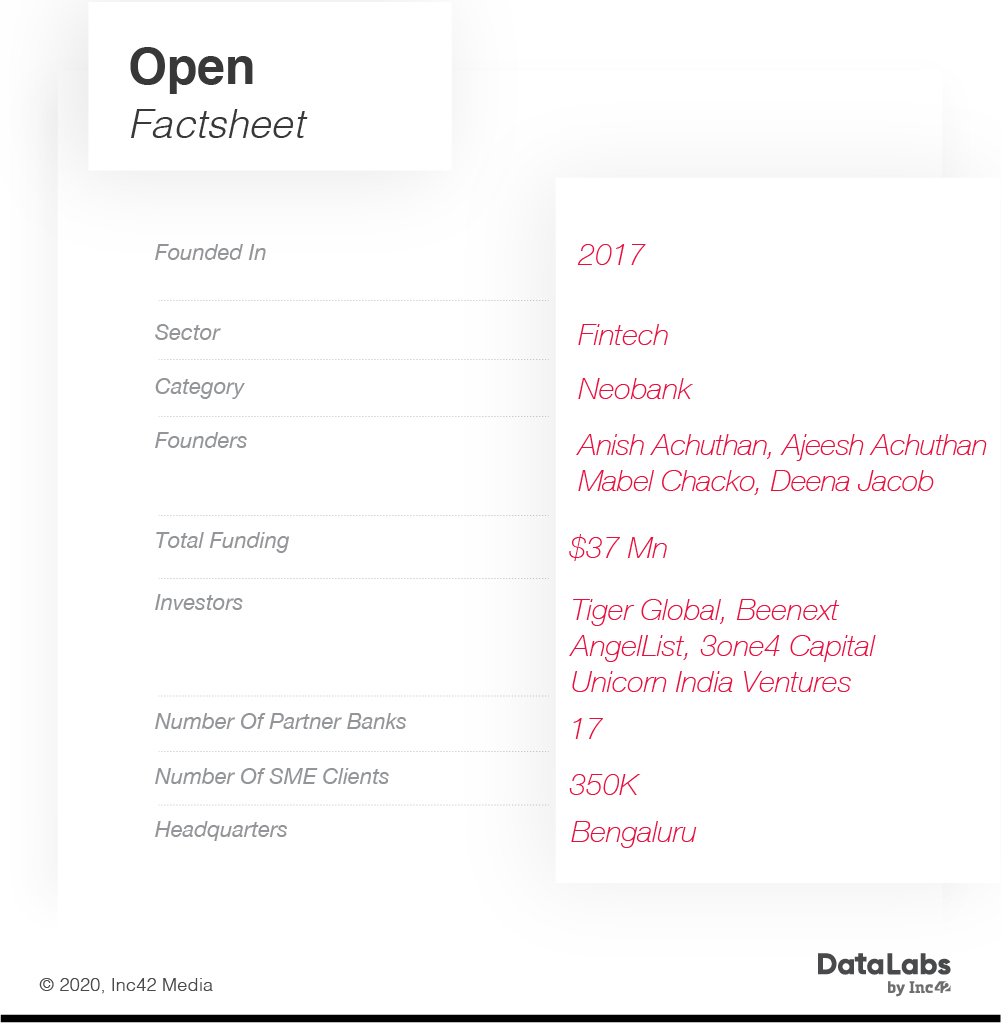

An SME-focused neobank, Open aims to bring 1 Mn businesses to its platform by September 2020

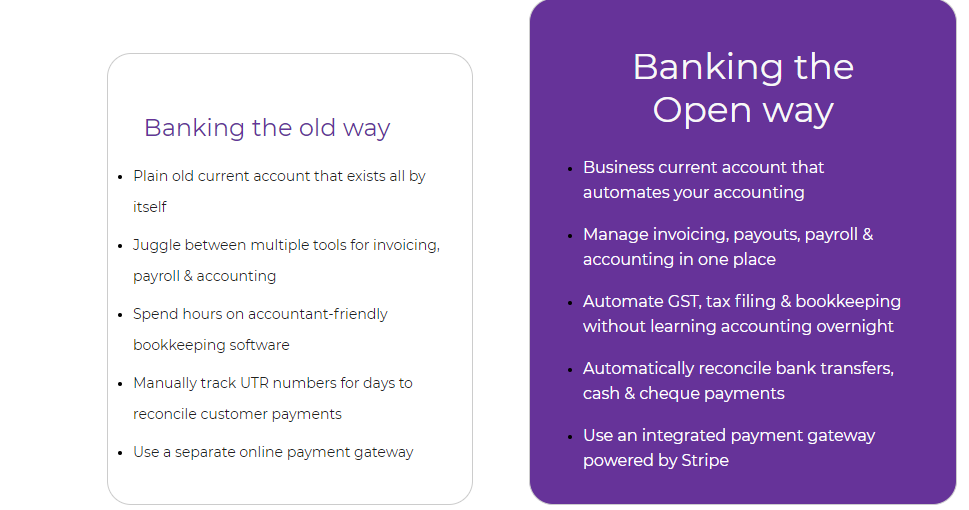

Open brings services such as payments, reconciliation, invoicing, bookkeeping and GST filing for SMEs

Backed by investors such as Tiger Global, Beenext, Open has raised $37 Mn in funding so far

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

“While I was in PayU and Citrus we had to deal with a lot of small businesses. That’s when I realised that these businesses were facing a lot of challenges when it comes to managing their finances,” – Anish Achuthan, cofounder and CEO, Open.

