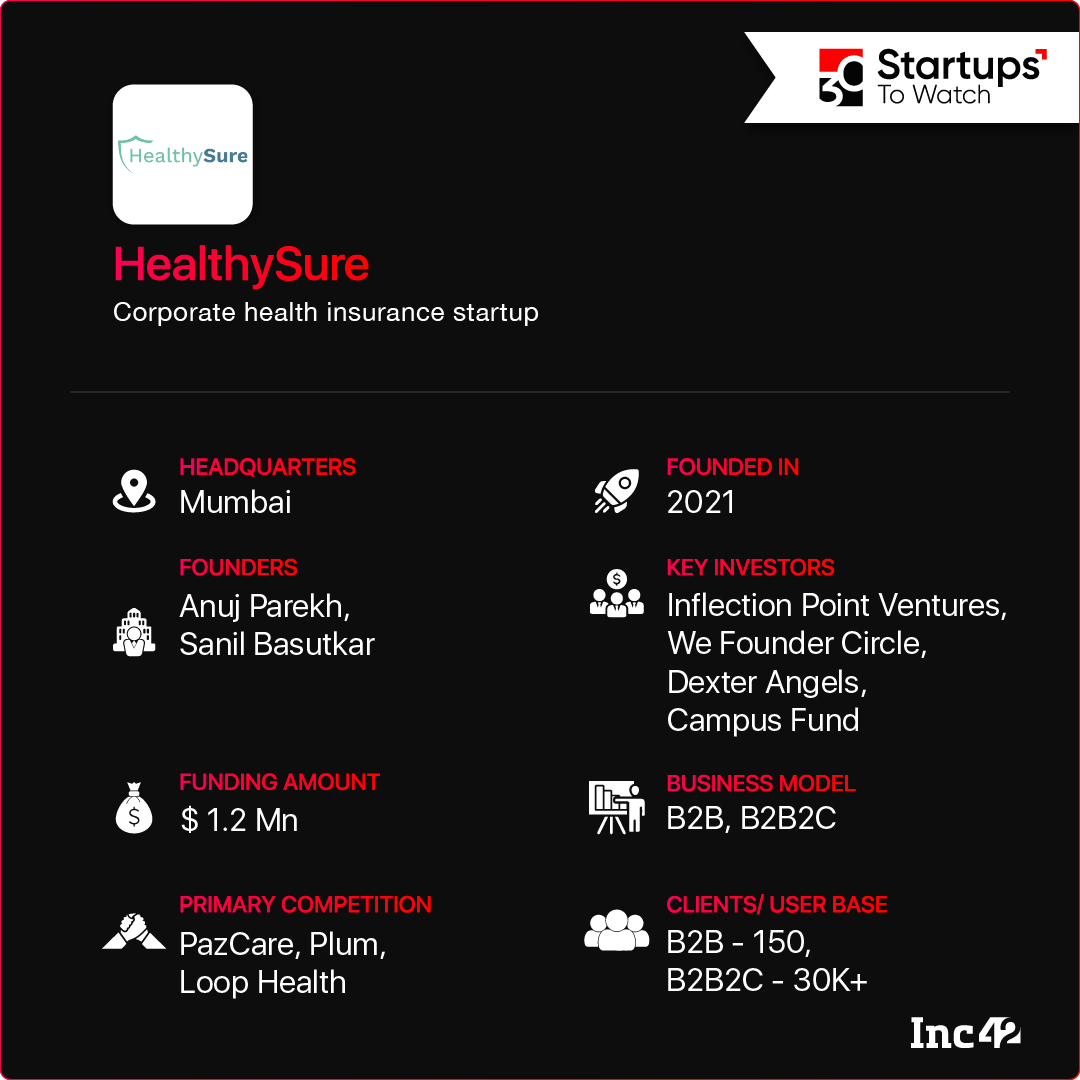

HealthySure

Why HealthySure Made It To The List

Corporate health insurance policies significantly boost the insurance sector in India, although the overall penetration of the industry (life and non-life) is relatively low. On top of it, corporate healthcare is not adequate for individuals for a couple of reasons.

First, the sum assured may not be enough in many cases. Second, an employer-provided policy may not get converted into an individual policy in case of a job switch/loss. Of course, IRDAI has a provision for the same, but it depends on the insurer. As a result, most employees are compelled to buy additional health insurance or pay out of pocket. Mumbai-based HealthySure intends to bridge this gap with its flagship product, Unified Health Insurance.

Launched in 2021, HealthySure has come out with corporate health insurance programmes ranging between INR 50 and INR 3,000 and offers additional services, including teleconsultation, physical and mental wellness checkups and discounted pharmacy purchases and lab tests. But here is the USP. The insurtech startup allows employees to upgrade their corporate health plans and add INR 30 Lakh of extra coverage for an additional INR 1,000. It further enables them to save up to 90% on an independent policy and get the added advantage of continuing the policy in his/her personal capacity after leaving the company.

HealthySure earns commissions on corporate policies and additional insurance coverage taken by employees. The startup claims to have more than 30K employees across 150+ companies and has done business worth $1 Mn in FY22. It aims to increase its sales to $4 Mn by serving more than 1.5 Lakh customers in FY23.

