Unlisted shares of IPO-bound startups are seeing a lot of demand in grey market trading

Dear Reader,

The IPO bug has bitten a lot of tech startups and every couple of weeks there seems to be a new company eyeing the stock exchanges. It’s hard to miss the excitement around these IPOs — soon after a startup declares its plans of going public, the price of its unlisted shares in the grey market start soaring.

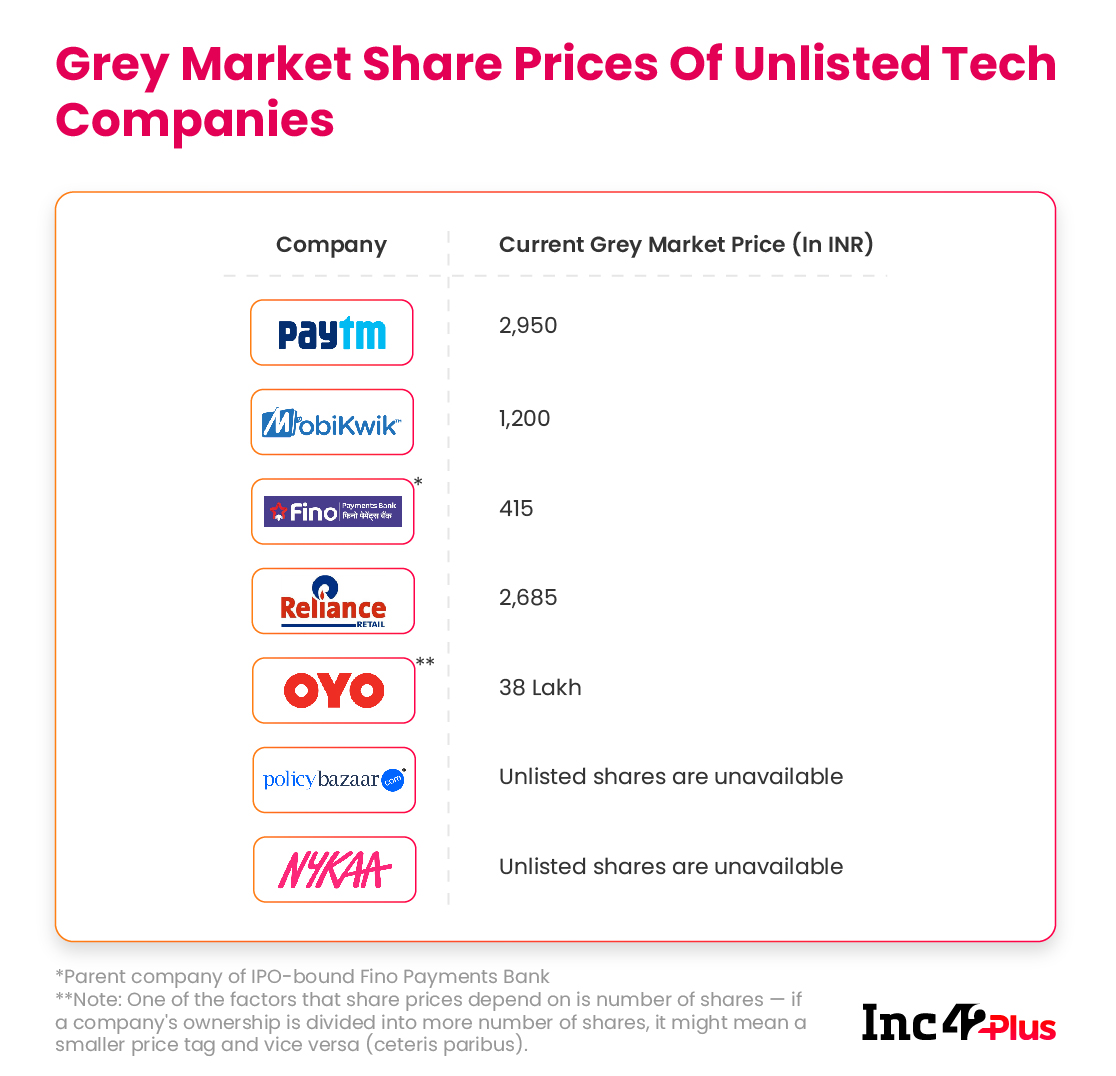

Like in the case of IPO-bound Paytm, where the fintech giant’s unlisted share prices rose more than two-fold from the INR 11,000-INR 12,000 range to above INR 24,000. Similarly, when Fino Payments Bank filed its IPO prospectus out of the blue, the shares of its parent company Fino PayTech jumped from INR 300-INR 325 to INR 375.

