Fintech

Fintech Travel Tech

Travel Tech Electric Vehicle

Electric Vehicle Health Tech

Health Tech Edtech

Edtech IT

IT Logistics

Logistics Retail

Retail Ecommerce

Ecommerce Startup Ecosystem

Startup Ecosystem Enterprise Tech

Enterprise Tech Clean Tech

Clean Tech Consumer Internet

Consumer Internet Agritech

Agritech

Only 30% of all farmers borrow from formal sources, while 50% struggle to borrow from any source

In FY19, banks provided agriculture credit worth $168 Bn

In the last ten years, the farm loan waivers have touched $63 Bn

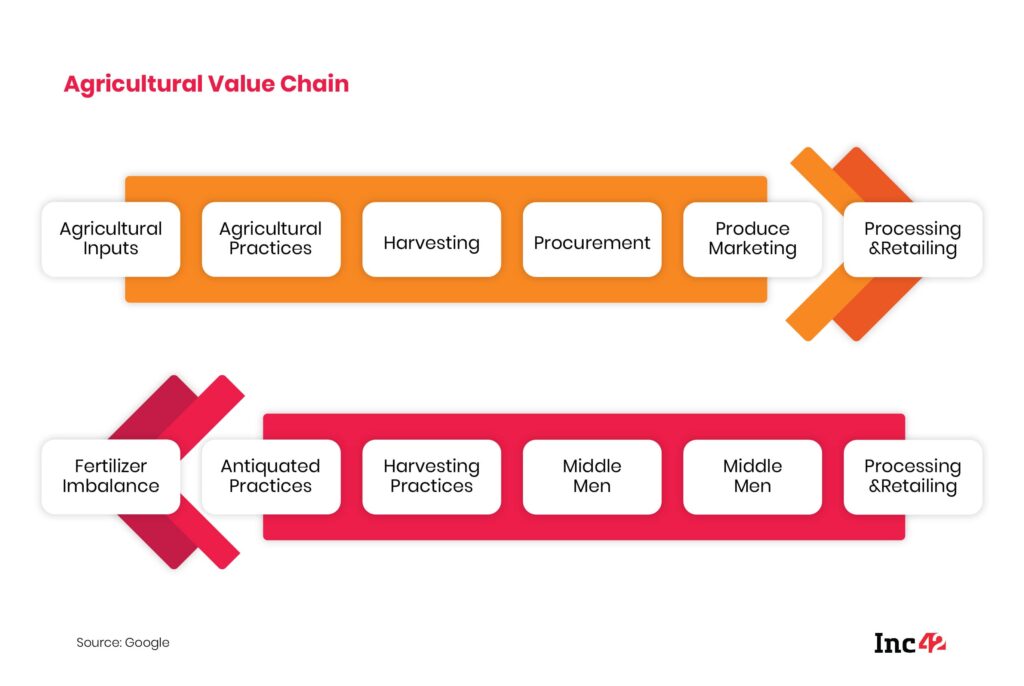

Agriculture and allied sectors contribute $368 Bn to the economy but its 16% share in India’s GDP isn’t an indicator of the financial inclusion of small and marginal farmers. According to ‘The Role of Tech-Enabled Formal Financing in Agriculture in India’ report by Rabo Foundation in partnership with ThinkAg and MicroSave Consulting, over 50% of India’s small and marginal farmers are unable to borrow from any source — tech or traditional — leading to a host of issues in production and income

