SUMMARY

The traditional financial sector faces issues in credit risk assessment due to lack of historical performance and the risk profile of farmers

Till date, Sagri has distributed loans to 200 farmers across Jaipur, Manipur and Karnataka

The Japanese company has partnered with Freshokartz, Freshies Fresh and EasyKrishi to provide loans to farmers

Access to capital has been one of the major roadblocks in the Indian agriculture landscape. Though a majority of banks and financial institutions offer loans to farmers. It is only limited to farmers with above two hectares of farmland, whereas small and marginal farmers less than that go underserved or underbanked.

The traditional financial sector also faces issues in credit risk assessment due to lack of historical performance and the risk profile of farmers. Coupled with lack of authentic alternative data sources for risk assessment and visiting every farmer to verify identity, the credit outlook for the farming sector is bleak.

Leveraging technology and creating secure-based financing models, a number of agritech startups have forayed into the agri ecosystem, where they are bridging the gap between farmers and financial institutions by providing financial access to underserved farmers. Some of the startups include Farmart, Dehaat, Kisst, Jai Kisan, Bijak, and Arya among others. Yet the gap remains.

The fintech companies in the agri-segment are struggling in assessing, collecting and monitoring the data, accurately and precisely. Every organisation is working with its own proprietary algorithms based on historical data. Japan-based Sagri is looking to bring in precision through its satellite imaginary and soil sampling technology in India.

“We are solving two main problems for farmers in terms of microfinance — one is the credit creation for farmers and the other is repayment of the loans from farmers. This is done by using technologies such as satellite imagery, soil sampling and testing,” said Satoshi Nagata, chief strategy officer at Sagri.

Till date, Sagri has distributed loans to 200 farmers across Jaipur, Manipur and Karnataka. Some of the startups that it has tied up with Sagri includes Freshokartz, Freshies Fresh and EasyKrishi among others. The company has also tied up with farmer producer organisation NAFPO in Delhi to reach out to farmers. “Farmers repay our loans through these partner organisations,” avered Nagata.