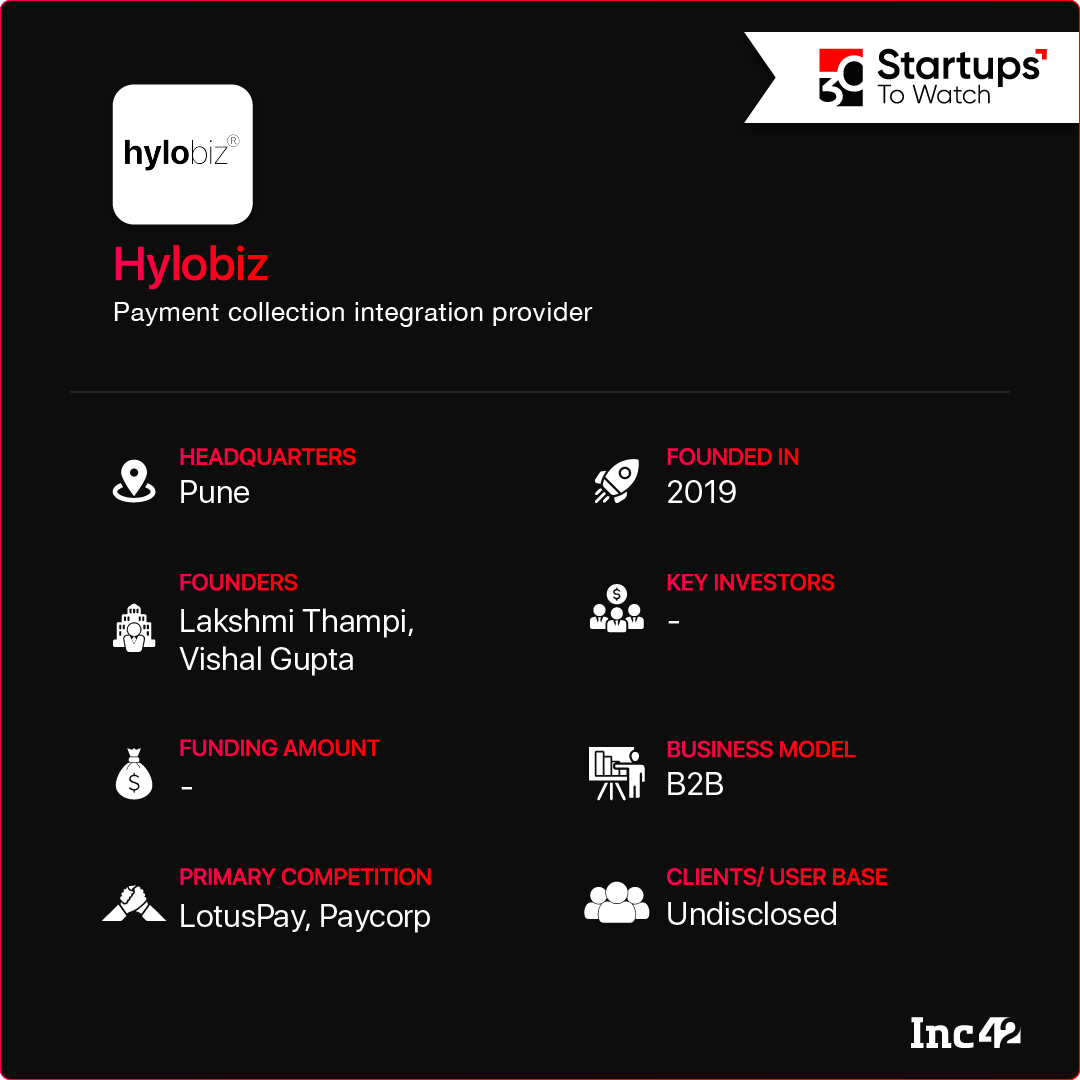

Hylobiz

Why Hylobiz Made It To The List

Although we have entered the digital-first era, legacy systems and traditional tools continue to hold back small and medium businesses from achieving their true potential through optimum digitalisation. Generic solutions do not help companies, either. For instance, many dukaan tech companies that digitalise mom-and-pop stores are now available in the market, but there is not much differentiation. In contrast, Bengaluru-based Hylobiz is building a specific solution for SME supply chain players.

Set up in 2019, Hylobiz specialises in working capital management, automated payment reminders, auto-reconciliation and integration with major ERPs. Simply put, it digitalises the value chain by helping businesses with various tasks such as invoicing, collections, payouts, inventory and working capital solutions, including business loans, SME credit cards and invoice discounting. The startup earns through a mix of monthly SaaS subscriptions and transactional fees. It plans to onboard 20K+ SMEs in India and the UAE and eyes an ARR of $3 Mn by FY23.

Hypto

Why Hypto Made It To The List

Chennai-based Hypto was launched in 2018 to help ecommerce players connect to open-source fintech solutions. However, the finance platform pivoted in early 2022 to serve crypto exchanges as ease of payments has become a coveted feature in the blockchain domain. Hypto enables fiat currency (INR) deposits and withdrawals across crypto exchanges and NFT marketplaces. It also ensures custody, safety and security of fiat money rails through solutions built for exchanges operating at scale.

Suppose a crypto exchange wants to add a payment feature (IMPS, NEFT, RTGS or UPI) to its product. In that case, Hypto leverages its connections with multiple banks and NBFCs to provide a low-code, simple API that can be easily integrated. Crypto exchanges are also allowed to create individual accounts for their customers. Hypto charges a variable fee on each transaction made through its APIs and tools.

Jify

Why Jify Made It To The List

Around 80% of the Indian workforce, especially the blue- and grey-collar employees, live from one pay cheque to another. Most of them lack adequate savings, so any contingency or unforeseen expenses compel them to opt for high-cost predatory credit, impacting their financial well-being. Mumbai-based Jify aims to build an inclusive financial ecosystem for this underserved segment.

Since its launch in 2021, the startup has operated as an earned wage access platform, addressing the short-term liquidity issue. Jify has also developed a ‘Smart Spend’ feature, prepaid cards and digital payment options. In addition, it offers a financial advisory tool to help employees save money and meet their financial goals. An employee has to log in to Jify’s android/iOS app with the company name and employee code to access the earned salary, courtesy of Jify’s partnerships with NBFCs. However, the amount must be returned on payday.

The ‘earned wage’ feature is free for employees, and Jify earns via transaction processing fees. Companies need not pay anything, but their attendance and payroll systems must be integrated with the platform. The startup uses this data to provide real-time earned-salary access to employees. As a young company, Jify wants to reach out to its target audience more aggressively and plans to launch educational videos to nudge its users into savings.

