![[What The Financials] Closing In On Unicorn Club, Curefit Needs To Shed Its Losses](https://asset.inc42.com/2020/02/Untitled-design-17-490x360.jpg)

SUMMARY

The company has raised over $365 Mn over multiple funding rounds

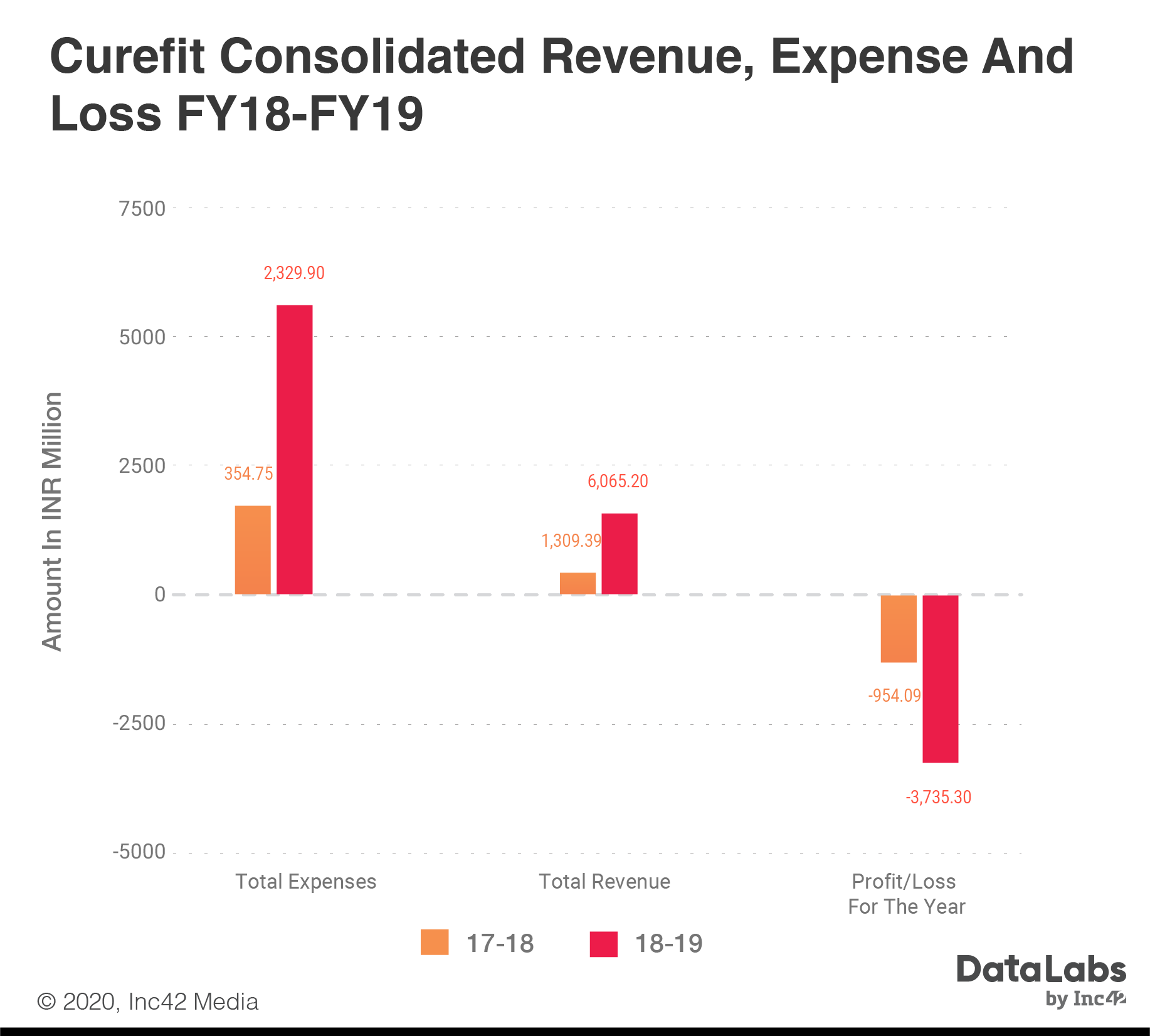

On a consolidated level, Curefit has grown its revenue 5.56X while its expenses grew 3.63X

