Over the past few years, the Indian startup community has received a shot in the arm with investor confidence rising exponentially with every deal made, every round of funding raised and every product rolled out in the market. Clear winners in the space have included startups as diverse and innovative as Flipkart, Ola, Paytm, CarDekho, Zomato, and many others – with aggressive expansion policies, viable business models and problem-solving attitudes – investors poured in money to the tune of billions of dollars.

While 2015 was a golden year for startups and investors in general, 2016 is a whole different story altogether. This phenomenon was first reported in our half-yearly analysis ‘The Curious Case Of The Indian Startup Bubble’ of the Indian startup ecosystem.

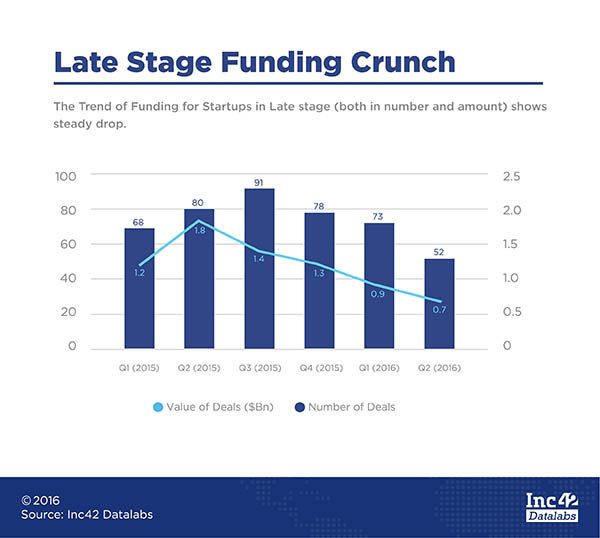

The report explored possible issues like late-stage funding crunch due to market capriciousness in H1 2016. February 2016 emerged as the worst-hit month, with late-stage deals receiving only 40% of funding and minuscule seed funding.

Early stage startups, on the other hand, received a lion’s share of investment with all six months of 2016 reporting a huge amount of money being invested. This tide has slowly but surely turned by August 2016, wherein late stage startups received around $463 Mn in Series B and above rounds of funding.

Healthtech Emerges As Clear Winner, Hyperlocal Shows Slowdown In H1 2016

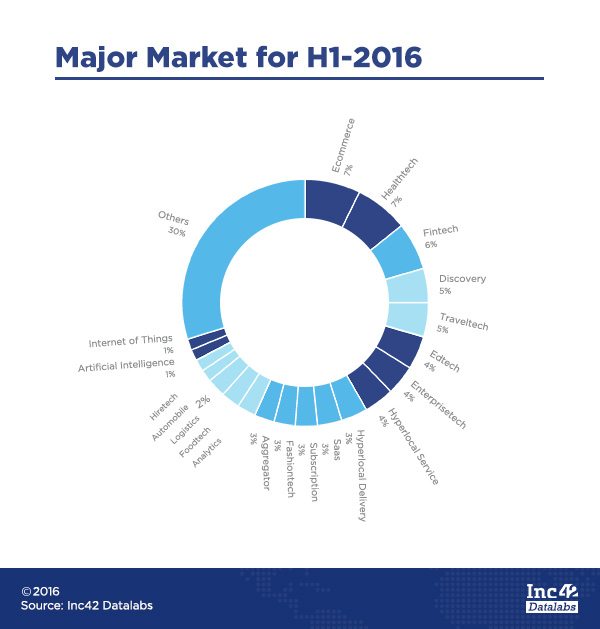

Sector-wise, healthtech emerged as a strong contender in the first half of 2016, to be on the receiving end of investor interest. With the rise in fundings for startups like AlternaCare, Tricog, and Ratan Tata-funded MUrgency Inc., investor confidence in the sector can be safely attributed to the potential $280 Bn available in India’s healthcare sector by 2020.

While traditional safe choices like ecommerce and fintech chugged along with 7% investments coming into these spaces respectively, it was hyperlocal services that took the biggest hit with a number of shutdowns, pivots, and M&As happening in the segment.

Once-promising startups like LazyLad turned B2B from B2C, and PepperTap initially shut down operations in six cities followed by becoming a ‘full stack ecommerce logistics company’ and shutting down hyperlocal entirely. Grofers, too, shut down operations in nine cities in January 2016.

Reasons for this meteoric rise and equally quick fall in the sector could be attributed to a number of reasons – such as aggressive use of an aggregator model, the rise in me-too startups with no clear, unique product or execution, and difficulty in conducting ease of business across states or even pan India.

And the one thing that most startups in ecommerce, mcommerce, and hyperlocal services did was to focus on user acquisition to prove the validity of the product in the market, forgetting that the next step – user retention – was equally important if not more.

From the available data, it is evident that hyperlocal is not the market darling anymore. On the other hand, edtech has steadily become an investor favourite by August 2016 taking 7% of the total market share.

The Problematic Side Of Starting Up

This is just one sector. Let us now analyse how the others have fared in recent months.

