Despite the CBDT having touched upon the points raised by investors, the latest draft rules only address the angel tax issue in bits and pieces

Introduced in 2012, Section 56(2) (viib) of the I-T Act was meant to be an anti-abuse law to discourage shell companies and black money circulation

Experts believe that the latest amendments to Rule 11UA would impact Series A to Series D startups, thereby making the funding winter grimmer

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

A few days ago the Central Board of Direct Taxes proposed a set of amendments pertaining to Section 56(2)(viib) of the Income Tax Act, 1961. This announcement brought a sense of relief to the Indian startup ecosystem and global investors, who hoped that the long-standing battle against the angel tax had finally come to an end.

Well, the nifty proposal comprising seven valuation methods and keeping six broad categories of non-resident investors outside the ambit of angel tax, among other things, was aimed at the same. However, with the devil in the details, The Finance Act of 2023 has yet again revived the ghost of the angel tax.

While adding more valuation methods and keeping a certain class of non-resident investors outside the ambit of angel tax and price-matching features are positive steps that have been welcomed by the industry, however, they do not solve the larger issue concerning angel tax.

This is also because a lot still depends on how assessing officers (AOs) exercise their power, and it is highly likely that a host of non-resident investors may end up coughing up taxes despite exemptions.

Before we get into the details, it is important to understand the core issue and how it has become an unending headache for startups and investors.

Angel Tax Was Meant To Keep Shell Companies & Black Money Circulation At Bay

Introduced in 2012, Section 56(2) (viib) of the I-T Act — income from other sources — now infamously called the angel tax, was meant to be an anti-abuse law to discourage shell companies and black money circulation.

The tax was payable on capital raised by unlisted companies if the value of the shares issued to investors exceeded their fair market value (FMV).

If the share value is less than the FMV, then the difference between the FMV and actual price is taken as “income from other sources” for angel investors, making them liable to pay an angel tax of 30.9% on the share premium issued by unlisted companies.

Let’s consider a scenario where a startup raises INR 2.5 Cr by issuing 20,000 shares at a price of INR 1,250 per share (a premium of INR 250 on each share). The fair market value (FMV) of these shares is determined to be INR 1,000.

In this case, as per the angel tax regulations, INR 50 Lakh [(1,250-1,000) X 20,000] of the funding raised would be considered income from other sources. Consequently, the company would be required to pay angel tax amounting to INR 15.45 lakh on the INR 2.5 Cr funding it received.

Until 2016, Section 56(2) (viib) was primarily unheard of among the startup community. But then some AOs started questioning the valuations of startups, directing them to shell out 30.9% in taxes.

But Startups Got Grilled In The Process

Between 2017 to 2019, several angel tax-related cases were reported widely. The cases would go on for several quarters with no clarity in sight. Most startups would hardly sustain that long and spend their funding money, time and efforts on fighting legal matters than developing products or focussing on businesses.

In 2019, Inc42 reported dozens of cases in which startups claimed refunds against the angel tax. Meanwhile, some startups even had to shut their shops or bribe AOs to keep surviving.

In November 2018, the Ministry of Consumer Affairs (MCA) issued notices to more than 2,000 startups that had raised money since 2013. The notices were mostly sent to the startups whose valuations had fallen after the first round of fundraising.

Government Comes To The Rescue

Amid uproar from the startup ecosystem, the DPIIT, in a notification issued on April 11, 2018, stated that certain shortlisted startups could skip the angel tax bump during their startup ride.

According to the notification, once a startup fulfils certain criteria, the inter-ministerial board would further analyse every startup and decide whether the entity under consideration was eligible for the exemption under the angel tax or not.

The threshold for startups to claim exemptions under the angel tax was:

- The aggregate amount of paid-up share capital and share premium of the startup after the proposed issue of shares not to exceed $1.5 Mn (INR 10 Cr)

- If the investor or proposed investor, who proposed to subscribe to the issue of shares of the startup has:

- The average returned income of INR 25 Lakh ($38K) or more for the preceding three financial years

- A net worth of INR 2 Cr ($300K) or more as of the last date of the preceding financial year

- If the startup has obtained a report from a merchant banker specifying the fair market value of shares in accordance with Rule 11UA of the Income-tax Rules, 1962

Clearly, angel tax exemption failed to do much for startups and investors, as they continued to get harassed by tax officials.

As a result, the DPIIT and CBDT issued a notification on February 19, 2019, saying, “All the startups are allowed to receive angel tax exemption regardless of their share premium values given that the aggregate amount of paid-up share capital and share premium of the startup after issue or proposed issue of shares, if any, does not exceed INR 25 Cr.”

The CBDT also promised not to proceed against pending cases of startups pertaining to angel taxes.

However, there was a catch.

To qualify for the exemption, startups were required to fill Form 2, wherein they declare that they do not engage in acquiring assets such as land or buildings, stock-in-trade, loans and advances, motor vehicles, aircraft, yachts, or any other mode of transport with an actual cost exceeding INR 10 lakh, unless these assets are held by the startup for the purpose of plying, hiring, leasing, or as stock-in-trade, among other conditions.