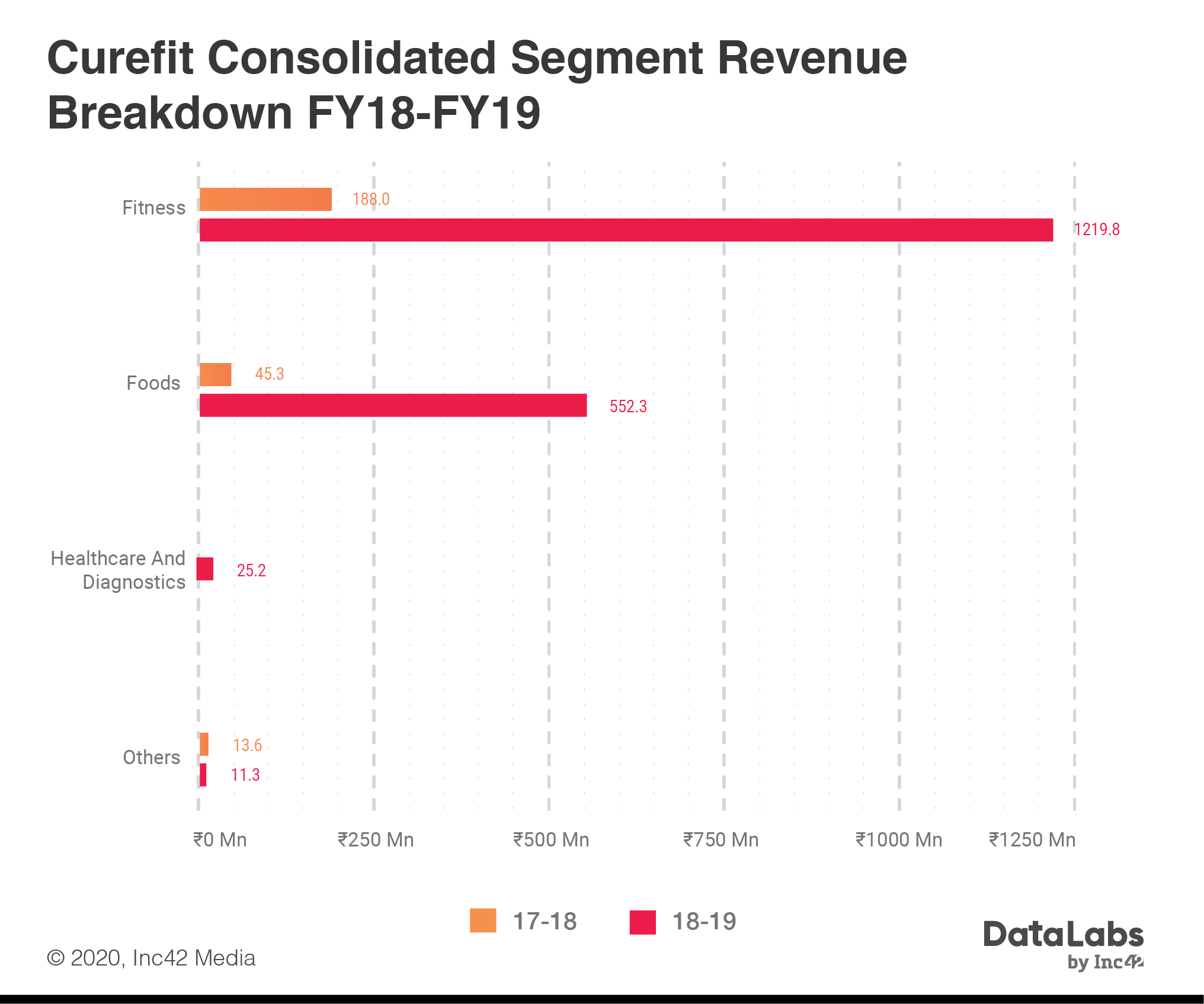

In terms of revenue, the fitness business has grown 5.48X

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

What The Financials

Inc42 unveils and deciphers all the important financial metrics of Indian startups across industries. Find out revenues, unit economics, profit & loss and all the important financial metrics to judge how the startup will perform in the coming years.

