![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?](https://inc42.com/cdn-cgi/image/quality=75/https://asset.inc42.com/2021/03/Outline-58_Feature_Final_1360x1020_feature.jpg)

Small VC firms are engineering powerful frameworks for early-stage funding

Dear Reader,

Stories abound about the camaraderie between startup founders and VCs. But how often have you heard about an LP (limited partners invest in VC funds) rolling up his sleeves to solve the pain point of a startup?

When Narendra Karnavat, whose son is an LP in Artha Venture Fund, came to know that a few of the VC firm’s portfolio companies were struggling to finance inventory and capital assets, an idea struck him. Karnavat, the promoter of a listed NBFC called Glance Finance, decided to extend revenue-based financing to these companies to meet their working capital requirements.

His micro-lending business found a new funnel altogether while solving the funding needs of those startups. But taking this offbeat route to startup funding would not have been possible for an LP in a large VC fund with a huge portfolio and billions of dollars in investments.

“In a large VC fund, your investments are passive — you can’t actively participate in the fund. My fundamental thesis of investing in a micro VC fund as an LP is that I can meet the fund manager every few weeks for a cup of coffee and discuss business ideas,” says Karnavat.

Micro VC funds do not have a watertight template. These are usually defined by their points of departure from traditional and large VC funds. But here are five key points that can differentiate them:

