Tech startups are leveraging VC funds to acquire legacy companies and gain a leg up in the market

Dear Reader,

David vs Goliath. It’s been one of the most prominent metaphors of human life, having endured for millennia. If you were to put it in the context of businesses today, it would be something like this — the underdog startup competes against majors, doggedly gains market share and finally grows big enough to stand up next to the majors as an equal, and perhaps even acquiring the very giant it started out competing against.

For most startups that’s a fairy tale, a story to keep the entrepreneurial flame alive — only a handful of startups will grow big enough to actually live out the dream in that sequence. The success of any startup ecosystem, however, is linked to this event. We have seen it in the US and Silicon Valley and now, we are seeing it take root in India too.

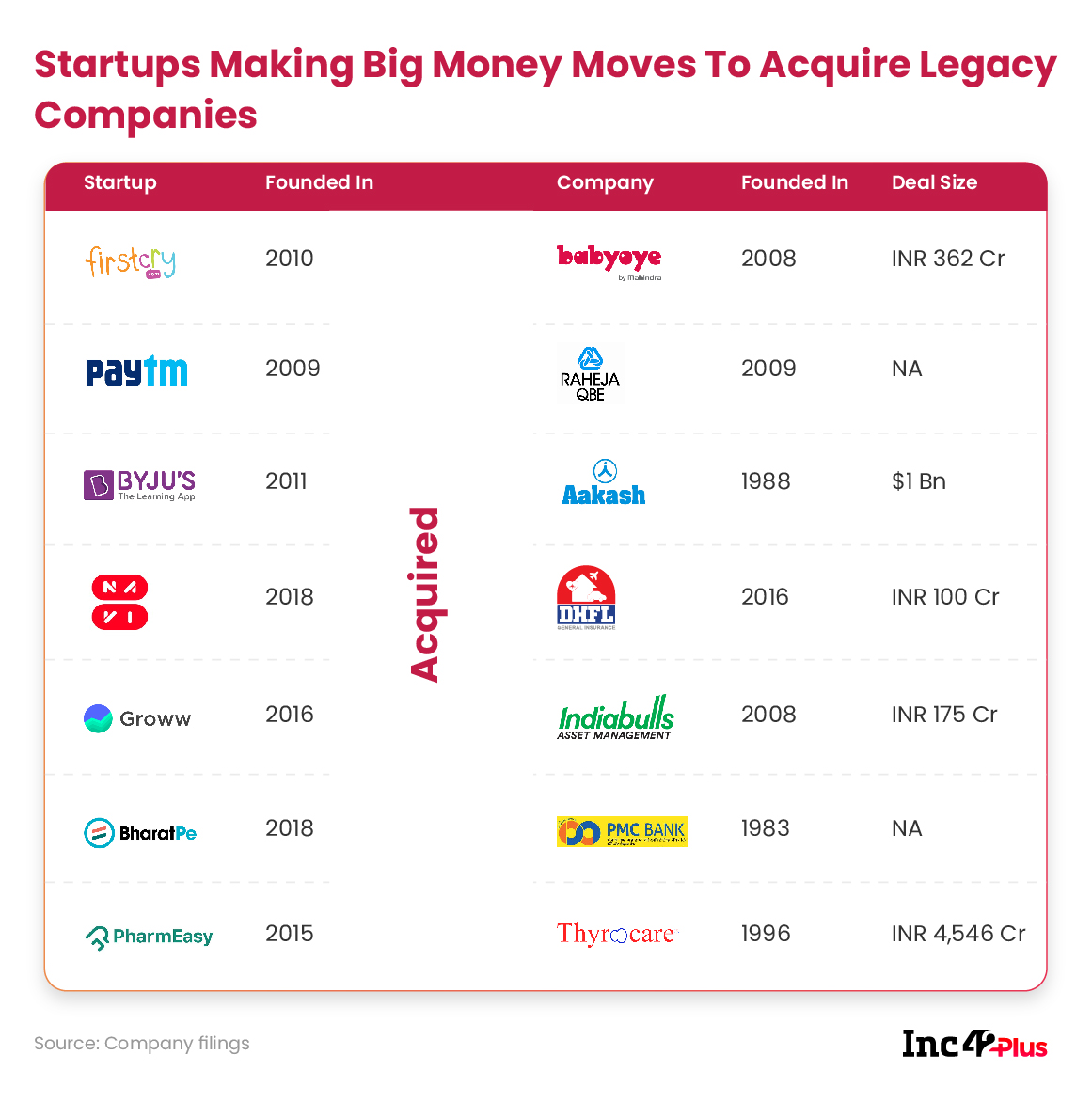

Startups are reaping the fruits after nearly a decade of shaping the tech industry in India and contributing to improving the digital infrastructure and economy. While groups like Reliance, which acquired 11 startups in 2018-19 have so far led the acquisition charts, the tables have turned. This is best illustrated by the major acquisitions orchestrated by startups to take over the legacy businesses in their respective sectors. The PharmEasy-Thyrocare deal in the healthtech sector is the latest example of a series of legacy company acquisitions by startups, which has also seen major deals in fintech and ecommerce.

As digital transformation becomes a necessary crutch for all businesses, more such acquisitions will happen in the next 12 to 18 months, according to market observers. Plus, legacy companies are seriously strapped for cash and lack the innovation required to meet the current market context. Startups are now the bailouts for these fallen giants or the exit route for the legacy business owner who is looking for a way out.

