SUMMARY

InsuranceDekho has been able to raise $150 Mn, in one of the largest Series A funding rounds so far this year, amid the ongoing funding winter

According to the founder & CEO, Ankit Agrawal, the company will break even by the next financial year

InsuranceDekho has partnered with 80,000 point of salespersons (PosPs) to sell non-life insurance to people across 98% of the pincodes in India

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

Beema, Berozgaari, Beemari – these are not election slogans but something which the CEO and founder of insurtech startup InsuranceDekho Ankit Agrawal claims are the current challenges in the country that he is determined to resolve.

Agrawal, who hails from Begusarai, a town in the northern part of Bihar, and hits the road every few weeks, believes that the growth story of the county lies in its hinterlands – areas where InsuranceDekho bets big.

Although it may sound like a difficult task to convince people in the rural parts of the country about the importance of insurance, Agrawal says this market is ripe and awaiting a disruption.

The strategy seems to be working wonders for InsuranceDekho, which has reported a 61% YoY rise in its FY22 revenue and narrowed its losses, according to Agrawal.

Meanwhile, what has visibly helped the company is its LIC-like playbook of having a strong network of on-ground agents. According to Agrawal, the importance of in-person sales should not be underestimated.

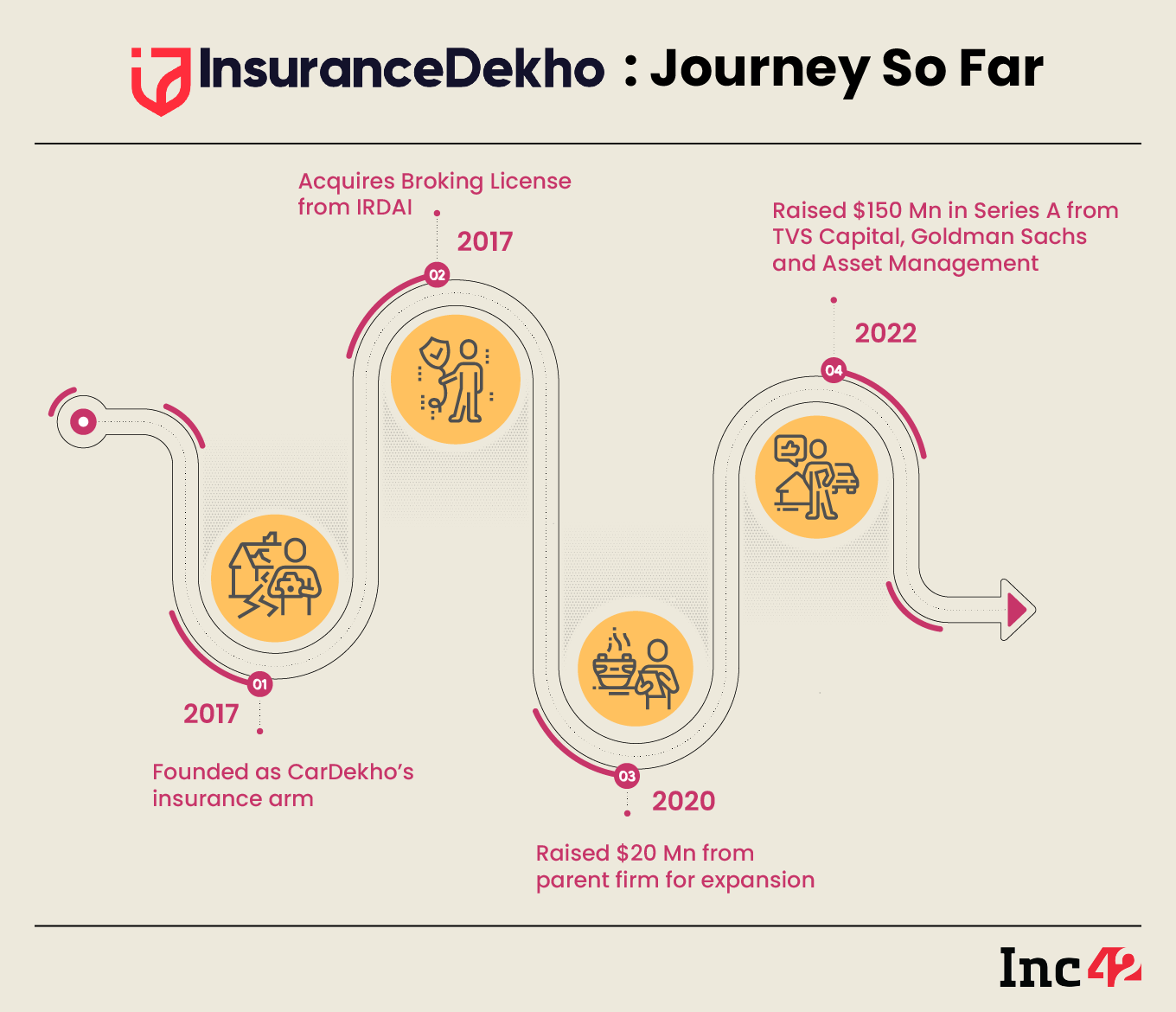

Further, it is pertinent to note that the insurance platform recently joined India’s soonicorn list, after raising $150 Mn in one of the biggest Series A funding rounds in the ongoing funding winter. Interestingly Agrawal told Inc42 that he wasn’t a big fan of fancy tags like unicorn, soonicorn or decacorn.

“I am a Marwari by origin and do not believe in burning cash, rather building strong business fundamentals, with cost efficiencies – something that has helped me shape many of my business decisions,” InsuranceDekho’s boss said.

