Walmart Recently Acquired 77% Stake In Flipkart For $16 Bn

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

On May 9, 2018, Walmart confirmed officially what had been rumored for weeks, and announced that it would pay $16 billion to acquire a 77% stake in Flipkart, an Indian online retail firm, translating into a valuation of more than $21 billion for a firm founded just over ten years ago, with about $10K in capital.

Investors are debating the what, why and what next on this transaction, with their reactions showing up in a drop in Walmart’s market capitalization of approximately $8 Bn.

For Indian tech startups, the deal looks like the Nirvana that many of them aspire to reach, and this will undoubtedly affirm their hopes that if they build an India presence, there will be large players with deep pockets who will buy them out.

The Players

The place to start, when assessing a merger or an acquisition, is by looking at the companies involved, both acquiring and target, before the deal. It not only provides a baseline for any assessment of benefits, but may provide clues to motives.

- Flipkart, an Amazon Wannabe?

Of the two players in this deal, we know a lot less about Flipkart than we do about Walmart, because it is not publicly traded, and it provides only snippets of information about itself. That said, we can use that information to draw some conclusions about the company:

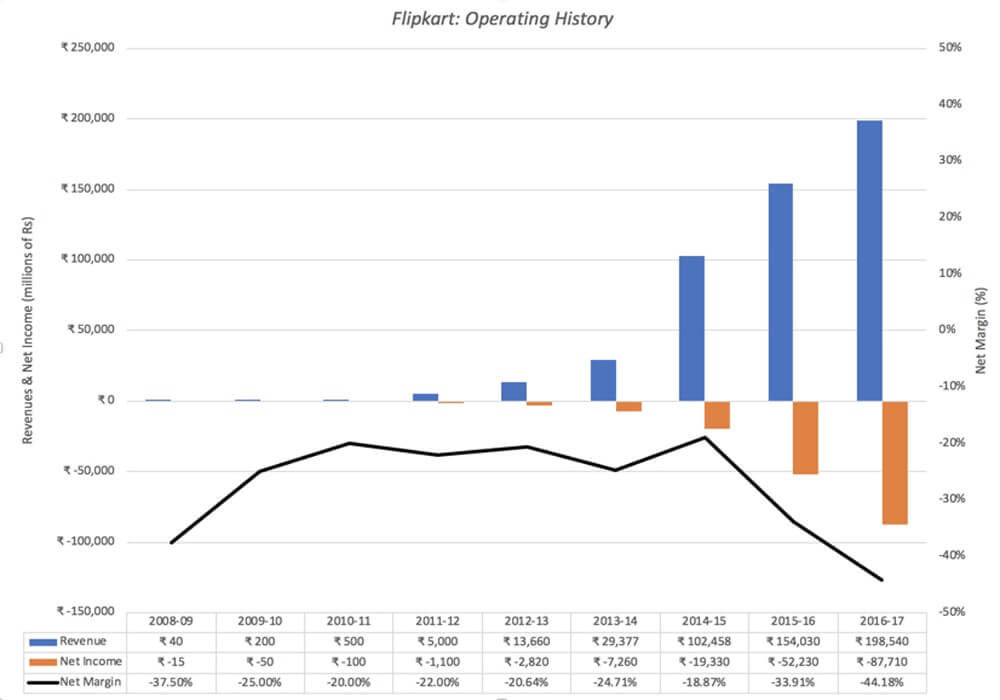

- It has grown quickly: Flipkart was founded in October 2007 by Sachin and Binny Bansal, both ex-Amazon employees and unrelated to each other, with about $6000 in seed capital. The revenues for the company increased from less than $1 million in 2008-09 to $75 million in 2011-12 and accelerated, with multiple acquisitions along the way, to reach $3 billion in 2016-2017. The revenue growth rate in 2016-17 was 29%, down from the 50% revenue growth recorded in the prior fiscal year. Flipkart’s revenues are shown, in Indian rupees, in the graph below:

- While losing lots of money and burning through cash: As the graph above, not surprisingly, show, Flipkart lost money in its early years, as growth was its priority. More troubling, though, is the fact that the company not only continues to lose money, but that its losses have scaled up with the revenues. In the 2016-17 fiscal year, for instance, the company reported an operating loss of $0.6 billion, giving it an operating margin of minus 40%. The continued losses have resulted in the company burning through much of the $7 billion it has raised in capital over its lifetime from investors.

