Incofin, M&S Partners, Das Capital, 3one4 Capital, Muthoot Fincorp Invested In The P2P Lending Startup

Gurugram-based P2P lending startup Faircent has closed $3.9 Mn in a Series B round of funding. Investors participating in this latest funding round include Incofin Investment Management and Faircent’ts existing investors JM Financial, 3one4 Capital, M&S Partners Pte Ltd and Aarin Capital.

The round also saw the participation of Muthoot Fincorp, Elevate Innovation Partners, Das Capital and Starharbor Asia Pte Ltd.

Faircent will utilise the newly raised funds towards strengthening the platform’s technology and creating greater awareness about P2P lending significance as a new and highly rewarding asset class.

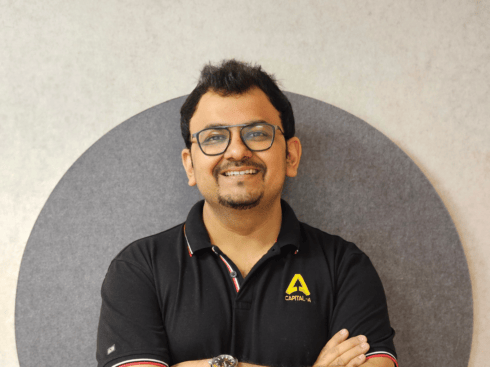

Founded by Rajat Gandhi and Vinay Mathews in 2014, the P2P lending startup provides a platform where people who have spare money can lend it directly to people who want to borrow, thereby eliminating intermediaries and the margins they used to make.

Speaking on the investment, Rajat Gandhi, Founder and CEO, Faircent, commented, “These are exciting times for P2P lending in India, and Faircent is here to unleash the power of retail lending. As India’s largest platform, being backed by marquee investors, and the fact that the RBI has come out with progressive guidelines for the sector is a great validation of Faircent’s business model. Moreover, with P2P lending, the financial market is all set to witness the creation of a totally new asset class.”

Faircent offers tools such as –Auto Invest feature, a fully-automated feature that matches a lender’s investment criteria with the borrower’s requirements and automatically sends proposals to the borrower on behalf of the lender, based on pre-selected lending criteria such as loan tenure, amount, and risk profile.

Recently, the startup, under the trusteeship of IDBI, created an Escrow account for its lenders to help in faster and smoother flow of funds enabling them to make greater returns on their investments.

“Faircent.com has done a terrific job of balancing the multi-dimensional value proposition of P2P lending to consumers – both an easy and affordable credit option, as well as offering them a high-yield asset class that can easily compete with more traditional investments. The team is now strongly positioned to work alongside the new regulations and lead this revolution in the space. We are happy to continue working with the team to help it leverage its learnings and advanced workflows to grow the market for all the stakeholders involved”, said Mohandas Pai, co-founder Aarin Capital and Advisor to Faircent.com.

Earlier in August 2016, the P2P lending startup had raised $1.5 Mn funding from Brand Capital. Prior to that, it had raised an undisclosed amount of funding in Series A round led by JM Financial Products Ltd., a subsidiary of JM Financial Ltd. In October 2015, it secured an undisclosed funding from the Chairman of Manipal Global Education, TV Mohandas Pai led Aarin Capital Partners.

Faircent was also part of the Microsoft Accelerator Winter Cohort and BizSpark programme.

The P2P Lending Market And Challenges

The Indian P2P lending industry has witnessed a sudden boom in 2017, facilitated by the fintech revolution. Expected to hit the $4 Bn-$5 Bn mark by 2023, the Indian P2P lending space has some 30 players, namely Faircent, LendBox, LenDenClub, IndiaMoneyMart, Monexo, Rupaiya Exchange, LoanBaba, CapZest and i2iFunding.

The market is currently marred by a myriad of risks and challenges, chief among which is of verifiable data. In a country with a population of over 1.31 Bn, only 220 Mn people have PAN cards. Other forms of KYC (know your customer), including voter ID, Aadhaar and ration cards are not considered as the sole identity proof, especially when it comes to financial activities.

This makes the process of borrower’s credit assessment and background verification difficult and unreliable. Awareness in the community about alternative investments is still relatively low. This, in turn, presents a challenge in getting lenders/investors on board.

Lack of awareness translates to lack of trust among borrowers, which is also one of the reasons why P2P lending has not yet gained much traction in the Indian market.

Earlier in October, RBI came out with the guidelines for the P2P lending marketplaces. In a Gazette notification issued by the central government, the RBI classified P2P lending platforms as a subset of the NBFC (non-banking financial companies) category.

In a bid to reduce the threat of money laundering the apex body has also put restrictions on the way funds are transferred between P2P lenders and borrowers i.e. all the borrowing-lending transactions will take place via direct bank-to-bank transfers.

Further, cash transactions have also been strictly prohibited. It also mentioned that the transfer between the participants on the P2P lending platform will need to be through escrow accounts operated by a trustee.

The new directives issued by the RBI will likely help bring transparency, credibility and accountability to the still-nascent segment. It will foster trust among both lenders and borrowers, which will, in turn, return the risk of loan delinquencies. Thus increasing the entry of investors as well as borrowers. With all this place, P2P lending platforms like Faircent are likely to benefit well from it.