Incorporated as the insurance arm of CarDekho, an online car marketplace, in 2017, InsuranceDekho received $20 Mn from its parent firm Girnar Software in 2020. From there, it hived off to function separately.

In a Linkedin post, following the round, Praveen Sridharan of TVS Capital (one of the major investors of the funding round) mentioned that various features of InsuranceDekho, including its quality team, focus on sustainable growth, digital DNA, make the VC firm bullish about the startup.

Agrawal, who is quite fascinated with the way cockroach startups function and survive various business cycles, says that he started the organisation to simplify the insurance buying experience and serve customers by offering holistic solutions – a market disruption exercise that has brought him many fortunes.

Sharing his aspirations with Inc42, the founder said that he wanted his venture to outlive him and thrive as an industry leader, transforming the insurance space.

“The success of InsuranceDekho is a testimony that one does not need to invest millions in attracting customers. I want this organisation to outlive me, and become an industry leader that continues to transform the insurance sector into a customer-centric space for decades to come,” Agrawal said, adding that his venture has significantly disrupted the insurance market with limited resources – a lesson that only cockroach startups can help you learn.

“In the current environment, only cockroach startups can win – the ones that are frugal and can truly withstand the market turbulence and dwindling demand,” he added, lauding the series of articles on ‘The Year Of Cockroach Startups’ that Inc42 published in January and February.

All Eyes On The Insurance Pie

The insurance sector is going through a paradigm shift, thanks to the rise of insurtech players in the country, which are changing the conventional way of buying insurance policies by helping people explore opportunities that otherwise remained hidden via traditional sources.

