Covid-19 has forced B2B lending startups and NBFCs to adopt e-Sign, e-Mandate and V-KYC which were partly physical due to SMEs not being digital savvy and lacks in terms of adequate data

Besides the lack of data, the digital quotient of B2B lending is low also partly because most of the technology-developments have been B2C centric and hence ain’t meeting the B2B demands

Credit managers who earlier were required to visit the MSMEs physically to verify their claims are now asked to do the same through video meetings; this also lowers the credit cost

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

India's Digital Lending Reset

India’s digital lending sector is currently in a reset mode as the contracting GDP, moratorium, & Covid-19 has forced companies to adopt digital, review credit models & more. This playbook takes a deep dive into the challenges and new pathways adopted by digital lending startups for survival and scale!

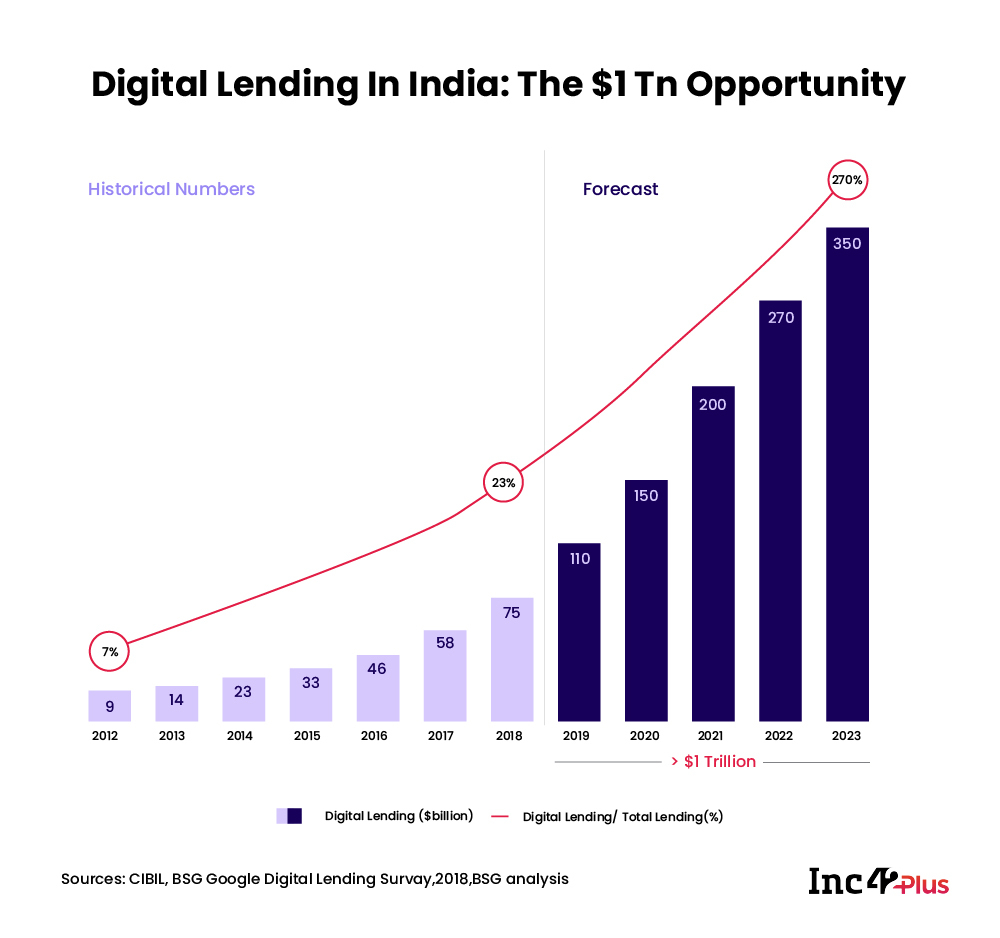

In 2018, Boston Consulting Group had come up with a report estimating India will create a $1 Tn digital lending opportunity between 2019 and 2023. While the total retail loan disbursement was expected to grow at 2.2x, from $330 Bn in 2018 to $730 Bn by 2023, the report estimated the digital penetration in loan disbursal from 23% in 2018 to 48% in 2023, witnessing 4.67x growth in digital lending.