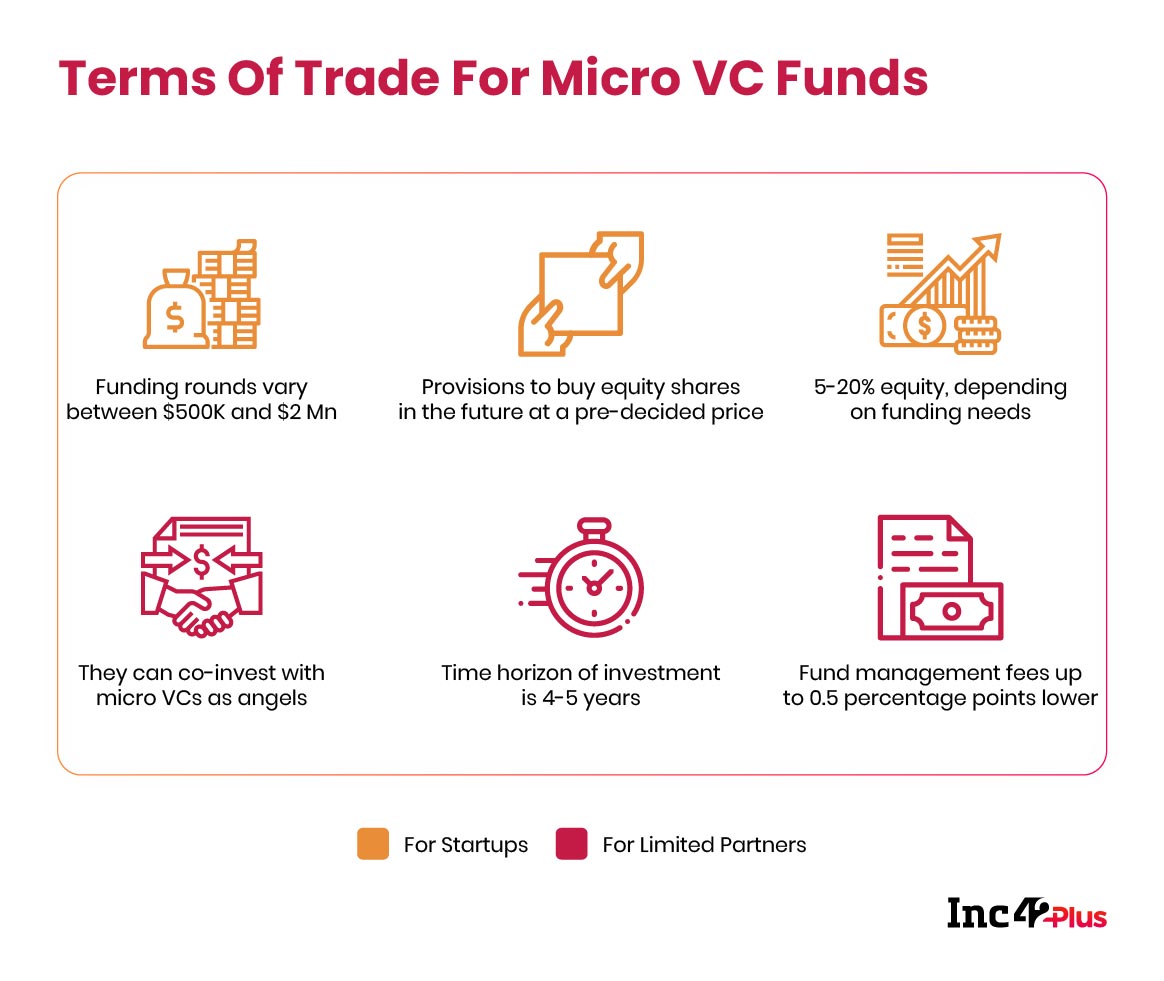

- Micro VCs write smaller cheques of $200K-$1 Mn, while large VC firms tend to pour multiples of $10 Mn.

- The fund size can be up to $20 Mn to $30 Mn (large VC funds can be upwards of $1 Bn).

- A micro VC has a fund manager who runs it almost single-handedly, unlike the army of partners and analysts that large VCs employ.

- Micro VCs seek exits in the growth stage, but large VCs want the fruit to ripen till the late stage or an IPO.

- They do not generally commit to follow-on rounds.

