Indifi reported a net profit of INR 5.1 Cr in FY23 as compared to a loss of INR 32.8 Cr in FY22, its maiden profit for the full year

Cofounder and CEO Alok Mittal recalled that Indifi pretty much restarted the business in June 2021 after leaving it since March 2020 when the pandemic began

Mittal believes Indifi's competitive edge over traditional lenders lies in how it integrates category-specific data into its MSME lending tech stack

“One of the keys for indifi

has been neutralising the pre-existing biases and assumptions in MSME lending. That is helping us get a larger share of women-run MSMEs and cater to high-risk MSMEs without much risk,” Indifi cofounder and CEO Alok Mittal

MSME lending in India remains the big hope for a host of digital lending startups. Even as fintech startups and ‘super apps’ have flocked to the lending aisle to shore up flagging revenue from other segments, the likes of Indifi and others are banking on their competitive advantage and MSME-specific risk models to edge out the new competition.

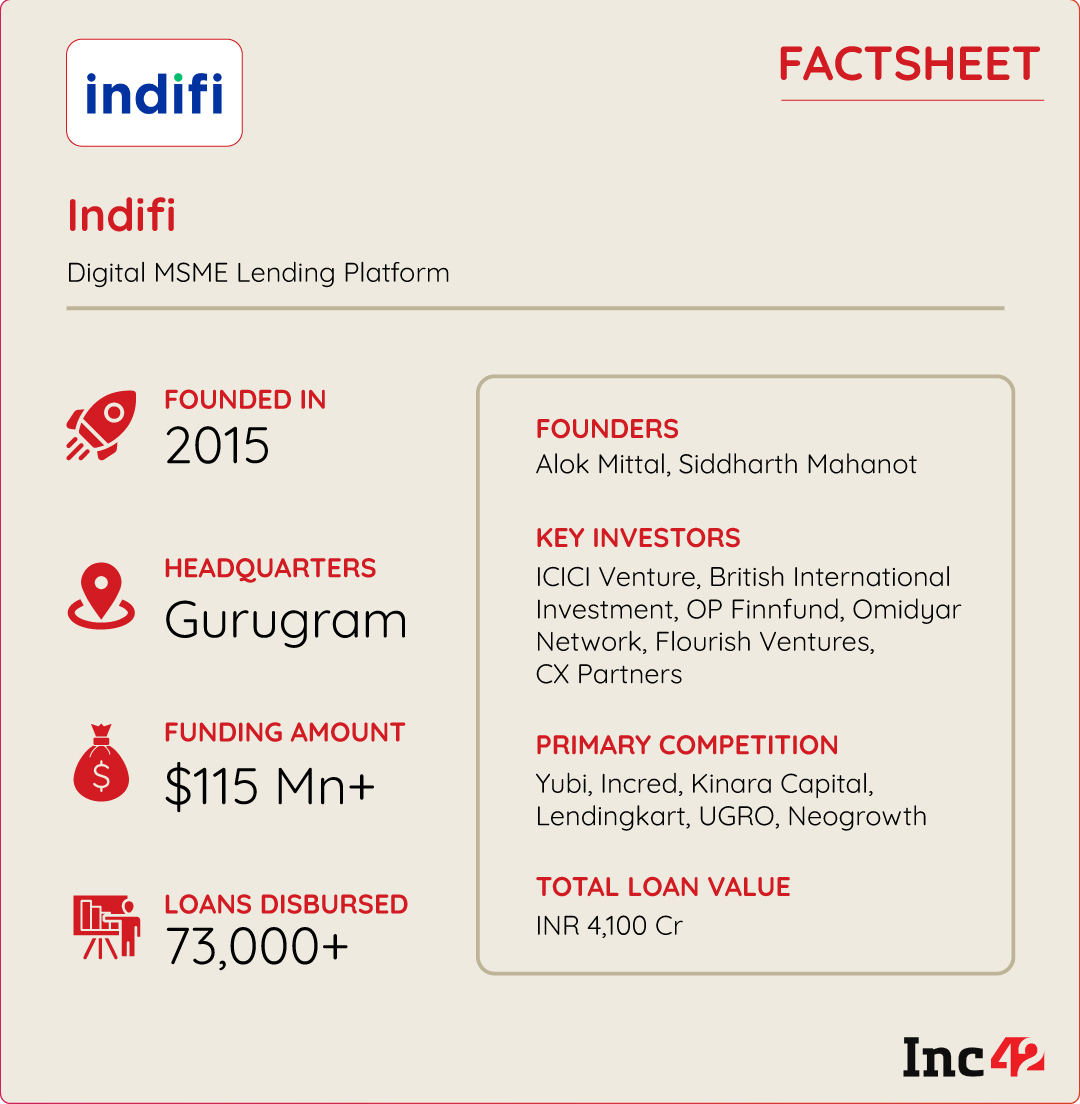

Founded in 2015 by Mittal, Siddharth Mahanot. and Sudeep Sahi, the startup claims to have hit its first profitability milestone in February 2022. Sahi quit the company in 2017 and is currently the founder of a payroll management company, Skuad.

