Given revenue challenges around UPI and distribution-led models, it’s not surprising that most fintech companies have moved to lending as their revenue rafts

Personal loans and other lending products have become the crutches for super apps in the fintech space as these bring in a steady income and are not subject to seasonality or economic cycles

From personal loans to BNPL to P2P lending, startups have adopted several ways to tap this opportunity but each model comes with its own peculiarities that can complicate the revenue outlook

Digital lending is the new battleground for India’s fintech startups, especially unicorns and giants with super app ambitions.

We have seen the likes of Paytm go from a payments-first mentality to seemingly sustainable growth through lending. Kunal Shah-led CRED is looking at a massive lending play for new-to-credit users. Even PhonePe has made its intentions clear with a bid to acquire ZestMoney, which eventually did not pan out, but we don’t think the fintech decacorn will wait too long before looking at other avenues.

Fintech in India is fast becoming a facsimile for digital lending. Every major fintech player is moving towards loans and credit products to eke out revenue, tap the relatively cheaper customer acquisition opportunity and basically turn profitable.

Indian Fintech Cos Look To Beat Revenue Blues

The revenue problems in the fintech space have been known for several years now. Regulatory intervention has reduced the revenue viability of UPI for payments apps, while credit card-related fintech services have not moved the needle either due to the slow-growing base of credit card subscribers.

Other fintech service areas such as insurance and investment tech have also not delivered the boost in terms of revenue. In most cases, startups earn distribution commission and fees for insurance and investment broking. But this pales in comparison to dedicated players that have the requisite licenses (insurer or AMC) to earn direct revenue from customers. And getting these licenses is also a significant challenge given the regulatory burden.

Given these revenue and operational challenges, it’s not unsurprising that most fintech companies have moved to lending as their revenue rafts. Personal loans and other lending products have become the crutches for super apps in the fintech space as these bring in a steady income and are not subject to seasonality or economic cycles.

“There have been a lot of shifts with startups moving from a payments or distribution play to lending. And the reason is undoubtedly the better revenue outlook for lending, as well as the relatively established playbook for scaling up,” Yashoraj Tyagi, chief operating officer and CTO at CASHe told Inc42.

