SUMMARY

The rout in Zomato shares is seen as a reflection of low confidence in promoters and ripple effects of moves such as the risky Blinkit acquisition

Zomato is seen as overpriced even at its current level; analysts say risk takers can park money around INR 40 levels as a high-risk, high-return strategy

The cashburn-reliant Blinkit deal is widely expected to widen the loss of Zomato in the near term, while the outlook for 10-minute food delivery is also muted

Casting doubts over the sustainability of its business model and viability of its Blinkit acquisition, investors and market analysts have once again given a big thumbs down to zomato![]()

![]() .

.

The stock tumbled below the INR 42-mark on Tuesday (July 26), closing at INR 41.65 on the BSE. It hit an all-time low of INR 41.25 intraday as pre-IPO investors exited on the expiry of the one-year lock-in period from the time of listing in July last year.

A large number of retail investors who bought Zomato in the IPO have already exited after the stock began its downslide. The stupendous fall of Zomato from a lifetime high of INR 169 to below INR 42 in a span of a few months is largely being seen as a “promoter failure” by market observers.

“The fall of Zomato stock from its all-time high means investors are losing confidence in the business model and there is low confidence in the promoters who have failed to perform what was said at the time of IPO process,” Prashanth Tapse, senior vice president of research at Mehta Equities, told Inc42.

More Correction On The Cards

Even as Zomato’s share price declined over the past few months, the debate over the true value of the stock has continued. Has Zomato hit bottom now?

Market observers believe that even at the current level, Zomato is overpriced and indicated that the worst is yet to come.

Aswath Damodaran, a professor of finance at New York University, who also goes by the sobriquet of the dean of valuation, had valued Zomato at INR 40 when the startup went public in July 2021.

One year down the line, his estimation seems to be playing out. The investor advice now is that Zomato at INR 40 could be a buy for high-risk investors. “Risk takers can park money around INR 40 levels as a high-risk, high-return strategy,” Tapse added.

Short-Term Outlook Is Muted

Zomato’s stock market performance has been eminently forgettable. The relentless battering of new-age tech stocks across the world points to investors’ concerns about inflated valuation, an unclear path to profitability and complicated or scattered business models of many new-age companies.

Zomato figures prominently in this unenviable list, along with other tech stocks such as Paytm.

While a large chunk of the stock’s value erosion can be attributed to capital flight from India, there are other problems that point to an unstable future, at least in the short term. For instance, Zomato’s business model split between food delivery, B2B supply, dine-out, and quick commerce (post the Blinkit acquisition) has not inspired too much confidence among investors.

In recent months, the Blinkit deal and alleged non-disclosures or late disclosures in relation to Zomato’s investment in the quick-commerce company have raised some concerns, according to Rahul Sharma, research head at investment advisory Equity 99.

Rising global inflation has also led foreign investors to move from new-age tech startups to low-risk stocks. Even crossover funds such as Tiger Global which have been bullish on tech have deleveraged their positions in recent months.

Sharma further noted that Zomato is unable to generate profits and the current outlook around high inflation is expected to put pressure on its unit economics and margins this year, leading to wider losses.

Zomato reported a loss of INR 359.7 Cr in the March 2022 quarter, compared to a loss of INR 134.2 Cr in the previous quarter. “The near-term outlook for Zomato remains muted as some regulatory hurdles like Blinkit acquisition risk and corporate governance issues would disturb the investor sentiment,” said Tapse.

In June, Zomato announced the INR 4,447 Cr deal to acquire instant grocery delivery platform Blinkit which had rebranded from Grofers in 2021. Zomato had already invested INR 100 Cr in Blinkit last year and was widely expected to acquire the company in 2022.

However, the decision has not been received well by retail investors or even analysts as evident from the mass exodus from the stock as well as the criticisms in the wake of the acquisition.

The stock has lost about 18% since the announcement of the Blinkit deal on June 25. On a consolidated level, Blinkit’s losses are likely to weigh heavily on Zomato’s books and complicate the path to profitability further. The deal is widely expected to widen the losses of Zomato in the near term even as synergy is seen accruing over the long term.

“A loss-making company acquiring a loss-making, pure-play quick commerce company for making it a profitable operational metrics in the long run,” Tapse said, wondering whether this strategy would indeed pay off.

Blinkit, for instance, has reported losing INR 84 for every order and this is likely to widen the blended delivery costs for Zomato across food and quick commerce delivery.

No End To Cash Burn

While Zomato CEO Deepinder Goyal showed bullishness over quick commerce in the most recent investor presentation at the end of FY22, the segment has turned into a highly competitive space.