Open claims to be Asia’s first neobanking platform and is working to bring digital banking solutions to small and medium businesses and startups.

With over 50 Mn SMEs operating out of India, the space that Open works in offers a huge opportunity. Traditional banks are generally not able to provide the value-added services to this large base of customers due to their legacy structure.

From using a traditional bank where the money is held, a separate tool for accounting, a payment gateway for payments and reconciliation and different software for invoicing, businesses today are dealing with disparate elements in their operations. As a result, finance teams and banks end up spending a lot of time in reconciliation and process-making.

“With this in mind we decided to build a platform which could integrate everything from banking to automated accounting in one place,” added Achuthan.

Founded by serial entrepreneurs Anish Achuthan, Mabel Chacko and Ajeesh Achuthan along with former TaxiForSure CFO Deena Jacob in 2017, Open is a neobanking platform that does not have a banking license but partners with traditional banks to offer value-added services to SMEs and direct consumers.

Open: Services Offered, USP And More

The SME-focused neobanking company offers tools for businesses to send and receive payments combined with automated accounting and bookkeeping, expense management and developer-friendly APIs to help SMEs integrate banking into their business workflows in minutes.

Recently, the company announced a partnership with Visa to launch the ‘Founders Card’, a business credit card that will enable startups and SMEs to seamlessly manage expenses and vendor payouts.

Open is working under Visa’s Fast Track programme for the India market which supports homegrown startups and helps businesses automate payments.

Besides helping SMBs manage payments and reconciliation and solving access to working capital, Open also supports critical tasks such as GST and tax filing, which have become a big compliance hurdle for SMBs in the past year or so.

Challenges Of Bringing A New Concept In Indian Ecosystem

In countries like the UK, US, China, Argentina, Europe, Brazil, Australia, fully operational neobanks have become commonplace. But due to regulatory hurdles, neobanks can not function in India directly and have to work as a platform along with partner banks.

“With Open, for almost the first one and a half year, we struggled to find the right banking partner who would help us leverage its base to build upon. It took us a lot of time to go through all the statutory permissions and requirements. We only partnered with ICICI Bank in October 2018,” said Achuthan.

But as they say, all’s well that ends well. Backed by leading global investors like Tiger Global, Speedinvest, Beenext, Recruit Strategic Partners, AngelList, 3one4 Capital, Unicorn India Ventures, Tanglin Venture Partner Advisors among others and has raised $37 Mn in funding so far.

Today, it has already grown to have over 350K SME customers and claims to process over $10 Bn in annualised transactions. The monetisation model includes pay per use charges, subscription fees for premium services and revenue share on apps on its app store. Open told us it adds over 35K SMEs every month, and now has 17 partner banks on board.

The Way Ahead For Open And Neobanking In India

Bill Gates once said: ‘Banking is necessary. Banks are not.’

The rise of neobanks globally is lending credence to Gates’ words. In fact, a Medici report revealed that in 2018, the neobanking market accounted for about $18.6 Bn in revenue, which is expected to see a herculean growth at a CAGR of 46.5% in the coming years.

The global neobanking market size is expected to grow up to $394 Bn by 2026, at a CAGR of around 46.5% between 2019 and 2026. This is further backed by the fact that European neo-banking players like Revolut, N26, Monzo have become unicorns in just a few months since launch.

And though the neobanking as a concept is new for India, there is no dearth of players in this segment. Namaste Credit, NiYO, SBI YONO, Kotak 811, Hylo, PayZello, InstaDApp, 0.5Bn FinHealth (YeLo), Forex-Kart, Walrus, Epifi, Neo-Bank, Amica, Fin.in, RazorPay X among others have already been gaining significant attention from consumers, industry and investors.

Going ahead, Open aims to bring one million SMEs on the platform by September 2020. The major concern for Achuthan and the team revolve around the regulatory aspects which are taken care of by the partner banks. But he seems optimistic and does see the regulator coming up with a digital banking or neobanking license in the near future, in line with what’s happening in Singapore, UK, Malaysia and Hong Kong.

“We have seen this earlier too with the payment banks license. In many ways, we have a very proactive regulator that keeps a keen watch on what’s happening in the global markets and adopting the best practices into the Indian use case,” he added.

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.