As per Inc42 data for unicorns, 10 startups are in danger of being locked out of the unicorn club due to the current dollar-rupee exchange rate

One reason why the valuations are influenced by exchange rate fluctuations is that private startups typically refer to their paper valuations and not the actual current value

Experts believe that a weakening rupee will change the valuations of some startups if they raise funds now, including those that have operations abroad funded by Indian entities

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

In early July this year, as the rupee’s exchange value slid to INR 79 per dollar, there were serious worries about how it might change startup valuations. Now, a couple of months later, with the rupee at over INR 81.5 in comparison to a dollar, the impact is deeper and some borderline unicorns in India are on the verge of being priced out of the unicorn club.

To be clear, the valuation impact from the rupee’s slide will only be seen on unicorns whose valuations have not changed between last October and this year. And in dollar terms, it will only lower the valuation of those Indian unicorns that were valued between $1 Bn and $1.2 Bn in Indian rupees in the past year.

A startup in India with rupee revenues, which does not have a foreign entity and adheres to Indian accounting standards, might raise funds in dollars, but the cash infusion is always in rupees. This is best highlighted by the PAS filings by startups to denote the infusion of cash into their accounts after an equity transfer.

The maths is rather simple: If such a business was valued at INR 7,500 Cr in 2021 and became a unicorn, its dollar valuation would change in October 2022 given the current dollar-rupee exchange rate. At INR 81.57 per dollar, the startup’s valuation of INR 7,500 Cr comes up to $920 Mn in October this year, well short of the $1 Bn mark.

Any startup that wants to claim the unicorn status now has to show a valuation of roughly INR 8,150 Cr as opposed to roughly INR 7,300 Cr in January this year. That’s a huge 10%+ fluctuation.

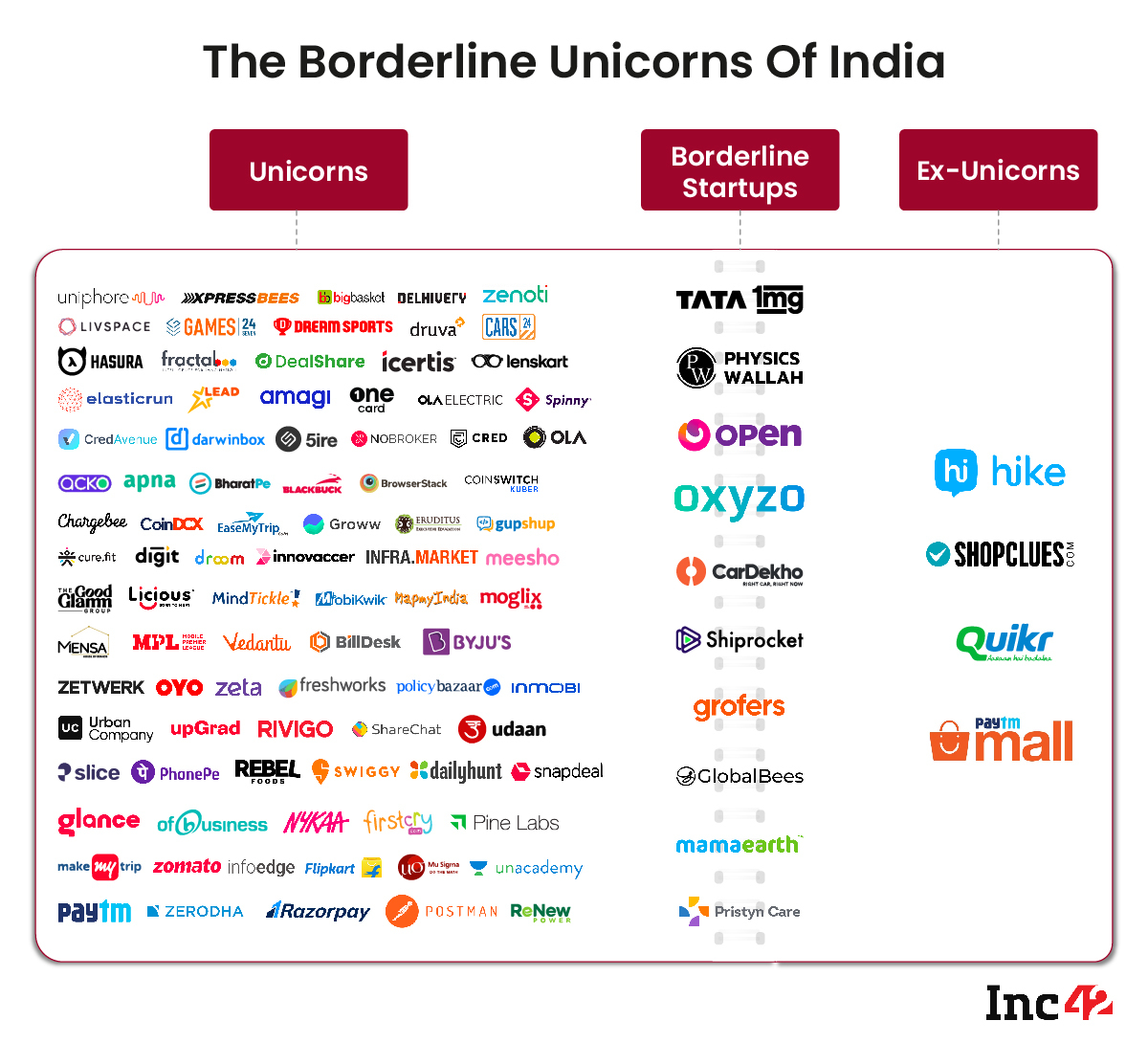

As per Inc42 data for unicorns, at least 9 startups are in danger of being locked out of the unicorn club due to the current dollar-rupee exchange rate. These include Grofers, PhysicsWallah (PW), Oxyzo, Mamaearth, Tata 1mg, Globalbees, CarDekho, Pristyn Care, Shiprocket at the very least.