The Indian healthcare industry has been growing at a tremendous pace owing to increased penetration of technology, improved connectivity, and enhanced healthcare policies. And aligned to healthcare, the Indian market has the fitness and wellness startup Curefit

What began as an app to book gyms, the Mukesh Bansal and Ankit Nagori-led company now caters to all segments within the health and fitness sector, including physical fitness through Cult.fit, mental wellness and yoga in Mind.fit, food delivery and diet recommendations through Eat.fit and medical and diagnostic centres Care.fit, as well as groceries through Whole.fit.

Curefit claims to have over 180 Cult.fit physical fitness centres and more than 35 Mind.fit centres in six Indian cities — Mumbai, Chennai, Jaipur, Bengaluru, Delhi NCR and Hyderabad — with customers booking sessions through an app.

The company has raised over $365 Mn over multiple funding rounds from investors like Chiratae Ventures, Accel Partners, Kalaari Capital, and Oaktree Capital among others. Over the last few years, the company has grown significantly in terms of customers as well as investor interest.

This has aligned well with the company’s financial performance too, as filings show. The company’s financial results for the year ending March 31, 2019, shows that it has grown its revenue 5.56X while its expenses grew 3.63X leading to 2.9X increase in losses on a consolidated level.

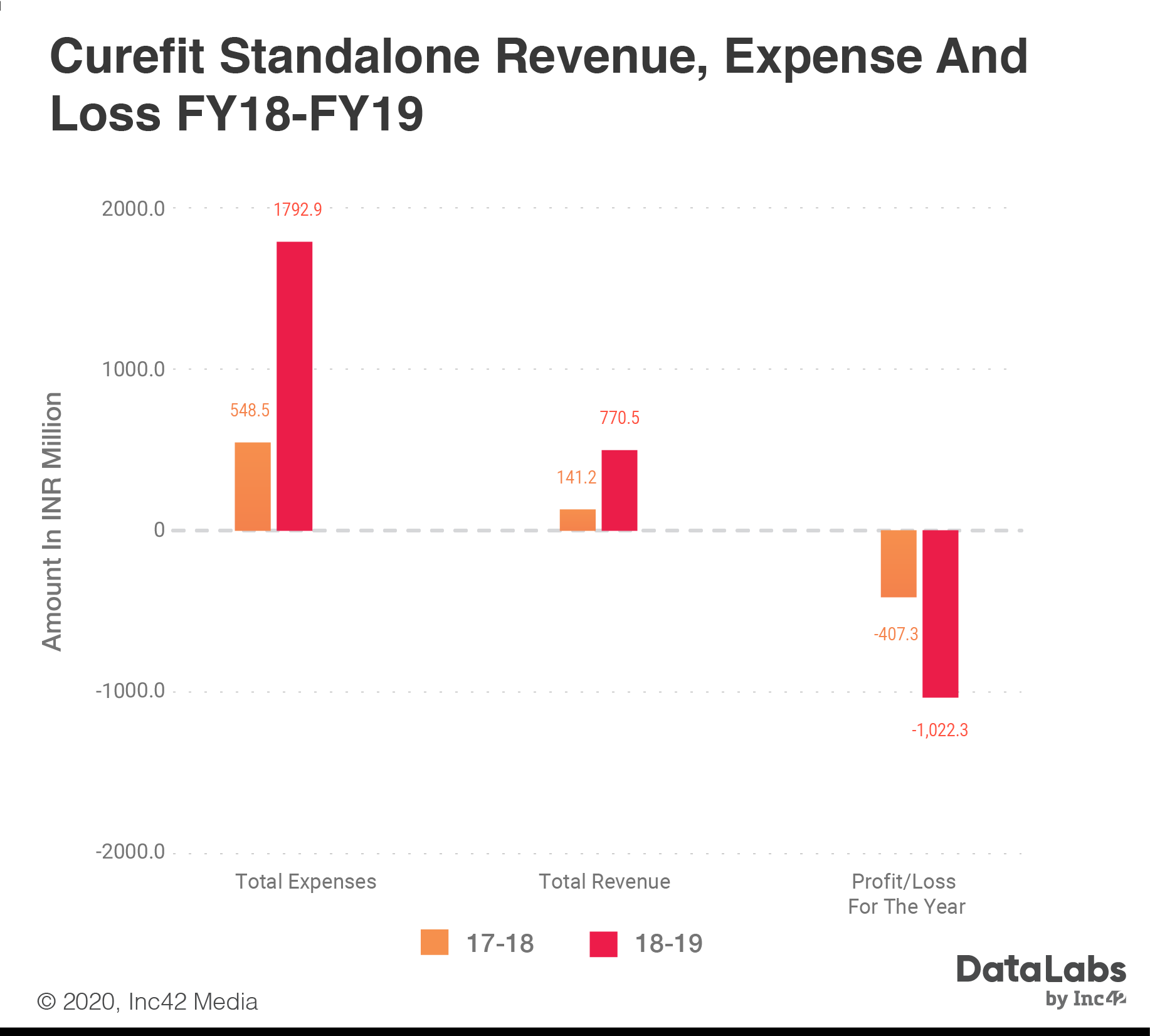

Notably, Curefit has multiple entities for its separate functions as well as website. Parent company Curefit Healthcare announced standalone and consolidated results for each business. Filings show that Curefit Healthcare is “primarily engaged in the business of providing management services (management support and brand building/marketing services) to its subsidiaries.”

Hence, the company’s standalone income and expenses are mostly supported income and costs. In FY19, on a standalone basis, Curefit reported a revenue of INR 77 Cr, with total expenses of INR 179.2 Cr leading to loss of INR 102.23 Cr.

In the filings, Curefit’s board noted that “the company is in its nascent stage and is focusing on attaining growth through scale and customer retention, hence the operating expenses of the Company are in excess of its revenue and as a consequence, the company has incurred losses during the year.”

Curefit’s Revenue Run