Startups Command The Moolah

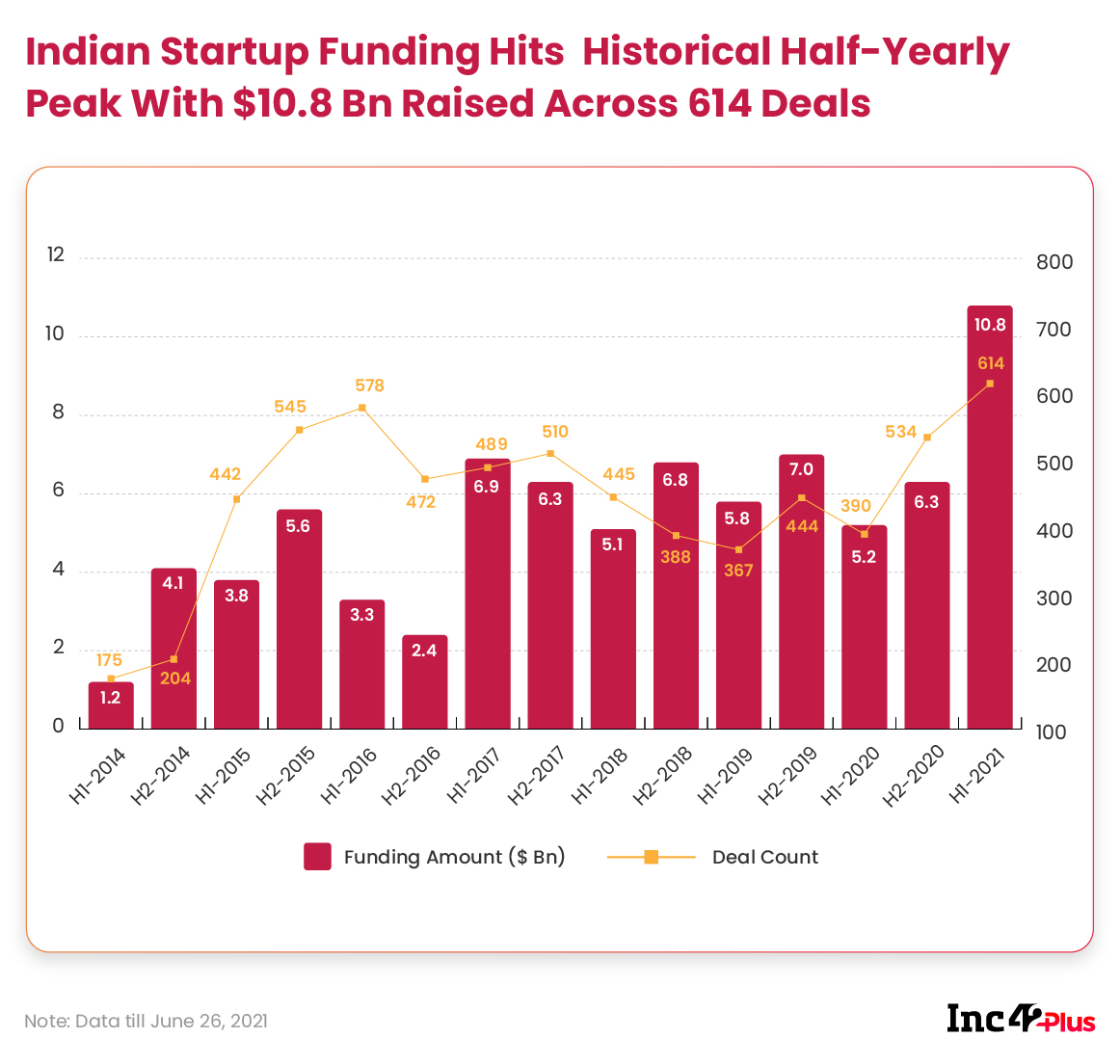

The growing appetite for corporate acquisitions can be largely attributed to the fact that startups are finding it much easier to raise capital in the post-pandemic market than legacy businesses. While venture capital investments are often derided as engines of paper valuations, the truth is that besides being put to use to acquire customers, startups have used the capital raised from VCs to build their tech prowess. This year, over $10.8 Bn has been raised in just the first six months, including over $500 Mn by PharmEasy alone, much of which was used for the Thyrocare acquisition.

Corporates with high public market valuations and huge market caps do not have the ability to raise large amounts of capital easily from the stock markets or private equity investors — at least not at the same frequency as startups can raise from VCs, with the exception of Reliance and Jio. This is a huge hurdle in a recessionary market where the advantage lies with those businesses that have the cash in the bank.

Legacy conglomerates such as the Tata Group, Reliance and Mahindra & Mahindra, which have massive globe-spanning businesses have had less of a hard time in the past couple of fiscals. They have built their empires over many decades and as such have plenty of reserve capital so they have moved to acquire startups as they go for a digital makeover. But those public companies that are strapped for cash or the loss-making subsidiaries of public companies will look at a startup as a rescue boat for the brand, an exit for the promoters or just the logical next step.

But beyond these mega-companies looking to solidify their businesses, slowly but surely the power to dictate terms is now shifting from corporates to startups that not only have the capital but also the technology, which has now become critical in the post-pandemic market.

According to Anand Lunia, this is what happened in Silicon Valley nearly 20 years ago — when startups became the ones with the power and started turning the entire industry around. The India Quotient founder believes that the ability of startups to access capital today is clearly much more than that of traditional businesses or even PE-funded businesses.

“It’s been the legacy of India that practically every business was run by people who had access and money. But now everybody (investors) is fed up with funding conglomerates or one more arm of a family business. I think capital is looking for management that is committed to only one company or startup, which is also tech-enabled,” he said, adding that it will become harder and harder for non-tech businesses to raise money, particularly if they are also struggling with growth.

His point is best illustrated by the staggering growth in funding amount and deals in 2021, till June, as compared to the previous years. More on this later…

Beyond public markets, bank loans which have propped up many Indian corporations have also dried up since banks have tightened their loan criteria after the major crisis around non-performing assets in the past 4-5 years. This has again made it hard for corporates to get bridge loans for survival.