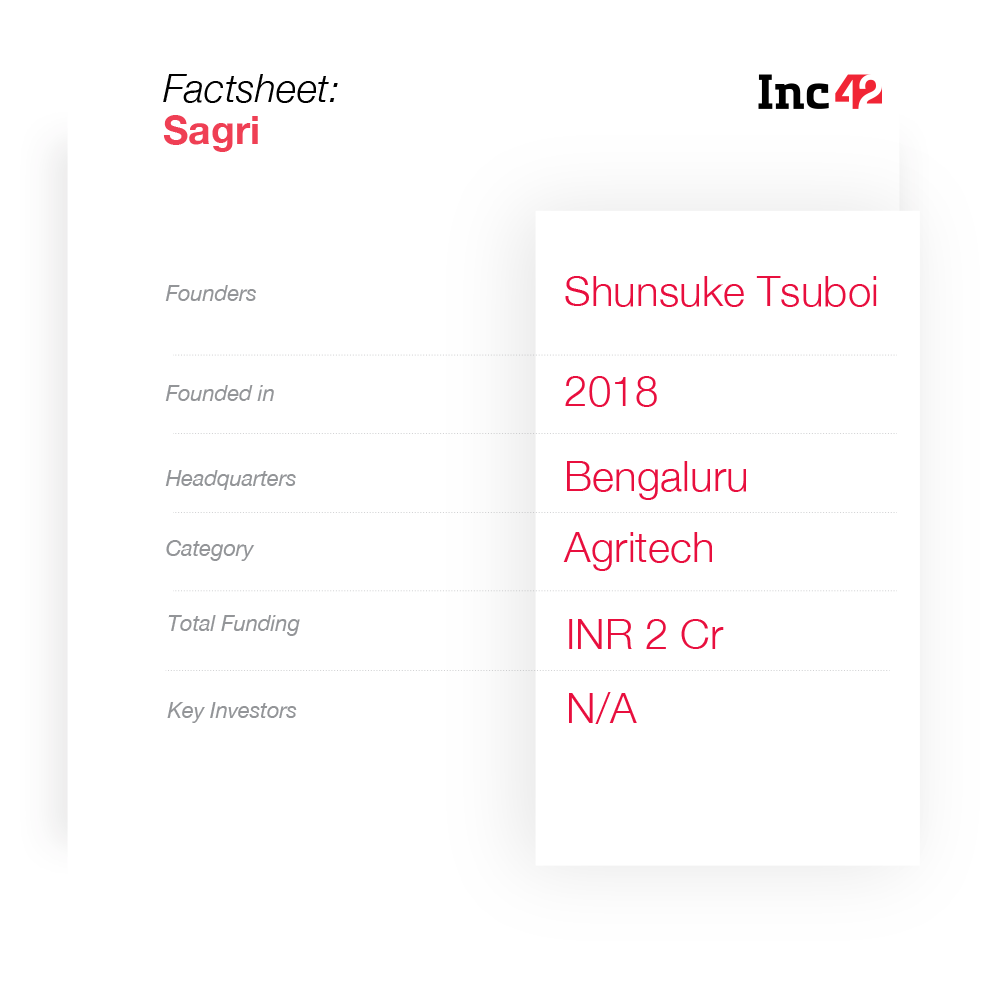

Sagri: The Journey Towards Financial Inclusion Of Rural Farmers

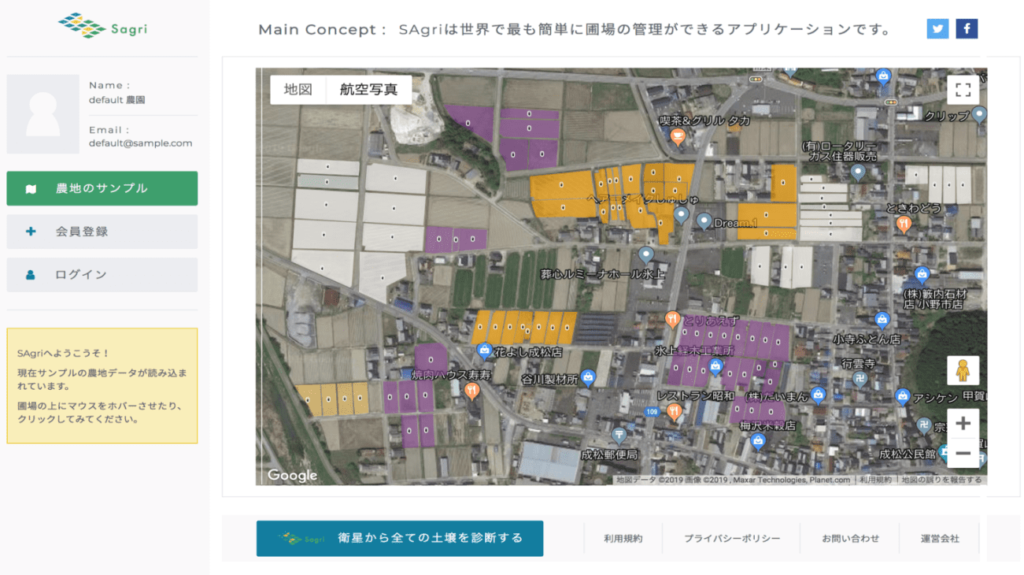

Founded in 2018 by Shunsuke Tsuboi, Sagri envisions creating value in the global agri market. It has developed a web-based and mobile application for experienced farmers, where it utilises satellite data, soil sampling and testing to help farmers increase their harvest yields and fertility by leveraging Farmer Credit Scoring technologies. The company said that it uses satellite imagery to calculate the NDVI (Normalised Difference Vegetation Index) of the farmland over a period of time. NDVI is a measure to calculate farm production and productivity.

Interestingly, it is one of the first startups to foray into Indian market with the support of Japan India Startup Hub, a joint initiative of India and Japan to promote startup enterprises and innovations in both the countries. The company has raised more than INR 2 Cr from Japan for their India operation. With a team size of seven members, Sagri helps farmers by improving their access to microfinance.

Currently, Sagri lends directly from its books, but in the future it plans to partner with other financial institutions to lend through their online platform for reaching out to as many farmers as possible. “As of now, we lend through our ‘SAgri Finance Platform,’ and it is also open to others to use, where they can lend to farmers,” Nagata added.

