On Monday, February 21, 2022, Paytm's stock hit its all-time low of INR 801

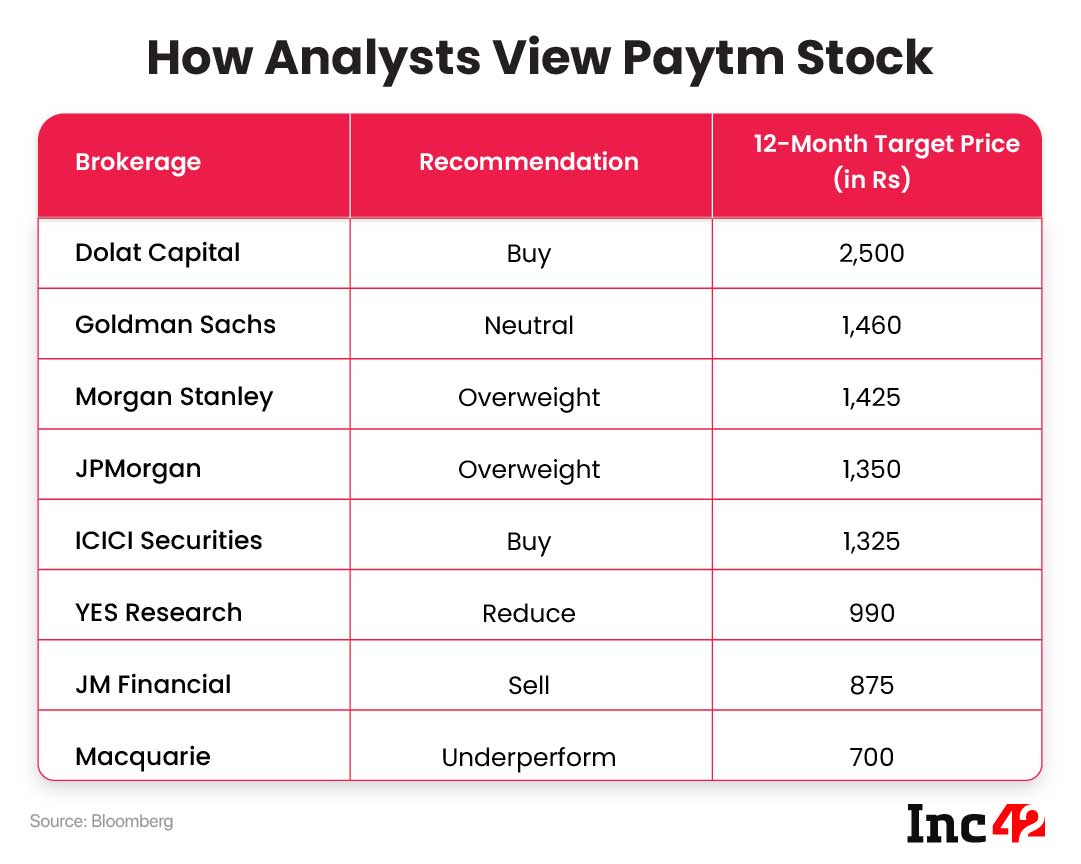

ICICI Securities has set a target price of Rs 1,352 apiece for Paytm, a 66% upside from its current price

Goldman Sachs also revised its rating for Paytm and went to a buy from neutral

Even as shares of Paytm parent One97 Communications fell to a record low, Indian equity markets research advisory ICICI Securities revised the stock to a ‘buy’ rating. ICICI was among the major brokerages that have changed their tune on the Paytm stock’s prospects.

The Indian brokerage expects a potential upside of up to 66% for Paytm’s stock based on its current price. The fintech giant’s share price tumbled to INR 807 at the end of trading on Monday, February 21, 2022 and during the course of the day, the company hit its all-time low of INR 801. ICICI Securities has set a target price of Rs 1,352 apiece for Paytm, a 66% upside from its current level.