These surges in share prices even before the listing is not unique to India. However, the market for unlisted shares is not very well understood in India, as typically retail investors only take a position in a company only after it hits the bourses. This is not just about playing it safe in terms of the investment, but also sometimes, IPOs are postponed or scratched off like in the case of WeWork a few years ago, which hurts the unlisted prices also.

Plus, it also protects individual investors against fraudulent practices by companies as SEBI keeps a watchful eye on every action of a listed company, but may not be so stringent before the listing.

Which prompts the question: Why are small individual investors suddenly going for shares in the grey market?

According to Vishal Chandiramani, managing partner of wealth management company TrustPlutus Wealth India, one of the main attractions is that one can buy as many shares as are available in the unlisted market, while IPO allotment of shares is limited. Moreover, share allotment happens by a lucky draw in the case of IPOs like Zomato, where the number of bids exceeded the number of shares for sale by 40 times. This means that buying unlisted shares can help an investor eliminate the luck of the draw.

But there is also a catch: unlisted shares or securities have a lock-in period of one year from the date of the public listing. It is a provision that the SEBI has formulated to protect the interests of the small retail investors. This helps in ensuring that promoters, founders and VCs, who usually continue to hold large amounts of unlisted shares in a company even after the IPO, do not sell off in haste to book gains and thus catch small investors unawares.