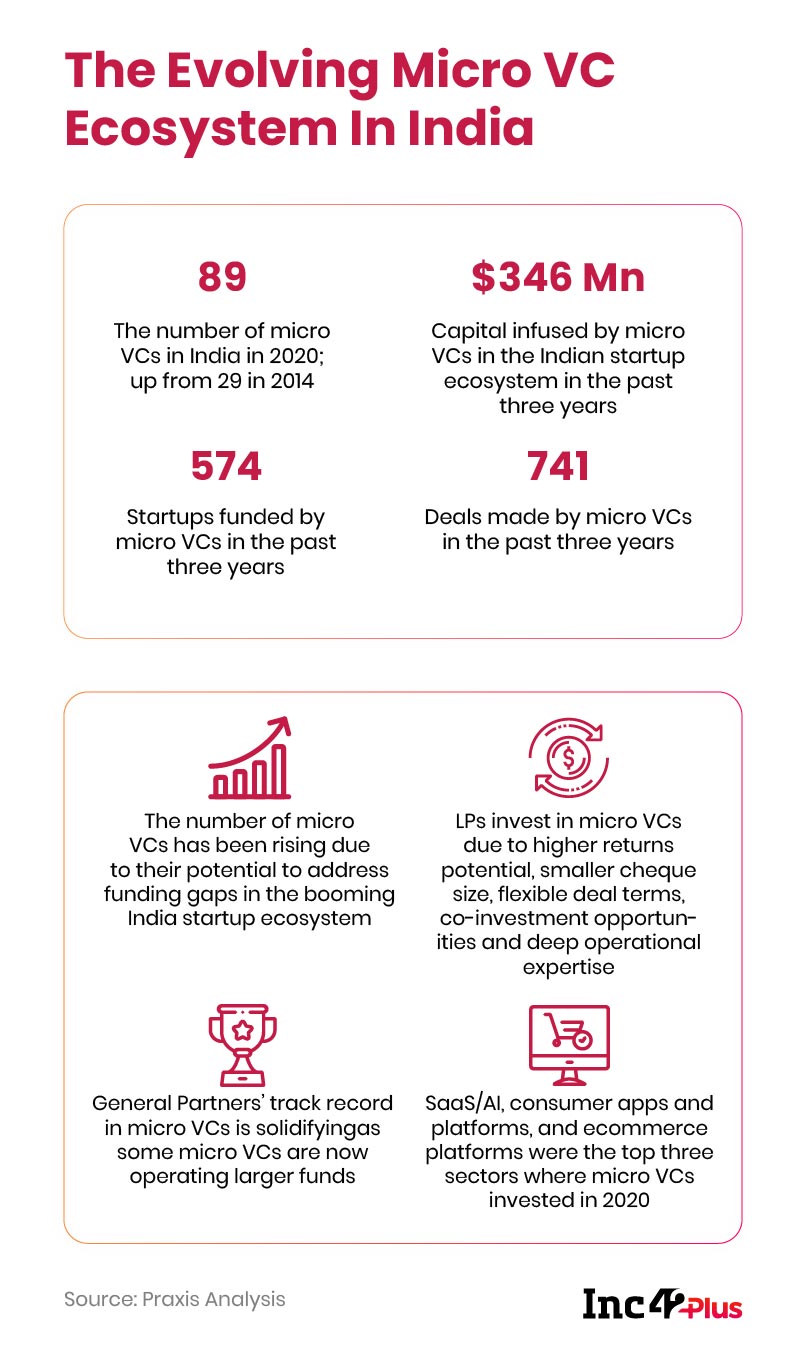

Although micro VCs have been around for a decade now, it is only in the past few years that the trend has caught up due to multiple factors. These include the RBI’s monetary easing, leading to more money in the financial system, startups delivering big-bang exits and the SEBI regulations governing alternative investment funds (AIFs) getting stricter to protect investors. According to a report by Praxis, there were 89 micro VCs in India in 2020, up from 29 in 2014. During 2014-2020, these funds infused $346 Mn through 741 deals in 574 startups.

“The maturation of the VC ecosystem happens when the informal fundraising infrastructure is subsumed into the formal, SEBI-sanctified construct. With the onset of the angel fund regulations, micro VCs have found the perfect platform to launch their fund management careers while adhering to the laws of the land. This will enable more structured investments into startups, which will add more value to the Indian startup ecosystem,” says Siddarth Pai, founder-partner of the VC firm 3one4 Capital that has more than $200 Mn of assets under management.

Another key reason micro VCs are gaining currency is that several angel investors, who used to fund startups (with small cheques) in their individual capacity, have raised concerns that they frequently get cornered to exit at lowball valuations. For instance, he/she could be misled to sell the shares at 10x and then discover that the company got a big VC round that would have delivered 100x gains. Therefore, when angels with small appetites (in the range of INR 25 Lakh-1 Cr) invest as LPs in micro VC firms, their interests are protected.

What’s The Deal For Startups

If angel investors are a bit wary of acting in their personal capacity, startups, too, are not keen to raise angel funding unless it is worth something more than just the cheque. Of course, they would love to welcome the big names to their cap table as it gives them a lot of positive PR, but startup founders try to steer clear of the wealthy nobodies from nowhere.

There is an excellent reason for not keeping the cap table too crowded. After all, a $500K cheque from a micro VC is always better than five angels putting in a hundred thousand dollars each. It means a founder need not chase and convince four other investors to raise the same amount of money. Moreover, it is not surprising that large VC firms considering a Series A or B round are put off by a messy ownership structure. In the fast-paced world of tech startups where fortunes hinge on making strategic decisions at lightning speed, boisterous boardrooms are not palatable for them.

Sanjay Mehta, founding partner of the micro VC fund 100X.VC, says, “Micro VC firms also help startups by mentoring them and networking with the ecosystem. More importantly, what matters to them (startups) is the visibility they get. It shortens the time needed to attract the next round from a large VC.” Interestingly, Mehta’s claim to fame lies in securing big-bang exits as an angel investor from companies like hotel aggregator Oyo and logistics tech platform LogiNext.

Being at the helm of affairs at 100X.VC, he has also designed a desi Y Combinator of sorts with an interesting investment playbook. Here are the key pointers:

- It invests in cohorts of 10 startups and each startup gets a cheque of INR 25 Lakh.

- Investment is made against ISAFE notes — a method that YC pioneered in 2013. These are securities that can be converted into equity shares in the future.

- Funding is completed within a week compared to the average three-month period required for traditional VC funding.

- There are no follow-on rounds of funding.

Why Small Numbers Work Well For Micro VCs

Although 100X.VC does not participate in follow-on rounds, Artha Venture Fund’s managing partner Anirudh Damani believes that the option to provide another round of funding gives his firm an edge over other micro VCs. “Founders come to us for the primary round of capital so that there is only one investor on the cap table. But we can also write a cheque up to six times that amount as a follow-on. That initial cheque is a small amount for large VC funds, and they may not be interested, in which case it becomes very difficult for the startup to solicit investments from other big players,” he explains.

