Zomato and Swiggy have more or less gone in a similar direction, but their experiments to grow revenue through acquisitions have come at a steep cost over the past two years

Despite increasing their pricing for restaurant partners and reducing discounts, Swiggy and Zomato are not in the black yet given the complicated unit economics situation

Even as the outlook for food delivery giant leans towards consolidation, the battle for market share is expected to intensify and start anew in quick commerce and other new sectors

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

India’s food delivery segment is a duopoly in many ways, with Zomato and Swiggy more or less splitting the pie. But in the push towards maximising their revenue, bolstering unit economics and carving out profitability, these food delivery giants have looked to expand their businesses into newer territories.

From quick commerce and grocery delivery to courier services and from B2B supply to dining out — Zomato and Swiggy have more or less gone in a similar direction, but these experiments have come at a steep cost over the past two years and driven by acquisitions and investments in other smaller startups.

This is the clearest indication thus far about the appetite of Swiggy and Zomato to diversify their portfolios.

While analysts and consumer services experts believe there is enough headroom for growth in the underpenetrated online food delivery market in India, going beyond Tier 1 locations is still a high cash-burn, low-margin business.

This is further fraught with conflicts as most food establishments continue to complain about shrinking profits as costs associated with leveraging online delivery platforms keep rising.

Despite the price increase for restaurant partners and reducing discounts offered to customers for deliveries, Swiggy and Zomato are not in the black yet. They are still looking for an ideal volume play that will push them out of the red.

In the meantime, they are keen to explore new but adjacent revenue channels in the wake of a funding freeze and a global downturn where profit could be the only survival mantra. This largely explains why these heavily funded industry leaders are constantly exploring new service zones.

Here, Zomato is seen as the more aggressive of the two, putting in more than $1.2 Bn for investments and acquisitions, while Swiggy has spent around $250 Mn on such deals.

A quick look at Zomato’s Blinkit deal, its most significant acquisition to date, amply supports the current scenario. After months of deliberation, the Zomato board approved the acquisition of Blinkit (previously Grofers) for $568 Mn (INR 4,417 Cr) in June this year. While commenting on the all-stock deal, Zomato’s founder and CEO Deepinder Goyal said that the offerings of the quick commerce startup would be synergistic with its core food delivery business.

