Fintech

Fintech Travel Tech

Travel Tech Electric Vehicle

Electric Vehicle Health Tech

Health Tech Edtech

Edtech IT

IT Logistics

Logistics Retail

Retail Ecommerce

Ecommerce Startup Ecosystem

Startup Ecosystem Enterprise Tech

Enterprise Tech Clean Tech

Clean Tech Consumer Internet

Consumer Internet Agritech

Agritech

Robo advisory is still a nascent business in India, with only a handful of startups operating in the space

There are three types of robo advisories in the country — fund-based, equity-based and comprehensive wealth advisories

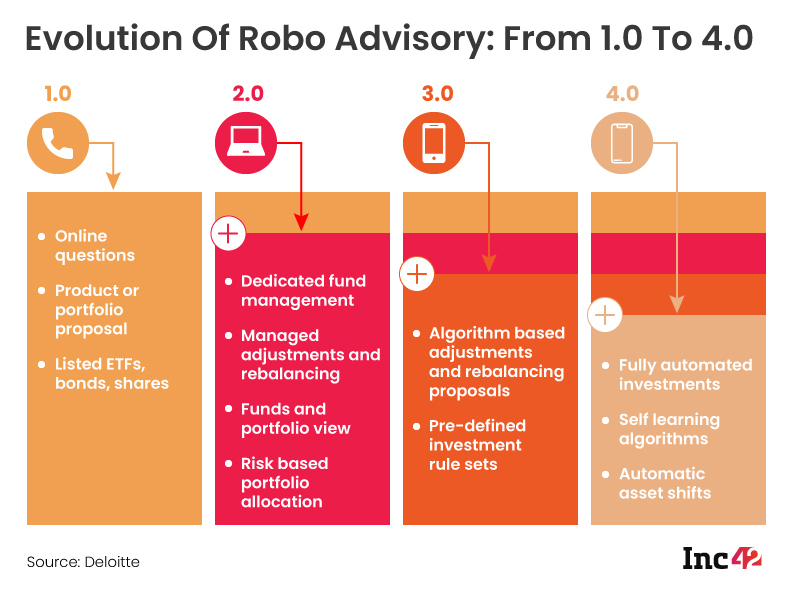

India is on its way to enter the robo advisory 4.0 phase with fully automated investment platforms

Retail investors, especially those who are young and uninitiated, often seek the services of financial advisors or traditional financial institutions to get started but rarely see the desired outcome. For one, very few players in this space do a thorough and need-based analysis and provide customised solutions based on the output. On the other hand, top-grade financial advice comes at a premium but very few small investors can afford it. In such cases, one opts for robo advisors, which help people navigate the complex world of financial investments efficiently and at low cost.

Robo advisors are automated investment platforms that provide algorithm-based solutions after analysing a user’s financial position (existing assets and cash flow), goals, aspirations, time horizons, risk appetite and capital market expectations. Robo advisory services were first introduced in 2008 in the US, and they soon became popular due to minimum investment, low cost and operational ease. In India, robo advice has evolved in the past few years, thanks to the rising financial awareness across the board. According to research by MEDICI, a fintech research firm, the number of robo advisors in the country rose from three in 2013 to 16 companies by the end of 2019.

Assets under management (AUM) in the Indian robo advisory segment is expected to reach $53.9 Bn by 2025, with a 43.8% CAGR during 2020-2025, according to Statista.

Robo advisors are gaining traction over their human counterparts/traditional players for several reasons. Apart from the tech-enabled operational efficiency (more on that later), the fees charged by robo advisors are much lower than other financial advisors. Before these automated investment platforms came into play, investors never imagined that the cost of financial planning and investment could be less than 1% of the AUM. But robo advisors have made it possible.

Another key factor is the minimum balance feature. It is a boon for investors with a minimum net worth as they can now access and afford capital market investments via robo advisory services. Better still, robo advisors are developed in a way to minimise capital gains taxation, and this benefits investors in terms of tax optimisation.

Finally, a number of macro factors such as growing per capita income, growing number of millennials with more disposable incomes, a major shift in investment behaviour due to economic uncertainties and the increasing smartphone and internet penetration have paved the way for the growth of robo advisory in India.