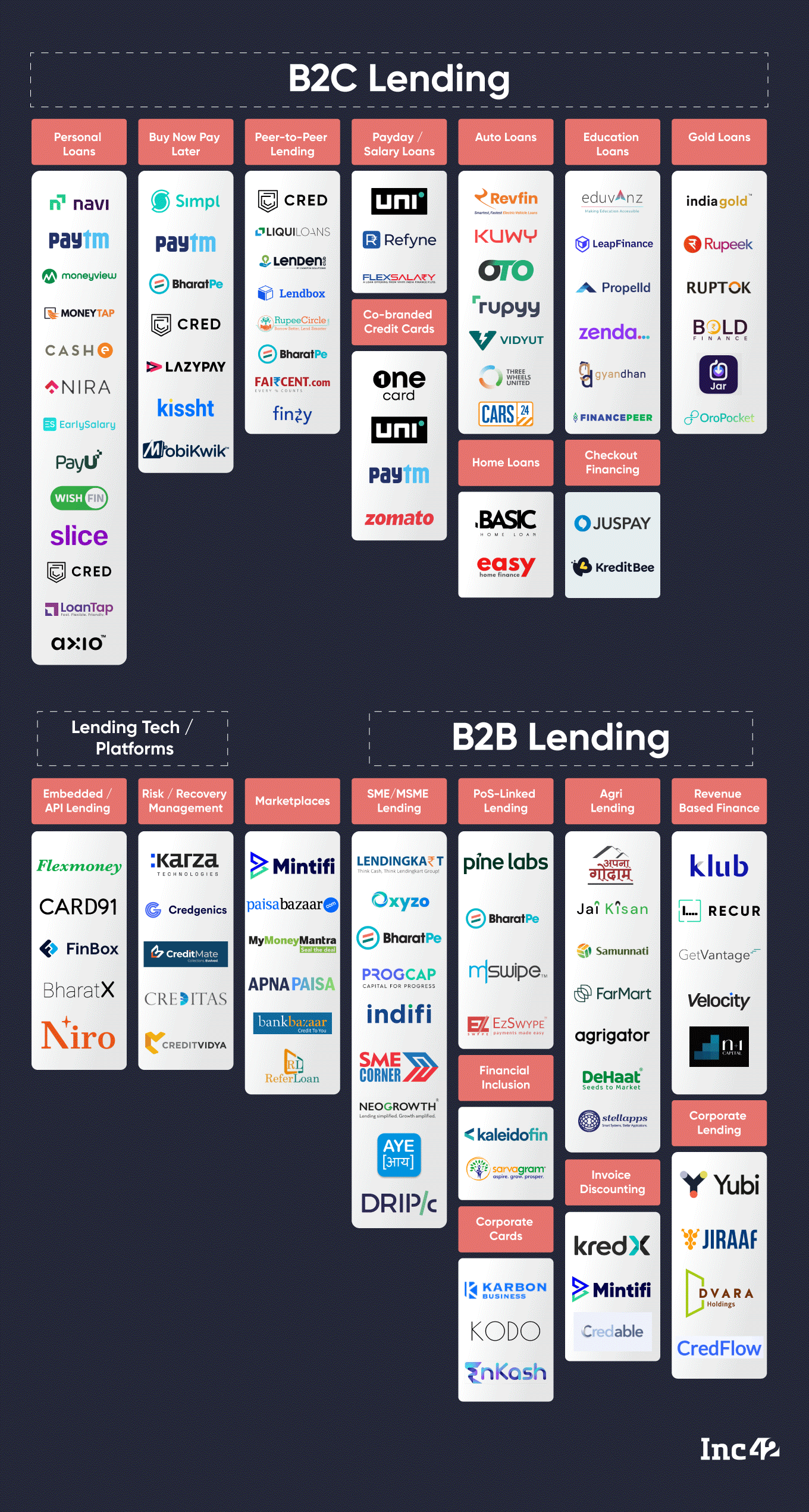

Digital Lending Models Galore

As simple or straightforward as digital lending may have become over the past few years, fintech startups have approached this very differently when it comes to the models. And this is where digital lending revenue models need to be scrutinised — they are not all equal.