Since the 2010 global economic crisis, lending has constantly been marked as the cash-cow sector, with payments, consumer companies slowly jumping into the bandwagon, extending short term credit loans to their consumers. Behind the growth is the increasing data that companies have been able to accumulate since the fintech revolution post-India Stack, making lending digital, easier and cost-effective.

The policy and technology developments — demonetisation and GST, India Stack APIs, and RBI regulations in this regard — have helped fintech adoption to grow exponentially, from 52% in 2017 to 87% in 2019, according to EY.

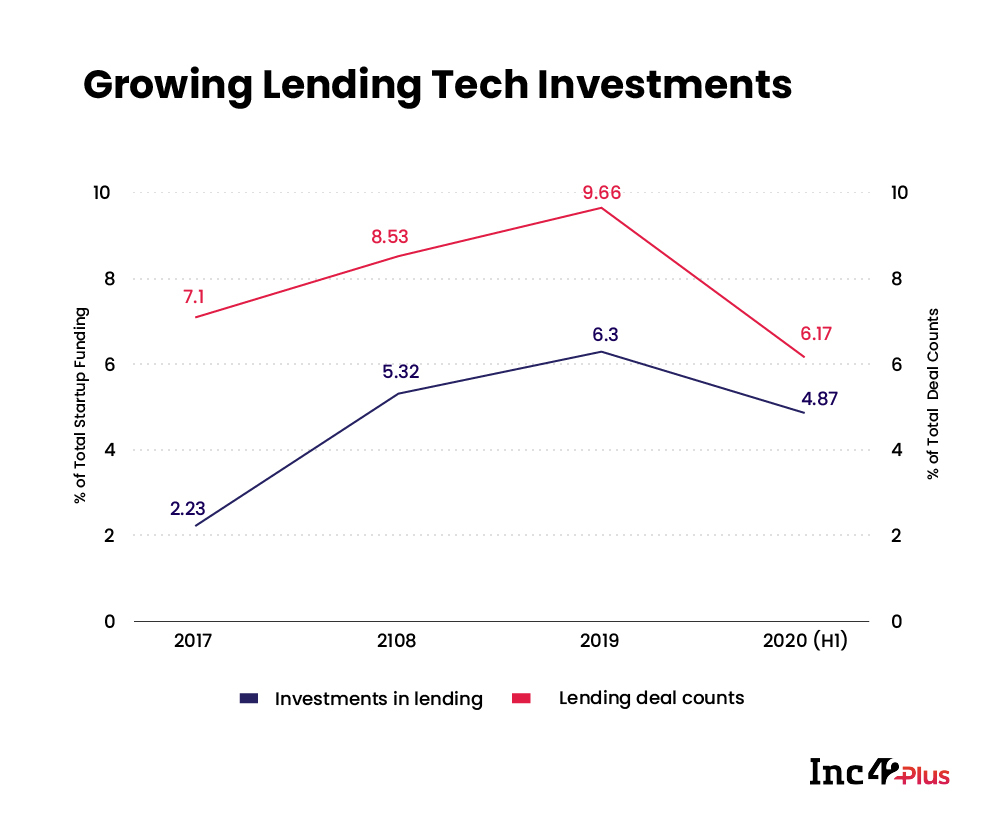

Like the burgeoning payments sector driven by UPI apps, lending has been an attractive area for investors in the last four years. This could also be seen in terms of lending share in total investments and deal counts. In H1 2020, lending despite being down to 5-10% during the lockdown period remained the most attractive fintech area for investments.

Behind the increasing interest in digital lending is also the late twists and turns in the banking sector and lending at large which has forced stakeholders to adopt digital lending as it’s cost-effective, transparent, and saves time as well.

The infamous IL&FS scam among the firsts to shake the entire Indian lending market. Under a debt of INR 94,000 Cr, the investment company defaulted on a few payments, failing to service its commercial papers (CPs) on the due date resulting in the company facing a liquidity crunch.

The IL&Fs crisis along with banking scams of Punjab National Bank, Allahabad Bank, YES BANK, and ICICI bank put the entire lending market through a downturn and led to non-performing assets growing by a huge magnitude. Secondly, a large number of suspect loans provided to industrialists such as Vijay Malya, Nirav Modi, Gitanjali Jewellers’ Mehul Choksi, REI Agro’s Sandip and Sanjay Jhunjhunwala Videocon Group and more also made life difficult for leading public and private sector banks.