Problems of such magnitude saw a correction in the valuations of Ola (marked to $4.2 Bn now from $5 Bn last year) amid legal tangles and government sanctions.

Indian crowd favourite Flipkart’s valuation fell down to $9.9 Bn after Morgan Stanley marked down its stake in the ecommerce giant by 27% in March 2016 and a further 15.5% in May 2016. T Rowe followed this trend by marking it down by 20%, while Fidelity marked-up the valuation of its shares by a mere 3%. This bump was further compounded by Valic marking up its share valuation by 10%, leading to an eventual valuation of $11.2 Bn.

Flipkart is also reportedly in talks with Jack Ma-owned Alibaba to get in business with arguably one of the biggest ecommerce players in the world. It also doesn’t help that with these valuations come a tactic of course correction for both these homegrown unicorns: layoffs and shutting down underperforming acquisitions after absorbing them.

Snapdeal too has been undergoing its fair share of issues with allegations of malpractice rising against its founder, and reports of losing a major delivery player GoJavas suspending operations and being absorbed by a smaller company Pigeon Express.

And, even more recently, AskMe, one of the oldest internet portals established in India is undergoing a slew of troubles — ranging from primary investors backing out of an alleged MBO, vendors taking recourse from the Economic Offence Wing and the company itself applying to the NCLT for compensation from Astro Holdings, one of the main investors. While the MD Sanjay Gupta has asked for an MBO for the third time to pay off vendors and employees among other scandals.

Crunching Numbers: Comparing Timelines

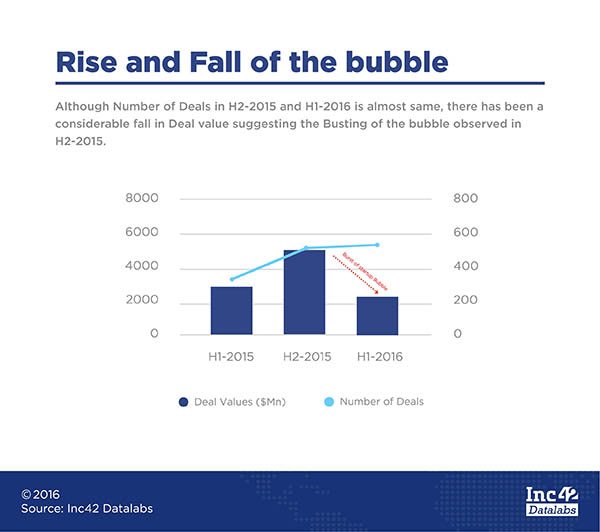

According to the half yearly report, H2 2015 saw a record number of deals (500) across sectors being struck between investors and startups in H2. The total value of these deals stands at a whopping $5 Bn.

What is interesting to note here is that while the same number of deals were struck in H1 2015 (~300) and H1 2016, the deal value vastly differs. The deal value in H1 2015 is $3 Bn, while in the first half of 2016 it has shrunk down to approximately $2 Bn.

This overflow of funding in the market, along with the inflation of the ecommerce and hyperlocal sectors led to the phenomenon of a rising bubble. And a bubble, as we all know, can only rise for so long before bursting into thin air.

The issues plaguing the Indian startup ecosystem in general and a few sectors, in particular, have now led to a quiet unrest among investors who are no longer opening their purse strings for every seed stage, early stage and late stage entrant around. They have become more cautious and are taking heed of shifting market valuations, user retention, unviable business models, and more before pouring in money.

All of which brings to the forefront a single burning question: Is a startup bubble burst imminent?

Fall Of Funding

So far we have discussed what has happened to the startups and its impact on investor behaviour. Now let us examine actual investor behaviour in H1 2016.

The most alarming fact is the gradual fall of the number of investors in H1 2016, which was its peak in Q1 2016 with 250+ investors investing in enterprise and fintech startups. By the end of June 2016, the number of investors had halved and stood at 125.

According to our newest funding report, this number has again risen significantly to stand at 178 in August 2016, indicating a cautious optimism in the investor community.

Ajeet Khurana, angel investor and Advisor at Kalaari Capital has the most interesting take on the situation. “The word “bubble” implies an artificial state that eventually bursts and nothing remains. That’s my problem with the characterisation of the startup funding scene as a bubble. In my opinion, there was definitely an over-exuberant buildup of valuations,” says Khurana.

There were three indicators for the same, all of which eventually turned red.

“Companies with business models that are intrinsically not equity-fundable were getting funded, lots of first time investors were making a large number of bets and most important, valuations could neither be extrapolated from present fundamentals (which is ok), nor from even a highly optimistic future scenario (which is not ok),” he adds.

While Sanjay Mehta, a member of CIO Angel Network, compares the current situation to that of fluctuations in the stock exchange. According to Mehta, startup investments are subject to the same market risk as all the others and this does not mean the companies are doing badly. It is just market fluctuation.

Fall In Ticket Size

The total number of VCs participating in funding in Q1 2016 were 379. Blume Ventures continued to bet big on the ecosystem with 20 deals between January and June 2016. This was followed by Accel, Sequoia, and Kalaari capturing the following three spots with 10, nine, and eight deals respectively.