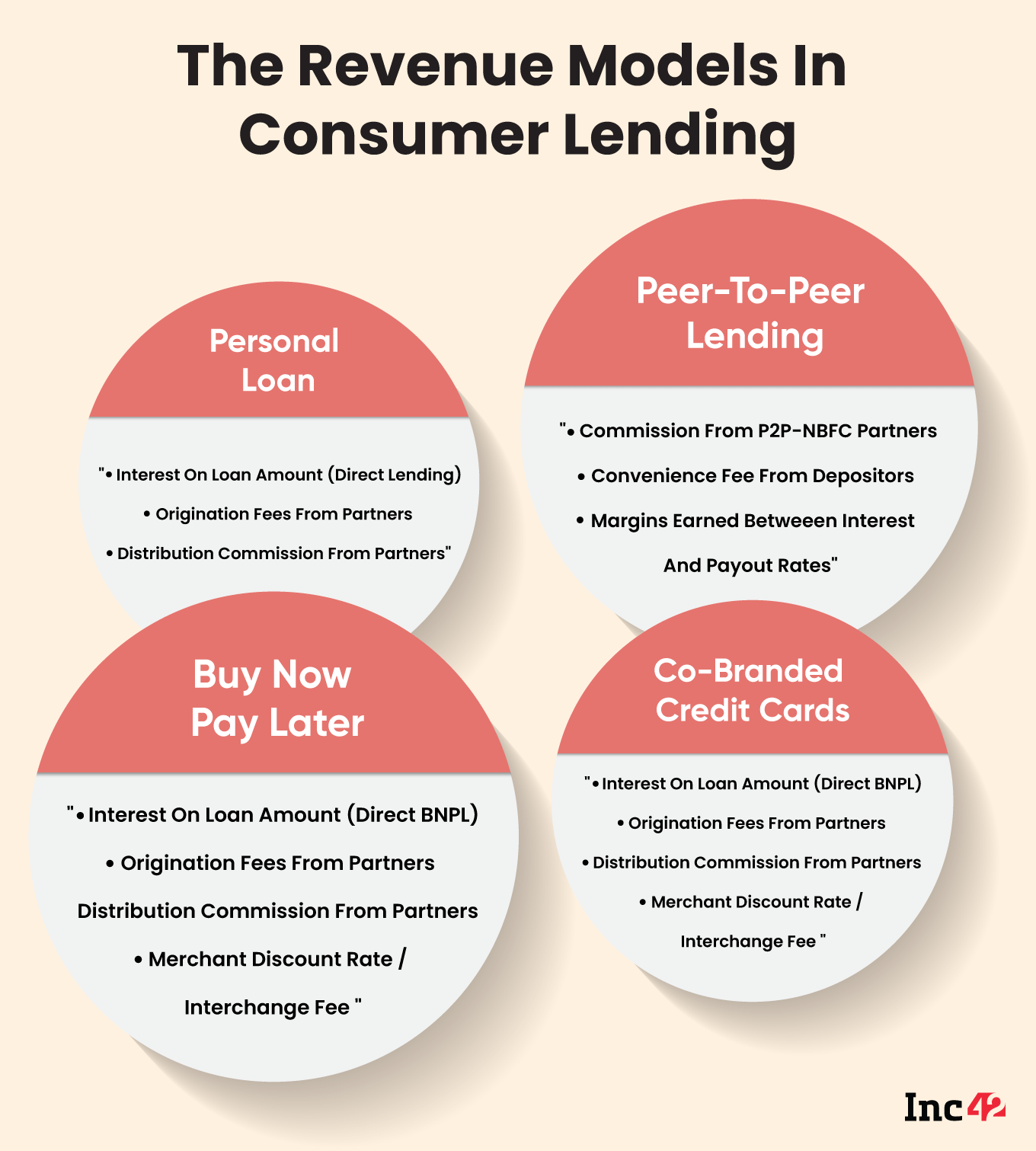

“Today, you will find B2C fintech startups in four primary lending models — personal loans, buy-now-pay-later, peer-to-peer lending and co-branded credit cards. They are all lending products, but each has different revenue implications. The key for startups is finding the product-market fit based on their customer base,” according to Kissht and RING cofounder Ranvir Singh.

Of these, personal loans are perhaps the most well-understood model because the approval and disbursal processes are largely similar to bank loans to consumers.

The partnership model adopted by fintech companies is a response to the regulatory environment around lending. Startups cannot lend directly from their books and therefore have to rely on banks and NBFCs as partners.

“From a market size standpoint, Personal loans are an order of magnitude bigger than any of the BNPL, P2P lending or co-branded credit card products. Almost 90% of the digital lending market would be personal loans,” Singh estimated.

Why Personal Loans Is The Best Bet For Digital Lenders

Further breaking down the revenue model around personal loans, he says there are three primary ways companies make money through lending.

Firstly, there’s the interest payments, which is perhaps the biggest chunk of revenue, but not all startups can avail this, particularly if they are lending through partners.

Then there’s the fee structure for each loan, which borrowers usually see as the processing fee for the loan. This includes the origination fee from the bank or NBFC partners as well as a distribution commission depending on the size of the loan.

Besides this, startups can also leverage the lending business to upsell insurance or investment products through their distribution channels, which would fall under add-on income.

But the revenue promise starts falling apart when you examine the number of competitors in this space as well as the reliance on partnerships for lending. Lending directly through in-house NBFCs or small finance bank licences is a much larger revenue proposition than lending through partners, but not all startups have this advantage.

In effect, finding the right partnership is key for startups. “Some startups may feel that banks and NBFCs don’t offer the right terms and commissions for personal loans because their user base does not match the bigger players. In other words, startups with larger scale will have cheaper and better access to capital for lending,” according to the CEO of a Mumbai-based checkout finance startup.

The founder did not wish to be named since the startup works with a number of banks for co-branded solutions.

Will The BNPL Boom Translate Into Revenue?

When it comes to BNPL, startups have access to the various revenue streams that are attached to personal loans, but there’s a merchant discount rate or interchange fee as well, which makes it a lucrative revenue play for startups.

BNPL startups earn income from both sellers and consumers. In the case of sellers, there is an interchange fee ranging between 2% and 8% of the purchasing amount. On the customer front, by charging an interest ranging between 10% and 30% based on their credit score, and repayment tenure. On average, the interest rate is around 24% for BNPL, according to the startups we spoke to.

However, unlike a personal loan, this interest is only charged if the availed BNPL amount is not repaid on time. Besides interest, there’s a minor late fee component as well.

Even when it comes to MDR, small-ticket BNPL spending which is typically seen in online food delivery or grocery delivery, does not have too much revenue potential.

“When BNPL customers purchase from the likes of Swiggy or Zomato, the sellers don’t have to shell out too much MDR, but for larger ticket items, the MDR can be significant, which is why BNPL adoption is lower for categories such as consumer durables, appliances and other high-value products,” Kissht’s Singh told Inc42.