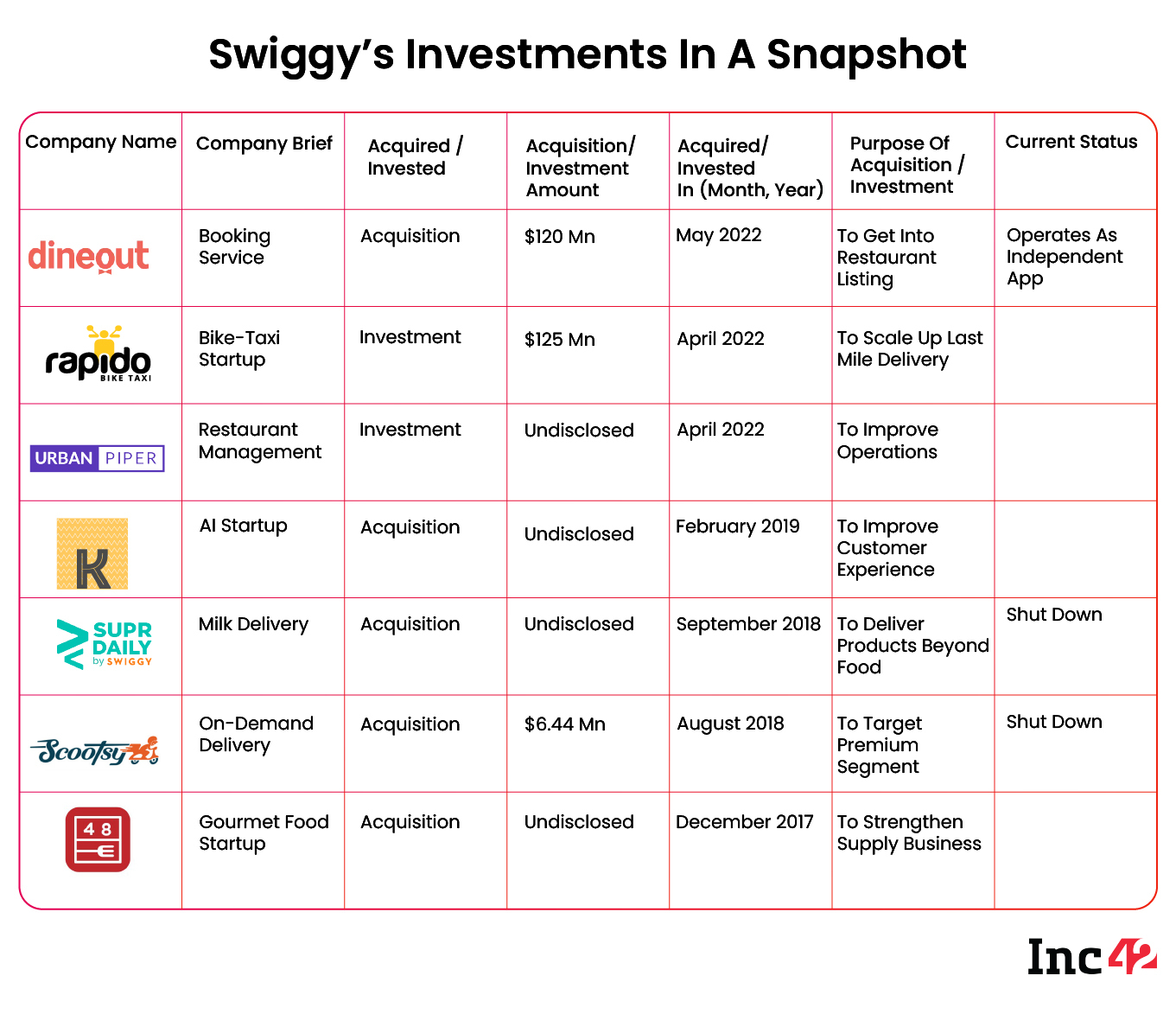

Weeks before the Zomato-Blinkit deal was announced, rival Swiggy acquired Dineout from Times Internet to enter the discovery, online reservations and other relevant services for dining out to compete with Zomato’s dining business. The deal, which was reported to be in the region of $150 Mn-$250 Mn is seen as Swiggy’s way to maximise the value offered to thousands of restaurant partners.

“Sometimes it makes a lot more sense to acquire certain skill sets from the market rather than trying something new. It is a faster way to get into the market and explore opportunities. At times, the valuations are high for core businesses, and you need to enter a new segment to justify the valuation. It is happening to many businesses in India,” an investor in a leading quick commerce startup told Inc42, requesting anonymity.

But the experimentation does not always work out. Take, for example, the grocery saga where both companies saw synergies and potential. Although Swiggy has made its mark in grocery delivery with Instamart, Zomato has tried more than once to crack the segment without much success. While multiple Indian startups across healthtech, ecommerce, fintech, logistics, foodtech and edtech have made strategic acquisitions, the business case is often very straightforward, added Vivek Jhunjhunwala, partner at Deloitte India.

For instance, Zomato piloted a grocery delivery service in April 2020 as food delivery orders dwindled at the beginning of the pandemic. But within two months, it decided to shut down the grocery arm, saying that the business was not scalable. In June 2021, Zomato re-entered the segment, but the initiative was scrapped again in September.

A similar story played out on the nutraceutical front where Zomato launched a private label before winding down that business.

Bigger Focus On Tech, Logistics

But the acquisitions are not just about revenue. The foodtech behemoths are looking at inorganic growth and also bolstering their respective tech stacks and delivery capabilities. One of the biggest friction points in positive unit economics within the food delivery space is of course the delivery cost per order.

Given that per-hour gig worker costs have to be spread across several orders, the logistics challenge has been ever-present in the food delivery space.

In its first large-scale investment in this space, Zomato put $75 Mn in logistics tech company Shiprocket that primarily caters to D2C brands. At a time when delivery costs are accelerating almost everyday, this investment is claimed to be helping Zomato reduce food and grocery delivery servicing costs (through Blinkit).