In a more recent development, Blume continued as the leader in August 2016 with three deals, followed by Softbank, Sequoia, Kalaari, and Accel.

Anil Joshi, Managing Partner at Unicorn India Ventures talks about how new businesses in the startup economy are supposed to fill the blue ocean space and solve real problems of real consumers.

He says, “The basic premise of the new economy was to build business on freebies or discounts and not on addressing a real problem or need for the consumer.”

Joshi continues with, “Whatever has been invested in addressing real needs or blue ocean space is doing well, the rest have to struggle as new money wasn’t available for further growth of business built on discounts.”

This is a pointed dig at aggregator models and the current ecommerce scenario in India.

On the other hand, defending the need to allow time for new companies to build, Gaurav Sachdeva, Managing Partner at JSW Ventures’ says, “In H1 2015, there was immense optimism on the addressable market, speed of adoption of sales channels, push versus pull strategy, in “app-only” decisions – speed of internet, etc. In a lot of cases, it was a miscalibrated expectation of growth and consumer adoption. Late 2015, early 2016 everyone started asking the right questions on unit economics, consumer adoption, repeat, AOV etc. This helped founders and investors realise the time it takes to build any business in India.”

He further adds that a similar situation had occurred back in 2005-2007 in the organised retail and real estate sectors when the market had to course correct after initial over-exuberance shown by investors and businessmen alike.

Fall In Late-Stage Funding

Angel investors too made significant contributions, with Ratan Tata emerging as the undisputed winner with 15 deals, followed by Infosys Ex-CFO Mohandas Pai with 10 by H1 2016. While Tata continued to diversify his portfolio by funding in healthtech startup mUrgency, among others, Pai invested in edtech and fintech startups. Both of them were firm about shying away from the floundering ecommerce and hyperlocal segments. August 2016 though saw Kunal Shah and Anupam Mittal take the lead in angel investing with six deals.

This data shows quite conclusively that investors are not afraid to invest, they have finally understood the need to back the right product, company and business model. This is what leads to a thriving ecosystem built on sustainable growth and unique problem-solving products.

Krishnan Ganesh, Founder of Portea Medical and Promoter at Growth Story, pivots to another extreme phenomenon plaguing the startup economy at the moment – that of swinging between absolute euphoria and despair. Neither of which is an accurate barometer of what is happening on the ground. He cites many reasons for the way PE/hedge funds invest in India without evaluating the market holistically for the fall in late-stage funding.

“Global market changes – the valuations, China markets, the drop in valuations of publicly listed companies and sentiments; new category of late stage PE/ hedge funds coming to Indian Growth/VC segment and writing big checks, doing quick decisions and being less sensitive to valuations, the run-up of some models in the US creating appetite for similar models in India in a bull market that is fuelling quick and easy funding –it is almost like momentum play in rising public markets,” says Ganesh.

All of them agree that in theory, funding is available for everyone in the ecosystem. Ganesh puts it best when he says, “But this does not mean any bubble exists. We have seen and are seeing irreversible changes in consumer behaviour, wholesale adoption of new products and services, many of them driven by discounts but nevertheless a strong desire for the consumer to seek out new products and services.”

In Conclusion

All the investors we spoke to agree on one thing: the party of 2015 is over.

Not every great idea in seed stage will get funded nor will every ecommerce/fintech/healthtech startup (among others) achieve unicorn status on the back of enormous rounds of funding. Valuations have become more realistic as the euphoria over startups becoming popular is dying down and problems in business models, traction, scale, and growth are coming into clear focus.

Startups have now discovered a solution to this so-called burst: M&As. SaaS-based startups consolidated and merged in H1 2015 and hyperlocal services went the same route in H1 2016. This move, while not considered as successful as an exit, is a predictor that they can still stay in the game by backing each other up, absorbing each other and continuing to make developments in product and model.

By August 2016, there has been a marked fall in the number of M&As as compared to Q2 2016, signifying a slight optimism in the way startups are conducting business in the ecosystem.

“2014, and more so the first three-quarters of 2015, saw exuberance to the point of irrationality. Interestingly, VCs and other market participants themselves were the first to notice that things were going haywire. But most demonstrated a lack of conviction in their beliefs. Instead of watching others blunder along the way, they decided to go with the flow. Naturally, they are bearing the consequences of that today,” says Ajeet, assessing the situation.

But it is Sanjay Nath co-founder and Managing Partner at Blume Ventures who has a very balanced view of the ecosystem going forward. He says, “There was a higher than expected number of investments in 2014-15 (you could say we were in a period of “over-investment”). For example, a few larger VCs had invested in 15-18 seed deals in each of those two years. So in that sense, after that period of over-investment, the number of checks cut this year are being ‘rationalised.’ The positive effect is that the best-run founders and companies, with the most sustainable models, will stick around and break through – and this is healthy for the ecosystem.”

So there you have it, startups. The secret sauce needed to make it in the present economic climate: problem solve for India, build for PMF, attain growth through a sustainable business model instead of one based on wild valuation or unrealistic user growth and show real traction. Investors are waiting to open their purse strings to the Next Big Idea.