Sharing the journey of Sagri, Nagata said that they started the pilot with INR 10K per farmer. “Based on our study and research in India, anything below that is useless and anything above INR 50K, for most small to medium farmers, is a greed,” he said.

Today, the company provides loans in the brackets of INR 10K to INR 50K as it believes that anything above that the farmers are already big and they have access to institutional credit.

Lending Blended With Satellite Imagery

Nagata explained that Sagri uses satellite imagery to calculate the NDVI (Normalized Difference Vegetation Index) of the farmland over a period of time. In other words, NDVI is a measure to calculate farm production and productivity.

The company collects data such as the area of farmland, distance of the farmland from the main road, water supply and about weather or climate within that region. Also, it verifies whether the farmer or family members already have existing credit history from institutional banks.

“This is still a work in progress, and we know we will be switching context and detailing as we go along collecting and understanding the data,” said Nagata.

He further said that through a permutation and combination of the data-parameters that they collect and the history farmers build up over time. “This is going to be our unique selling point,” he added, intrigued.

In terms of credit cycle followed at Sagri, Nagata said that for farmers growing seasonal produce, it will be seasonal. For vegetable, cash crop growers, agro-based businesses, it is more suited to be fixed tenure based on the size of the loans and repayments on a monthly basis.

The Current State Of India’s Agri-Financing Landscape

As financial institutions and lending companies fear bad loans in the Indian agri lending space, it becomes imperative for them to rely on safe and secure methods of assessing farmers. Sagri believes that technology could solve the problem here, where farmers behaviour could not only be tracked through repayment habits, but also via offline data collection which could analyse and predict farmers’ future credit and repayment trends/patterns.

Many industry experts said that companies that provide loans to farmers with no security could end up in a tough situation. Nagata, throwing light on how Sagri ensures the repayment of loans, said that once they have the farm-level data, it becomes evident and easy to find out if a farmer is not likely to repay. “The farmland productivity is a good indicator,” he said.

‘To make it easier at this start, we are partnering with startups that have already worked with farmers and have a transactional history with them as it is easier to provide loans to their customers (farmers) and kickstart a data-history of farmers,” said Nagata.

How Different Is Japan From India?

According to the latest report, India stood at 53rd position in terms of agriculture growth, and Japan was ranked at 154th position. In terms of cultivable land, India has close to 158.65 Mn hectares, whereas Japan has only 4.33 Mn. However, when it came to cereal yield, Japan stood at 15th position, which is two times more than India.

Also, India currently has about 261.63 Mn farmers working in the field, on the other hand, Japan has only 1.63 Mn, which is almost 160 times more than Japan. All in all, both the countries have a huge difference in terms of the volume of land, climate and agri-population and outputs in the agriculture space.

Agri financing has been rapidly gaining a lot of traction in the market. Since a majority of the banks and financial institutions struggle to provide credit to small and marginal farmers, startups are looking at developing innovative approaches to financing such farmers, where they are creating technology-driven solutions for insurance, savings and commodity risk management among others.

In 2019, the agritech sector recorded a total funding of $244.59 Mn, an increase of over 350% in the amount of funding in the agritech sector from the previous year. Now, due to Covid-19, the sector is now witnessing a spur of new investments. The pandemic has highlighted the need for strong agri infrastructure, government’s support, data collection and farmer-friendly-policies.

Also, it has to be noted that agriculture is one of the riskiest sectors for lending as it becomes difficult for banks and financial institute to recover and mitigate risk arising due to untimely repayments (increased interest) and defaulters, thereby leading to a high incidence of non-performing assets (NPAs). In an attempt to make sure the farmers get easy access to capital, the government has also launched several schemes and measures to boost the sector, which includes the likes of Kisan Credit Card, Pradhan Mantri Fasal Bima Yojana among others.

Recently, the government has given a 3% concession to farmers on crop loan interest for prompt repayment, 1 Lakh Cr stimulus package for boosting the agricultural infrastructure and others.

[With inputs from Meha Agarwal]