- And borrowing money to plug cash flow deficits: Perhaps unwilling to dilute their ownership stake by further seeking equity capital, the founders have borrowed substantial amounts. The costs of financing this debt jumped to $671 million in the 2016-17 fiscal year, pushing overall losses to $1.3 billion. Not only are the finance costs adding to the losses and the cash burn each year, but they put the company’s survival, as a stand-alone company, at risk.

- It has had issues with governance and transparency along the way: Flipkart has a complex holding structure, with a parent company in Singapore and multiple off shoots, some designed to get around India’s byzantine restrictions on foreign investment and retailing and some reflecting their multiple forays raising venture capital.

While the defense that will be offered for the company is that it is still young, the scale of the losses and the dependence on borrowed money would suggest that as a stand-alone business, you would be hard pressed to come up with a justification for a high value for the company and would have serious concerns about survival.

b)Walmart, Aging Giant?

Walmart has been publicly traded for decades and its operating results can be seen in much more detail. Its growth in the 1980s and 1990s from an Arkansas big-box store to a dominant US retailer is captured below:

That operating history includes two decades of stellar growth towards the end of the twentieth century, where Walmart reshaped the retail business in the United States, and the years since, where growth has slowed down and margins have come under pressure. As Walmart stands now, here is what we see:

- Growth has slowed to a trickle: Walmart’s growth engine started sputtering more than a decade ago, partly because its revenue base is so overwhelmingly large ($500 billion in 2017) and partly because of saturation in its primary market, which is the United States.

- And more of it is being acquired: As same store sales growth has leveled off, Walmart has been trying to acquire other companies, with Flipkart just being the most recent (and most expensive) example.

- But its base business remains big box retailing: While acquiring online retailers like Jet.com and upscale labels like Bonobos represent a change from its original mission, the company still is built around its original models of low price/ high volume and box stores. The margins in that business have been shrinking, albeit gradually, over time.

- And its global footprint is modest: For much of the last few years, Walmart has seen more than 20% of its revenues come from outside the United States, but that number has not increased over the last few years and a significant portion of the foreign sales come from Mexico and Canada.

Looking at the data, it is difficult to see how you can come to any conclusion other than the one that Walmart is not just a mature company, but one that is perhaps on the verge of decline.

Looking at the data, it is difficult to see how you can come to any conclusion other than the one that Walmart is not just a mature company, but one that is perhaps on the verge of decline.

Very few companies age gracefully, with many fighting decline by trying desperately to reinvent themselves, entering new markets and businesses, and trying to acquire growth. A few do succeed and find a new lease on life. If you are a Walmart shareholder, your returns on the company over the next decade will be determined in large part by how it works through the aging process and the Flipkart acquisition is one of the strongest signals that the company does not plan to go into decline, without a fight. That may make for a good movie theme, but it can be very expensive for stockholders.

The Common Enemy

Looking at Flipkart and Walmart, it is clear that they are very different companies, at opposite ends of the life cycle. Flipkart is a young company, still struggling with its basic business model, that has proven successful at delivering revenue growth but not profits. Walmart is an aging giant, still profitable but with little growth and margins under pressure. There is one element that they share in common and that is that they are both facing off against perhaps the most feared company in the world, Amazon.

a. Amazon versus Flipkart: Over the last few years, Amazon has aggressively pursued growth in India, conceding little to Flipkart, and shown a willingness to prioritize revenues (and market share) over profits:

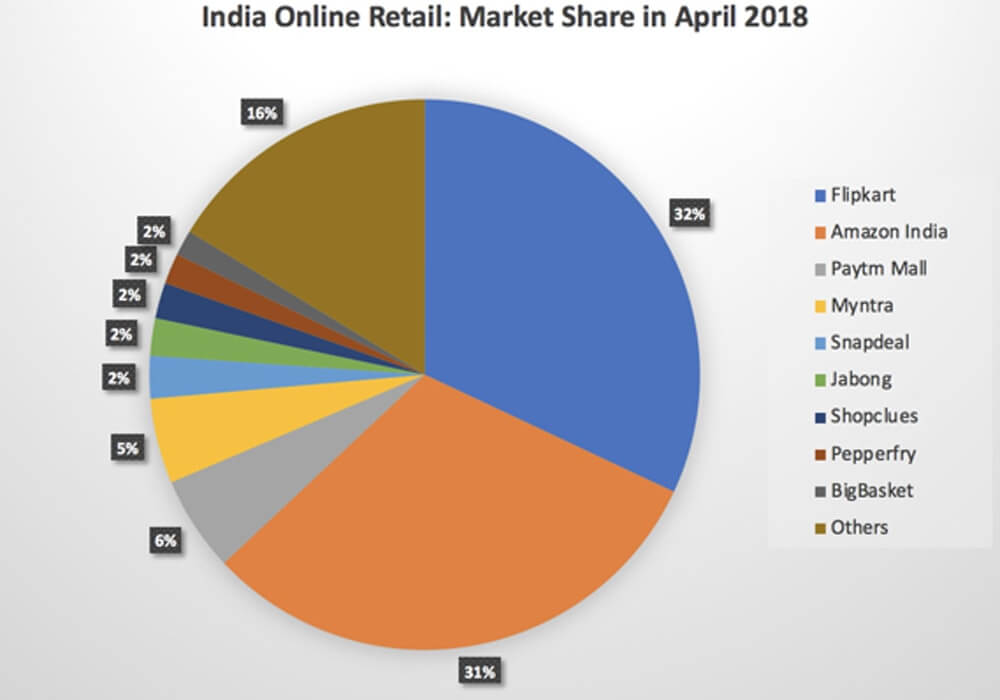

b) Amazon versus Walmart: If there is one company in the world that should know how Amazon operates, it has to be Walmart. Over the last twenty years, it has seen Amazon lay waste to the brick and mortar retail business in the United States and while the initial victims may have been department stores and specialty retailers, it is quite clear that Amazon is setting its sights on Walmart and Target, especially after its acquisition of Whole Foods.While Flipkart remains the larger firm, Amazon India has continued to gain market share, almost catching up by April 2018, and more critically, it has contributed to Flipkart’s losses, by being willing to lose money itself. In a prior post, I called Amazon a Field of Dreams company, and argued that patience was built into its DNA and the end game, if Flipkart and Amazon India go head to head is foretold. Flipkart will fold, having run out of cash and capital.

It may seem like hyperbole, but a strong argument can be made that while some of Flipkart and Walmart’s problems can be traced to management decision, scaling issues and customer tastes, it is the fear of Amazon that fills their waking moments and drives their decision making.

The Pricing of Flipkart

Walmart is just the latest in a series of high profile investors that Flipkart has attracted over the years. Tiger Global has made multiple investments in the company, starting in 2013, and other international investors have been part of subsequent rounds. The chart below captures the history:

Note that, through this entire section, I have used the word “pricing” and not “valuation”, to describe these VC and private investments, and if you are wondering why, please read this post that I have on the difference between price and value, and why VCs play the pricing game. Why would these venture capitalists, many of whom are old hands at the game, push up the pricing for a company that has not only proved incapable of making money but where there is no light at the end of the tunnel? The answer is simple and cynical. The only justification needed in the pricing game is the expectation that someone will pay a higher price down the road, an expectation that is captured in the use of exit multiples in VC pricing models.

The Why?

So, why did Walmart pay $16 billion for a 70% stake in Flipkart? And will it pay off for the company? There are four possible explanations for the Walmart move and each comes with troubling after thoughts.