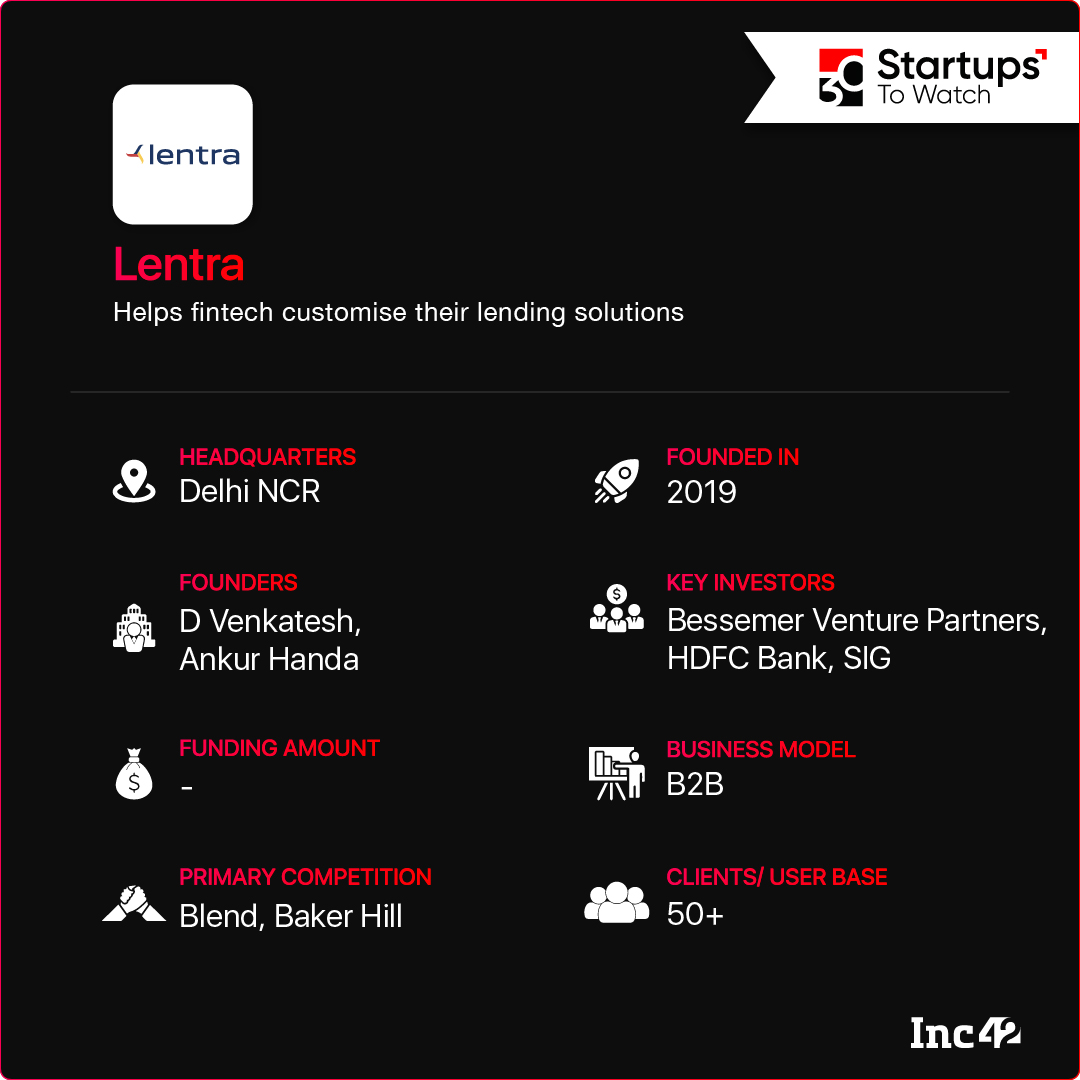

Lentra

Why Lentra Made It To The List

For a long time, India’s financial ecosystem was synonymous with legacy institutions like banks and FIs, with little scope for mass inclusivity or large-scale access to essential financial tools like lending, insurance or investments. But with the rise of new-age tech across financial services, the focus is now on greater inclusion and access. In sync with the fast-changing landscape, former Softcell Technologies executives D. Venkatesh and Ankur Handa envisioned replacing the traditional lending system (read on-the-ground and paper assessments) with cloud-native backend solutions. So, Pune-based Lentra was launched in 2019.

The lending tech SaaS platform offers various solutions across BNPL, open credit enablement networks, account aggregation, anchor financing, credit card, small-ticket loan and other co-lending solutions. For banks and NBFCs, it provides a low-code, API-driven architecture to launch B2B lending products such as agri loans, vehicle financing, supply chain financing and loan against property. In the B2C category, the startup covers home, personal, auto and education loans. Lentra hosts eight lending products on its platform and offers auxiliary services such as loan processing, credit bureau access, communication and video KYC tools (for bankers), a loan management dashboard and a loan application evaluation tool, among others.

So far, the startup has serviced 50+ FIs and processed more than 13 Bn transactions. Its end goal is to help banks digitise their systems using Lentra’s embedded tech, offer tailored lending experiences, increase customer efficiency and bring down NPAs.

MoneyyApp

Why MoneyyApp Made It To The List

The creator economy in India is worth $10 Bn. But creators, or most solopreneurs for that matter, still manage their finances using pen-and-paper or traditional spreadsheets, although the latter could be too complex for new users. Launched in 2021, MoneyyApp’s B2B platform acts as an end-to-end finance management tool for creators, keeping things both simple and effective.

The Bengaluru-based startup helps them track and manage previous and upcoming earnings on a single dashboard and allows them to create invoices and send payment reminders on time. It also enables expense tracking and filing tax returns through the startup’s Android and iOS apps and gets business loan approval from partner banks.

MoneyyApp charges a commission on every transaction and provides the analytics dashboard for an annual subscription fee. The company claims to have 8K+ creators on board but plans to take the number to 50K and eyes $3 Mn in revenue by FY23.

OmniCard

Why OmniCard Made It To The List

Despite the widespread usage of digital payments in India post-demonetisation, less than 30 Cr people, or 21%, use online payment methods as easy-to-access, easy-to-use and reliable systems are not always available. Also, many users have trust issues and prefer to pay offline. Keeping these pain points in mind, Noida-based OmniCard is building a comprehensive payment ecosystem wherein users can use online and offline features such as the UPI, tap-to-pay and ATM withdrawal.

Launched in 2018, OmniCard claims to be a debit card challenger. One can download the android/iOS app, get the KYC done (it takes less than one minute) and get a RuPay card for online and offline payments, including ATM withdrawals. Users can also transfer the money from their bank accounts to OmniCard wallets for merchant payments.

One can generate cards for family members (each will have his/her wallet) and manage the entire family’s expenses from one place. The idea of OmniCard is to create a security line between users and their bank accounts, protecting them from increasing card-based scams.

The fintech startup charges a processing fee on every transaction and claims to have a user base of 500K. It aims to expand to 3 Mn users by FY23 and 50 Mn+ by 2025 as a go-to solution for spending, payment and money management needs. It will also introduce a keychain payment feature (a tap-to-pay feature) on OmniCard-created physical keychains.