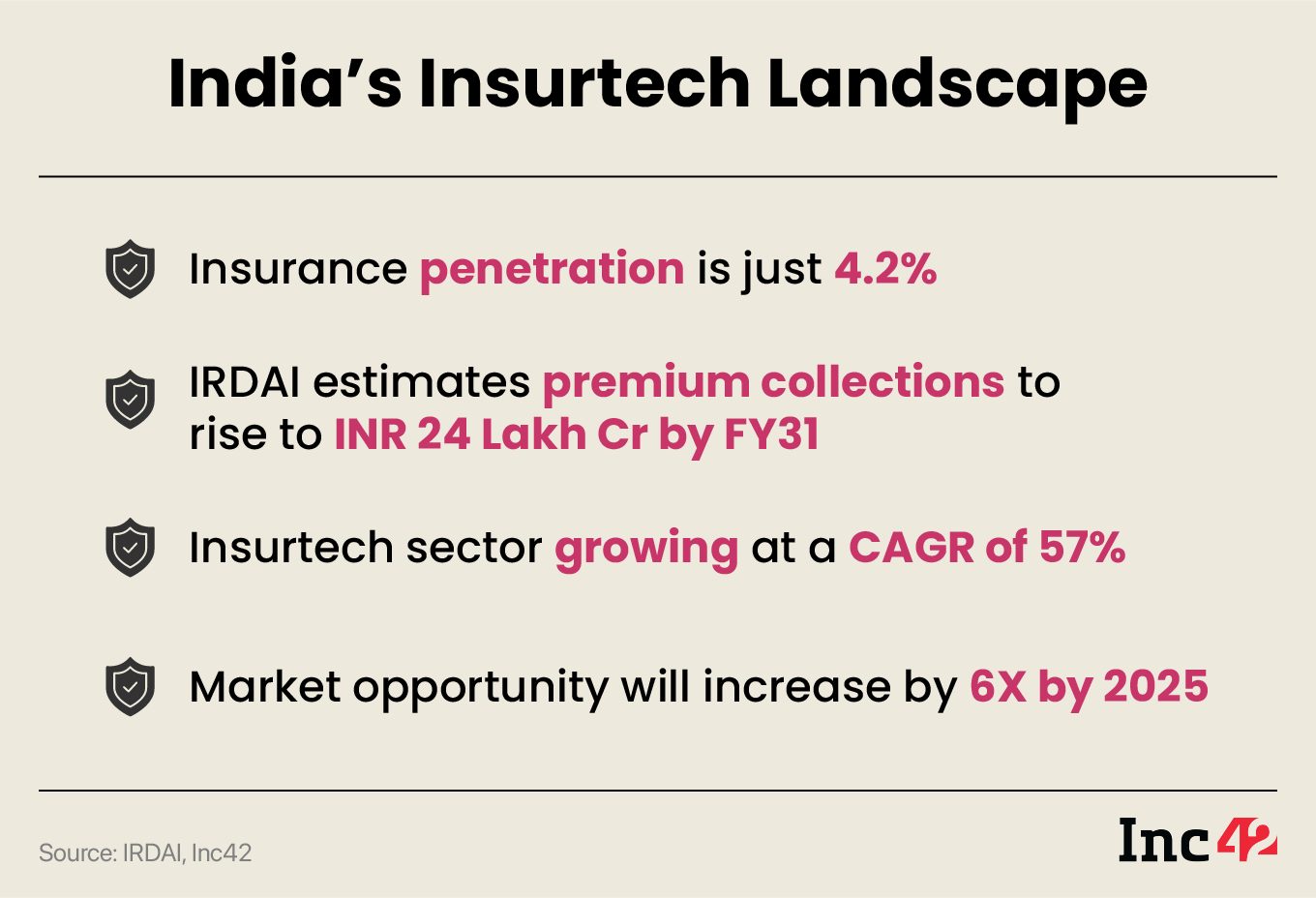

According to the Insurance Regulatory and Development Authority (IRDAI) data, life insurance premiums are expected to reach a size of INR 24 Lakh Cr ($317.98 Bn) by FY31.

Further, Inc42 estimates that the insurtech space is growing at a CAGR of 57%. This means that between 2021 and 2025, the market opportunity for insurtech players is expected to rise by 6X.

Various factors like the insurance penetration of a mere 4.2% in India (according to IRDAI) and an increase in the disposable income of Indians have paved the way for more insurtech players to enter the space.

Despite the entry of soonicorns, unicorns and decacorns in the segment, an increasing number of players are eyeing this ripe market.

Some of these names include PolicyBazaar, Acko, Digit (unicorns), Turtlemint (soonicorn), and PhonePe (a decacorn that plans to enter the space).

Many insurtech companies, including Digit, Acko, and TurtleMint, primarily act as tech platforms to sell policies from various insurance firms. Acko most recently acquired the IRDAI licence to become the first tech startup to sell life insurance.

While PhonePe recently said that it will focus its investments towards offering insurance services, the erstwhile founder of Flipkart, Sachin Bansal, has become one of the first tech entrepreneurs to have ventured into the insurtech space through his financial services firm, Navi. Most recently, BharatPe’s former CEO and MD Ashneer Grover, too, hinted at his plans to venture into the space, in an exclusive interview with Inc42.

These are just a few of the many names that crop up when you scratch the surface and do not include conventional players like LIC or retail banks that are focussed on amping up their digital capabilities to capture a chunk of the burgeoning market.

The COVID-19 Boost

According to Agrawal, insurance was synonymous with LIC until a few years ago and was only looked at as a tax-saving measure by salaried folks.

But the COVID-19 pandemic changed this equation. The pandemic expedited the adoption and awareness of insurance among Indians in a way no marketing campaign could do so far.

This is particularly true for health insurance, which has seen a spurt in the number of claims being filed and premium collections since 2021. Vehicle insurance has also seen an uptick lately.