Indifi reported a net profit of INR 5.1 Cr in FY23 as compared to a loss of INR 32.8 Cr in FY22, its maiden profit for the full year. Revenue from operations more than doubled to INR 198 Cr in March 2023 from INR 96 Cr, and Mittal is confident about maintaining this growth rate in FY24 as well.

This makes it a rare startup in the fintech space, as 40 out of the 48 fintech unicorns and soonicorns posted losses in FY22. This includes some direct rivals to Indifi besides the likes of CRED, BharatPe, PhonePe Paytm and the ones who also lend to merchants.

With rising digitisation and the constantly growing credit needs of MSMEs, the digital lending sector has emerged as a vital segment within fintech. India is estimated to be home to more than 63 Mn MSMEs, as per the MSME ministry data.

Gurugram-based Indifi’s growth in the past year has also attracted investors, even amid the ongoing funding winter. The startup raised $35 Mn in a Series E round in June this year, taking its lifetime funding tally to over $120 Mn.

Now, armed with this capital, Indifi and Mittal are ready to double down on the strategy that has unlocked profitable growth in the past two years.

How Covid Changed Indifi

First, some context on why digital lending emerged as something of a winner in the micro, small and medium enterprises (MSME) space after Covid. Before 2020, most MSME lending was led by banks and NBFCs, but as more MSMEs adopted digital tools during the pandemic, digital lending players leveraged the new data that was created to scale up.

The RBI’s 2022 report on ‘Trend and Progress of Banking in India’ noted that in the post-Covid period, credit growth to MSMEs in the industrial sector was distinctly higher on a year-on-year basis, as well as in comparison with credit growth to large industries.

Mittal recalled that Indifi pretty much restarted the business in June 2021 at about the same level that it had left it in March 2020 when the pandemic began. “In those 15 months, our risk models got stronger. When you go through these down cycles, the negative data of the cycle starts to come into your models,” Mittal told Inc42.

The cofounder and CEO also believes that the market conditions and the improved risk models from the Covid era helped streamline collection capacity and processes for Indifi, as it did for most of the other players.

Competing with the likes of Incred, Yubi, Lendingkart, Kinara Capital among a host of other players, Indifi primarily provides unsecured term loans and credit lines to MSMEs. The model involves lending directly from the NBFC as well as a marketplace for other lenders.

Indifi’s focus is entirely on the MSME class and retail merchants, whereas competitors have occupied other niches. Kinara Capital for instance is focussed on manufacturing, whereas ofBusiness has built its lending play around commodity supply chains as well as manufacturing.

This allows the startup to not only get direct revenue from interest on loans but also through origination and collection fees from third-party lenders. The diversification in the revenue stream helps Indifi shore up the bottom line, but for Mittal and Indifi, the real growth story has come in the past two years amid the pandemic.

Since July 2021, Indifi claims to have quadrupled its business on a monthly basis in terms of assets under management. To date, Mittal claims Indifi has disbursed more than 89,000 loans, with a cumulative value of over INR 4,100 Cr.

The company claims to have an average ticket size of INR 5 Lakh across the borrower base. A majority of its customers (63%) are from metro locations.

Mittal claimed that Indifi targets and maintains a 2.5%-3% rate of gross non-performing assets (NPAs). But how exactly have Indifi’s risk models evolved in the past two years and what does the founder mean when he talks about negative data from the Covid era?

Rewriting MSME Lending Risk Models

To start with, we all know that Covid created a lot of stress for MSMEs, resulting in a dramatic increase in their credit needs. The government schemes guaranteeing credit for MSMEs are a key indicator of the need in the market in mid-2020.

But Mittal emphasises that any credit slowdown doesn’t affect all MSMEs in the same manner.

“We started to get data around what kind of MSMEs are more vulnerable to stress relative to others. We modelled the stress response of different MSMEs differently. In a normal case, a particular MSME operates in a certain fashion, but is it resilient to stressful situations? That is the new dimension we added to our models,” the Indifi CEO, who was previously the managing director of Canaan Partners, added.

While conventionally, underwriting has been done with a view to take a yes or no decision on a particular application, Mittal said Indifi wanted to delve deep into segment and category data.

“We can take a different approach, a more proven approach of understanding what is the absolute level of risk that this (any business or category) represents. If someone represents a 1% risk of default, then I can price it differently for that customer than someone who represents a 5% risk of default,” he added.