As on June 21, 2019, a total of 944 startups applied for angel tax exemption, out of which the CBDT exempted 702 startups under this provision.

Most of the startups passed this in silence. Until February 2021, hardly 8% (3,612 startups) of then 44K recognised startups filed form 2 to avail exemptions under the angel tax.

Explaining the issue, 3one4 Capital partner Siddarth Pai said, “If you fill out the self-declaration form 2 then you may have to abide by the don’t do list of some 12 activities, with some being permissible basis one’s business model. The issue lies in three restrictions: loans & advances, shares & securities & capital contributions. This means salary advances, creating a subsidiary or JV, M&A all get impossible to execute. Even when regulations demand a subsidiary or alternative structure, one can’t undertake it due to these restrictions.”

“That’s how tightly they did. And in case you violated, you pay the tax when you represent and pay a fine that is two times your tax, along with interest & penalties. You would end up losing close to 85 to 90% of your money. Who will take that risk?” Pai added.

Finance Ministry Drops Another Bomb

Just as the Indian startups recorded the lowest quarter of funding in the last five years, finance minister Nirmala Sitharaman, during her budget speech earlier this year, proposed another amendment to Section 56(2) (viib) which brought non-resident investors under the ambit of the angel tax.

This majorly impacted foreign investments. While offshore funds invest in startups, it’s little compared to how much these funds invest in infrastructure and real estate projects in India.

Amid cold response from the investors, the CBDT in a set of proposed modifications to Rule 11UA has now stated that:

- The number of prescribed valuation methods be increased from existing two to seven

- Certain categories of non-resident investors are exempted, including sovereign wealth funds, pension funds, endowment funds, and broad-based pooled investment vehicles where the number of investors in such vehicles or funds is more than 50 and such fund is not a hedge fund or a fund which employs diverse or complex trading strategies

- Price matching for resident and non-resident investors would be available with reference to investment by VCs or specified funds

- To account for forex fluctuations, bidding processes and variations in other economic indicators, which may affect the valuation of the unquoted equity shares during multiple rounds of investment, the ministry has proposed to provide a safe harbour of 10% variation in value

Now, the CBDT has issued a list of 21 countries from where non-resident investment in unlisted Indian startups will not attract Angel Tax. Interestingly, the list does not include countries like Singapore, Mauritius and the Netherlands.

Does The Proposed Amendment Solve The Issue?

Highly unlikely! Multiple investors that spoke with Inc42 highlighted concerns over how the government will determine the number of investors in an investment fund. In most cases, the number of investors is very less. Further, most investors invest via fund managers because they do not like to disclose their identity.

How does the government plan to count these investors? A master fund has many feeder funds, blocker funds and SPVs for its investments – which are legitimate under their respective regulations.

“Prominent funds & even corporate VCs may have a single investor – so how would one reach 50 investors? This may work for a mutual fund, but not a VC or PE Fund” Pai argued.

Also, many funds invest in Indian startups through their Singapore and Mauritius SPV. Since Singapore and Mauritius have not been included in the list of angel tax exemption list, these SPVs will come under the ambit of angel tax.

On price matching and allowing 10% safe harbour, Bhavin Shah, deals leader at PwC India, commented, “Almost all fresh investments by VC Funds in startups have historically been through compulsorily convertible preference shares. The relaxation provided under draft rules for price matching and 10% safe harbour is restricted to equity shares. It is important that these relaxations are extended to investments by way of CCPS as well.”

“For price matching, the draft rules provide for separate baskets for VCFs and offshore notified entities. The government may consider combining both these under a single basket if they invest in the same round,” Shah added.

Does It Solve The Valuation Issue?

No. The latest proposed draft rules don’t solve the valuation issues of the startups, said some of the AIF partners.

It’s the AOs’ prerogative to the valuation definition that becomes an issue. In most of the previous cases, AOs ask for previous valuation reports and if the startup in question has not performed as per the data suggested in valuation reports, AOs create an issue.

Valuation expert and professor at New York University Aswath Damodaran in his paper “Valuing Young, Start-up and Growth Companies: Estimation Issues and Valuation Challenges” states that it is almost impossible to evaluate an early-stage company.

Yet, in multiple cases, AOs not only refuse to accept the valuation estimated by designated CAs or merchant bankers but also start suggesting valuation methods.

In multiple cases, startup founders even bribe AOs to settle their cases.

India is perhaps the only country where for one funding of a company, three separate reports by three separate entities are filed to three separate regulators — MCA, Income Tax and the RBI under FEMA.

Pai suggested that an SOP for AOs to look at the source of funds to gauge if the premium is warranted would probably help smoothen the process. Valuation is subjective and premium is the consequence of legitimate business decisions.