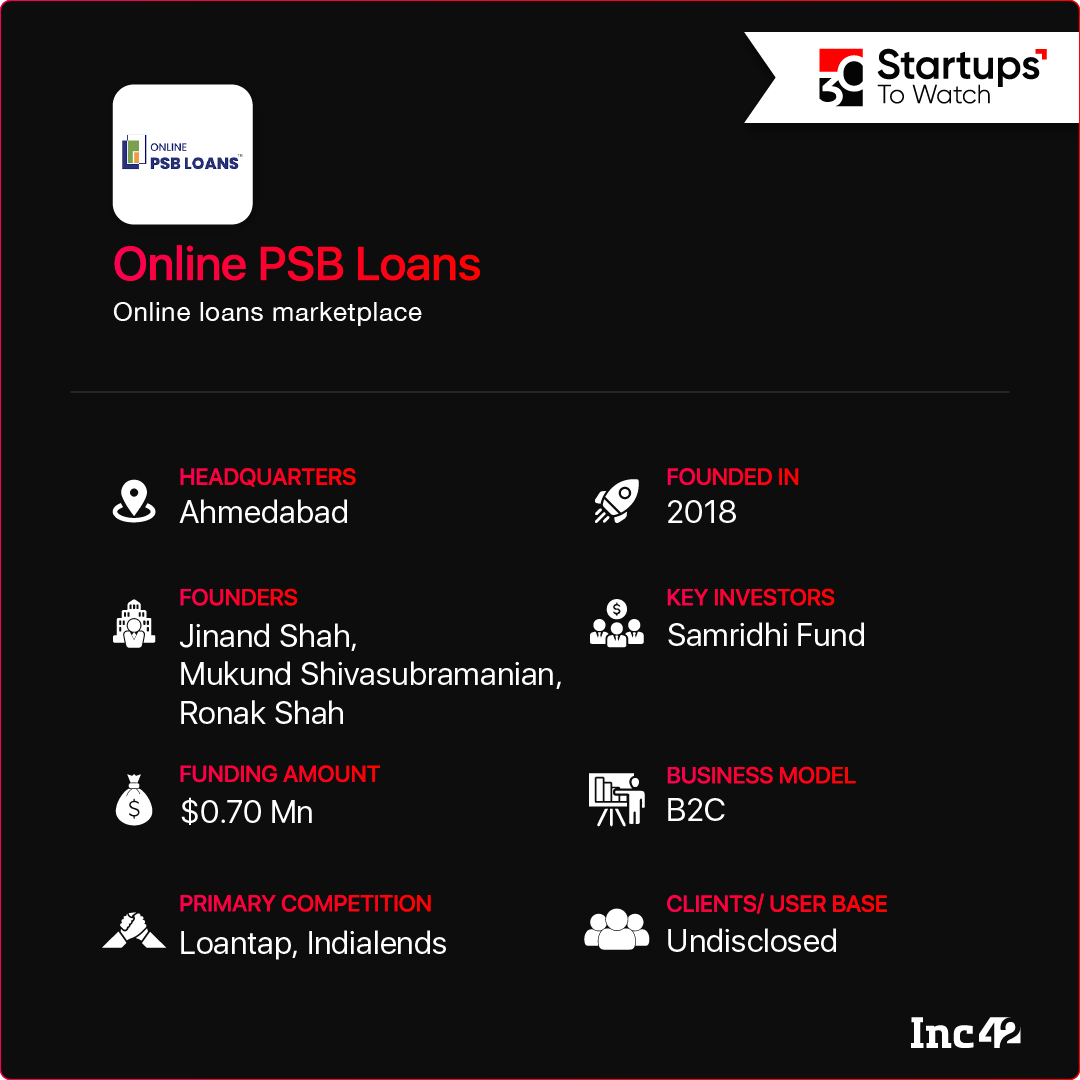

Online PSB Loans

Why Online PSB Loans Made It To The List

Thanks to the boom in the Indian credit economy, especially in the quick credit space, startups like Ahmedabad-based Online PSB Loans are gaining prominence. Launched in 2018, this one is a credit marketplace that helps B2B and B2C borrowers meet their financial aspirations. The startup works with more than 20 FIs to provide business and retail loans to MSMEs and individuals in the form of mudra, personal loans, home loans and auto loans. Better still, these loans can be processed in under one hour.

This is how it works. A user needs to sign up and build a profile on the company’s web platform. Next, a dashboard will showcase loan products from various banks and financial institutions in sync with the user’s requirements. Individuals can use their PAN numbers to check their loan eligibility, while businesses use TAN for raising loans.

The startup charges a convenience fee from borrowers and lenders and has helped disburse more than INR 70,000 Cr in loans.

