Paytm is no stranger to insurance; the arrival of UPI and subsequent pressure on payments fees has led it to look beyond payments

Ecommerce insurance is yet to take off in a material way unlike China

Paytm First is said to offer a wearable-linked health insurance product

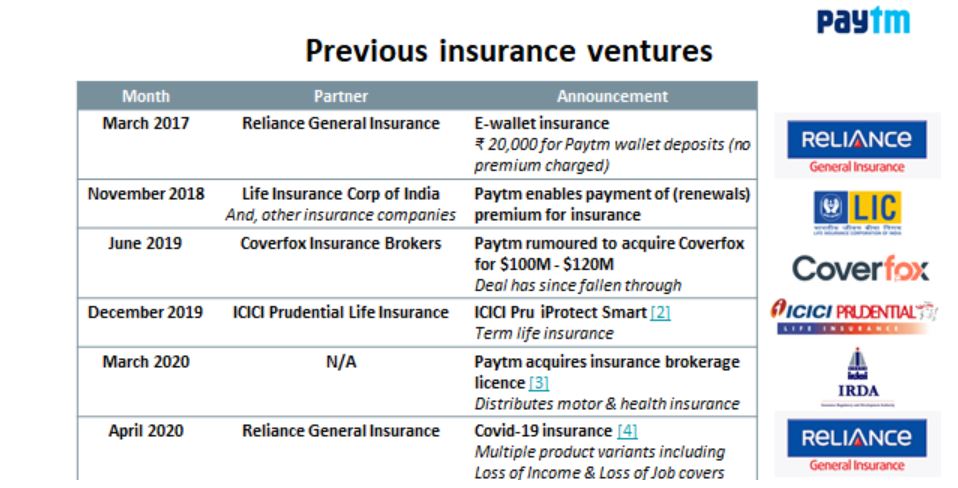

On July 7, Paytm announced its move to acquire Raheja QBE Insurance on July 6 for INR 568 Cr (i.e. $76.1 Mn). Although this deal is pending regulatory approval; it marks a shift away from Paytm’s previous strategy of acting as an insurance distributor (which seemed to be reinforced by the fact they got a brokerage licence in March 20).

Paytm is no stranger to insurance; the arrival of UPI and subsequent pressure on payments fees (e.g. MDR) has led it to look beyond payments to alternative services to capitalize on its existing user base of ~150M MAU and ~15M merchants.

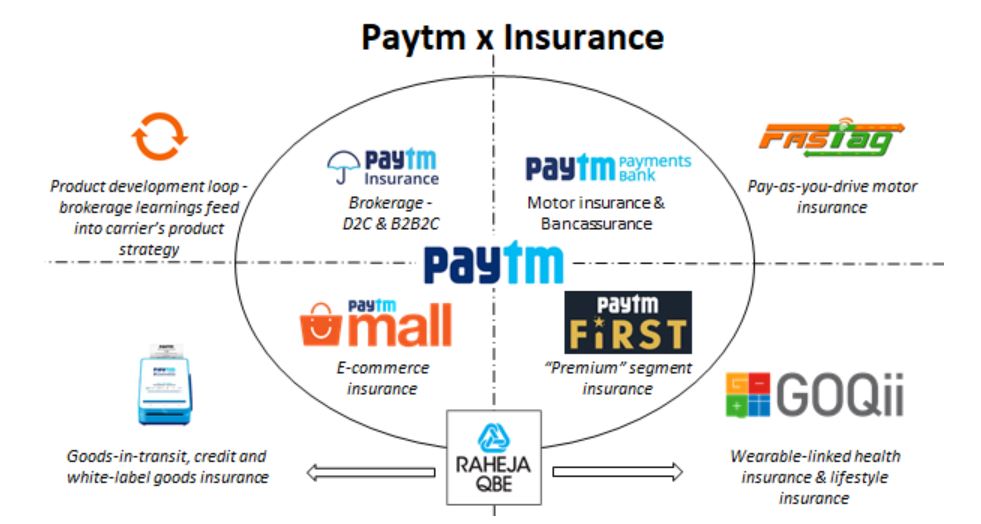

Whilst you may have heard the clarion call “What is Paytm’s business model?” – honestly, I don’t know but I can share my view on why they’d want to acquire a general insurance carrier. The graphic below summarizes my take:

In my personal view, owning an insurance carrier (especially in India), allows a company to innovate on the product side of insurance. We’re seeing early signs of this via the IRDAI’s InsurTech sandbox which is pioneering credit insurance, wearable-linked health insurance, “pay-as-you-drive” motor insurance amongst other products.