The game of tech-driven acquisitions also involves deep-pocketed companies such as Flipkart or Amazon India that have made smaller deals in the hope of opening up M&A paths. While Flipkart invested in Aditya Birla Fashion, Amazon India’s investment in Reliance’s acquisition target Future Group has become a contentious issue and a major corporate conflict. Both Aditya Birla and Future Group have a massive footprint in offline retail, while these categories of commerce are moving online, and with offline retail being severely hit in the past year, ecommerce giants now dictate the terms.

Startups Break Through India’s License Raj

The answer to the question of what startups actually get from such distressed acquisitions varies from sector to sector. For PharmEasy, it was about having the retail diagnostics network to serve millions of customers; BYJU’S founder Byju Raveendran said the company acquired Aakash because the “future of learning is hybrid and this union will bring together the best of offline and online learning”; but in the fintech sector, corporate or legacy company acquisitions are primarily a gateway to getting a license.

Incidentally, BYJU’S fits our montage of a small startup acquiring a giant in its field aptly as when BYJU’S was founded, Aakaash already had over two decades of presence in the market. But because of the complacency that comes with incumbency, it was not able to halt the edtech juggernaut.

Similarly, legacy banks and financial services players continue to have a huge hold on the economy. For all of India’s progress and development in the past three decades, the ghost of license raj continues to haunt some sectors, particularly banking and financial services. Many are of the opinion that regulators have to be strict to avoid scams and that is right, but as times have changed regulations need to be brought up to speed.

When BharatPe announced that it had received the in-principle approval from the Reserve Bank of India for the PMC Bank licence acquisition, the Delhi-based startup’s statement said this is the first fresh banking licence issued by the RBI in six years. Another startup Navi has faced rejection from RBI for its own application — even though Navi founder and Flipkart cofounder Sachin Bansal is a noted entrepreneur and had orchestrated the biggest exit so far in the Indian startup ecosystem.

But banks in India are aging edifices and they are crumbling not only from the point of view of bad loans but also due to the inability to implement or integrate technology in onboarding, customer service, operations, service delivery and more. Neobanking startup Jupiter’s founder Jitendra Gupta told us that banks do not have technology in their DNA as they are essentially money businesses which use technology, but not tech businesses that revolve around money. Turning this identity around while keeping a massive multi-billion dollar business up and running — even in a decade — is next to impossible.

And so far banks have been lethargic, and are also dealing with other issues as in the case of PMC Bank, where due to a spate of bad loans, the bank had to halt its operations. In the case of major banks, the technology deployment has been slow and startups are knocking on the doors to be let into the banking arena.

Vivek Belgavi, a fintech expert and partner at PwC India believes that banks need to more than double their current top-line investment in technology solutions. “There is a need to extend the investment to 8-10% from around 2-3% of their top line to support the growing transaction volumes over the next few years,” he said.

Fintech and neobanking startups in India cannot operate as independent banks, but need to partner with entities with the licence. As such they are hamstrung by the regulations. So BharatPe’s acquisition of PMC is a huge deal in that regard, according to fintech experts and investors.

It could open up the doors for other tech startups to acquire less profitable banks and become digital-first banks. Setting up a retail bank will be a capital-intensive nightmare and this is an entry barrier, but acquiring one is less fraught with challenges — VCs are willing to fund these acquisitions for the massive upside in reutilising dormant or dying legacy assets for digital or omnichannel plays.

Turning Competition Into Investments

This brings us to our next point about corporate giants shedding deadweight to focus on profit-making entities. When Mahindra saw that competing with FirstCry was simply not possible for BabyOye, it decided to bow out of the business. And Mahindra got the timing right, according to Lunia, who founded Brainvisa with Supam Maheshwari in 1999, much before the latter went on to become the cofounder and CEO of FirstCry.

Today, FirstCry is valued at $2 Bn, whereas it was close to $400 Mn in 2016 when BabyOye agreed to the acquisition. So FirstCry had less bargaining power at that time and therefore Mahindra managed to get a better deal out of it. Eventually Mahindra ended up investing in FirstCry in 2018 and is a shareholder in the kidswear unicorn.