The corpus size makes a marked difference in the maths of micro VCs and larger funds. For instance, a micro VC can offer seed capital of INR 2 Cr for a 10% stake and then follow it up with additional rounds of up to INR 10 Cr for another 10% at a later stage (assuming that the standard rise in a company’s valuation in follow-on rounds). If the startup grows to become a $100 Mn business, which is not a rarity now, the micro VC can avail of a $20 Mn exit — an amount that is likely to cover the fund’s entire corpus size. This means all other exits from the fund’s portfolio will be just profits.

Something similar happened recently when the VC fund IvyCap made an INR 330 Cr exit from the online beauty marketplace Purplle. The returns from the INR 15 Cr investment overshot the fund’s INR 240 Cr corpus by a margin of INR 90 Cr. “A large VC firm will not buy this as it will need unicorn exits to cover even its smallest fund sizes of about $200 Mn (approximately INR 1,450 Cr at current exchange rates) or more,” adds Damani.

There is another angle to the maths of micro VC investments. As large VCs progress from being big fish to whales with billion-dollar funds to deploy, many feel that young startups are becoming more judicious in how they spend the ‘Big VC’ money.

Suraj Malik, partner at the financial consulting firm BDO India, says, “Earlier, investors expected that a technology startup in India would need at least $1 Mn to grow meaningfully. Now, with the capital efficiency improving in the ecosystem due to better talent and other enabling factors, one can also build a successful startup with a smaller cheque size.”

But it is not only startups who are finding innovative ways to survive and thrive. Micro VCs are also pushing the envelope to attract LP investments and discover startups with potential. If some of the micro fund managers are heading to Tier 2 and Tier 3 cities to find LPs and startups, others are writing newsletters and creating podcasts to grab attention.

Of course, many of these fund managers want to become large VCs themselves one day, and it gives first-time players an opportunity to cut their teeth on the game. That is how they learn what it takes to manage the big bucks. In a way, micro VC firms are a sandbox for them to find out if their investment models are working or not.

Forging A Royal Connection

British Royal Prince Harry is joining Silicon Valley startup BetterUp as chief impact officer. Following the Wall Street Journal report, New York-based VC investor Matt Turck took a dig at Britain’s colonial history in a tweet that went viral.