However, all of the above is in “pilot” mode; below, I will share 3 areas where I feel owning an insurance carrier can benefit Paytm:

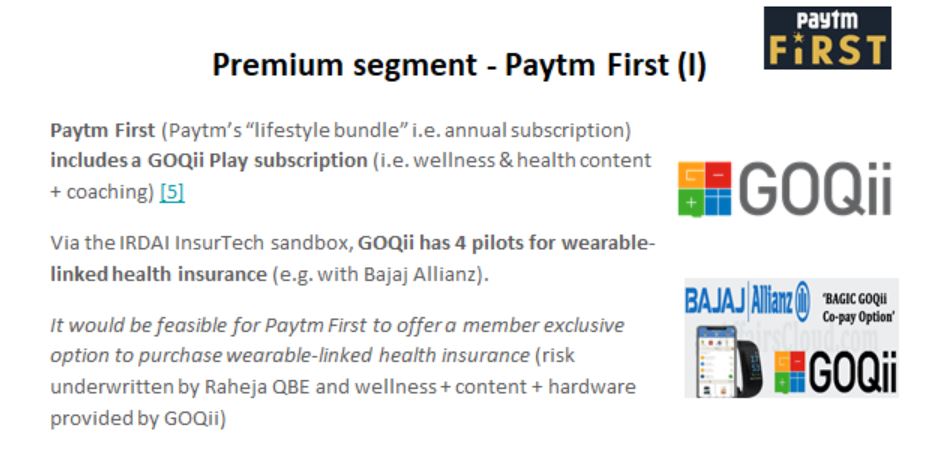

Lifestyle Insurance Via Paytm First

Paytm First is analogous to an Amazon Prime-style play of bundling “value-add services” for Paytm users into a single subscription fee; more notable amongst their partners is GOQii. The wellness provider currently has 4 wearable-linked health insurance products in the IRDAI’s InsurTech sandbox (it’s fair to call them the “default provider” of hardware + wellness + content in the context of health insurance in India).

The obvious play, in my mind, for Paytm First is to offer a wearable-linked health insurance product. Whilst GOQii could provide the hardware + content + wellness; Raheja QBE could underwrite the risk i.e. Paytm can build a “closed-loop ecosystem” for health insurance (Vijay Shekhar, Founder of Paytm, is an investor in GOQii)

However, that’s not all – Paytm First, together with CitiBank, offers a Visa-branded credit card. In the UK, Vitality has an AMEX card offering with cashbacks linked to physical activity (i.e. insurance + credit + health in one offering).

By owning Raheja QBE, Paytm could offer health insurance (via Raheja QBE) + credit (via Paytm First card) + wellness (via GOQii) + via a single Paytm First offering.

Motor Insurance Via Paytm Payments Bank

Paytm Payment Bank has issued ~4M FASTags as of March ‘20.

(FASTag is a sticker placed on windscreens for automated toll payments via an interoperable framework)

Via its Payment Bank, Paytm knows which of its users are car owners and moreover – it can triangulate usage of a vehicle (especially if petrol refills are made via Paytm).

“Pay as you drive” motor insurance is being piloted in the IRDA sandbox. Amongst all payment apps/FinTechs in India, Paytm is currently the best placed to up-sell pay-as-you-drive motor insurance.

- It can segment its driver base – “weekend drivers” can be targeted with a pay-as-you-drive product (by positioning it as savings on insurance).

- FASTag creates a natural engagement point for Paytm with drivers; it can push its own insurance products via behavioural nudges towards purchasing/renewing motor insurance

As previously mentioned, owning Raheja QBE will provide Paytm complete control over the user journey (insurance + payments for motor vehicles).

Ecommerce Focused Insurance

Ecommerce insurance (e.g. goods-in-transit, credit and white-label goods insurance) is yet to take off in a material way unlike China – which has seen ZhongAn emerge as a “star” player reaching $2bn in premiums within 7 years! In the Indian context, this opportunity is best highlighted by Amazon’s investment into Acko.