With multiple divisions and access to a differentiated audience for the health sector, Curefit has opened itself to multiple revenue-generating units. Interestingly, Curefit has adopted an acquisition-led strategy to expand and scale its platform. For instance, Cult was acquired by the company in August 2016 for $3 Mn. Since then, it has acquired startups such as Tribe Fitness, Seraniti, Kristys Kitchen, and a1000yoga.

It could be said that its acquisitions are reaping in money as income has grown, even though the costs associated are larger.

In terms of revenue, the fitness business has grown 5.48X reaching INR 121.98 Cr in FY19. At the same time, the foods business with Eat.fit has also grown 11.2X reaching INR 55.25 Cr. This could be much higher in the next fiscal with the introduction of groceries.

One of the interesting details was that the company’s income from platform fees doubled, while its sale of products business showed INR 12.5 Lakh revenue.

Burning Cash Instead Of Calories

While burning cash seems to be the easiest ways to get new users in consumer services and B2C models, the focus of the VC ecosystem these days is on lean businesses, that can acquire customers through innovation and product development rather than splurging on discounts. Admittedly, Curefit used some of the cash it raised from investors and its founders for the boost in the customer base and is now spreading those acquired users across various pockets in the health and wellness consumer sector.

When we look at Curefit’s cash burn it is to be remembered that the company operates fitness chains, for which it has to invest in the rent, equipment, trainers, basic expenses etc. Even though Curefit is not the most affordable fitness chains in the country, its per-user revenue is questionable in the face of these costs.

![[What The Financials] Closing In On Unicorn Club, Curefit Losses Surge](https://inc42.com/wp-content/uploads/2020/02/Graphs-30.png)

A look at the company’s expenses in the filings shows that employee benefit costs have increased 2.72X, while the cost of material consumed grew 5.19X, advertising expenses grew 3.92X among others.

Curefit declined to comment on Inc42 queries on its FY19 performance. The company is eyeing more capital raise, international expansion and targets growth in Indian cities. How it gets revenue to grow faster than expenses in the capital-intensive business remains to be seen.

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.