In essence, Mamaearth today is a new-age D2C brand, retail FMCG player, as well as a services company

Mamaearth’s approach has been dictated by the age-old mantra for selling products: sell closer to your customer

BBlunt as a channel for Honasa and Mamaearth’s products can be a competitive edge for the company

When Mamaearth![]()

![]() or Honasa Consumer’s IPO first came to the market in late 2022 and early 2023, we wondered whether the company could shake off its identity crisis. As we said at the time, the company’s key strength is its retail or offline sales network, even though Mamaearth disrupted the space in its early years as an online-first direct-to-consumer brand.

or Honasa Consumer’s IPO first came to the market in late 2022 and early 2023, we wondered whether the company could shake off its identity crisis. As we said at the time, the company’s key strength is its retail or offline sales network, even though Mamaearth disrupted the space in its early years as an online-first direct-to-consumer brand.

Of course, as companies and brands mature, they have to adapt to the tune of the market. Mamaearth’s latest avatar has been dictated by the age-old mantra for selling products: sell closer to your customer.

Mamaearth began as an aspirational brand, but it had to transition to a model that more or less resembled traditional FMCG players because it realised the real strength of these brands is in their retail presence and distribution prowess.

Along the way, the company raised funds to acquire several players, and now, beyond the retail channel, it has the salon chain BBlunt as an intermediary channel to reach customers. So, in essence, Mamaearth today is a new-age D2C brand, retail FMCG player, as well as a services company.

So the biggest question for many investors ahead of the company’s IPO today is which Mamaearth should they bet on, if at all?

But before we go ahead, we must mention, we are not focussing on the company’s valuation, which many claim to be rich, or indeed its revenue growth. Instead we wanted to examine what expectations investors and other observers can have from the company, given that services, products and new-age companies are respectively evaluated very differently.

What Even Is A D2C Brand?

In the past two years, the line between ecommerce and retail has blurred repeatedly in different ways. Many D2C brands, particularly in the beauty and personal care category, took the omnichannel route to reach retail consumers, but they also realised that the most habitual online shoppers had changed their shopping behaviour.

Particularly, in the metros, where quick commerce apps became the go-to destination for the most active online shoppers. Dark stores and apps such as Zepto, Blinkit or Swiggy Instamart are fast replacing marketplaces from a FMCG consumption point of view, at least in dense urban areas.

Today, the presence on marketplaces such as Nykaa, Tira, Myntra, Flipkart, Amazon India or Meesho is necessitated by the fact that brands are building a second layer of customers. That’s the online shopper from Tier 2 and 3 and beyond, being targeted by the likes of Mamaearth and Honasa’s other brands, The Derma Co., Aqualogica, Ayuga, BBlunt and Dr. Sheth’s.

Lastly, the less tech-savvy retail consumer is still buying from traditional stores and prefers the high-touch experience. So Mamaearth has to cater to these, also build up marketplace presence and work with quick commerce distribution and procurement teams.

Besides, it has to build native channels like its app or website for the fraction of shoppers who become repeat and loyal users. Therefore, they can be pulled into the more profitable native channels.