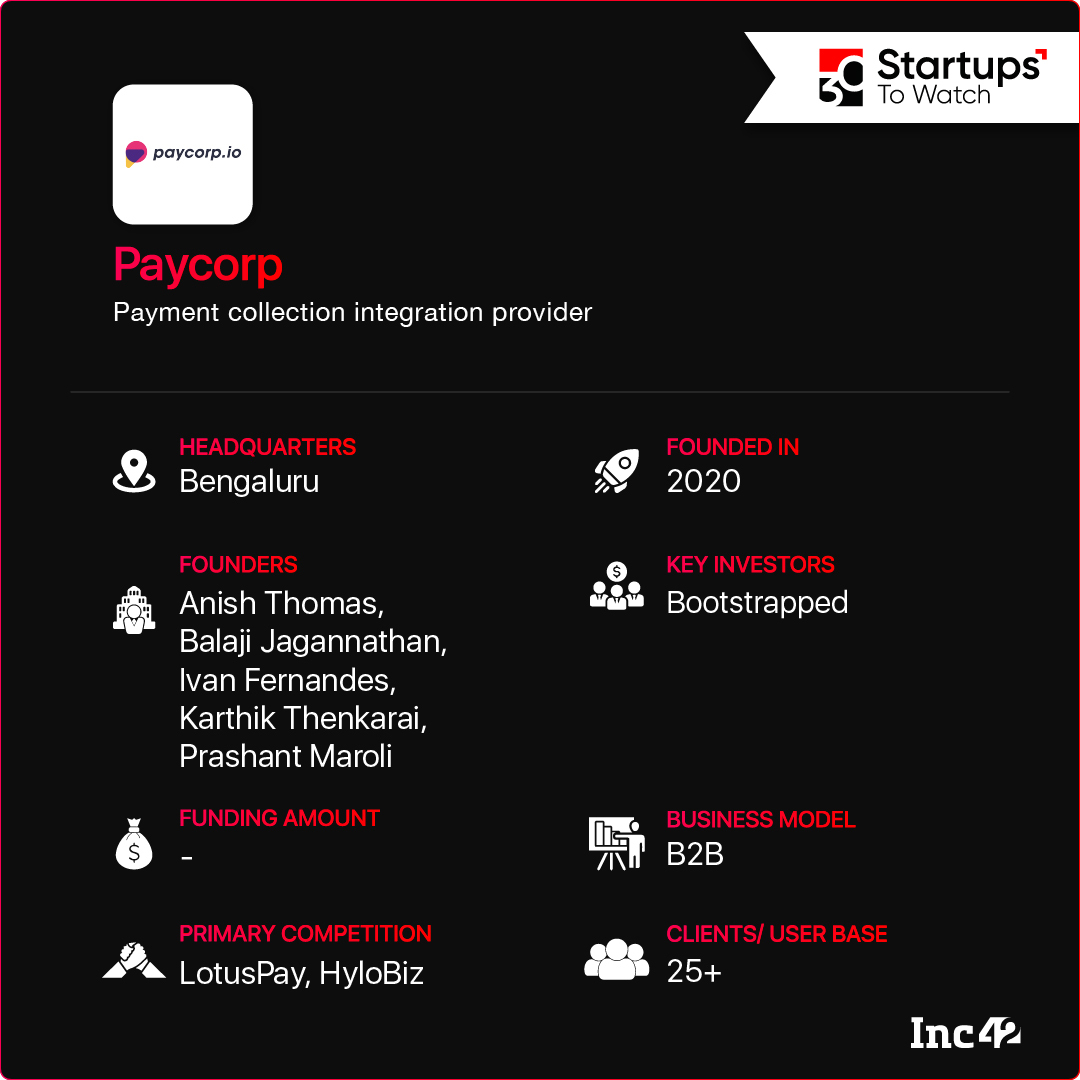

Paycorp

Why Paycorp Made It To The List

The peer-to-peer (P2P) and peer-to-merchant (P2M) payment segments in India flourished in the past five years due to record UPI transactions. But the same did not happen in the recurring payment space where auto-debit is mandated on credit and debit cards enabled between merchants and customers. This can be both paper and digital mandates, but irrespective of the format, 35 out of 100 auto-debits fail, according to Bengaluru-based Paycorp. Every failed mandate costs INR 150, and these losses can quickly accumulate, eating into a company’s revenue.

Paycorp was launched in 2020 to offer a SaaS-based recurring payment and e-mandate platform that would do away with operational glitches. Currently, most businesses use manual means to process collection requests on due dates, which are settled after two working days. In contrast, the fintech startup digitises all recurring payment requests on behalf of its clients and partners with banks to procure the money on the same day, thus saving float on receivables. It also provides a predictive analytics dashboard to help businesses identify potential defaults.

Paycorp also has an API for banks, enabling them to onboard corporate clients and their payment businesses.

The company currently collaborates with eight banks for its B2B clients and has a pay-as-you-go pricing model. It plans to launch a recurring rental payment platform in July, aims to work with 25 banks and start its operations in the Middle East by the end of this year.

PayKun

Why PayKun Made It To The List

Consumer internet is estimated to emerge as a $1.6 Tn opportunity by 2025. But this can only be possible if business platforms are built with robust payment features. Aware of this imminent requirement, PayKun was launched in 2018 to develop payment gateway solutions for digital businesses like ecommerce, gaming, IT, SaaS and OTTs.

Based in Bhavnagar, Gujarat, PayKun offers a plugin and SDKs so that digital businesses can provide their customers with 120+ payment options, including net banking, card payments, UPI, mobile wallets, QR codes and others. It has also come up with payment buttons and links to help improve consumer conversion on the web and through apps. Additionally, PayKun provides an analytical dashboard to help businesses track sales data and develop business strategies. The startup does not charge any setup or integration fee apart from a trade discount rate (TDR) of 1.75% on every transaction a merchant does.

