SUMMARY

In April 2022, Dunzo cofounder and CEO Kabeer Biswas said quick commerce is a game of optimisation, but ironically, 18 months later, Dunzo has very little left to optimise

The startup's quick commerce ops are in disarray and more or less winding down, while the growth in B2B operations has not moved the revenue needle enough

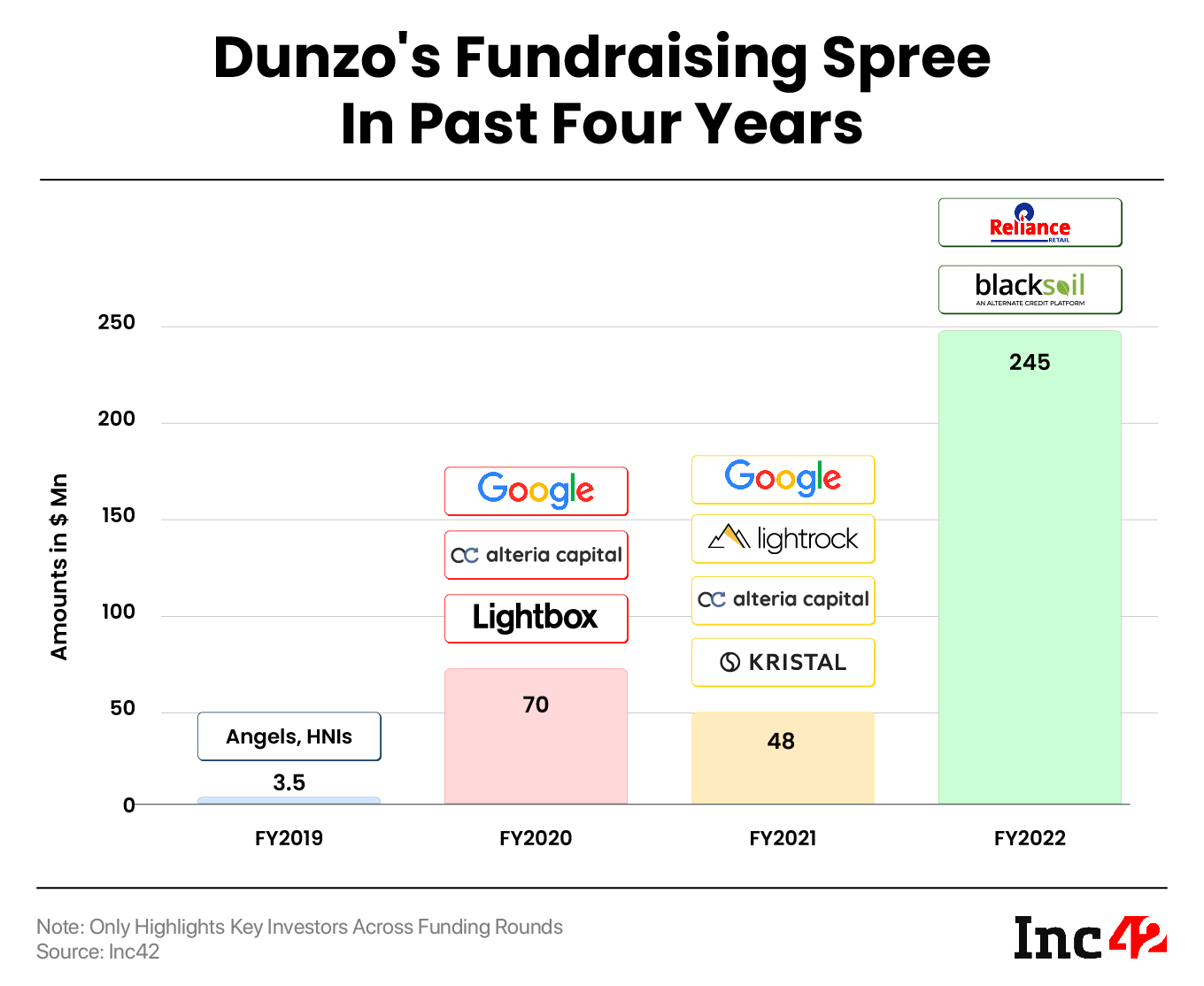

Even after raising nearly $500 Mn, Dunzo’s future comes down to the question: can the company raise more funds in today's funding environment?