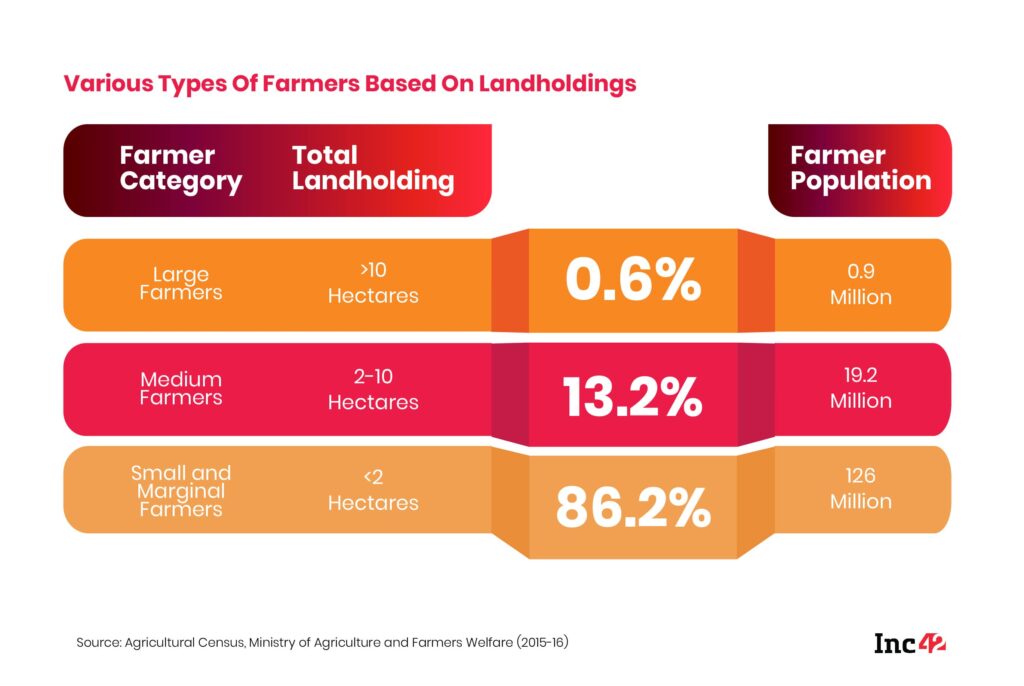

The report, which was released last week, reveals that of the 124 Mn of small and marginal farmers, only 36 Mn borrow from formal sources. Small and marginal farmers are those with less than 2 hectares of farmland.

They constitute about 86.2% of the total farmers in the country. To make things more difficult, of the $168 Bn agriculture credit offered by banks in FY19, over half was offered to medium and large farmers, who already have access to formal capital.

In 2019, the total agriculture credit disbursed stood at $168 Bn. Out of this, 75% of the capital was disbursed by commercial banks, 13% through cooperative banks and 12% regional rural banks (RRBs).

According to an analysis by Ashok Gulari, the former chairman of the commission for agriculture costs and prices (CACP), roughly 30-40% of the credit funds allocated under the interest subvention scheme for farms get diverted to non-agriculture usage such as education, healthcare expenses and marriage. Therefore, it becomes important for banks to ensure that the loans provided to farmers are used specifically for agricultural purposes.

But the report by Rabo Foundation highlighted that the banks are reluctant to offer credit to small and marginal farmers due to poor access, limited information and unpredictable policy environment. Also, in the last ten years, the farm loan waivers have touched $63 Bn in the country, the report added.