The NPA of Indian banks which was supposed to be 1-2% of their two assets under management rose to 8-9%, clearly demanding greater transparency in terms of data, alternate data provided by loan applicants. Lending tech via digital lending/blockchain has certainly increased the transparency level and hence the confidence of investors in lending tech startups which claims provide a better solution, wider reach in the Indian market.

However, the question is, as BCG estimated, is the Indian digital lending market onroads to create a $1 Tn opportunity? Despite the Indian government largely being called a digital banking friendly government in terms of policy initiatives, digital lending could never take off the way it was expected and there remained a huge gap between the demand and supply.

In 2020, the supply crunch made it wider. According to an RBI report, the total addressable credit demand by the country’s medium and small enterprises is pegged at $490 Bn and the overall supply from formal sources is at $192 Bn.

What’s Weighing B2B Digital Lending Down?

While clearly there is a high growth ceiling, tapping the B2B lending market space has not been easy for digital lending startups and certainly not as easy as consumer lending. In stark contrast to the shockingly low credit bureau coverage in the MSME sector of under 10%, the credit bureau coverage of consumers increased from 10.8% in 2007 to over 43% in 2018.

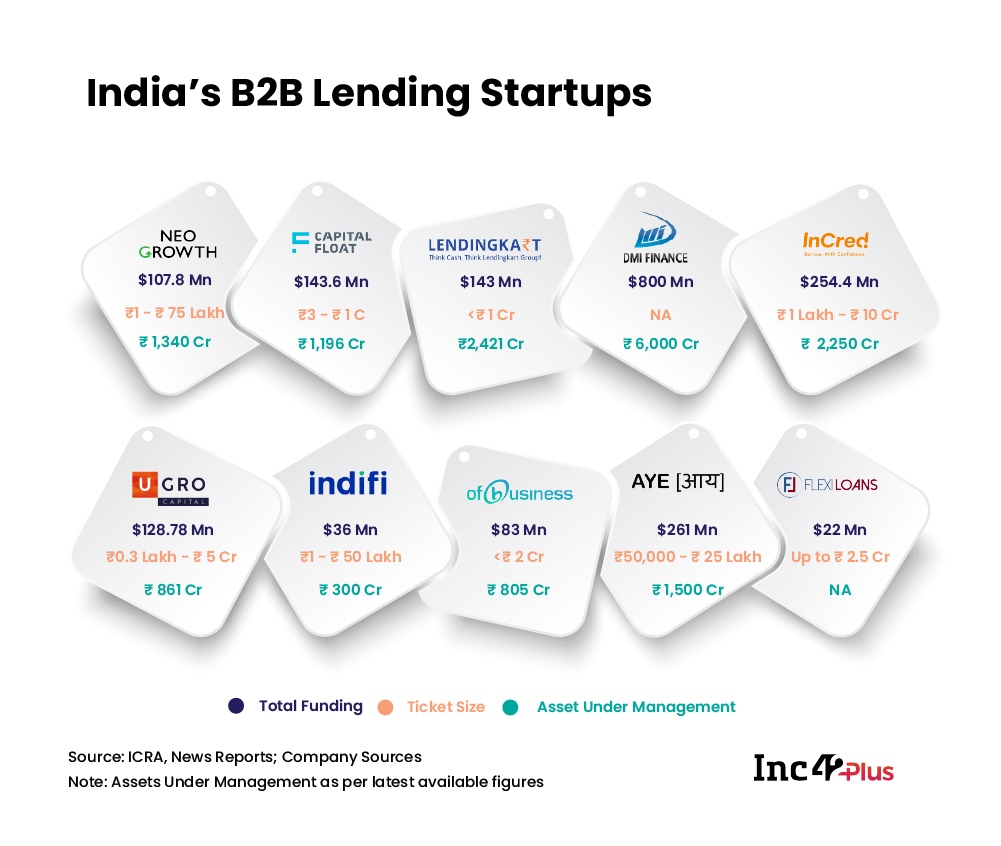

Ahmedabad-based Lendingkart is one of the several digital lending startups looking to improve the MSME credit inclusion. It has not been an easy road for Lendingkart, which has existed since 1996, or indeed any of the newer SMB-focussed lenders. Mithun Sundar, CEO of Lendingkart Finance, which has an NBFC license, explained that the key challenge is evaluating the potential loanee.