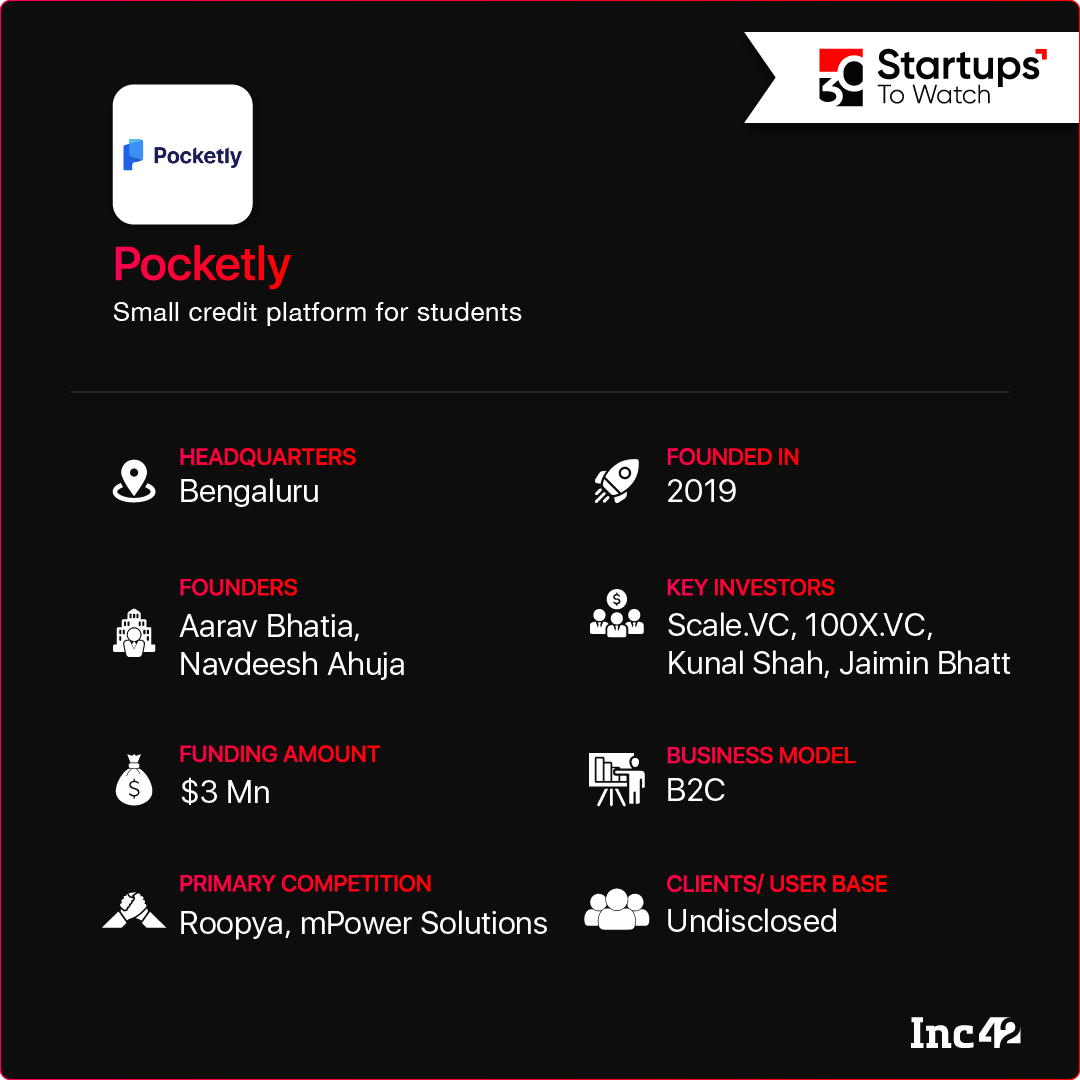

Pocketly

Why Pocketly Made It To The List

Although microlending solutions are on the rise, users still require credit scores to qualify for loans. The problem gets tougher for first-time borrowers without any credit history. So, Pocketly was launched in 2019 to tap into this market. The Bengaluru-based startup targets college students, helps them take small-ticket loans for the first time and thus builds their credit scores.

Pocketly offers loans for 60 days and earns via interest commissions on loans extended through its credit line. Users need to register with its Android/iOS app to raise a collateral-free loan of up to INR 10K. The startup has partnered with Fairassets (a P2P lending marketplace), LiquiLoans (a loan facilitator) and Speel Finance (an NBFC) to finance these loans. It has already disbursed loans worth INR 1,000 Cr+ and plans to expand its product range by including BNPL services.

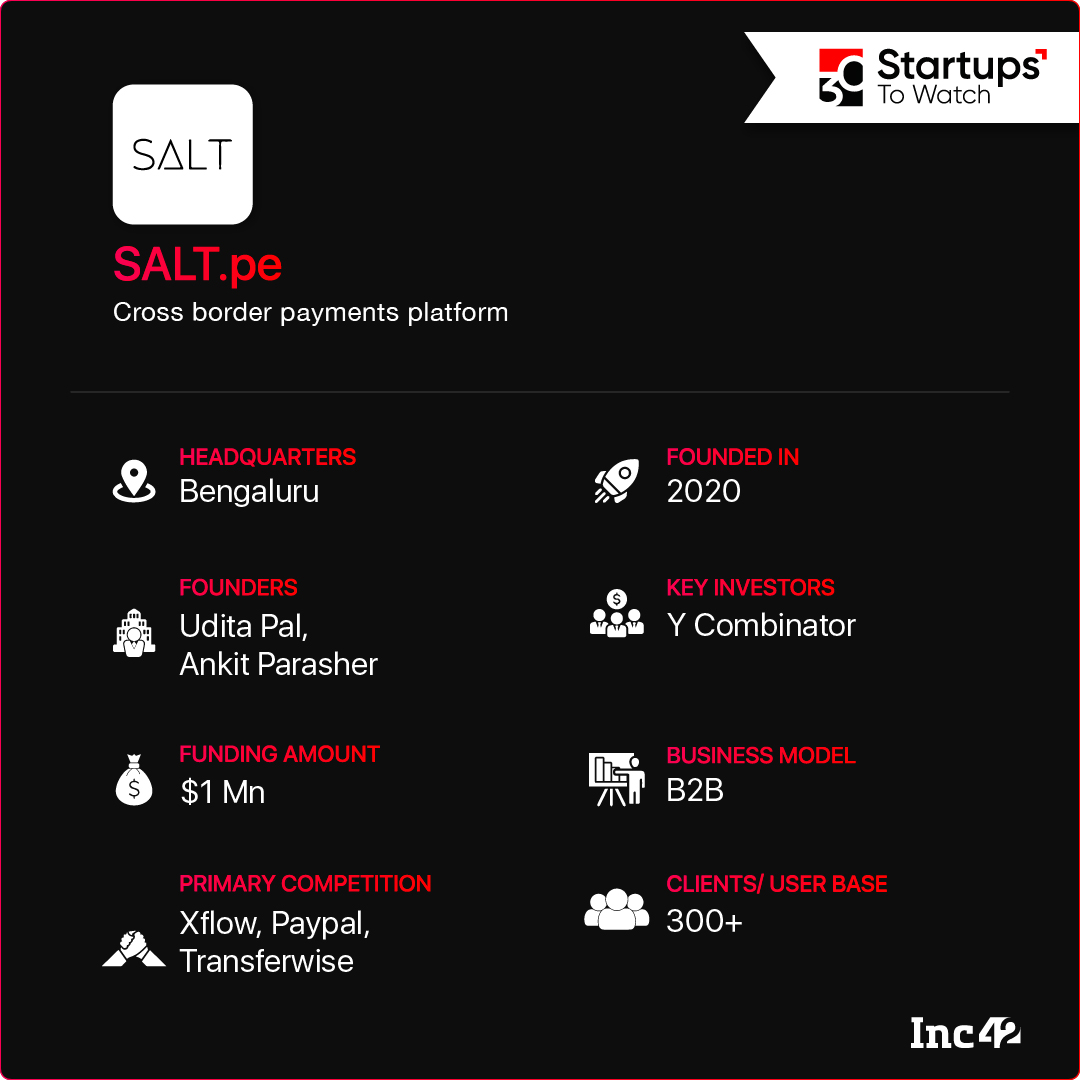

SALT.pe

Why SALT.pe Made It To The List

Cross-border payments are often a hassle due to lengthy processing time, high cost and inadequate digital support. SALT was set up in 2020 to address this pain point as founders Udita Pal and Ankit Parasher earlier struggled with overseas remittances. Eventually, the duo returned home and launched the startup that simplifies global payments and documentation, digitises the process and speeds up foreign remittance, forex conversion, contract and invoicing management and credit facilitation.