Agritech Boom Does Not Carry Agri Financing

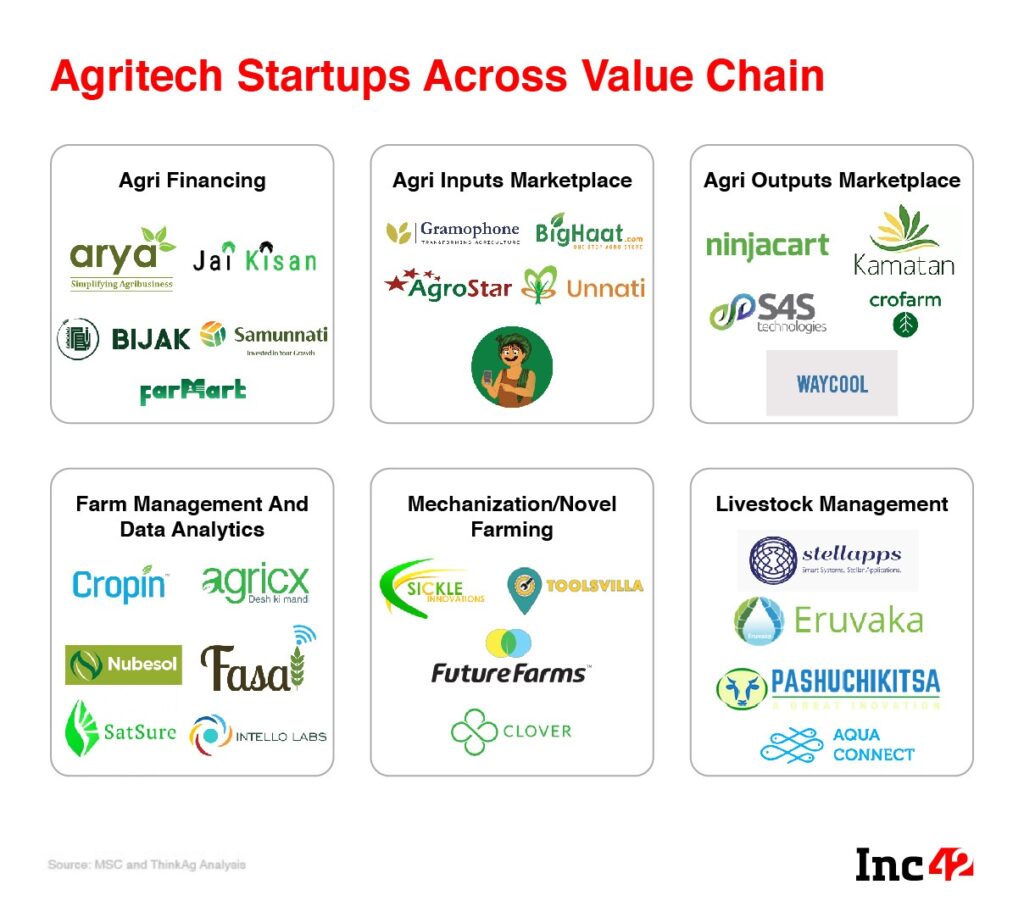

However, complex policy patterns and lack of loan access, provides an opportunity for ag-fintech startups to provide credit to small and marginal farmers by leveraging technology such as satellite imagery, soil testing and climate forecasting tools, wearhouse-sourced loans among others. Some agritech startups that provide financial products and services include Sagri, Samunnati, Arya, Jai Kisan, DeHaat, FarMart, Kissht and Bijak. The past five years have seen about 3,116 startups registered in the food and agriculture sector in the country, this is a 25-30% growth in the number of startups on a year-on-year basis, with approx $500 Mn investment since 2014, as per Rabo Foundation’s report.

According to Rabo, over 70% of the deals are focussed on early-stage agritech startups that focus on smart farming, farm-to-fork chain, insurance, credit and other segments. As per DataLabs by Inc42, the agritech sector recorded a total funding of $244.6 Mn in 2019, an increase of over 350% in the amount of funding compared to previous year.

Why Agri Financing Continues To Lag

However, agri financing solutions continue to see challenges around funding, partnerships and access to data for scaling. Some of the key challenges include the high risk perception among investors, limited funding for early stage agritech startups and mismatch of expectations between corporate partners and startups.

Banks, which are reluctant to offer credit to small and marginal farmers due to

poor access, limited information and unpredictable policy environment, have also made it difficult for agri fintech startups to have the trust in the farmer.

Agritech startups have a role to play in farmer financing — from credit origination to assessment, monitoring and recovery. Digitisation, access to alternate data and transactions in the agri supply chain will improve the integration of financing solutions, the study said. Creation of a single unified digital agri-database ‘AgriStack’ for India can enable financing for small and marginal farmers, it said.

Further, the study revealed that India could emerge as the hub of developing agri-fintech solutions for rest of the world particularly for regions such as Africa, South Asia and Southeast Asia, which have similar farming profiles

Banks Defer Partnering With Startups

The report highlighted that meaningful partnerships between financial institutions and agritech startups need more time to scale as most agritech startups at present offer standalone or partial solutions to banks. This becomes difficult for banks to collaborate with multiple agritech startups, and are most likely to choose agritech companies that offer them a full stack, comprehensive solution.

Besides this, banks have limited knowledge about how startups provide loans to farmers and even till this day, they trust their office staff to do the survey for them, and believe that agritech startups fail to add value in assessing the creditworthiness of small and marginal farmers, and banks require agritech startups that have data points for around 4-5 years, before conducting a pilot, the report added.

Furthermore, the report showcased the importance of an end-to-end, agri-stack platform which improves the existing farm-lending processes — and calls for a one-stop solution for banks, which includes features like innovator group, financial institution group, pilot development and build data and history around agri-value chain.

Will India See An AgriStack?

Today, only a few states have digitized land records, and a single platform to verify and gather the records can benefit farmers to a large extent. Also, agritech startups find it challenging to partner with the government. If the data is shared with the agritech startups, this can create a powerful partnership between the government and agritech startups.

In its report, Robo Foundation revealed a single unified digital agri-database solution such as AgriStack which enables credit access to farmers by providing information related to farm, farmer and crop. This, in a way, also paves a way for open APIs for agritech startups to develop various applications such as digital GPS-tagged land boundaries that guarantee land titles, digital records, etc.

Most importantly, the development financial institutions need to create a separate fund like rural infrastructure development fund (RIDF) or seek alternative sources of funding from global development and financial institutions like Asian Development Bank (ADB), International Finance Corporation (IFC) and Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) should help build agri-market infrastructure and offer capital to institutions that lend to small and marginal farmers, the report added.