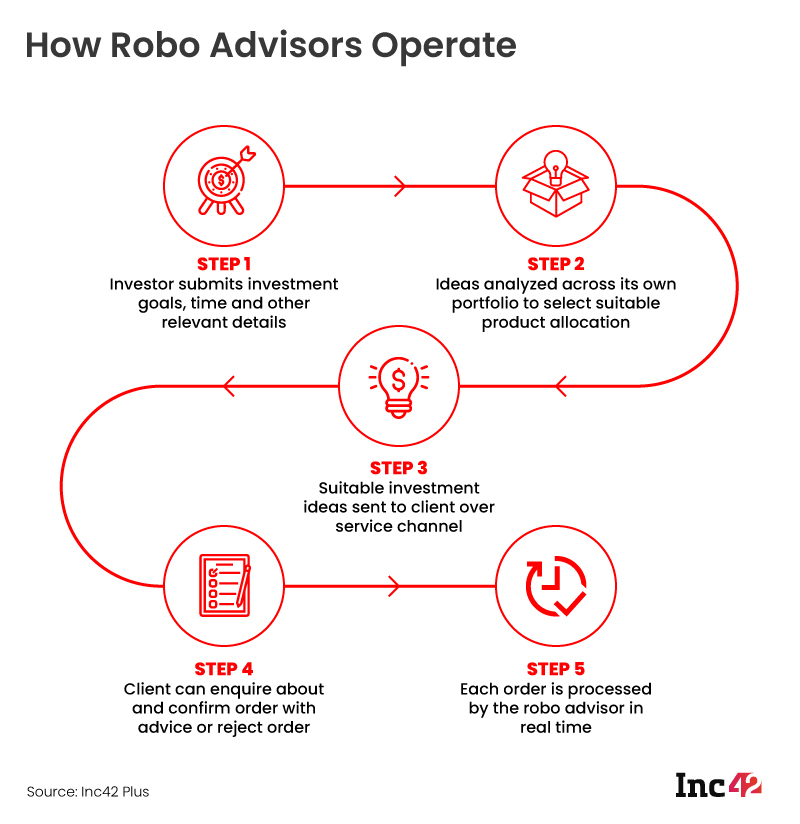

How Robo Advisors Work

The essential function of a robo advisor is to advise people on their investments and help develop their investment strategies. On a robo advisory platform, users must fill in all necessary details, specify the financial goals they want to achieve and indicate their risk tolerance. When all relevant information (time frames, risk appetite, goals, nature of employment, age and other financial details) is fed to the system, the software analyses these parameters to create a score for every individual, builds a matching portfolio based on that score and manages it on its own.

Robo advisors typically use investment algorithms based on artificial intelligence and machine learning to augment the services of a traditional financial advisor.