Sequoia’s Two Reasons For Celebration

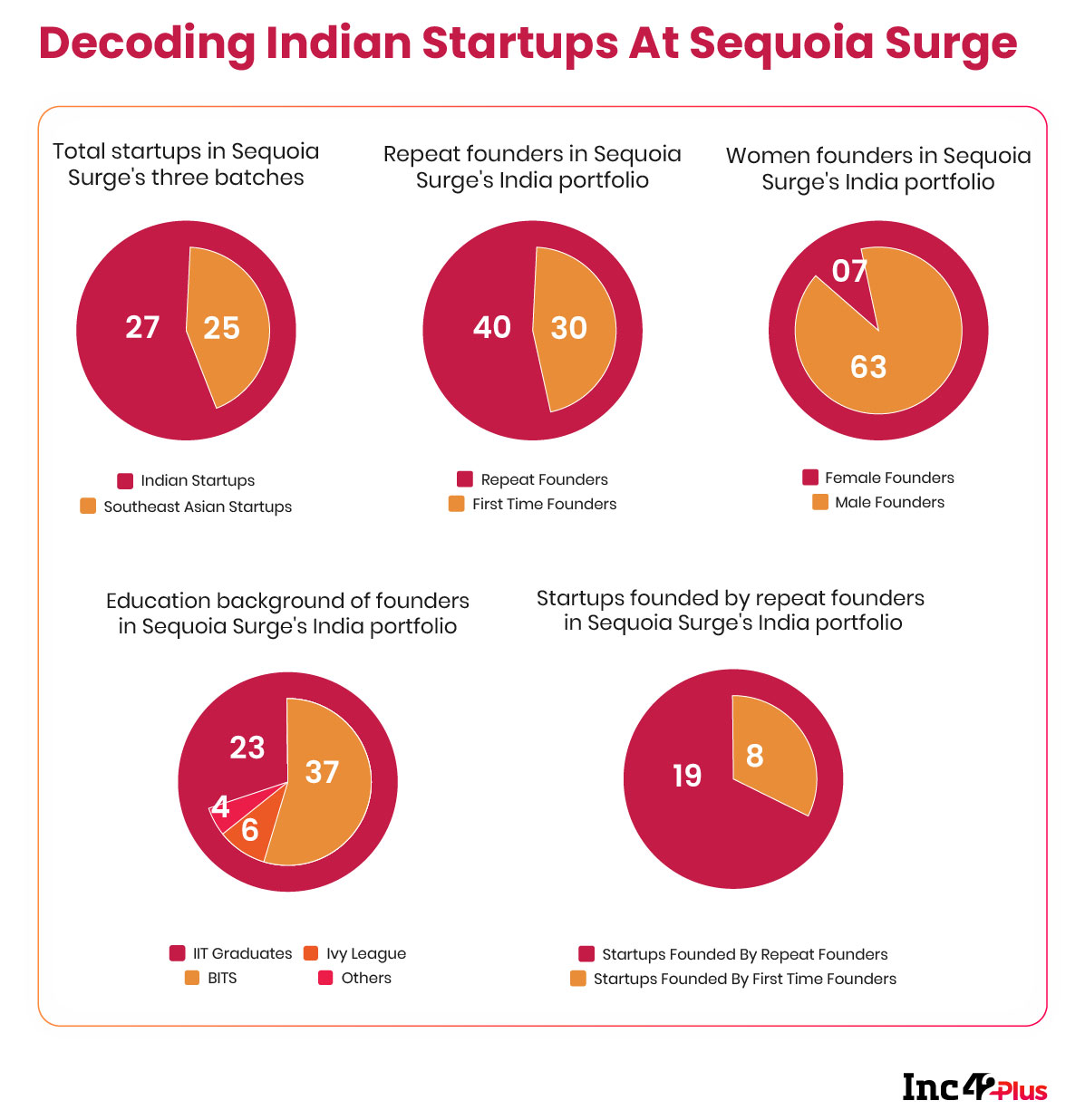

As micro VCs dominate the early-stage deal flow, large VC firms are now coming up with incubators and accelerators to fund seed-stage startups in India. This week, Sequoia Capital India closed its second seed fund at $195 Mn as part of its accelerator programme Surge.

Shailendra J. Singh, a managing director at the VC firm, tweeted that Surge completed its second anniversary on the same day (March 25). Although the VC firm boasts funding 69 startups through Surge, an Inc42 report published last year and based on the analysis of the first three batches of the accelerator programme found that almost 50% of the startups backed by it were founded by repeat founders.