Shiprocket’s API-based approach will enable richer location data and logistics intelligence for Zomato that can be used to improve penetration of dark stores for Blinkit, or indeed the food stations being planned for Zomato Instant.

Like Zomato did with Shiprocket, Swiggy has placed a bet on hyperlocal services and invested around $150 Mn in bike taxi startup Rapido to bolster its logistics and leverage the synergy to bring down operational costs.

In another case, Zomato invested $5 Mn in a kitchen automation startup called Mukunda Foods. The company has developed robotics technology to automate the preparation of certain food items without human intervention. This can be leveraged for Zomato Instant as well as many of Zomato’s cloud kitchen and restaurant partners.

Not only will automation boost the creation of new cloud kitchens, but it reduces manpower costs, which are a key expense for such dark kitchens.

According to Deloitte’s Jhunjhunwala, Zomato and Swiggy’s acquisitions mean that certain capabilities, technologies and addressable markets can be unlocked without spending on building the right team for it. It is simply not worth it for a well-funded, large company to spend precious months building these things from scratch.

“These businesses have adequate capital as they have raised money from investors. They have seen the startup journey themselves. They have seen the entire growth curve and have the bandwidth and the knowledge to know which business models would do well,” added Karan Taurani, senior vice president at Elara Capital.

What About The Profitability Of Zomato & Swiggy?

Even though these synergic investments make interesting business cases for Swiggy and Zomato, profitability is far from close.