According to General Insurance Council statistics, the gross premium collections for health insurance in India (by only health insurance providers) for FY23 (until February, 2023) stood at INR 22,103 Cr, up 27.2% YoY from INR 17,370 Cr in FY22.

Similarly, gross premium collections for health insurance by general insurance providers stood at INR 59,892 Cr, up 22.7% YoY, in FY23 (until February 23) compared to INR 48,788 Cr in FY22.

For motor insurance, the gross premium collections grew 15.6% YoY to INR 72,860 Cr in FY23 (until February 23) from INR 63,05 Cr in FY22, according to the GIC data.

InsuranceDekho’s CEO wants to tap this sweet spot in the growing insurance industry. However, the approach of his new-age tech company is almost similar to that of LIC, which has over the decades sold its products via its network of agents.

Just like LIC, InsuranceDekho has partnered with 80,000 point of salespersons (PosPs) to sell non-life insurance across 98% of the pincodes in India.

In 2015, the IRDAI came up with a new distribution model of Point of Sales Persons (PoSPs), which allowed firms to hire people from various backgrounds and give them basic training to allow them to sell pre-underwritten insurance products to their customers.

InsuranceDekho had the first-mover advantage here, as it acquired the broking licence in 2017. PB Fintech, the parent firm of PolicyBazaar is one of the insurtech firms that obtained the broking licence in 2021.

Agrawal hates to draw parallels, and says that his seven-year-old startup is basically aiming to fill the voids, which the old insurance firms in India have not been able to.

“Even if we are deploying the field workers or our sales agents to sell policies, we are a tech-first company and hence that gives us an edge over the legacy firms when it comes to deploying technology right from premium collections to claims settlements. And the numbers speak for themselves,” he added.

Besides, the CEO said that when it comes to Tier 2 and 3 towns, the importance of in-person sales cannot be underestimated.

“I have been travelling widely which led me to believe that although smartphone penetration in the country is massive, people essentially use it for entertainment and content purposes and not investments, which puts the onus on traditional sales channels to convince them to pay for insurance,” the CEO said.

Is InsuranceDekho On The Right Track?

Despite its losses ballooning 56% to INR 72.29 Cr in FY22, the startup is aiming to break even by the end of the next financial year.

“The company’s operating revenue for the year ended March 2022 grew ~60% YoY to over INR 100 Cr (~$12 Mn). We have also managed to reduce our loss margin by more than 3 percentage points in the period. We are expecting to hit the premiums collection at an annual run rate of INR 3,500 Cr (~$427 Mn) in the year ending March 2023,” the CEO said.