In personal loans, lenders only need to look at the credit score and the income which is very easy to process. Even in the case of the loans against property, the lender just needs to underwrite the value of the property. There’s no ambiguity or doubt in this case.

When lending to a business, the lender needs to evaluate business fundamentals that require accurate and up-to-date information — some MSMEs might not even have formal ledgers. There are issues if someone lends to a micro-entrepreneur sitting far away somewhere in Guwahati. The lender needs to evaluate all their transactions for a certain period of time to understand the health of their business.

Now, before that, the MSME will need to share their bank statements and there are certain levels of friction in doing so. Even today, it’s not a simple one-click track where you’re able to share all of the banking details of your company in one form, or all the GST and all of your IT returns and so on. That requires some work before it is shareable, said Sundar.

Nevertheless, the B2B opportunity is hard to ignore. The challenges in vetting businesses have not deterred formerly consumer-focussed lenders to look at small business loans. Uday Somayajula, CEO of ePayLater, which has shifted its focus from B2C to B2B lending, believes the low penetration has attracted players in the last 18 months.

“In the case of B2B lending, the penetration of formal credit has always been abysmally low,” he said. He further added that the low technology adoption and lack of structured data are the major hurdles.

The lack of adequate structured data often correlates to the low tech adoption among small businesses — many might not have formal books or sales trackers and practice unwritten processes. With Udyog Aadhaar, rise in online GST filings and IT returns, some of the data problems are being solved, but tech adoption has largely been a policy-driven strategy in small businesses. The other thing that has pushed SMBs to digitise their operations and adopt tech is, of course, the pandemic.

While there are undoubtedly hurdles in the growth path for SMB lending, things are changing. On the face of it, digital payments and lending might seem like two disparate segments within fintech, but for SMB lending, digital payments has acted as a data hoover. With rising digital point-of-sale machine adoption among MSMEs, the availability of SMB data has increased to an extent.

The adoption has not been very encouraging overall, lenders told us that the MSMEs are still hesitant about this due to the 2% rental fee for such PoS machines. Plus, the RBI has strictly made it clear that this fee must not be passed on to the end consumers.

In such cases where businesses show lethargy in digitising payments and streamlining data, the alternative data sources are being used to mitigate lending risk, but with the pandemic, such alternative data sources may have to be reviewed by lenders as risk models get rewritten.

The lending platforms are nowadays also evaluating social media data, data from smartphones, and websites besides a business’s Udyog Aadhaar ID — much like in the case of consumer lending. But what kind of businesses are being tapped in this phase when everything seems to have changed?

