The upstream auto value chain is a complex system consisting of many just in time moving parts

The majority of the Tier 1 auto-component players are not facing any major labour challenges

Electrification, connectivity and smart vehicles will continue to impact the upstream value chain

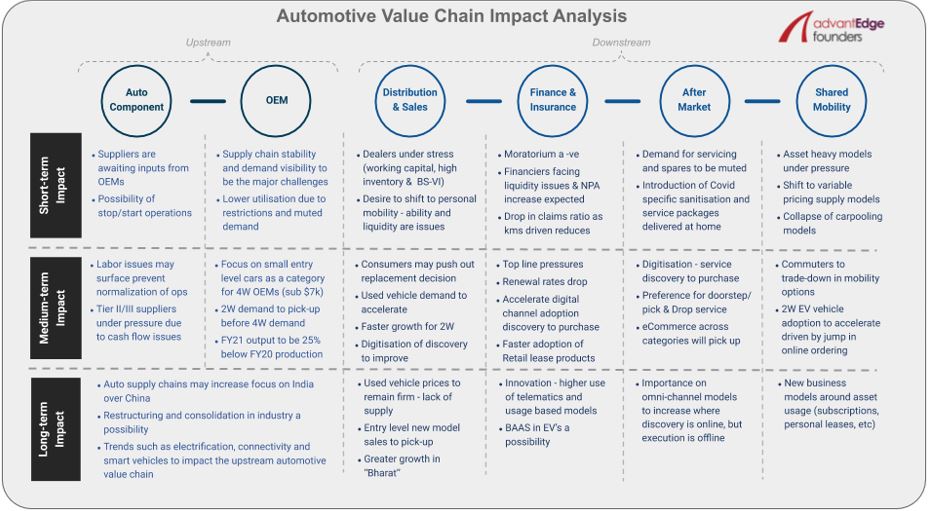

India was quite fast and proactive to put in place measures to deal with the Covid-19 threat, which started with a three-week lockdown in March and has now seen multiple extensions of the same. Given this extended lockdown in the country, the entire automotive value chain like most other sectors has been operationally impacted to a significant degree.

In this article, we highlight the immediate short-term (3-4 months) impact of the crisis, as well as the changes and opportunities this may throw up in the medium (up to 12 months) to long-term (beyond 12 months) for the auto and mobility ecosystems, both upstream and downstream.

The upstream auto value chain is a complex system consisting of many just in time moving parts. For an OEM to produce just one vehicle, they need thousands of separate parts arriving at their plant on time. This entire system which was brought to a grinding halt by the lockdown has started opening with many large OEMs and their Tier-I auto-component suppliers starting production at their plants. India’s largest OEM, Maruti started production at their Manesar plant on 12th May 2020, but are only operating a single shift, which is also reduced from 8 hours normally to 6.5 hours given the protocols/restriction in place.

“Both OEMs and their supplier production levels are at much-reduced capacities, as the auto-component players are awaiting inputs from the OEMs, who in turn are waiting for firm signals from their dealership network on end-consumer demand.”

In the short-term, there will be uncertainty over the stability of the auto supply chain, as the country is classified into zones based on certain Covid related metrics and the colour of the zone can change at any time resulting in halted operations. Demand visibility can also be a major challenge for OEMs in the short-term.

As per RC Bhargava, Chairman Maruti Suzuki, some of their dealerships which have opened have respectable levels of enquiries (Maruti has opened almost 2000 of their 3000 dealerships till now). However, using these early enquiries as a benchmark for short-term demand could be misleading, as there may be pent-up demand due to the 2-month lockdown.

Presently, the majority of the Tier-I auto-component players are not facing any major labour challenges as they are operating at low 20-30% capacity utilisations. As this utilisation is ramped up in the medium term, labour issues can crop up given the mass migration of labour taking place in India at the moment. Tier 2/3 companies may be worse affected by labour shortages due to larger dependence on contract labour.

Further, like most MSMEs, the smaller Tier 2/3 suppliers are expected to be under severe pressure due to cash flow issues. In the long-term, this is expected to give rise to restructuring and consolidation in the industry, as stronger Tier-I suppliers are nudged by OEMs to subsume weaker players in the value chain.

During economic downturns, household budgets come under severe pressure and individuals cut back on discretionary spends and also tend to trade down on essentials to cut costs.