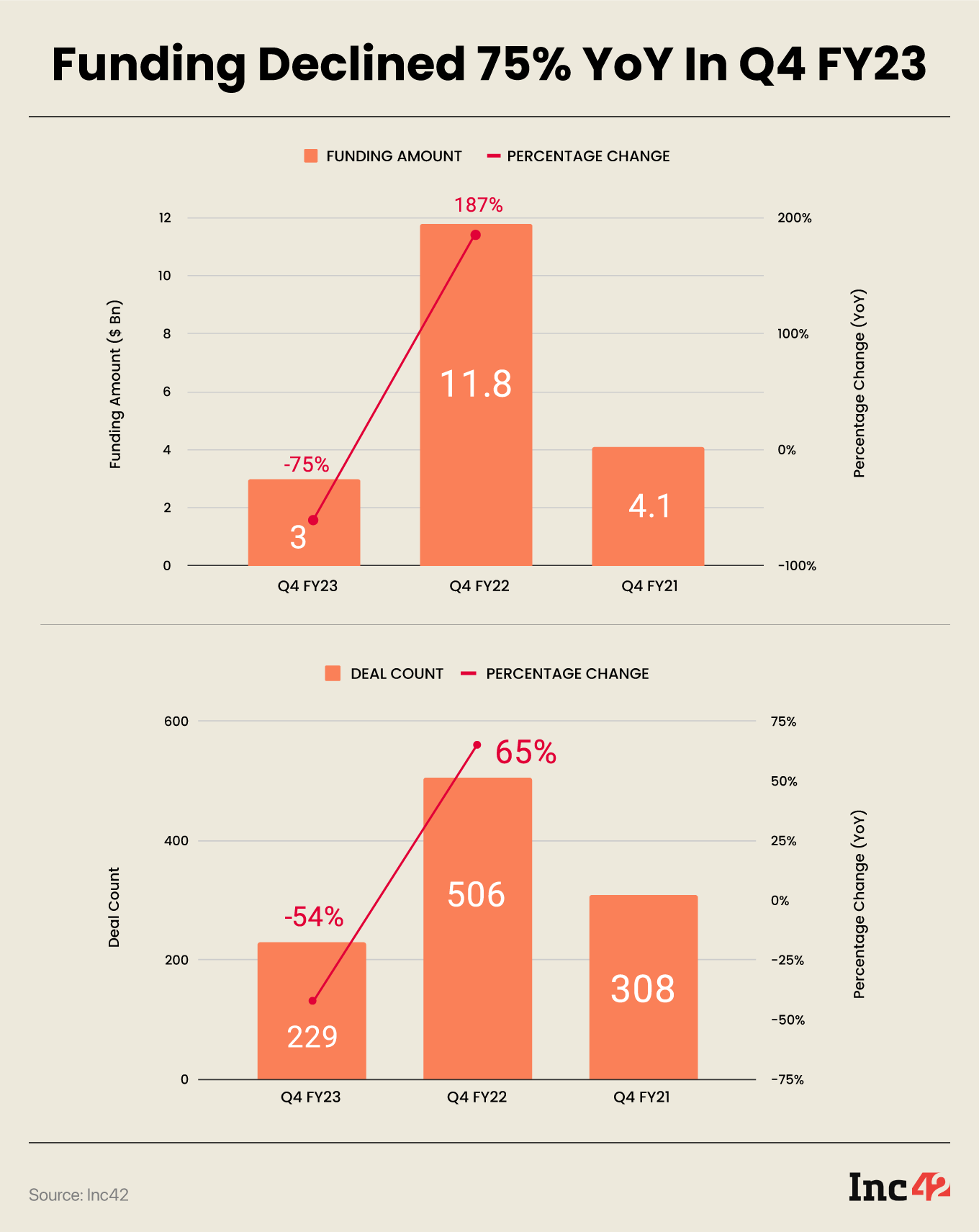

According to data compiled by Inc42, Q4 FY 23 recorded a 75% and 54% YoY decline in startup funding and deal counts, respectively. (See the chart below)

As per reports, while BYJU’S, Swiggy and Meesho are facing down-round challenges, e-pharma unicorn PharmEasy too may raise funds with a 50% cut in valuation. Meanwhile, SoftBank, a prime backer of Ritesh Agarwal-led OYO, marked down the hospitality unicorn’s valuation by 20% on its books, from $3.4 Bn to $2.7 Bn.

Further, at a time when Series A to Series D funding rounds are mostly supported by SPVs and other non-resident funds, failure to get exemptions under Section 56(2) (viib) of the Income Tax Act, 1961, will only dampen the investment sentiment further.

“This step may hit the startups most between Series A and Series D as VCs need small reasons to delay the funding,” Pai said.

Among other suggestions, Anil Joshi, the managing partner of Unicorn India Ventures, suggested that the definition of startups which is valid for 10 years also keeps a large number of companies outside the ambit of benefiting from the exemptions formulated under the angel tax regime.

While the government needs to rethink its stand on angel tax, it also needs to understand the basics of Section 56(2)(viib), which, in the first place, was introduced as an anti-abuse law and not a tax-harvesting instrument.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.