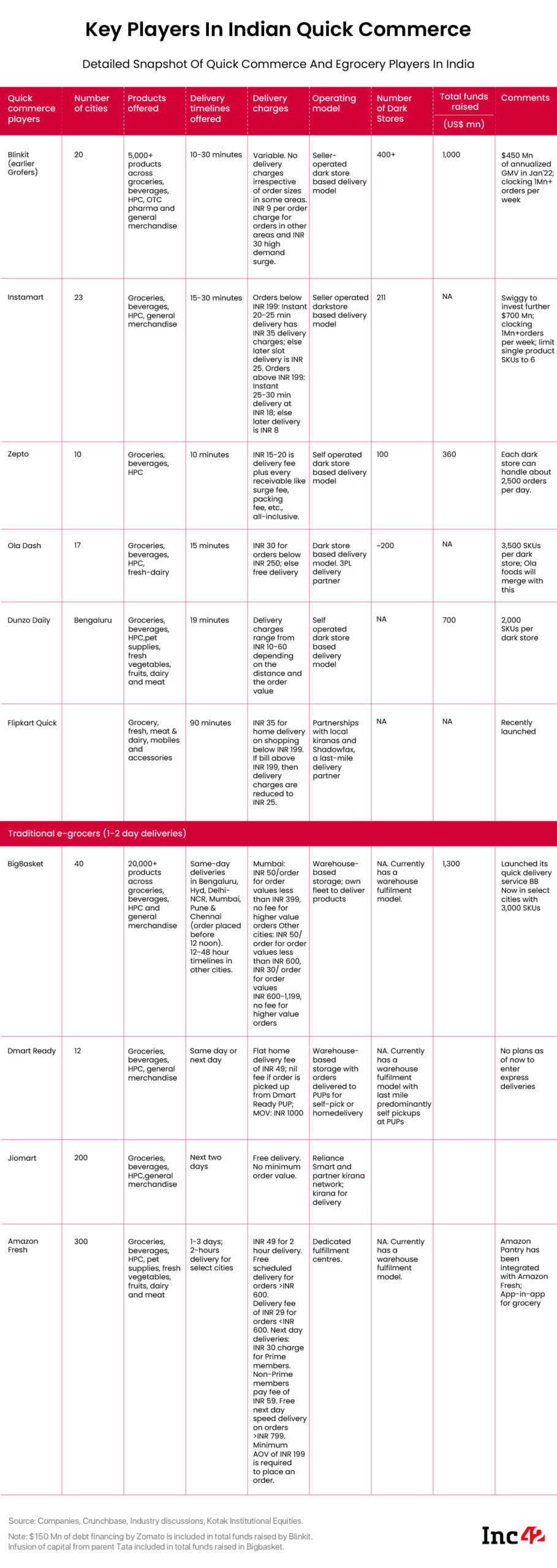

The feeling is that quick commerce will require substantial and constant cash infusion as the likes of Swiggy, Zepto, Dunzo, Ola, BigBasket, Amazon, JioMart and Flipkart vie for a piece of the pie.

According to a research note by Kotak Institutional Equities, the next two-three years may see a large amount of investments by these players in a bid to acquire and retain consumers, fuel habits, set up dark stores as well as fulfil and deliver orders on a cost-effective basis.

“We predict that the industry as a whole may incur ~$750 Mn of cash burn over the next three years, before turning contribution margin positive in FY2025 and EBITDA positive in FY2027,” Kotak’s note said.

According to Kotak, for viable unit economics in quick commerce, customer acquisition costs (discounts) will have to come down while delivery time and delivery charges for customers will have to increase.

While the quick commerce vertical will likely evolve gradually, one area that Zomato is looking to target is instant food delivery or 10-minute delivery of pre-packaged food and beverages.

This proposal of 10-minute delivery was met with concerns about the safety of delivery partners as well as pressures on restaurants around food quality and preparation time. While Zomato has said that it is looking to tackle these issues from the get-go, the Zomato Instant food delivery is yet to take off beyond the pilot stage.

“We feel that implementation cost will be much higher even after considering the additional subscription revenue, leading to more losses,” Sharma said about Zomato Instant.

New Verticals, Old Problems

What makes things worse for Zomato is that it needs more money to run the show and sustain and grow amid intense competition. Even though investors have given a thumbs down to Zomato with the sell-off this week, there is little doubt about the scope of food aggregators and delivery business.

One way that Zomato is likely to boost its overall revenue is through subscriptions that cover not just food delivery but dining out as well. According to reports this week, the company is looking to revamp its Zomato Pro subscription programme to offer incremental discounts on dining out and other benefits.

The hope is that the subscription revenue will offset some of the higher costs related to deliveries or repeat orders. However, the last time Zomato tried to expand its subscription programme and customer discounts, it faced a huge backlash from restaurant partners, many even threatening a boycott.

So even as Zomato looks to widen its revenue streams, it could still face fresh headwinds within these new verticals. Will Goyal & co be able to steer the Zomato ship in the right direction amid the current choppy waters?