Besides this, Rivigo, which turned unicorn in 2018, could also be on the verge of exiting the club. However, the company is raising a pre-IPO round, which is likely to come at a higher valuation. It has already raised $2 Mn in this round, as per a VCCircle report.

Fickle Paper Valuations For India’s Unicorns

One reason why the valuations are influenced by exchange rate fluctuations is that private startups typically refer to their paper valuations and not the actual enterprise value based on its assets and revenue.

While there are several ways in which a startup’s valuation is arrived at, the most prominent one is discounted cash flow (DCF) analysis. This involves forecasting future cash flow of a startup and an expected rate of investment return is used to calculate the current worth of that future cash flow.

In contrast, the market cap of publicly-listed companies is a more solid measure, which does not entail projections. The market cap is a factor of its share price and the number of outstanding shares. Any retail or institutional investor can easily calculate the market cap of a publicly-traded company in this manner, but the same cannot be said for startups.

Haircuts And Down Rounds

Indeed, in the course of our reporting on fundraises and valuations, our calculations and estimates rely on a certain degree of assumption based on revenue and cash flow projections. That’s because the share price offered to investors changes with each round as new investors come on board and even existing investors routinely invest at a higher price in later rounds.

This is highlighted by how hospitality unicorn OYO saw its valuation slashed by Japanese VC giant SoftBank. SoftBank is reported to have slashed the valuation of its stake in OYO by as much as 20% to $2.7 Bn at the end of June quarter, from the earlier $3.4 Bn. Some other OYO investors may follow suit, according to a report in The Ken earlier this week, and OYO’s $9.6 Bn valuation is likely to plummet in the next few weeks.

Of course, a similar valuation drop was seen in the case of Quikr, which exited the Indian unicorn club after a markdown in February 2020 by one of its key investors, Sweden-based Kinnevik. Quikr was hit by allegations of fraud by employees, which resulted in Kinnevik’s haircut.

In 2022, edtech giant BYJU’S will find it hard to raise funds at its current $22 Bn valuation and is said to be in talks with investors for several months to raise capital.

“No amount of selling and marketing justifies this valuation. The investors in BYJU’S, even the likes of General Atlantic, Sequoia, etc., must be a worried lot,” an analyst had told Inc42 soon after BYJU’S reported massive INR 4,588 Cr losses in FY21.

Even ecommerce unicorn Meesho is facing a downround and is likely to see a 25% haircut on its current $4.9 Bn valuation, according to a report by The Morning Context last month.

Down rounds are not new in the context of startups — particularly after a boom. This was seen in the case of Indian unicorns Ola’s $260 Mn round in 2017 and Flipkart’s fundraise in 2016, after both companies had raised significant rounds.

Earlier this week, investment platform We Founder Circle’s cofounder Gaurav Singhvi told us that international investors stand to gain because now they would need to invest fewer dollars in the startups they have been negotiating for.

“When the rupee depreciates, the return-on-investment increases by a few more dollars. For example, if they were getting a return of INR 78 on a dollar, with the rupee depreciation, they are getting an approximate increase of 3%-4%,” Singhvi said.

Similarly, experts believe that a weakening rupee will change the valuations of some startups if they raise funds now, including those that have operations abroad funded by Indian entities, particularly D2C brands who may not necessarily have an overseas entity.

With investors having much of the leverage, valuations will suffer if the revenue expenditure of startups and brands is skewed towards international markets.

Our Take: Time To Redefine Unicorns?

It’s not just startups with inflated valuations that are likely to see valuation pressures.

Even startups, whose valuation is a reasonable multiple of revenue — surprisingly, not the case with most unicorns — will now have to show a significantly higher revenue growth rate to meet the multiples at which investors had poured in the capital, according to a Bengaluru-based valuation expert who did not wish to be named.

The valuation pressure will be more keenly felt by founders that are in the market to raise funds but do not have the leverage in terms of equity holding. Those who have diluted a lot of their stake will have no bargaining chips left and therefore have to settle for the investor’s ask.

In such a situation and given the fickle nature of private valuations, one must question whether it is time to revisit the question of what makes a unicorn.

Firstly, if the $1Bn valuation is the barometer, and if USD keeps climbing in relation to INR, several more startups might lose their unicorn status in India. Is it time that Indian startups start relying on their rupee valuations to claim unicorn status?

We would not be debating about dollars or rupees, if valuations of the unicorns in India were about actual revenue multiples and profitability.

When the term unicorn was coined in 2013 by venture capitalist Aileen Lee, she used it to describe a rare startup that had reached a valuation of $1 Bn. In an article in TechCrunch at the time, Lee asked, “How likely is it for a startup to achieve a billion-dollar valuation?”

The question seems almost cute now, with unicorns becoming so mainstream and numerous in India that the term itself has lost much of its essence. Given the VC frenzy in 2021, unicorns have became more ubiquitous than rare in India.

The game of VCs driving up valuations is becoming rather apparent and obvious — what’s really rare is a profitable startup and not one with a $1 Bn valuation. And perhaps, it’s time to focus on revenue and profitability as a real barometer for unicorns rather than propped-up valuations.

Correction Note | October 6, 2022; 6 AM

An earlier version of this article considered Spinny’s valuation to be $1 Bn instead of $1.75 Bn and hence it was included among unicorns whose valuations might drop below $1 Bn. We have rectified the error.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.