In April 2022, dunzo![]()

![]() cofounder and CEO Kabeer Biswas claimed that quick commerce in India is a game of optimisation. He also stated that this is a quest that will drive Dunzo “till a point where we don’t have anything more to optimise”.

cofounder and CEO Kabeer Biswas claimed that quick commerce in India is a game of optimisation. He also stated that this is a quest that will drive Dunzo “till a point where we don’t have anything more to optimise”.

This was of course before Zomato fully acquired Blinkit, before Swiggy Instamart’s rapid expansion and when Zepto was relatively new to the market. But today, these are the players that are still challenging for quick commerce supremacy.

Sadly and ironically, 18 months later, Dunzo has very little left to optimise.

Its quick commerce operations are in disarray and more or less winding down, while the growth in B2B operations has not moved the revenue needle enough to sustain the startup’s employee and resource base.

In the past few weeks, the problems at Dunzo are becoming more and more apparent.

- Severe cash crunch and talent attrition

- Resignations of key board members, including representatives of lead investors

- Resignation of cofounder Dalvir Suri

- Key exits across teams, including multiple rounds of layoffs

- High dependency on debt and payroll financing to sustain operations

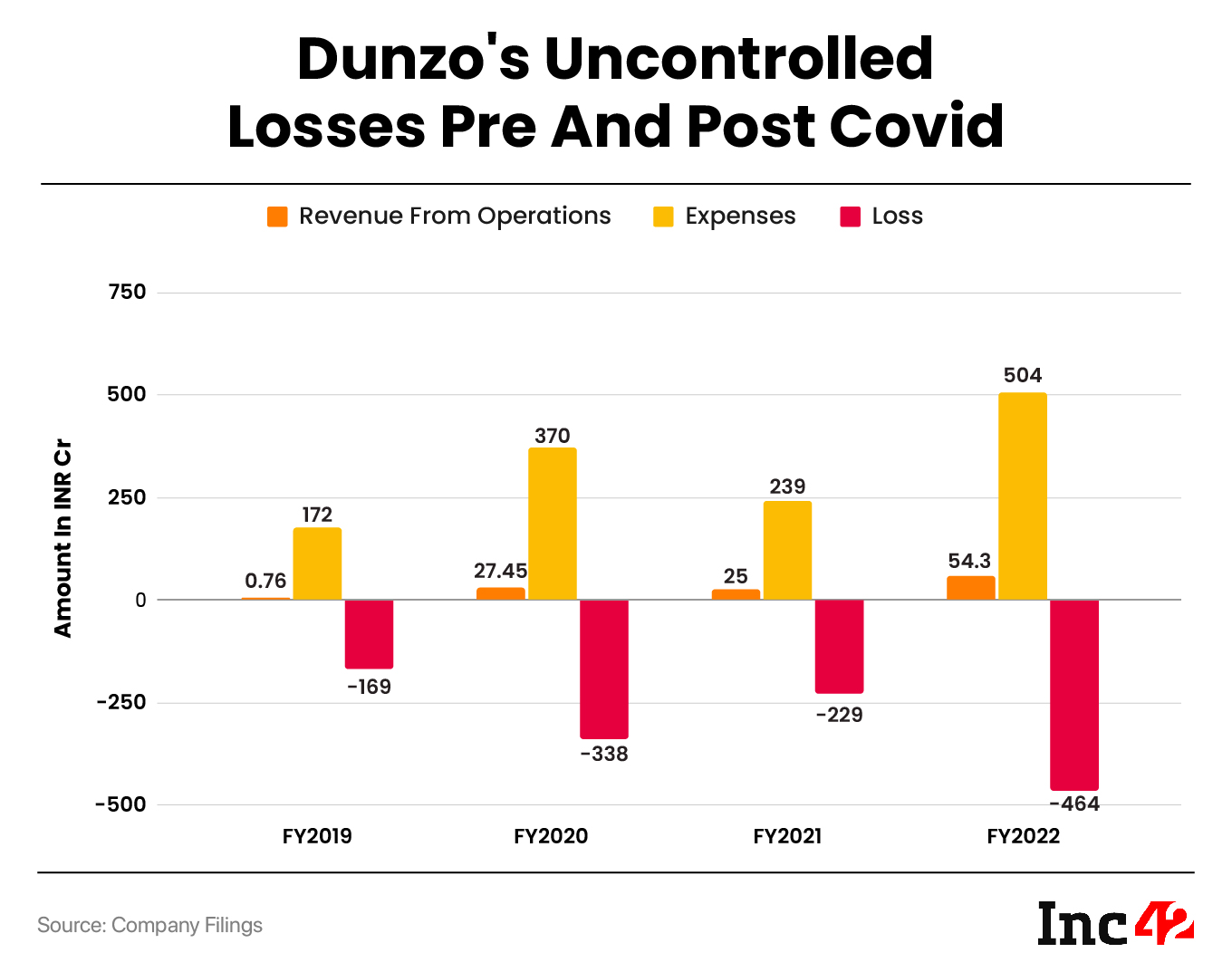

- Cumulative losses of over $150 Mn vs revenue of just around $12 Mn from 2018 to 2022

While some of these problems have stemmed from the recent cash crunch and lack of product direction, the larger issues around uncontrolled losses show that even when Dunzo’s consumer business was seemingly flourishing, the growth was well below expectations when you look at the competition.

Dunzo Fails To Scale Up

As we reported just a couple of months ago, Dunzo is transitioning from a dark store-centric quick commerce business to bringing larger supermarkets and grocery stores on a revenue-sharing basis. This is more or less the original hyperlocal model popularised by Dunzo in its early years between 2015 and 2020.

In late 2020, Dunzo began dabbling in quick commerce through dark stores and invested heavily in the Dunzo Daily product. Even as the quick commerce promise has more or less turned into 30-minute delivery, Dunzo faltered when it came to scaling up.

For instance, last April, Biswas said that while quick commerce as a category can exist in India’s Tier II or III cities, it is important to redefine what convenience shopping looks like for those customers.

He also cautioned that players might end up seeing only sparse network expansion in those markets till consumer behaviour changes.