Indian Startup Funding Could Get A Liftoff

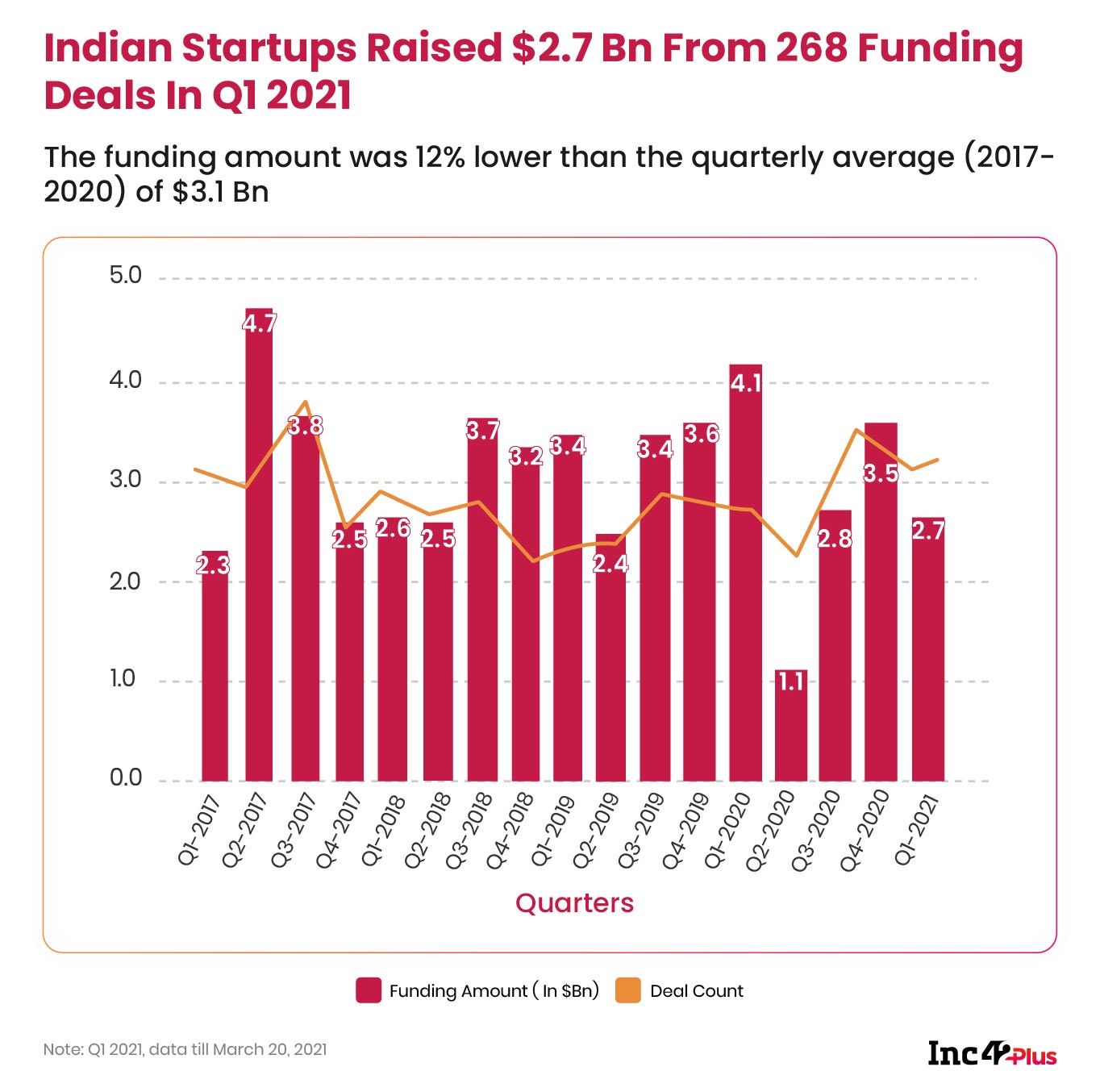

In the first quarter of 2021, Indian startups raised $2.7 Bn from 268 funding deals. The funding amount was 12% lower than the quarterly average (2017-2020) of $3.1 Bn, according to an upcoming Inc42 Plus report. However, the deal count was 20% higher than the quarterly average of 223.

In the wake of the developments in the country’s foreign direct investment (FDI) policy that restricts Chinese investment in India’s burgeoning startup ecosystem, the government and the industry stakeholders have been exploring various ways to increase access to under-utilised asset classes within the country.

Given that the EPFO, holding about $6.9 Bn, is one of the biggest pools of investable cash, the government has opened a small window to test how well Indian VCs can marshal funds. Although that sum still remains out of reach, the finance ministry has allowed domestic private provident funds to invest up to 5% of their surplus in AIFs, of which VCs are a subcategory.

“This is a defining moment for India as it means government backing and support towards domestic managers and funds,” said Ishpreet Singh Gandhi, founder and managing partner at Stride Ventures, a Delhi-based VC firm.

As the government is looking to attract domestic capital for Indian startups and make the new-age economy ‘Aatmanirbhar’, it has included an important caveat: Funds have to ensure that investment should not be made directly or indirectly in securities of the companies or funds incorporated and/or operated outside India.

Even though we take a critical stance now and then on the government’s policies impacting startups, this is a move that merits applause. After all, the wealth created in India should not leave the country.

Until next time,

Deepsekhar

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/featured.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/academy.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/reports.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/perks5.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/perks6.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/perks4.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/perks3.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/perks2.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/perks1.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/readers-svg.svg)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/twitter5.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/twitter4.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/twitter3.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/twitter2.png)

![[The Outline By Inc42 Plus] Will Micro VCs Rule Early-Stage Funding?-Inc42 Media](https://asset.inc42.com/2023/09/twitter1.png)