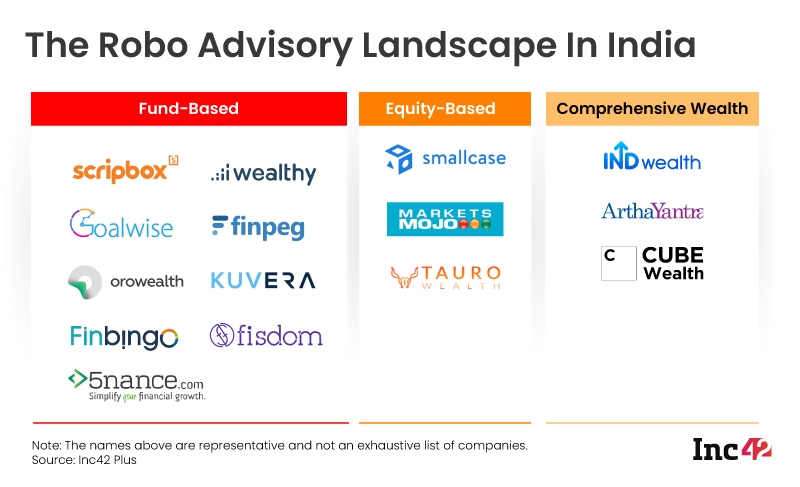

Types Of Robo Advisors

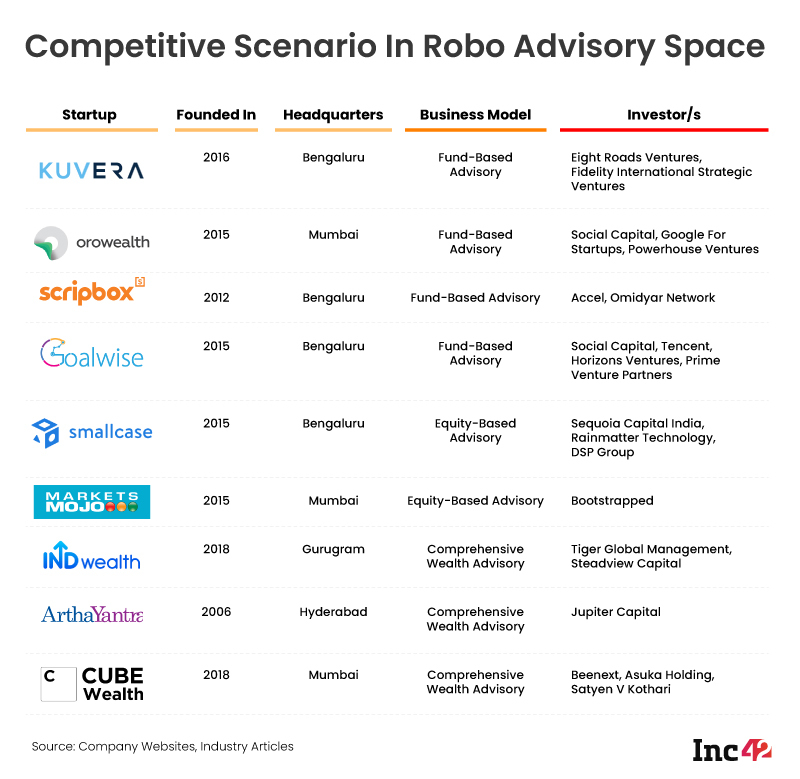

- Fund-Based Robo Advisory: Fund-based robo advisors offer risk profiling and goal-based suggestions to customers. Investments are made in single asset class funds, which are either managed or exchange-traded. These are suitable for both new and seasoned investors, who are relatively risk-averse and do not wish to have direct exposure to equity but need guidance on the most optimal investment mix. These robo advisories mainly generate their revenues through fund distribution commissions — fees received from fund houses or asset management companies (AMCs).

- Equity-Based Robo Advisory: These robo advisors focus purely on equity portfolios. These are suitable for investors with a fair understanding of equity markets, moderate-to-aggressive risk profiles but a preference for experts’ guidance to design the most optimal portfolios. Some of these advisors offer thematic portfolios, which are designed around specific sectors or investment philosophies. Pricing is usually fixed, either as an annual fee or a transaction fee per investment.

- Comprehensive Wealth Advisory: They focus on aggregating customers’ financial net worth and understanding their risk appetite and then offer comprehensive wealth management services. This can be done for an individual investor or an entire household. Besides fund-based portfolio recommendations, they also offer financial planning, portfolio management services and financial advice for wealth and estate planning. Pricing is usually fee-based for a package of combined services. They also get commissions from fund houses if investors make their investments via those platforms and waive the service fee and offer free advice in such cases.

Key Startups In The Indian Robo Advisory Space

India is still a nascent market for robo advisory services. So, the value of assets under advisement (AUA) are low compared to developed markets like the US. Here are some major Indian players, their business models and their investors:

Future Of Robo Advisors In India

Robo advisory in India is currently at the 3.0 phase and is expected to move towards phase 4.0, similar to developed markets like the US, the UK and others countries using advanced technology.

The emergence of fully automated robo advisors will further reduce existing costs and rationalise the fee structure in this segment based on three saving potentials — personnel costs, operating expenses and capital expenditure due to complete digitalisation of financial advisory services.

Based on current trends, experts believe that the country will soon witness the emergence of a hybrid robo advisory model that will combine the best of digital and traditional services. In essence, these will be AI- and ML-powered robo advisories with options for interactions with human advisors.

Besides, the market has already seen M&A activities in this space. Last year, Bengaluru-based Niyo Solutions, a digital banking startup, acquired mutual fund investment platform Goalwise and rebranded it as Niyo Wealth to expand its product offerings. Existing and upcoming fintech players planning to foray into the financial advisory and wealth management space may also buy out key robo advisories to expand their respective businesses and user base. Overall robo advisories may see an exciting future in terms of growth and technology enhancement for a long time.