Stock Market Watchers Bullish On Paytm

ICICI Securities, initiated its coverage on Paytm, last week and claimed that while the business continues to have risks, the firm’s performance and particularly the revenue from merchant payments is encouraging.

ICICI tempered this assessment by clarifying that like many new-age tech companies, Paytm’s model and growth focus calls for a different view on evaluation and assessment of the business. It added that the Vijay Shekhar Sharma-led company will have to make significant investments and burn cash in order to optimise its acquisition funnel. It counted the rapidly evolving business model, a highly competitive fintech market and regulatory uncertainties as risks for Paytm.

ICICI Securities forecasts the company’s intrinsic business value at about INR 94,000 Cr, which comes up to INR 1,352 per share. This is calculated on a lifetime customer value of INR 2,000 from every monthly transacting user and INR 29,600 for transacting merchants.

Last week, Goldman Sachs also revised its rating for Paytm and went to a buy from neutral, after the company’s financial results from the December quarter. GS has set a 12-month target price of INR 1,460, which would represent a gain of more than 80% from the current stock price.

Among the brokerages that adjusted their ratings to accommodate potential upsides in the business, Dolat Capital was the most bullish and maintained a buy rating with a 12-month target of INR 2,500. Dolat Capital’s analysis (DART) said the fintech company offers a unique play given the conducive market conditions for digital payments, ecommerce and financial services in India. It counted the company’s lower customer acquisition cost as a significant advantage over rivals.

On the other hand, brokerage firm Macquarie Research continued to call Paytm an under-performing stock and cut its target price to INR 700 from the earlier INR 900. Macquarie had been bearish on Paytm’s stock ever since its debut on stock exchanges.

UPI Growth Is Still Key For Paytm

According to ICICI’s report, which Inc42 has reviewed, the gross merchandise value (value of transactions processed) is projected to have a CAGR of 36% over FY22-FY26. The cloud business (payments gateway and services) and ecommerce (mini app store and Paytm Mall) offerings are expected to grow at over 30% CAGR till FY26, while the financial services arm’s revenue will grow at 57%, ICICI Securities said.

It added that Paytm’s ability and the regulatory attitude towards UPI monetisation will play a key role in this projected growth as UPI constitutes half of Paytm’s gross merchandise value. This despite the fact that Paytm has diversified its payments platform with the addition of tokenisation for credit cards and the fact that its wallet and payments bank business was boosted by favourable regulatory policies.

Lending Sets High Expectations

Analysts’ expectations were buoyed after Paytm’s Q3 results were encouraging in terms of the topline performance. However, the monetisation challenges in the financial services business as well as unfavourable regulatory outcomes are counted as risks by brokerages covering the fintech giant.