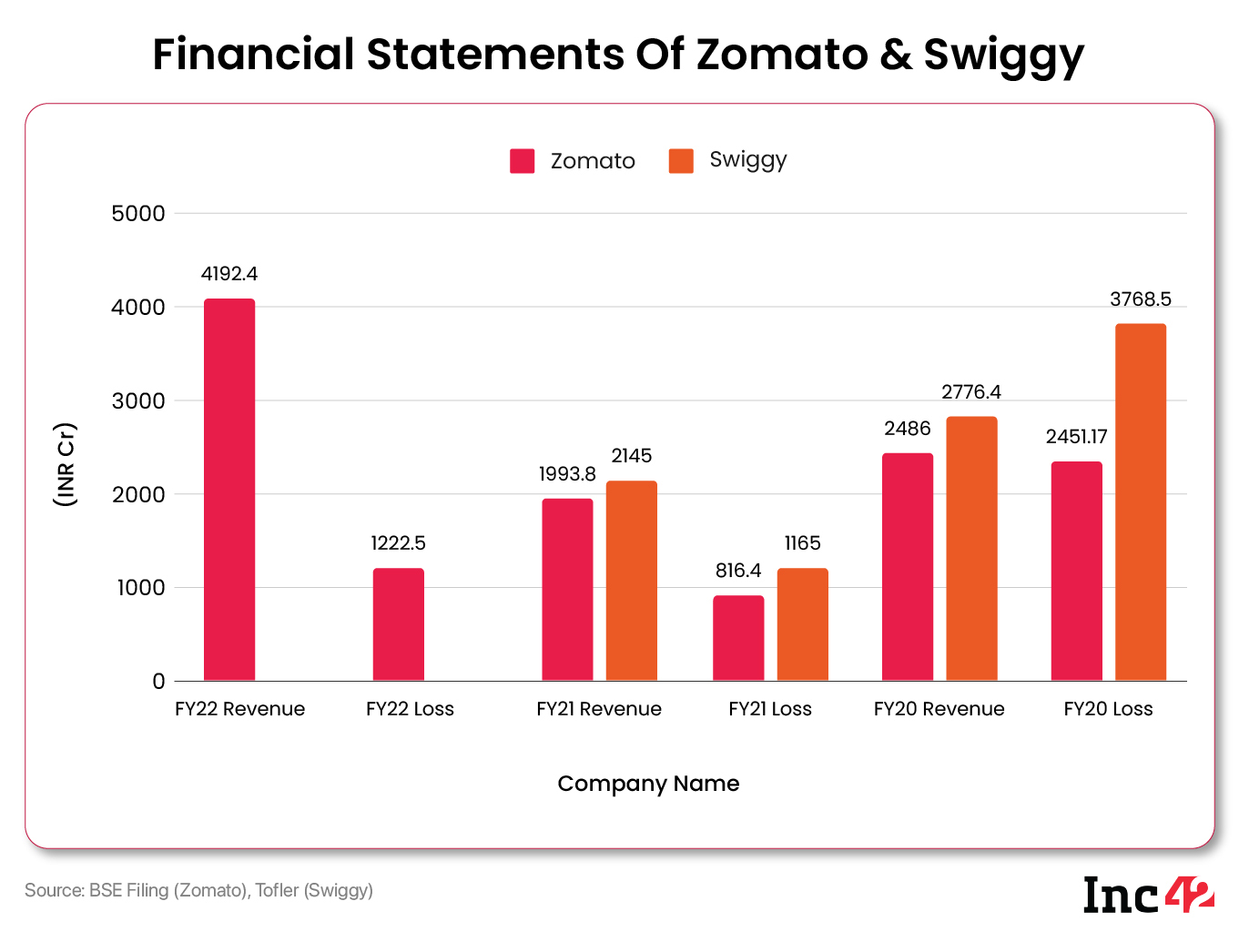

Consider this. Despite twofold revenue growth, Zomato’s net loss widened in FY22 due to a significant rise in expenses. The company reported a net loss of INR 1,222.5 Cr in the last fiscal compared to INR 816.4 Cr in FY21, while its costs rose 137%, from INR 2,608.8 Cr to INR 6,205.5 Cr.

Investor expectations have also taken a beating as the foodtech firm continues to record losses. The acquisition of loss-making Blinkit has complicated things further.

In this week, Zomato has seen a major crash as its shares hit an all-time low and ended Tuesday (July 26) at under INR 42.

While earlier the company was expected to be profitable by FY2025, this is likely to be pushed by at least a year, i.e from FY25 to FY26, according to analysts at JM Financial. Although Zomato believes Blinkit will turn profitable in less than three years, the company conservatively forecasts that the standalone business will turn profitable only by FY27.

A quick look at Swiggy’s business performance reveals a slightly different picture, but the losses are equally grave.

The Bengaluru-based company posted a loss of INR 1,165 Cr in FY21 but managed to shave around 70% off the INR 3,768.5 Cr loss incurred in FY20. However, Swiggy’s revenue dropped too, from INR 2,776.40 Cr to INR 2,145 Cr in FY21, a 22% dip largely due to the pandemic headwinds.

As it gears up for an IPO in 2023, Swiggy needs to look closely at its numbers as potential investors will be closely monitoring its performance till the public listing and if the path to profitability is not clear, Swiggy might face similar challenges to Zomato as a public company in the future.

M&A Cash Burn: Is It Needed During A Funding Winter?

Given the current market volatility and rising global recession risks, the startup ecosystem worldwide is facing a funding winter. Therefore, analysts believe that all late stage startups (even those listed) must adopt a conservative approach — this is where things get complicated for Zomato and Swiggy.

They can hardly afford to take their foot off the accelerator when it comes to growth.

“The problem is they [Swiggy and Zomato] have not yet generated enough cash flows or profits. So, it does not make sense to invest further at this point. There has to be some monitoring regarding capital allocation. They, too, have to reach their unit economics,” said Elara’s Taurani, adding that raising funds will nevertheless be critical to push for growth.

Continually evaluating and executing investments and acquisitions is one way to remain an innovation leader, but this too takes cash infusion. The funding boom that India witnessed last year will impel these late stage startups to invest and acquire aggressively. If this volatility continues, assets will be available at cheaper prices, leading to more M&A opportunities.

Even as the outlook for food delivery giant leans towards mergers, acquisitions and consolidation, the battle for market share is expected to intensify and start anew in quick commerce and other emerging sectors. The dining-out business will be of particular interest, since both Swiggy and Zomato are looking at subscription revenue linked to heavy discounts and repeat usage.

Will this new bet pay off for the core food delivery business too? Or is the focus now on improving the areas of business that will bring in enough revenue to offset the losses on a consolidated basis? These are the big questions awaiting the leadership at Zomato and Swiggy in the second half of the year.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.