The B2B Lender Focus Areas

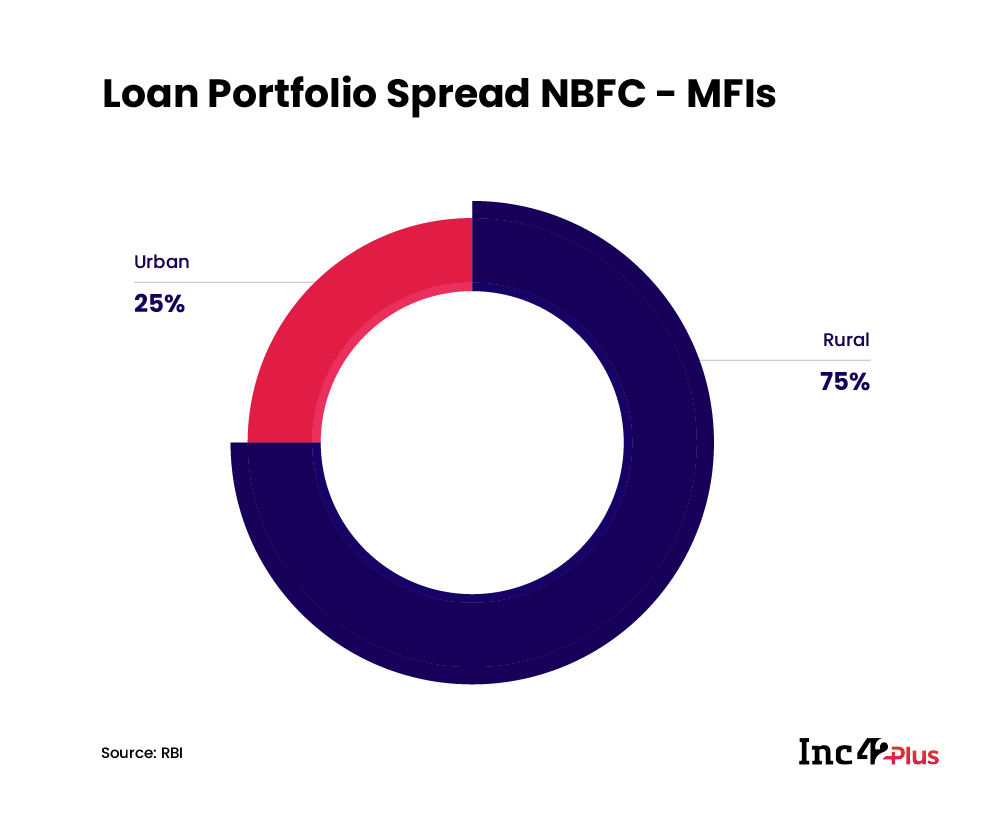

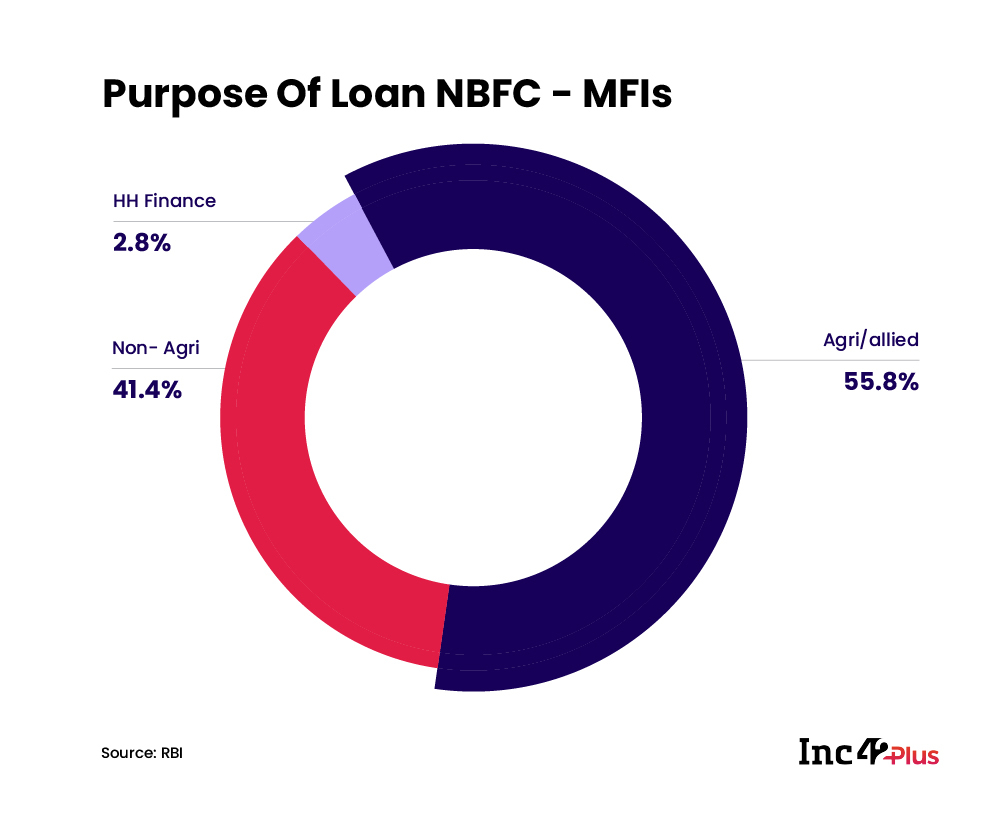

According to the RBI September report, the loan portfolio of NBFC-MFIs is concentrated in rural areas. A majority of NBFC-MFI loans thus are given for agriculture and allied activities, followed by non-agriculture activities (trade, service, manufacturing and production etc.) at 41.4% and household finance (education, medical, others) at 2.8%. This has also been the reason that numerous NBFCs and lending startups extending credits in rural areas and the agricultural sector are finding it difficult to go digital in comparison to the lending tech startups focussing on urban areas.

As we have seen through our coverage on the economic impact of Covid-19, certain sectors such as supply chain, food delivery, travel, mobility, ecommerce marketplaces among others saw an adverse downturn, whereas edtech, fintech (digital payments, insurance) and healthtech saw an adoption boom.