BNPL is often seen as a gateway towards entering personal loans territory, because customers with propensity to use credit are more likely to become future customers in the personal loans business.

So often, BNPL players leverage partnerships to become distributors of personal loans, but here the revenue potential is much lower, since there’s just a minor distribution fee involved.

But BNPL represents something of a grey area in lending since models have changed multiple times and nowadays, startups are straddling the line between BNPL and personal loans. BNPL by itself, has a high degree of risk, competition, and consequently higher cost of credit sourcing.

More than anything, BNPL is about adding to the base of creditworthy individuals, and reaching new-to-credit consumers.

This can be highlighted by Paytm’s example. At the end of FY23, Paytm cut its net loss by 25% largely on the back of the growth in its lending business. Founder and CEO Vijay Shekhar Sharma was confident of growing this even further due to the low penetration of the loan business among the total monthly transacting user (MTU) base.

However, on the lending side itself, one potential stumbling block could be that Postpaid or BNPL has grown the fastest quarter-on-quarter at 30% compared to 17% for personal loans and 26% for merchant loans.

The company admits that even as it has grown its Postpaid acceptance network in the past year, it will need the loan ticket size to grow. The larger base of Postpaid users are key to bringing more borrowers on the personal loans side as well as credit card users, Paytm said in its results.

RBI’s notification last year banning PPI or digital wallet players from offering credit products has more or less changed the dynamics of this industry and reduced the revenue potential of BNPL. It has forced many of them into the personal loans fold, where the MDR and interchange fees are not revenue options.

Last year, the central bank changed the rules around lending through PPI or digital wallets, which had grown prevalent thanks to fintech startup partnerships with banks and NBFCs. Almost overnight, the likes of Slice, Uni, Jupiter and LazyPay had to change their lending model and rework features that disrupted operations.

Further, RBI also released the long-awaited digital lending guidelines, which includes the potential for legislative intervention in lending-related issues. While the guidelines primarily apply to banks and NBFCs, it did ruffle some feathers for startups that partner with these banks.

Decoding The P2P Lending Promise

If BNPL is an unstable model, P2P lending is even more so, say fintech founders.

Firstly, the regulatory situation is less certain, and revenue streams are not well defined. Even in this model, many fintech startups such as CRED or Jupiter act as distribution points for registered P2P lenders aka P2P-NBFCs.

So startups largely rely on a thin slice of the margin (bulk of it going to registered P2P players) between the principal amount and the interest paid back.

Simply put, P2P lending involves a platform connecting individuals who deposit funds to those who want to borrow these funds. “On the depositor side, P2P lending companies can charge a convenience fee. There are some restrictions around how much convenience fee can be charged because depositors expect a return from the P2P player,” Tyagi said.

But Kissht’s Singh reckoned 90% of the players make money on the difference between the interest charged to the borrowers and the returns paid out to depositors. The margin becomes the primary revenue source, but this is usually split between the regulated P2P entity and the fintech startup.

P2P lending is a bigger grey area because of the relatively high-risk profile of the borrowers, since they are largely individual borrowers. For depositors, the risk assessment of a P2P platform is paramount. Without risk assessment of borrowers and adequate systems to recover bad debts, P2P lending loses the investment value proposition.

There’s also a threat of depositor-run on P2P lending platforms (not the NBFCs behind them) as depositors might misread signals in the market to withdraw funds en masse.

The RBI is also keeping a close eye on how P2P-NBFCs operate, their default guarantee agreements with fintech players and also the interest rates. The source of depositor funds is another concern for the regulators.

The central bank is reportedly seeking details from P2P-NBFCs about partnership models with consumer-facing fintech applications, the flow of funds, risk sharing and other details. P2P lenders are regulated non-banking finance entities that need to share business updates with the regulator.

Co-Branded Credit Cards: The Big Future Opportunity?

Unlike BNPL and personal loans, co-branded credit cards have a relatively uncomplicated revenue model.

Startups earn a distribution commission from banks for acquiring new customers, plus they get some share of the MDR paid by the merchant to the bank. Besides this, there is some integration with the main fintech platform in terms of rewards and loyalty points, which becomes a secondary or tertiary source of revenue.

Banks prefer this approach because it relies on less manpower on their end, and a lot of the activation and engagement around the credit card is also driven by startups.

But as a revenue source, co-branded credit cards are only a big boost when the offering platform has large reach and scale. It makes sense for the likes of Amazon, Zomato and Paytm which have hundreds of millions of users, but smaller startups will need to spend heavily to first acquire customers and then convince banks to enter into partnerships.