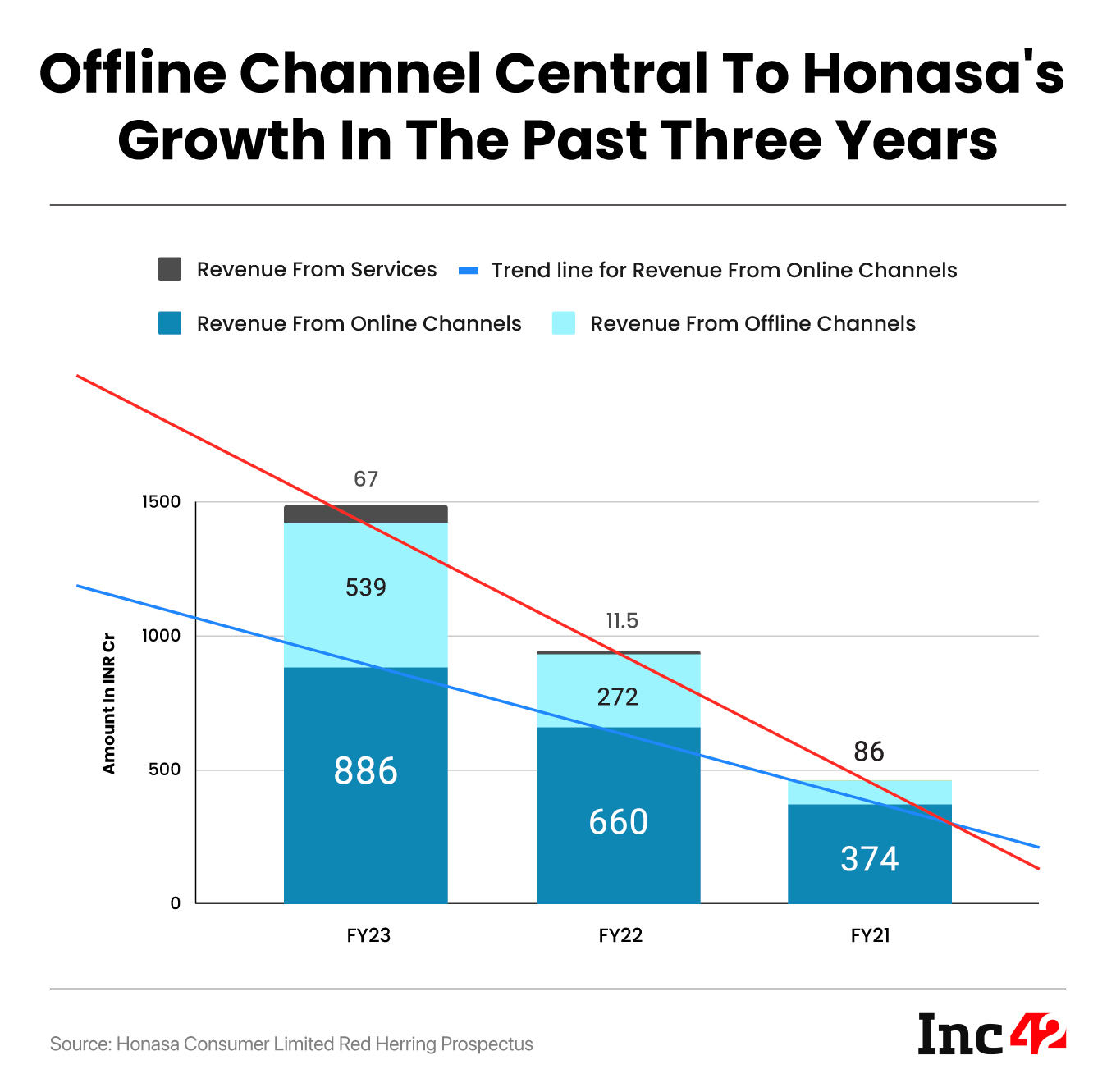

And that’s not the story for Mamaearth alone. It’s the trajectory that D2C brands, particularly in BPC and F&B, have to follow today. Profitability, in the long run, depends on a healthy mix of these channels that offer varying margins. In FY23, Honasa earned 59% of its revenue from online sales, whereas 36% came from offline channels. However, the share of offline channels doubled from 18% in FY21.

So firstly, looking at Mamaearth as a technology-first D2C brand would be folly. Yes, it has the branding nuance and digital marketing nous of a D2C brand, but the core of the business as we have seen in our analysis recently is a retail brand.

BBlunt: Honasa’s Trump Card?