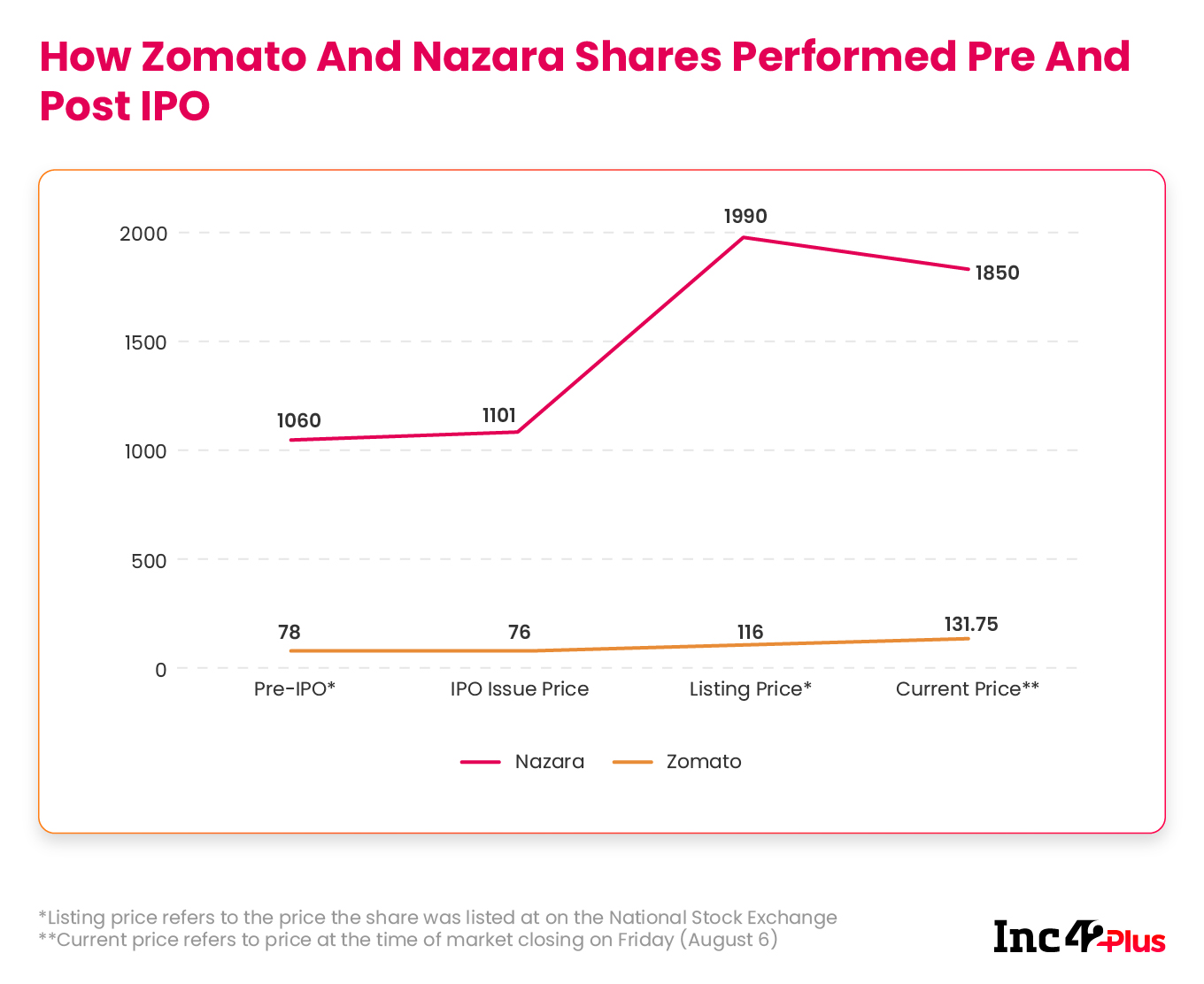

That is why investors in unlisted shares can not benefit from a possible listing gain — the rise in a share’s price after it’s allotted during the subscription to when it is listed on the stock exchanges. For instance, the issue price of gaming company Nazara’s shares in the IPO was INR 1,101 whereas its listing happened at INR 1,990 on the National Stock Exchange — so an IPO allottee made a profit of 81% on the first day of itself. Similarly, Gurugram-based food delivery startup Zomato listed on the bourses on July 23 at INR 116, a 53% premium over the issue price of INR 76 per share.

One Year Is A Long Time

While the two cases of Nazara and Zomato have been a source of comfort and encouragement for many investors in the unlisted share market, there is of course an element of risk associated too. While HSBC has sounded a word of caution on the Zomato stock and signalled a target price of selling at INR 112, global brokerage CLSA said that Nazara faces a revenue risk and the company’s stock may suffer a 41% crash.

Sandeep Ginodia, CEO of unlisted shares platform Altius, who has been facilitating the buying and selling of such securities for over two decades, says “Yeh zamana hi tech ka lag raha hain (This seems to be the age of tech stocks) … I do not understand how there is such a demand for companies that make little money. While most people get into unlisted shares thinking that the IPO issue price will be more and the listing will be at a higher price still, they should not forget that there have been duds in the past.”

While he cites cases such as UTI Asset Management that listed last year at a price lower than that of the IPO issue price, perhaps recent tech listings provide a better example. San Francisco-based food delivery company DoorDash, which went public amid much fanfare in December 2020, has seen its share price drop as much as 48% from its listing price of $189. No one is sure what its fortunes will be come December 2021.

One of the prime examples of a star tech stock that did not perform well in its first year of listing in recent times is Uber. It got progressively worse even before the pandemic — its issue price of $45 was called a ‘flop’, then it listed at a loss at $41.6 in May 2019, before sliding to $27 in December that year, and ultimately hitting a low of $21 in March 2020. It has slowly climbed back up in recent months after the worst of the pandemic was over in Western nations.

This is why TrustPlutus’ Chandiramani tells his high net-worth clients that they should invest in unlisted stocks with a horizon of 12-18 months, and only if they have a high risk appetite. Further, such shares should never be more than 5%-10% of the portfolio, even if the investor is aggressive.

Moreover, investors do not have to necessarily go on solo expeditions to bet on IPO-bound companies. Asset managers like Edelweiss, IIFL, Kotak Investment Advisors have recently launched pre-IPO schemes which invest in late stage technology companies — these are large funds of sizes upwards of thousands of crores and invest in a basket of unlisted shares, compared to an individual investor who might pick out a few.