“Mobility is not a discretionary spend and daily commute is a requirement for the majority of Indians to earn a livelihood, even after accounting for accelerated trends like work from home or flexible work.”

This combined with the fact that there will be a preference for personal mobility in the short and medium-term, we see two-wheeler (2W) demand picking up before four-wheeler (4W) and 4W OEMs focusing on the small entry-level car segment (sub $7k category). However, FY21 output is still expected to be 20-25% below FY20 production numbers.

In the longer term, major auto sector trends already underway like electrification, connectivity and smart vehicles will continue to impact the upstream value chain. If anything, electrification, for example, may accelerate given the lower total cost of ownership of many EV form factors in commercial use cases already.

Any acceleration will open up even more opportunities in the upstream value chain in India, as a majority of key EV components are currently imported like the motor, cells, etc and even the Government is keen to localise.

Downstream as well, across the value chain, the short-term impact is extremely negative. Dealers are under tremendous stress due to working capital pressures, high inventory levels and BS-VI issues. As discussed above, we do expect a desire from individuals to shift to personal mobility in the short term, but their ability and availability of liquidity to do so is still a question.

Hence, we expect demand for pre-owned vehicles to increase significantly, something which the two largest organised used car companies, Mahindra First Choice and Maruti True Value are already reporting. For new vehicles, demand will grow faster for 2Ws and from rural areas (assuming a normal monsoon which is currently predicted). Customers can also be expected to push out vehicle replacement decisions and not make a purchase decision in the medium term given the uncertainty of income and jobs.

In the longer term, we expect used car prices to remain firm due to the increased demand and the lack of supply. But this higher used vehicles pricing can drive prospective customers to buy new vehicles rather than used ones due to the price difference narrowing, pent up demand stretching over years and consumer confidence returning.

Both the finance and insurance and the aftermarket parts of the auto value chain have significant headwinds in the short-term. Extension of the moratorium has put further liquidity strains on the financiers and an NPA increase is expected. For auto insurance players, there is a silver lining as claims under motor insurance are expected to come down due to a fall in kilometres being driven from total/partial lockdowns and individuals desire to social distance.

However, with the claims ratio hovering around 160%, a deferment of the third party insurance rate increase by IRDA (revised yearly) and renewal rates expected to decrease, this may be a small positive.

“In the medium and longer-term, within the finance & insurance vertical, we do see opportunities for new business models to emerge due to changing customer preferences, market dynamics and possible regulatory shifts.”

Some of the opportunities could include a faster adoption of retail lease products, innovations around the usage of telematics & usage-based products and also the emergence of the battery as a service (BAAS) models supplementing EV adoption.“

As kilometres are driven are expected to be muted in the short-term, so will demand for servicing and spares. To drive demand, we expect players to introduce Covid specific sanitisation and servicing packages. Further, given the current emphasis on social distancing, in the medium-term customer preferences may shift to doorstep servicing and pick/drop off of vehicles.

“For the entire downstream auto value chain, digitisation of discovery should accelerate and in some cases, even decision making and purchase will be done online.”

Given this trend around the acceleration of digitisation, for the aftermarket vertical in the long term, we feel the importance of omnichannel models will increase with discovery online and execution offline like for batteries or tyres.

Restricted movement of individuals during the lockdown in India, saw revenue of all shared mobility models (like many other non-mobility businesses) collapse over 80%. Business models which are asset-heavy will remain under higher pressure in the short term and asset-light model recovery will vary by form factor and use cases.

As an example, carpooling models will not recover very fast, but low price point asset-light models should see faster recovery. The lockdown has provided a very valuable opportunity to some shared mobility players to move supply away from minimum guarantee models to revenue share models. Hence, even if the demand recovery takes slightly longer, the ability to achieve pre-covid margins will be faster.

“In the medium term, we see commuters trading down to save costs and hence 2W ride-sharing platforms like Rapido should gain market share from auto-rickshaws and even 4W rideshare for shorter distances.”

We also expect 2W EV adoption amongst the supply side to accelerate mainly driven by a jump in online ordering. Shared mobility is here to stay, despite the short-term & medium-term hiccups, but we should also see new business models emerge around asset usage, as well as targeting niche segments which are highly sensitive to the current crisis.