But where rivals such as Swiggy-owned Instamart, Zomato-owned Blinkit and Zepto managed to push ahead and maintain the scale needed for pan-India quick commerce, Dunzo was only a favourite in certain urban pockets.

In April, the Reliance Retail-backed startup decided to shut dark stores that were seeing less than 1,000 orders per day, as per sources. Now it’s reevaluating more such dark stores and going back to the hyperlocal play in many cities.

On the other hand, Swiggy and Zomato pressed forward by leveraging their core delivery stack for quick commerce. Zepto’s advantage is its deep category focus, which the company’s founders have time and again touted as its key competitive edge. The company claims that its singular focus on quick commerce — unlike Swiggy or Zomato — means it has executional efficiencies unlike the other players.

Quick Commerce Experiment Tanks

The gap is really apparent when you stack up Dunzo’s revenue to Blinkit, Zepto or Instamart.

In FY22, Dunzo’s operating income of INR 54 Cr is way below Swiggy Instamart’s revenue of INR 2,036 Cr, Blinkit’s tally of INR 236.3 Cr and even Zepto, which saw revenue touch INR 140 Cr in its first full fiscal year of operations.

Even a relative newcomer to the space outperformed Dunzo’s operational revenue in FY22.

This is despite Dunzo offering B2B deliveries through Dunzo For Business (D4B) and B2C deliveries under two different models (hyperlocal and dark stores).

Despite having a seven-year headstart on Zepto in many regards, Dunzo managed to only earn half of what the Y Combinator-backed startup did in FY22. This indicates not only a scale problem but also that Dunzo was unable to build revenue momentum in the face of stiff competition.

What makes this decline more curious is that Dunzo had the brand power to press forward on even the slightest product advantage. It had the early mover advantage in hyperlocal deliveries, but when that model was replaced with dark stores, Dunzo became one of the players rather than a trailblazer.

“Competition forces you to innovate in different ways, but Dunzo remained the same. Zomato and Swiggy never stopped experimenting with this category because it’s still evolving. Dunzo did not do that,” says a former KPMG analyst who has advised on a number of startup M&As and led due diligence into retail businesses.

The analyst pointed out that while the likes of Instamart, Zepto and Blinkit have improved their supply chains for fresh produce, and solidified quick commerce models for categories like electronics and beauty, Dunzo was stuck between the decision to scale up dark stores, and continued its B2B play as well as hyperlocal deliveries.