Further, fintech startups offering co-branded credit cards or credit card challenges have taken a regulatory beating in the past year.

Most of them have suffered a loss of credibility due to issues surrounding SBM Bank, which was a key partner for credit card challengers such as Karbon Card, Happay, EnKash Card, Kodo, RazorpayX, Open Card, Velocity, and OneCard.

In December 2022, SBM India blocked all transactions on prepaid cards directly funded through its loans and credit facilities, which disrupted operations for credit card challengers.

Then in January, the RBI further directed SBM Bank (India) Ltd to stop all transactions under the liberalised remittance scheme, due to certain material supervisory concerns observed in the bank. This caused more friction for users of co-branded credit cards.

But in recent times, credit cards have become key drivers of card transactions. With 250 Mn card transactions for merchant payments in April this year, credit cards overtook debit card swipes, which stood at 220 Mn. In terms of value, credit cards accounted for INR 1.3 Lakh Cr of all swipes compared to INR 53,000 Cr for debit cards.

Interestingly credit card usage has jumped 20% YoY, while debit card usage has dropped by 31% since last April. India currently has over 85 Mn issued credit cards, up 10 Mn in the past year and more than double the number of issued CCs in 2020.

The entry of a number of co-branded credit card players is largely due to this influx and the expectation that credit card usage will skyrocket as the economy matures and per capita income grows.

Fintech’s Focal Point: Digital Lending

Of course, neither debit nor credit cards are anywhere close to UPI, which had 536 Cr merchant transactions in May, up from 254 Cr last year. UPI payments is easily the primary digital transaction mode for most consumers in India today, but the zero MDR regime around UPI has made it an engagement product, rather than a revenue product.

Lending is really the only vertical that is providing sustainable revenue growth to startups given that the zero MDR ruling for UPI has made revenue generation tricky for apps in this space. While distribution revenue from insurance and other segments is significant, it is not something that will yield great profitability for fintech companies.

While the increased scrutiny on digital lending is definitely a headwind, that has not stopped fintech giants from exploring various models. Besides the revenue upside, there’s the fact that a lending playbook is ready in India.

As per Inc42’s State Of Indian Fintech Report Q1 2023, the lending tech opportunity is estimated to grow to $270 Bn by 2030. Consumer lending is the most sought after segment by Indian startup investors due to the larger addressable market and growing demand for credit-led consumption in India.

Consumer lending has garnered nearly half of the total funding for lending tech (2014-2022). CASHe’s Tyagi believes there is a precedent being set by startups that are pure-play lending operations, which can be easily adopted by the wider fintech industry to solidify their lending foray.

More importantly, partnership models are also established and the regulatory uncertainty around digital lending can largely be avoided with the right partnerships. He added, “Companies don’t have to develop rich features or marketing experiences for their lending plays. And with the right partners from a range of RBI-authorised lending entities, they don’t have to do the heavy lifting either.”

There’s little doubt that digital lending (the business and the tech) has become a huge focal point for fintech companies. CRED’s acquisition of CreditVidya, PhonePe’s attempt to snap up Zestmoney and Paytm’s growing dependency on loans for sustainable growth in the future are clear signs of larger players taking lending very seriously.

The big threat for fintech players is that banks that are seen as partners right now could become competitors down the line, especially if they continue to harbour their own super app ambitions like Kotak and SBI have.

Abhishek Singh, COO and the former head of business at Lendingkart, believes that while the B2C opportunity is wide and everpresent, it is also helping B2B lending players reach the untapped market.

Indeed, Lendingkart is an MSME-focussed digital lender and does not have a personal or consumer loans portfolio. But B2B digital lending is also fuelled by consumer loans, Abhishek added.

Consumers are able to increase their discretionary spending and this increases the working capital needs of merchants, SMEs and small businesses that cater to consumers. “Consumers today need ecommerce sites to offer options such as BNPL or other embedded credit features. As a result online merchants are on the forefront of adopting B2B tech to enable these features.”

This in turn has driven adoption of BNPL products, POS-based financing, checkout financing and other niches within the B2B digital lending segment. The other is the raft of technology players that are enabling lending for merchants and businesses.

From embedded or API-based lending products, risk management SaaS players, credit recovery and collections platforms to credit score data facilitators, India’s digital lending landscape is made up of more than just loan apps. But the fact is that consumer lending is the centre around which a lot of these platforms are revolving.