The biggest advantage here is that there is a margin of safety: the funds strike deals such that the price at which they buy into an IPO-bound company is always lower than what the issue price would be. However, the problem here is that only the wealthy can invest in such funds as the minimum investment amount can run up to as high as INR 1 Cr. Plus, the risk associated with the one year lock-in remains, although it is evenly spread out among multiple pre-IPO companies.

All That Glitters Is Not Gold

It is no secret that startups are going for mammoth funding rounds and IPOs because the world economy is flush with cash being pumped in by central banks — led by the US Fed — commonly known as liquidity. Many have pointed out that this is the reason that Series A and below rounds are attracting millions of dollars, rather than superior product or market validation.

Beerud Sheth, founder and CEO of B2B messaging startup Gupshup, recently told Inc42 — many rookie entrepreneurs may make the mistake of thinking, ‘Oh, wow, I got this and that valuation. Now, let me spend it all because my next valuation is going to be higher.’ But there is no such guarantee. If you have not built a viable business, it may not sustain.”

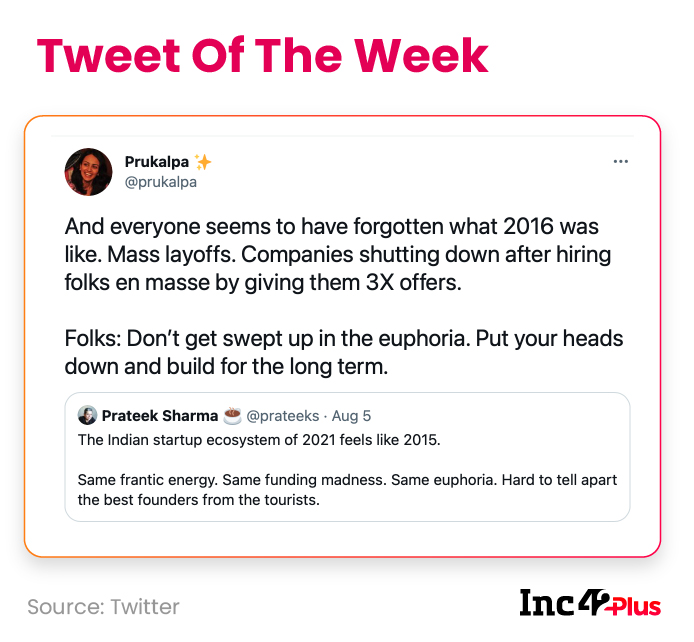

In a year when 19 startups have entered the unicorn club in just over seven months, several stakeholders in the ecosystem are visibly worried about what this might mean. One consequence is the talent crunch created due to soaring salaries in tech roles. Prukalpa Sankar, founder of Sequoia-backed data workspace startup Atlan HQ, and angel investor Prateek Sharma sounded a word of caution about the situation on Twitter.

Separating The Wheat From The Chaff

A startup’s funding history is no longer the barometer by which investors gauge potential bets — relevance and product-market fit is the go-to indicator these days. In such a time, the role of unearthing promising early-stage startups assumes even greater importance.

In our latest edition of 30 Startups To Watch, we have companies helping salespeople turn into micro-entrepreneurs as well as startups that are bringing data-driven decisions to SMBs. We have startups in the electric vehicle infrastructure and charging space, trying to grab the first-mover advantage in a segment that remains largely unaddressed. Then there are HRtech companies addressing the pain points of recruiters and candidates in this ultra-competitive hiring climate, and edtech solutions bringing more upskilling opportunities to future leaders. Of course, while the pandemic hovers over India, health and fitness startups will continue to find the right backers, and will look to go deeper into R&D.

Despite being less than three years old, almost all of these startups have seen significant traction, which is a testimony to their relevance in the new normal. It is our hope that even when the current tide of massive funding runs out, the pace of innovation sustains and grows. Perhaps, a few of these will go for an IPO in the next couple of years, and you might want to be a part of their potential success story, in the grey market!

Until next time,

Deepsekhar

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/featured.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/academy.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/reports.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/perks5.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/perks6.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/perks4.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/perks3.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/perks2.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/perks1.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/readers-svg.svg)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/twitter5.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/twitter4.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/twitter3.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/twitter2.png)

![[The Outline By Inc42 Plus] The Grey Market Rush For Startup Stocks-Inc42 Media](https://asset.inc42.com/2023/09/twitter1.png)