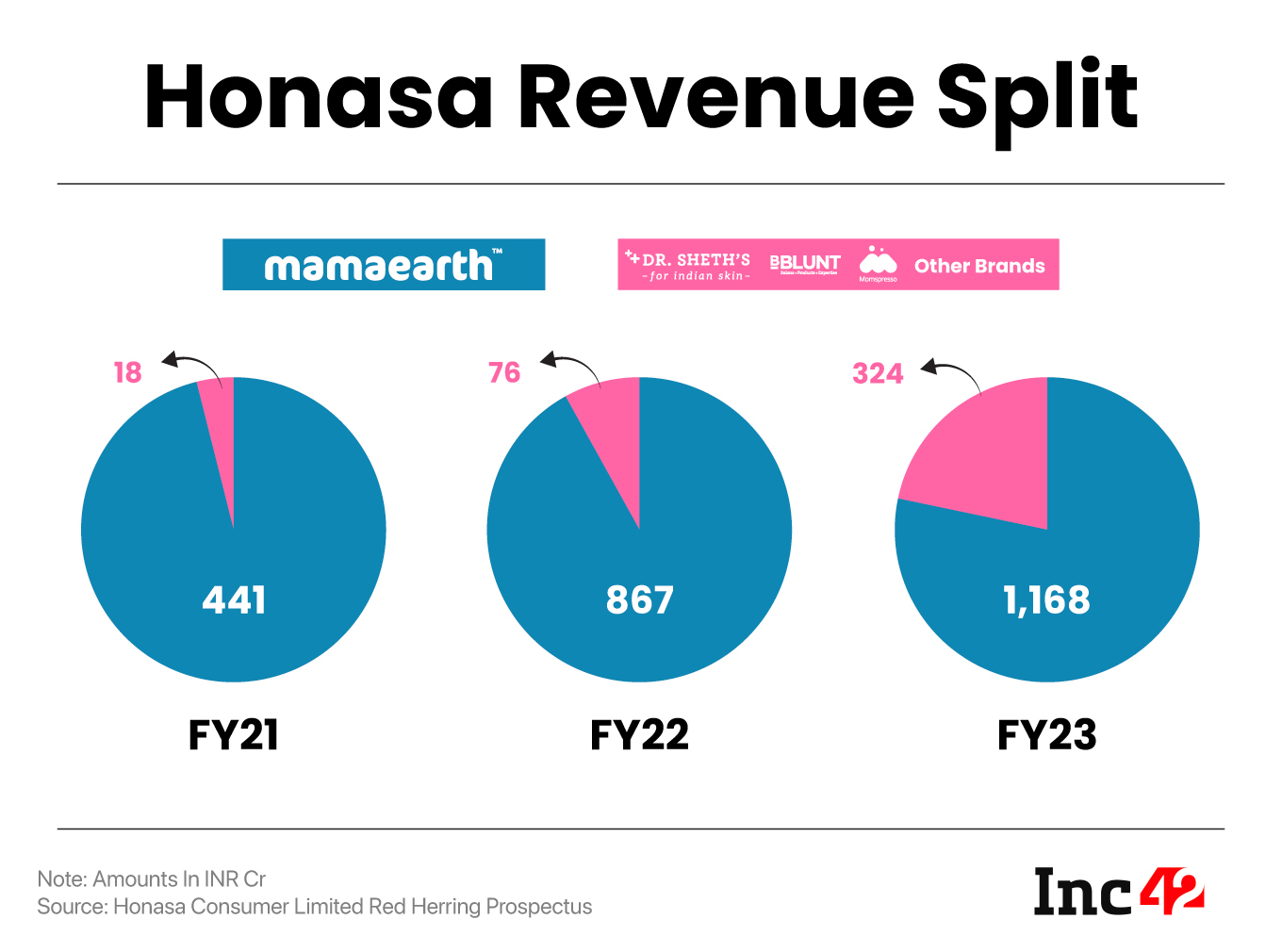

Of course, what sets Honasa’s product and brand umbrella apart is BBlunt, which is the company’s services arm in the beauty and wellness space. BBlunt is not just an independent salon chain, but a channel for Honasa and Mamaearth’s products.

One can see The Derma Co. (skincare), Aqualogica (hydrotherapy), Ayuga (ayurvedic products) being consumed at the salon end, while this will help reinforce the brand’s presence in retail shelves and online channels.

Founded in 2004, the BBlunt salon chain already has very strong brand recall and enjoys the goodwill that comes from being in the market for nearly two decades. One can see Mamaearth leveraging BBlunt to enable the efficiency that the house-of-brands model requires.

Indeed, ‘house of brands’ as a concept has failed to take off because platforms are unable to make the most of the margin efficiency offered by the omnichannel GTM across their portfolio. Only one or two brands have the appeal to bring customers into brand-owned retail stores.

In Honasa’s case, Mamaearth enjoys a lopsided advantage in terms of brand recall, whereas the other brands in its portfolio are not immediately associated with the company. The non-Mamaearth brands would gain from the wider spotlight under BBlunt to gradually gain some equity.

However, the big challenge here would be the expansion of BBlunt’s salon network from the current 10 salons. BBlunt has zero presence in North India, for instance, according to the company, so this channel only becomes meaningful if the company spends a significant amount of its IPO proceeds to expand BBlunt. The filings indicate an allocation of INR 26 Cr from the IPO proceeds to expand BBlunt. Will this be enough?

Honasa is bypassing several complexities in the house-of-brands model through BBlunt, but the latter being a retail services business has different headwinds. “This channel is expected to provide us with a ready base of consumers to generate trials and will provide the ability to acquire new consumers, not only for BBlunt but also for other brands in our portfolio,” the company said in its RHP.

And looking at it from a competitive standpoint, it is a big strength that is unmatched by many of its direct rivals. Having said that, BBlunt itself has competition from franchise or brand-owned chains such as Jawed Habib, Gitanjali, Lakme Salon, Looks, Naturals and a host of other international brands such as Jean-Claude Biguine and Toni & Guy, among others.

To maximise revenue under its various channels, Honasa would need a steady stream of new SKUs and the right SKUs for the right channels. As outlined in the company’s pre-IPO filing, the contribution of new SKUs to overall revenue growth in FY23 was 56.58% higher than FY22.

Adding new SKUs across price points is one way to win the game, as seen in the case of FMCG majors such as Unilever which has 15 unique brands in BPC alone.

What Mamaearth IPO Means For D2C Brands

Speaking of rivals, their attention will be on Honasa and Mamaearth for altogether different reasons. As some analysts told us this past week, this is a litmus test for the D2C segment and the Indian ecommerce ecosystem as a whole.

Yes, Mamaearth and Honasa have to invest more to bolster their in-house manufacturing operations, but short-term profitability hinges on efficient distribution and supply chains.

Even though many of the private equity and venture capital investors that backed D2C brands were bullish on the ecommerce aspect, pretty much all food & beverage, beauty and lifestyle brands now acknowledge that omnichannel is key and retail is king.

So while Mamaearth might not be a puritan’s D2C brand that only uses native channels, the success or failure of its listing and the subsequent movement of the stock with investor sentiment will inform a lot of its competition about how to tailor their operations.

The likes of SUGAR, WOW Skin Science, Purplle, The Ayurveda Co., Pureplay Skin Sciences and others are some of the brands that are waiting in the wings to not just go to the public markets like Honasa, but also see whether the company’s bet on a hybrid services-plus-products model will fulfil its potential.