The Bengaluru-based startup currently offers two products. Its flagship Inward Remittance enables small businesses to remit money by creating virtual accounts across the UK and the US. The second product, Table by SALT, is still in beta. It is a tool for early stage startup founders raising funds from foreign investors, helping automate fundraising, banking and compliance work.

The SaaS startup allows businesses to set up virtual foreign currency accounts by partnering with banks and financial services across 50 countries and six currencies. Companies are charged a percentage on each transaction. With 300+ clients on board, SALT claims to have completed $10 Mn+ transactions between March and May 2022.

The fintech firm will expand its use cases to other cross-border banking solutions and compliance workflow automation, planning to make remittance as easy as using the UPI by 2025.

Samudai

Why Samudai Made It To The List

Think Web3, and one is bound to wonder how blockchain, DAOs, decentralised operations and eventually, a tokenised economy will become an integral part of that journey. In other words, Web3 tech will soon rule the fintech landscape, and it is crucial to look at the next level of development that will redefine the ecosystem. So, VIT alumni Kushagra Agarwal and Navin took the plunge and launched Samudai in January 2022 to help communities build seamlessly within the Web3 space without worrying about operational issues.

The New Delhi- and Singapore-based startup is working on a suite of tools that will allow Web3 professionals to build communities and facilitate collaboration via a Web3 native project management framework. Plus, there will be community management tools such as team graphs, an analytics dashboard and a roster-style platform. It is also developing a proprietary and verifiable reputation metric called Bushido to identify authentic contributors.

The platform will be launched in private alpha in July for a small group of users and in public beta in Q4 CY22.

Toppeq

Why Toppeq Made It To The List

As venture capital investments pour into the Indian startup ecosystem, the need for digitising equity ownership records also rises to ensure transparency and business clarity. With that notion, Mumbai-based Toppeq was launched in 2019 to help investors make informed decisions while funding private companies while founders can maintain comparatively clean cap tables.

The web-based platform has a subscription model and offers service bouquets for investors and founders. For investors, these include a portfolio management service that digitises equity and working capital data of portfolio companies, the Q-Insight to review shareholder agreements and other relevant rights and obligations and LP Reporting that allows fund managers to monitor and compare business performances.

For founders, these services include cap table management, working capital management (tool to be integrated with accounting software for tracking funds), ESOP management to generate reports regarding grants, schemes and vesting of stock options, and a WhatsApp-based digital ledger called Q-Bot. Investors and their portfolio companies only need to upload their existing PDFs and excel sheets. Toppeq will cut through data chaos and native systems to create a clean visual dashboard on the web.

The company aims to capture at least 5% business of the Indian startup ecosystem and expand in the US and the EU by 2025.

Tradetron

Why Tradetron Made It To The List

Most stock market traders/brokers have an operational strategy in place. But building and automating these for online stock trading can be a tough task that requires time and money. Enter Tradetron, the brainchild of Umesh Ranglani, a former fund manager and software developer.

Launched in 2020 in Mumbai, the no-code platform helps traders to build algo trading strategies using a virtual simulation, which can be applied to stocks and positions. Simply put, on Tradetron, traders can set the conditions and strategies for their trades, input multiple strategies over time or replicate others’ strategies. One can create a web/mobile interface that can be directly connected to their broking accounts, including Demat, SIP or gamma scalping accounts, to get actionable insights via WhatsApp, SMS or email messages.

The startup specialising in trading algo automation has applied for a U.S. patent for the algorithm-maker that connects with eight exchanges and covers stocks, options, commodities, currencies and cryptocurrencies.

Tradetron has a subscription-based revenue model and claims 30K+ algorithm deployments for 8 Mn+ trades every month as 70+ brokers in the US and India use the solution. It recently tied up with Paytm Money and 5Paisa to provide a white label solution wherein the Tradetron engine operates at the backend to help traders automate their activities. The fintech SaaS startup is now building a backtesting engine (a platform that will run the trading simulation) to speed up the application of the patent-pending algorithm.