- The Pricing Game: No matter what one thinks of Flipkart’s business model and its valuation, it is true, at least after the Walmart offer, that the game has paid off for earlier entrants. By paying what it did, Walmart has made every investor who entered the pricing chain at Flipkart before it a “success”, vindicating the pricing game, at least for them. If the essence of that game is that you buy at a low price and sell at a higher price, the payoff to playing the pricing game is easiest seen by looking at the Softbank investment made just nine months ago, which has almost doubled in pricing, largely as a consequence of the Walmart deal. In fact, many of the private equity and venture capital firms that became investors in earlier years will be selling their stakes to Walmart, ringing up huge capital gains and moving right along. Is it possible that Walmart is playing the pricing game as well, intending to sell Flipkart to someone else down the road at a higher price?

My assessment: Since the company’s stake is overwhelming and it has operating motives, it is difficult to see how Walmart plays the pricing game, or at least plays it to win. There is some talk of investors forcing Walmart to take Flipkart public in a few years, and it is possible that if Walmart is able to bolster Flipkart and make it successful, this exit ramp could open up, but it seems like wishful thinking to me.

- The Big Market Entrée (Real Options): The Indian retail market is a big one, but for decades it has also proved to be a frustrating one for companies that have tried to enter it for decades. One possible explanation for Walmart’s investment is that they are buying a (very expensive) option to enter a large and potentially lucrative market. The options argument would imply that Walmart can pay a premium over an assessed value for Flipkart, with that premium reflecting the uncertainty and size of the Indian retail market.

My assessment: The size of the Indian retail market, its potential growth and uncertainty about that growth create optionality, but given that Walmart remains a brick and mortar store primarily and that there is multiple paths that can be taken to be in that market, it is not clear that buying Flipkart is a valuable option. - Synergy: As with every merger, I am sure that the synergy word will be tossed around, often with wild abandon and generally with nothing to back it up. If the essence of synergy is that a merger will allow the combined entity to take actions (increase growth, lower costs etc.) that the individual entities could not have taken on their own, you would need to think of how acquiring Flipkart will allow Walmart to generate more revenues at its Indian retail stores and conversely, how allowing itself to be acquired by Walmart will make Flipkart grow faster and turn to profitability sooner.

My assessment: Walmart is not a large enough presence in India yet to benefit substantially from the Flipkart acquisition and while Walmart did announce that it would be opening 50 new stores in India, right after the Flipkart deal, I don’t see how owning Flipkart will increase traffic substantially at its brick and mortar stores. At the same time, Walmart has little to offer Flipkart to make it more competitive against Amazon, other than capital to keep it going. In summary, if there is synergy, you have to strain to see it, and it will not be substantial enough or come soon enough to justify the price paid for Flipkart. - Defensive Maneuver:Earlier, I noted that both Flipkart and Walmart share a common adversary, Amazon, a competitor masterful at playing the long game. I argued that there is little chance that Flipkart, standing alone, can survive this fight, as capital dries up and existing investors look for exits and that Walmart’s slide into decline in global retailing seems inexorable, as Amazon continues its rise. Given that the Chinese retail market will prove difficult to penetrate, the Indian retail market may be where Walmart makes its stand. Put differently, Walmart’s justification for investing in Flipkart is not they expect to generate a reasonable return on their $16 billion investment but that if they do not make this acquisition, Amazon will be unchecked and that their decline will be more precipitous.

My assessment: Of the four reasons, this, in my view, is the one that best explains the deal. Defensive mergers, though, are a sign of weakness, not strength, and point to a business model under stress. If you are a Walmart shareholder, this is a negative signal and it does not surprise me that Walmart shares have declined in the aftermath. Staying with the life cycle analogy, Walmart is an aging, once-beautiful actress that has paid $16 billion for a very expensive face lift, and like all face lifts, it is only a matter of time before gravity works its magic again.