Moving with the market, lending platforms trained their eyes on MSMEs and small businesses that are working in these sectors. In the manufacturing sector, health and pharma-related manufacturing saw a major upswing with many companies pivoting to making PPEs, face-masks, sanitisation products, and more. And in the past few months, with hospitality, some amount of tourism and travel opening up, these sectors are coming back into focus, while edtech, FMCG and healthtech continue to grow even after the countrywide lockdown period.

According to Abhijit Ghosh, CEO of UGRO Capital, since NBFCs and lending platforms deal with the riskier and informal businesses that banks hesitate to lend, it is essential to first understand the dynamics of space. UGRO focuses on small businesses in eight key sectors including healthcare, education, chemicals and food processing, which have grown in the past few months, as well as hospitality, which is now bouncing back.

“The better one understands the space, the quality of data collection gets better and hence it would be easier to offer customised offers,” Ghosh said. He also highlighted that it is essential to have a clear focus on the sectors that are working because that’s where the data will come from.

The Dream Of Full-Stack B2B Digital Lending

In our conversations with B2B digital lending startups, the consensus was that this segment has grown by a significant margin over the last few months, despite the challenges in the past. With India Stack making financial data easier to verify and with the growing awareness for digital consumer loans, even SMBs are being exposed to more digital touchpoints, and one of the ways that B2B lenders are tapping small businesses is by approaching the market from a B2C perspective.

This means having completely tech-driven processes and automation to make SMB lending just as simple as B2C loans. Saurabh Jalaria, cofounder of InCred believes that many companies are looking at full-stack digital lending for SMBs now, rather than a mixed-mode approach. In the case of InCred, which offers both consumer and business loans, Jalaria said up to 90% of operations are digital stack with the rest going online soon.

This includes replacing physical forms and signatures with e-signatures, in-person KYC being retired for video KYCs and using every possible digital connection to verify businesses.

“In pre-Covid times, a credit manager would visit the customer’s premises to verify the credentials. This too has been made digital by adding two new features into our app,” Jalaria told Inc42.

Anuj Kacker, cofounder of MoneyTap, which is primarily focussed on consumer loans, however, feels that while platforms and NBFCs are seemingly ready to serve digitally, the MSMEs, particularly the ones that were impacted the most by the pandemic, still face a huge challenge in going digital. Some of them are not ready to invest money in digital means having already suffered losses.

Will Post-Pandemic Demand Lift SMB Lending?

Making matters tougher for businesses the threshold for getting loans is actually getting higher for B2B loans — even if the process may have become simpler and faster. That’s because the rising NPAs over the past two fiscals have alarmed many NBFCs that lend directly, and even digital lenders, who work with NBFCs and banks.

Despite the RBI indicating a $331 Bn gap in demand and supply, the suppliers i.e. lending platforms and NBFCs have only toughened their criteria in post-pandemic situations citing estimations of increased default rate.

Lending partners (NBFCs, banks) are getting more stringent too, believes Pallavi Srivatsava, cofounder of ProgCap, which does real-time scoring and sources MSME clients for lenders. Lending partners are exercising more caution in terms of how and who they will lend to even though the Indian government’s MSME stimulus package has relaxed some of the criteria. There is a definite need to revisit these criteria in the face of an unprecedented economic downturn for the Indian market.

As a result of lending partners tightening the eligibility criteria, digital lenders have also had to target low-ticket size loans and sachet credit products. These may be good enough for a few businesses for a short period of time, but it is definitely not going to make a large dent in the credit gap.

How long can lenders continue to rely on the same sectors that have seen growth in the past few months? Lending startups have already started figuring out the other sectors that are now slowing opening up. While travel and tourism is still lost cause for many particularly in the case of India, lending platforms and NBFCs are opening up for Kirana stores, supply chain management, agritech particularly after the government’s enactment of three farm bills. A parallel challenge for the NBFCs/MFIs has been to make its consumers digital-ready while applying for loans.

The next big push is expected in the form of account aggregators — the final piece in the India Stack puzzle — which would help lenders reduce the cost and time associated with small business and MSME loans, but more importantly make an informed data-led decision and not just rely on legacy metrics.

However, the account aggregator has its own implementation issues, something that we would see in the upcoming article.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.