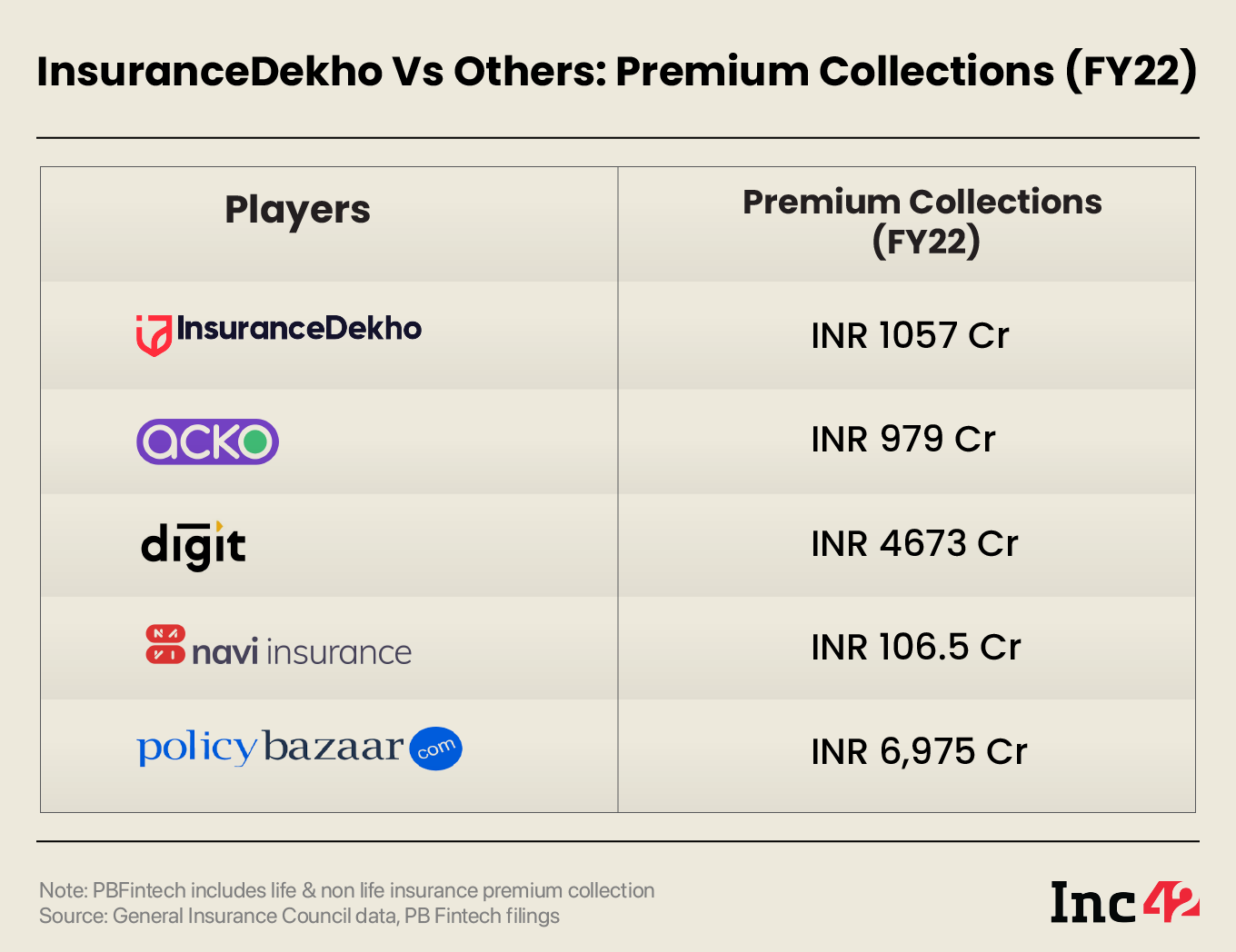

In FY22, InsuranceDekho’s premium collections stood at INR 1057 Cr, so if the company hits the target, that would be a solid 3x jump in premium collections.

We did a comparative analysis of the premium collections of InsuranceDekho with some legacy insurance firms and its competitors and observed that the startup has actually better premium collection numbers compared to its counterparts in the space.

According to the InsuranceDekho chief, this could be attributed to the underpenetrated insurance market in India’s heartland and remote villages that the startup is trying to tap through its PoSP agent network and where the leading players do not have a significant presence.

Besides, the insurtech startup claims to provide employment to more than 80,000 people, including housewives, college students, and retired professionals.

Agrawal told Inc42 that, with his venture, he is trying to solve real problems of the country like unemployment and making people aware of the importance of health insurance.

Meanwhile, when we asked if the company faces challenges in collecting premiums from people based in the country’s smaller towns and regions, Agrawal said that the statistics portray a positive picture.

Fighting Goliaths Of The Insurance Space?

The insurance sector has attracted a lot of attention in the post-COVID era, with conglomerates like Reliance, cash-rich startups like PhonePe and many entrepreneurs planning their foray into the space.

Experts say that in the next five to seven years, the non-life insurance vertical is expected to see a huge inflow of capital, especially in Tier 2 towns and beyond where the market is still in its nascent stages.

Earlier, research firm Jefferies had said that Reliance aspires to foray into non-lending financial businesses – life, general insurance and AMC – where it can even take the inorganic route and benefit from recent regulatory changes that allow banks to have up to nine insurance partners.

While the government has eased sectoral regulations by allowing PoSPs to sell policies from multiple insurers, it will now tax individuals, on the maturity amount of life insurance policies, whose aggregate annual premium exceeds INR 5 Lakh.

InsuranceDekhho CEO, however, says that the number of insurance buyers who pay premiums in the range of INR 5 lakh and above is very less.

When asked if the entry of new players poses a threat, Agrawal said that the market is large and there are enough opportunities for all, including the big players.

“Besides, we are not even competing with LIC or other insurers. We are simply partnering with them and helping in speedy disbursals of policies and claim disposals,” he added.

One may argue that the PosP network deployed by InsuranceDekho, which works on a commission basis, looks cost heavy; however, Agrawal says that he has taken very calculated decisions on marketing, hiring spends and raising funds. Further, according to him, his venture has enough cash runway and they are a clear path to profitability, despite the competition getting intense.

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.