Paytm’s ecommerce ventures can be split into:

- Paytm Mall (ecommerce marketplace) ~ 100K sellers.

- Paytm for Business (O2O2O commerce via Kirana & PoS stores) ~ 15M merchants

Insurance products for MSMEs are yet to fully evolve in India:

- Credit insurance is just being tested in the sandbox.

- IRDAI has recently launched a standard Fire & Allied Perils insurance product for MSMEs. This product was typically reserved for larger enterprises i.e. small store owners and shopkeepers can seek insurance cover against fire, theft & other damage via a “white-label” product.

- The “every Kirana store is an InsurTech company” theme is emerging via StoreKing & other pioneers (who have begun to appreciate the PoS model in insurance)

MSME insurance is a greenfield for Paytm – together with Paytm’s merchant data and the fact that no incumbent has access to historic claims data, Raheja QBE would have a clear edge here.

The Weird – Broker & Insurer?

At first glance, people wondered whether owning a broker & a carrier makes any sense. This isn’t the first time I’ve seen a play like this – in Germany, WeFox (technology provider for insurance brokers) acquired digital insurance carrier ONE.

Effectively, owning a brokerage platform & your own insurance carrier creates a self-reinforcing product loop (i.e. discover gaps in the market and “learn” from other carriers).

That being said, Paytm would have to be careful about how it conducts business (other carriers might become suspicious) and there are certain regulatory aspects (which I will avoid).

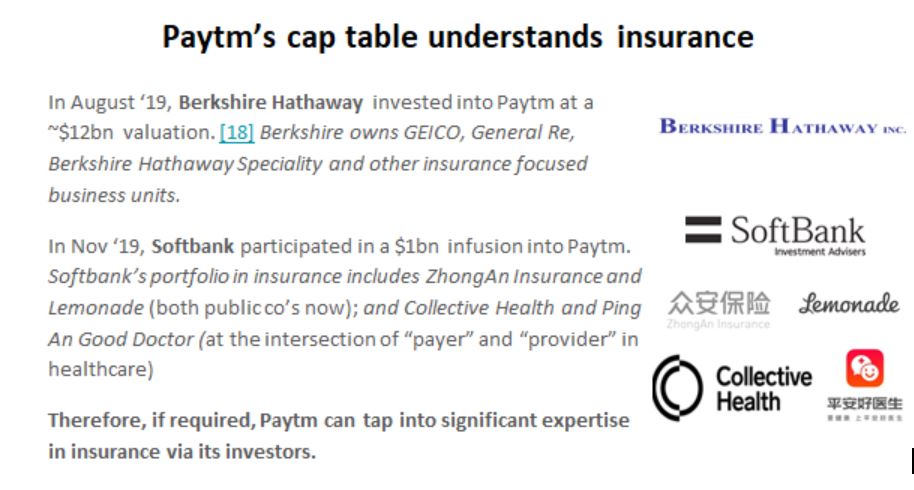

The last point I want to make: Paytm’s cap table has strong insurance pedigree – it can tap into expertise when required.

Closing Thoughts

This deal is (as of July 12) pending regulatory approval. Paytm doesn’t have a shortage of capital to run its own insurance carrier (with a $1bn infusion) and has broad distribution (~15 Mn merchants and ~150 Mn monthly active users) – the perfect ingredients for success as an insurance company.

Owing a carrier (given Paytm’s capital position) permits innovation on the product side of insurance (i.e. credit insurance, wearable-linked health insurance & “pay-as-you-drive” motor insurance) which is tricky to achieve as a broker (“skin-in-the-game” matters!)

In February 2018, Paytm registered “Paytm Life Insurance” & “Paytm General Insurance”; it has been a long journey since – can Raheja QBE become Paytm General Insurance? Only time will tell.

Disclaimer

Views expressed in this article are my own and do not represent those of Accenture, its management, its employees or its affiliates.

This article does not constitute investment or any other form advice. The author bears no responsibility in the event of financial or other loss arising from actions taken by the reader or any related party on the basis of information represented in this article. The author does not have any financial interest in any firm mentioned in the article above; this article is produced for educational purposes.