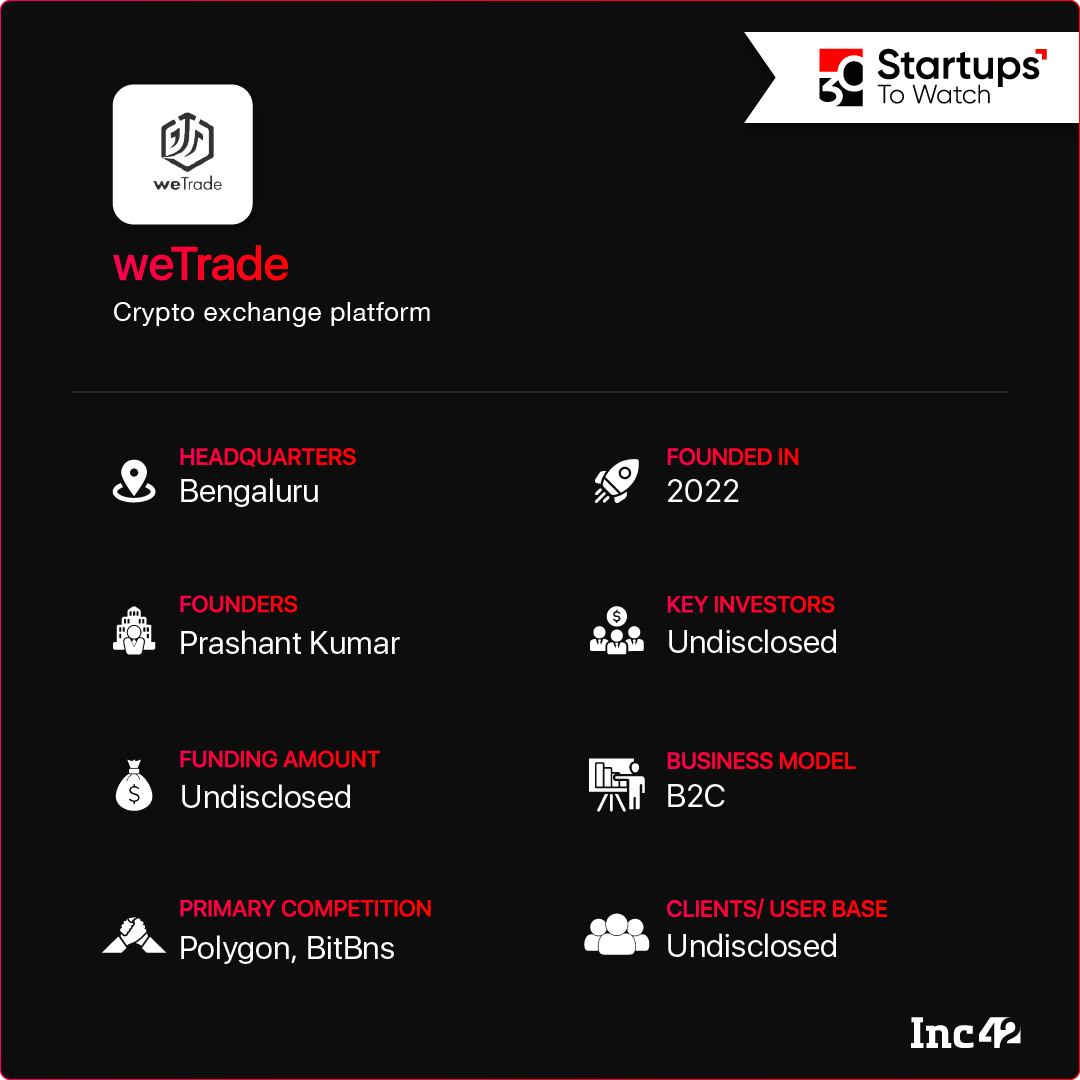

weTrade

Why weTrade Made It To The List

Crypto investments in India can be split into two broad categories. On the one hand, crypto exchanges offer various currencies, but profits, in such cases, solely depend on market movements. Then there are blockchain-powered startups that help generate steady returns on crypto-assets by investing them against stablecoins like USDT and USDC. Bengaluru-based weTrade has been building an investment platform for crypto users since January 2022 to help them reap the dual benefits of price appreciation and multiplying rewards for every validated block.

The platform works at the intersection of smart deposits and stablecoins. Users can download the Android/iOS app where weTrade offers 10+ cryptocurrencies, including Bitcoin, Ethereum, Dogecoin and more. Just five months into the launch, weTrade has onboarded 10K+ users who can buy and sell cryptocurrencies and trade their crypto assets against USDT and USDC. This ensures steady returns irrespective of market fluctuations. For further growth, the startup banks on its hassle-free user experience, including a less-than-one-minute KYC, built-in investment and tax advisory and insurance coverage for wallets.

The Bengaluru firm currently charges a transaction fee on both buying and selling. The platform is still in the works and plans to add a ‘smart deposit’ feature to the app besides growing its user base to 1 Mn by the end of this year. By 2025, it aims to create an educational layer for crypto investors with the help of community channels and interactive videos from experts.

Whrrl

Why Whrrl Made It To The List

Warehouse receipt financing is all about using stored commodities as collateral for securing loans. For example, a small or medium business or even a farmer keeping their inventory at a certified, independent facility can raise a loan against the goods stored there. But there is a glitch. The process is mainly manual, and lenders often have to deal with scams and fraud, while credible borrowers are left in the lurch.

Mumbai-based Whrrl was launched in 2019 not only to digitise the entire process and make it more efficient and convenient but also to bring blockchain into the equation to ensure credibility. The startup’s flagship product is a service suite for banks that creates blockchain-powered document profiles of warehouses, collateral managers and borrowers. With blockchain in use, risks of generating fake/duplicate warehouse receipts, ghost collateral lending and multiple lending are largely eliminated, further reducing underwriting costs.

Whrrl also acts as a marketplace, connecting lenders and borrowers and enabling an end-to-end digital lending process. It charges a platform usage fee of 0.25-0.35% per annum from all users, an annual customer acquisition fee of 2-5% of the loan amount from banks and a licence fee from warehouses for using the Whrrl infrastructure. The platform is now free for borrowers (farmers/traders), but it plans to charge a commission on each loan.

Winvesta

Why Winvesta Made It To The List

Forex cards have limited utility in India, but the same cannot be said for countries like the US and the UK, where users can make cross-border investments and savings. Founded in 2019 by former Deutsche Bank executives Swastik Nigam and Prateek Jain, Winvesta is building a cross-border fintech platform for everyone – whether you are an individual looking to invest overseas or an exporter getting paid by foreign buyers.

The Mumbai-based startup offers two cross-border neobanking solutions – an international investment account set up via its Android/iOS app and a business account that accepts payments in more than 30 currencies. Winvesta accounts can be used to fund overseas savings (for education) and investments and receive overseas payments. Or an account can be opened here before going abroad. It charges transaction fees on foreign exchange value and investments.

Currently operational in India, the UK and the US, Winvesta plans to expand its footprint to 30+ countries by 2025.

Zyro

Why Zyro Made It To The List

Corporate cards are all the rage nowadays as they help companies streamline employee expenses without depending on paper bills and ensure instant payments. Therefore, Noida-based Zyro, an expense management startup for businesses, has come up with many solutions, including pay-out services through virtual and physical cards, in-built expense management modules and pay-in services such as PoS, link- and QR-based payment collection and invoice generation.

Launched in 2019, Zyro has a co-branding agreement with NSDL Payments Bank and tie-ups with the ICICI Bank, HDFC Bank and Axis Bank to allow companies (especially startups and SMEs) to manage employee expenses. Corporate clients need to sign up and link/open their savings and current bank accounts with Zyro. After that, they can offer their employees expense cards, travel cards, fuel and meal cards, gift cards and payroll cards. With 100+ businesses as its clients, the startup is eyeing a subscription-based revenue of INR 20 Cr in FY23.

In the future, Zyro intends to obtain a PPI licence in FY23 and bring every financial aspect of a business under its ambit, including cross-border payment, tax filing, subscription buying and utility bill payments.

[Edited By Sanghamitra Mandal]

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.