In summary, I think that the odds are against Walmart on this deal, given what it paid for Flipkart. If the rumors are true that Amazon was interested in buying Flipkart for close to $22 billion, I think that Walmart would have been better served letting Amazon win this battle and fight the local anti-trust enforcers, while playing to its strengths in brick and mortar retailing. I have a sneaking suspicion that Amazon had no intent of ever buying Flipkart and that it has succeeded in goading Walmart into paying way more than it should have to enter the Indian online retail space, where it can expect to lose money for the foreseeable future. Sometimes, you win bidding wars by losing them!

What Next?

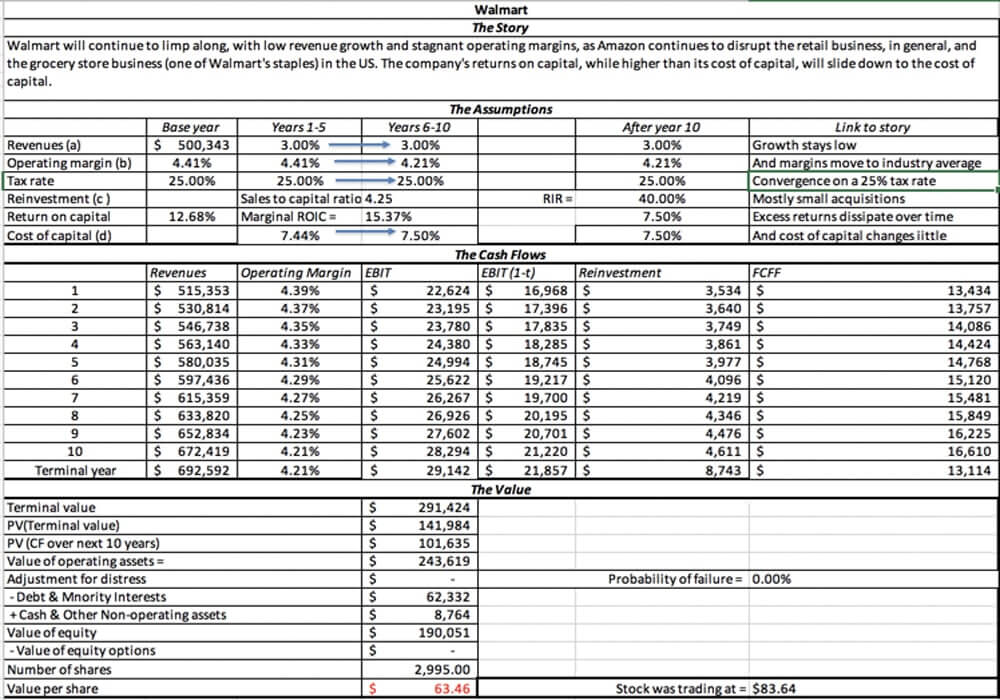

In the long term, this deal may slow the decline at Walmart, but at a price so high, that I don’t see how Walmart’s shareholders benefit from it. I have attached my valuation of Walmart and with my story of continued slow growth and stagnant margins for the company, the value that I obtain for the company is about $63, about 25% below its stock price of $83.64 on May 18, 2018.

In the short term, I expect this acquisition to a accelerate the already frenetic competition in the Indian retail market, with Flipkart, now backed by Walmart cash, and Amazon India continuing to cut prices and offering supplementary services. That will mean even bigger losses at both firms, and smaller online retailers will fall to the wayside. The winners, though, will be Indian retail customers who, in the words of the Godfather, will be made offers that they cannot refuse!

For start-ups all over India, though, I am afraid that this deal, which rewards the founders of Flipkart and its VC investors for building a money-losing, cash-burning machine, will feed bad behaviour. Young companies will go for growth, and still more growth, paying little attention to pathways to profitability or building viable businesses, hoping to be Flipkarted.

Venture capitalists will play more pricing games, paying prices for these money losers that have no basis in fundamentals, but justifying them by arguing that they will be Walmarted. In the meantime, if you are an investor who cares about value, I would suggest that you buy some popcorn, and enjoy the entertainment. It will be fun, while it lasts!

[This post by Aswath Damodaran appeared first on his blog and has been reproduced with permission.]

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.