In July, we wrote that there was also a wide chasm between what Dunzo spent in terms of marketing vs the competition. Dunzo’s advertising promotional expenses in FY22 came up to just over 10% of its total expenses, while this was as high as 33% for Zepto.

“Dunzo failed to position itself as a disruptor and did not enter the marketing game of 10-minute deliveries in a big way. Today, no one is delivering products in 10 minutes, but marketing it like that in the beginning helped Zepto and others gain traction and captive users,” according to a former employee, who parted ways with the company in September.

The employee added that product branding and marketing were Dunzo’s strong suits, but the competition went a step ahead by burning a lot more cash in the past two years to promote quick commerce.

What Happened To The Millions?

Even though it received a massive infusion of $240 Mn in January 2022 from Reliance Retail, Dunzo did not manage to push the accelerator in the right direction. And given the current situation around the short runway and the cash crunch, questions need to be asked about where and how the company burnt through so much capital in less than two years.

What makes Dunzo’s downfall alarming is that the company currently clearly lacks funds for day-to-day operations or even paying employees, even as it has raised over $365 Mn since April 2019.

It’s not clear where the company spent most of this money in the past four years. A lot of it would have been poured into expansion of the quick commerce model and the company’s network of dark stores. With competition for dark stores high, real estate prices were also artificially driven up, while procurement gaps and heavy discounting resulted in poor efficiencies.

It’s also not known whether revenue growth was better in FY23 compared to the slow pace in FY22. Dunzo did not respond to Inc42’s questions seeking clarifications on the revenue in the previous or the ongoing fiscal year.

Dunzo is said to have deferred employee salaries to September, while it has an outstanding balance of more than INR 11 Cr to several vendors, some of which have also sent notices to the startup. The company also let go of more than 30% of its workforce to get leaner and arrest the monthly burn.

To add to its woes, Reliance JioMart, the biggest customer of Dunzo Merchant Services (DMS), had cut the prices it paid for last-mile deliveries in June. The move saw DMS’ gross margins reduce by 50-75%, as JioMart accounts for 30-40% of its total business.

To secure much-needed capital, in late September, Dunzo is said to have proposed halving its monthly burn rate to $300K and trim its headcount to just around 200. The company’s monthly burn is said to have been $600K despite several rounds of layoffs and scaling the cash-guzzling quick commerce business down.

Now the question is whether cofounder Biswas can navigate these choppy waters even as other founders have quit the company and even representatives of key investors have resigned from the board in the past few months.

While the departure of cofounder Dalvir Suri was confirmed, Dunzo denied reports about the exit of cofounder and CTO Mukund Jha. Suri has also resigned from the company’s board of directors.

Besides this, Ashwin Khasgiwala, group chief of business operations at Reliance Retail, and Rajendra Kamath, finance head at Reliance Retail, and Vaidehi Ravindran, a partner at Lightrock India, also stepped down from the board. While Reliance has nearly 26% stake in Dunzo, Lightrock owns 8.6% of the company.

As per sources, the remaining board members, including cofounder Biswas, Siddharth Talwar from Lightbox and Hongjim Kim from STIC Investments, are looking to restructure the company and prepare it for leaner times.

The situation at Lightbox — another key investor — doesn’t help matters. The firm is in the process of a breakup at the very top. Partners Siddharth Talwar, Prashant Mehta and Jeremy Wenokur are leaving the Mumbai-based VC, according to sources close to the firm.

Lightbox cofounders Talwar and Sandeep Murthy are likely to separate the fund’s portfolio and part ways. The departing trio is looking to set up a separate fund comprising some Lightbox portfolio companies.

Talwar’s exit from Lightbox adds to the uncertainty around Dunzo, since he remains a board member at the company. It’s not clear whether Dunzo will be separated from Lightbox’s portfolio and go to Talwar’s potential new fund, and whether this will receive shareholder approval.

It’s also not clear when these changes at Lightbox will be finalised.

The Reliance Retail connection has fuelled some chatter about a takeover by the conglomerate, but whether Dunzo makes for an attractive acquisition target is unclear at the moment. The company definitely has the tech, but it has lost a lot of talent and is shedding assets to save costs.

Even after raising nearly $500 Mn, Dunzo’s future comes down to the question: can the company raise funds? The company has been around for nearly a decade, but the fact that it’s come to a basic ‘raise funds to survive’ equation shows just how deep a hole the Dunzo is in.