Indifi’s Category-Specific Risk Models

Breaking this down, Mittal reveals the three key elements that are factored into the customer models:

- The Extent Of Digitalisation Of The MSME

- How Underserved The Category Is

- How Indifi Can Fill The Gap

“Strategically, we have chosen to be in the unserved to underserved MSME zone. We don’t want to go after the same demand that banks are going after because we cannot compete on pricing there,” he added.

The rationale is that this is typically the customers and categories that have credit concerns. Take for example the restaurant business, where working capital needs keep growing as the business scales and the rate of failure is very high.

Banks and NBFCs don’t typically create business-level models, the CEO claimed. “They create surface-level models but not business survival models. So, those are the core gaps that we look at.”

Something like 15% of restaurants go out of business every year, he claimed. Indifi claims to have built an industry-first model to predict whether a restaurant will be alive in 18 months or not. However, the segment-level risks very often do not manifest themselves in cash flow projections.

“So, we ask deeper questions — which micro market are they in? What cuisine are they serving? What is the price point? What are customers saying about them? These end up being more predictive of future performance and most importantly survival than the current cash flows,” Mittal told Inc42.

The other major differentiation is, of course, the tech platform, where Indifi has automated some onboarding processes for new customers and where it feeds in market data as it is evolving for various MSME categories. Besides customer-level data, Indifi leverages new data streams.

According to Mittal, what helps digital lending companies is that they are more agile in adopting new processes and technology such as automating underwriting processes, KYC and managing customer contactability. ”Banks are not adjusting for more data as quickly, and there are biases in the way they approach particular categories,” the Indifi chief added.

Similarly, other MSMEs have specific risks that vary from category to category. For instance, in the MSME travel business, the risk is about what the working capital will be used for because often it is used for personal expenses such as real estate. In ecommerce, there are pricing, discounting and commoditisation risks.

“These questions vary across segments, and hence, our solution to them varies depending on the answer. And these answers are then baked into our risk models. For instance, we know that contactability of entrepreneurs has improved, so we use the extent of contactability data to assess risks,” the cofounder added.

Technology adoption for customer verification and KYC includes paperless onboarding and continuous KYC compliance. Indifi uses a risk-based approach (RBA) to address and manage identified risks, and this in turn has improved collections as well.

When it comes to collections, Indifi has an in-house team and uses recovery agencies across states. “We have implemented a tiered system based on postal codes, which have been configured through an AI/ML-based scoring engine through the analysis of thousands of our customers. By categorising regions based on their capability and risk profiles, we are better equipped to allocate resources where they are most needed.”

Gaining With Financial Inclusion

The category-specific approach has paid off for Indifi so far in terms of revenue growth. For Indifi, the approach has yielded favourable outcomes for lending to businesses run by women entrepreneurs, another niche and underserved category.

Mittal believes that the unfavourable outcomes typically seen around lending to women entrepreneurs are largely due to the bias that women entrepreneurs face today from traditional lenders.

Financial inclusion is a major objective for most of India’s MSME lenders, as priority sector lending by banks and NBFCs has not managed to close the credit gap for businesses run by women entrepreneurs.

“If you look at the broad MSME market, about 20% of the businesses are run by women but formal credit penetration is less than 10%. If you take microfinance out, which is the primary women-centric model in MSME lending, the situation is even worse,” according to the Indifi CEO.

Women MSME entrepreneurs find it harder to raise capital than their male counterparts because there are biases in the traditional banking and NBFC system.

“So, in our case, what we have done is take that variable out so our risk models don’t have a gender variable. And just by doing this, we’ve been able to level the playing field. In our case, 20% to 25% of borrowers are women-run MSMEs,” Mitttal added.

Digital MSME lending players have become critical enablers of the economy by supplementing the bank and NBFC credit lines. Despite several startups competing for the pie, Mittal believes MSME lending is severely underpenetrated.

To reach new categories of businesses, Indifi is eyeing lending products in supply chain finance, secured loans, and even non-lending use cases such as insurance, payments and wealth tech where there’s a real opportunity to disrupt the MSME space.

As per Inc42’s ‘State Of The Indian Fintech Report Q2 2023’ report, the lending tech market opportunity will grow at a 22% CAGR from $270 Bn in calendar year 2022 to $1.3 Tn by 2030.

Mittal is confident that the market has more than enough room for the host of competitors. His bullishness seems reasonable from a financial inclusion lens. Only 15% of the MSME credit demand is being fulfilled by all the players combined, the CEO added.

For Indifi, this room for growth means more opportunities for all players to solve the financial inclusion problem. Ultimately, a thriving MSME sector will lift all players in the fintech space.