Similarly, retail diagnostic chain Thyrocare’s founder and MD Dr A Velumani realised that his company needed to spend huge amounts of money to create digital acquisition channels, service platforms and more to serve the modern consumer. So it decided to find the best possible terms with PharmEasy with the INR 4,546 Cr deal, and is now also an investor in PharmEasy having picked up just under 5% stake.

The same could be said about DHFL, which is a housing finance company, but which ventured into general insurance in 2016 and as many expected, did not manage to break through into the market. Essentially, the insurance foray was possible for DHFL because of its deep pockets, but it got the timing wrong, given that the focus had shifted to digital insurance and insurance tech. Two years later, Sachin Bansal’s Navi Technologies acquired the company and has now turned it into Navi General Insurance.

The point is this: startups are flexing their capital muscle and proving that technology is more than just a buzzword — it can be a rescue boat for the beleaguered corporates or even startups that have so far been comfortably sitting in a leadership position due to their first-mover advantage.

The current wave of acquisitions is also being driven by the IPO ambitions of many of these startups — including Paytm, PharmEasy, BYJU’S. If some of these IPOs are successful, these newly-public companies could become acquisition vehicles. Think of the likes of Cisco, and IBM till the early 2000s to Facebook, Google, Amazon and Apple now, who acquire several companies every year for.

Lunia lamented that India does not have as healthy an M&A market like the US, but that could change in a matter of 12-15 months. “I am hoping that after Zomato, Paytm, PharmEasy, Policybazaar and others list, that they will have the muscle in the market to buy out corporates and smaller innovative startups. As things are going, it will only become easier for them to acquire.”

Indian Startup Funding Boom In 2021

Startups are finding it easier to raise funds now and this is backed by the fact that over $8.1 Bn was raised in the April-June quarter. For comparison, that is 3X the amount raised in Q1, between January and March of this year.

Here’s another major indicator of the tremendous VC and investor appetite in India — in 2020, we saw 28 unique mega-rounds or (over $100 Mn), while this year, we have seen 31 such funding rounds already. Investors are backing the late-stage and growth-stage startups and these startups are pulling off major acquisitions. Indian startups are likely to raise $22.6 Bn across 1,212 funding deals by the end of 2021 and as the funding boom continues, expect more M&A deals this year.

The Age Of D2C

For decades, retail behemoths offered the Indian household everything from food to clothing, but now purchase decisions have come down to individual products, which are researched online, bought online and reviewed online. D2C brands are challenging the high and mighty retail giants in every category and as seen in the Inc42 Plus Indian D2C Market Opportunity report, these brands have scaled the INR 100 Cr revenue wall faster — with the majority of the brands achieving this mark in six years or faster.

As we head towards The D2C Summit, it’s time to celebrate the brands disrupting the market at an early stage. The 17th edition of our much-loved ‘30 Startups To Watch’ series is now out and this time around, we are focussing on direct-to-consumer ‘davids’ taking on retail goliaths. The recent flowering of hundreds of D2C brands and startups in India has veritably spoilt the average Indian urban consumer for choice. In 2021, D2C startups have raised well over $290 Mn till mid-April and this week, ecommerce rollup or D2C aggregator 10scale bagged a $40 Mn seed funding deal, by far the largest such round in India.

Along with consumer preferences, sales channels and product development, even brand narratives are changing. And who knows, we might end up seeing a few retail acquisitions from D2C brands in the next year or so.

Till Next Week,

Nikhil Subramaniam

Featured image & graphics: Aprajita Ashk

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/featured.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/academy.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/reports.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/perks5.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/perks6.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/perks4.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/perks3.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/perks2.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/perks1.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/readers-svg.svg)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/twitter5.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/twitter4.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/twitter3.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/twitter2.png)

![[The Outline By Inc42 Plus] When David Acquires Goliath — India’s Age Of Startups -Inc42 Media](https://asset.inc42.com/2023/09/twitter1.png)