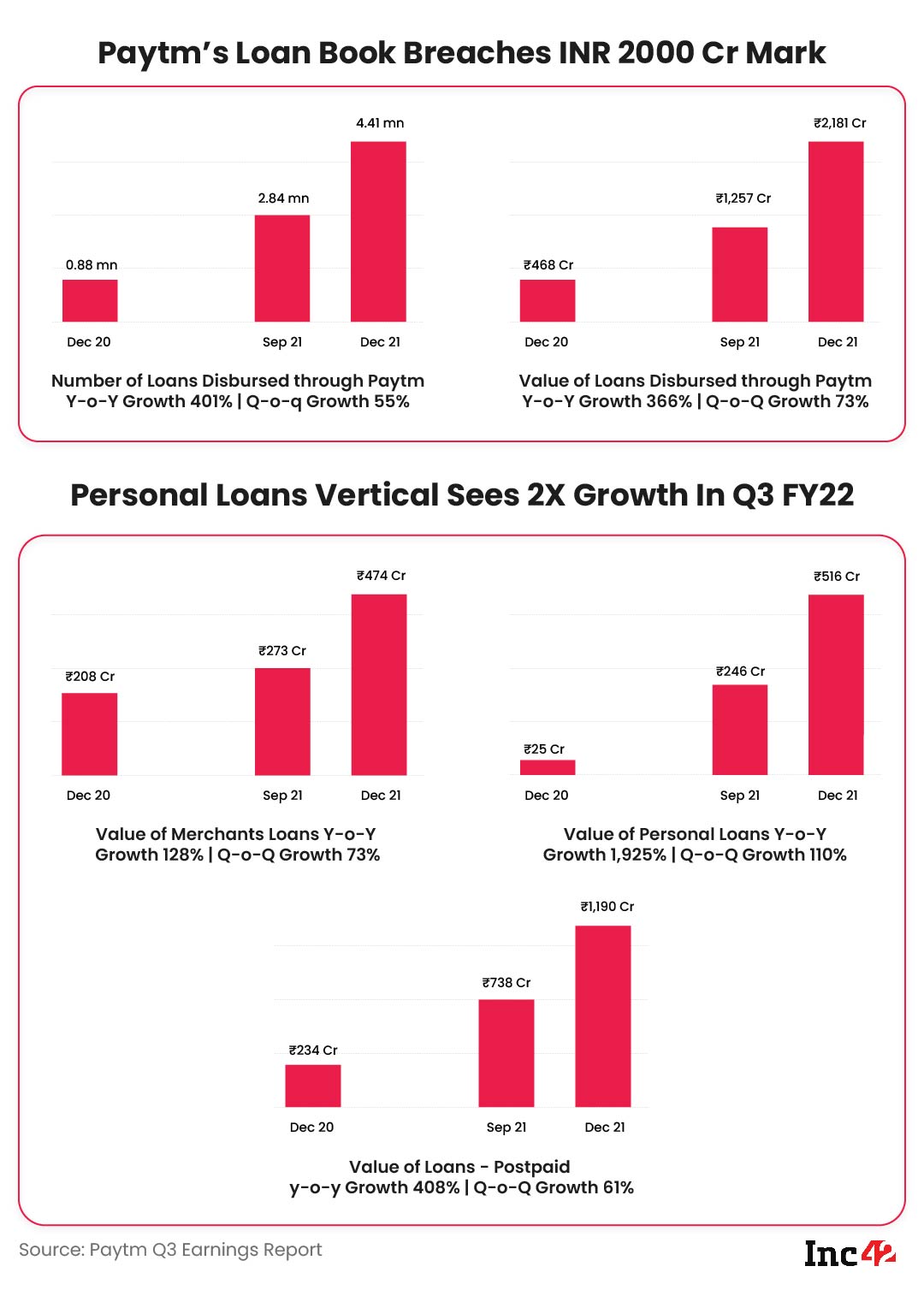

In particular, the lending business was something that encouraged Paytm watchers. Goldman Sachs noted that Paytm can comfortably scale up its lending play since it does not lend from its books or take any credit risk, instead lending through NBFCs.

Paytm posted INR 1,456 Cr in revenue from operations for the quarter ending in December 2021, i.e. Q3 FY22. This is almost 34% higher than the INR 1,086 Cr the company earned in July–September 2021.

Expenses rose by 44.8% on a QoQ basis and the total Q3 expenditure stood at INR 2,317.4 Cr. As a result, loss during Q3 was pegged at INR 778.5 Cr, a 64% increase from INR 473.5 Cr in Q2 FY22. For nine months in FY22, the fintech giant’s loss after tax stood at INR 1,633.9 Cr.

A look at the breakdown of income and operations showed that Paytm’s lending business disbursed 4.4 Mn of loans to the tune of INR 2,181 Cr in Q3. While the BNPL business disbursed loans of INR 1,190 Cr, a 408% YoY rise, the instant personal loan division disbursed INR 516 Cr, a 1,925% rise from the year-ago period. Merchant cash advanced loans worth INR 474 Cr were disbursed by the company in the quarter.

Goldman forecasts $10 Bn in disbursals by FY26 against $900 Mn in FY22 Q3, or over 10X growth for the lending vertical. The scale in payments products results in Paytm having superior lending data quality, according to the brokerage.