Here Are A Few Lessons On How To Prioritize And Work Across The Funnel

This is part of a series of advice for founders who need to raise money from venture capitalists. The first in the series is “Lemons Ripen Early,” which also has a link to other posts.

The most important advice I could give you before you set out in fund raising mode is to understand that fund-raising a sales & marketing process and needs to be managed. Somehow many first-time founders equate “sales” with something that is beneath them. I always tell founders …

“An investors job is to deploy capital and make a return. If you truly believe that you, your company and your products are exceptional and your company will be valuable then you’re actually doing them a FAVOR by helping them invest in your startup. If you don’t believe in your bones that you’re amazing then it’s no wonder you don’t want to sell them on making the investment.”

Like any sale you first need to plan your “prospects” and qualify whether or not they’d be a good fit for your product — an investment in your company. You need to figure out how much time to spend with each prospect and you need to rigorously manage your time and the calendar.

This is where most founders err. Most founders prepare a deck, ask a few friends and investors whom to meet, get a few introductions and just wing it. As a result, founders often meet the wrong investors, waste time on those who ask for more information.

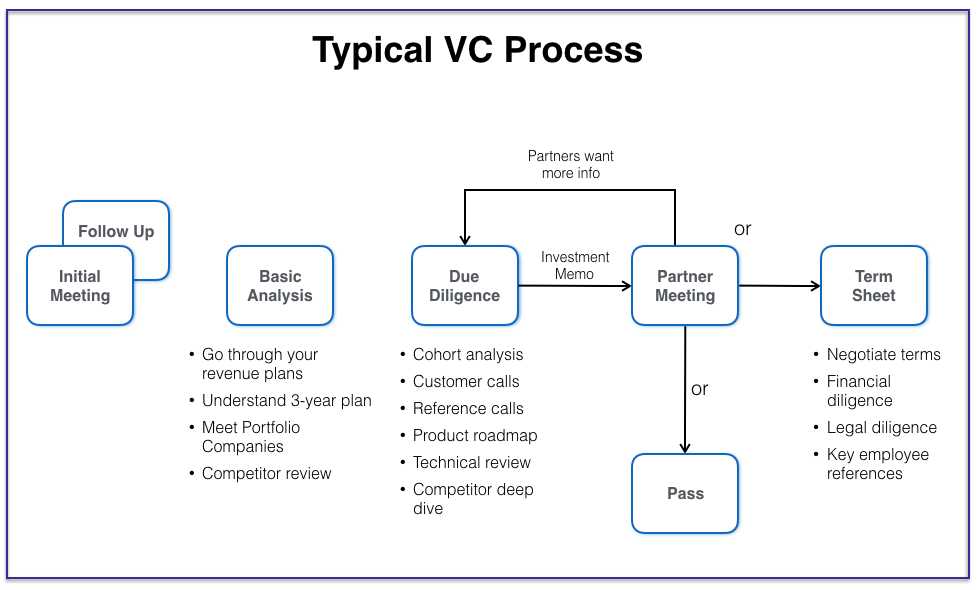

The typical VC process is as follows:

They say there are three rules in property: Location, location, location. In sales there are also three rules: Qualify, qualify, qualify. Your entire process should be about “testing” whether your prospect has:

- Interest

- Authority to make a decision

- Budget

- Is willing to continue spending actual time with you and analyzing you. You can short-hand this as “engagement.”

If an investor isn’t engaging then they’re not suddenly going to get a term sheet. The surest sign a fund-raising process has stalled is when you aren’t getting follow-up meetings or hearing from the VC or hearing from friends that they got a phone call or email asking about you.

If engagement wanes you either need to move that VC to a lower priority or you need to find ways to improve on any of these dimensions (obviously points 2 & 3 might mean you’re meeting the wrong person in the firm). Moving a VC from an A to a B doesn’t mean they aren’t still your top pick, it just means your chances are less likely and your extremely limited resources should be allocated elsewhere.

In my post “Measure twice, cut once” I’ve outlined how to plan before you start raising. Today I want to talk about the process and how to allocate your time.

How Many Investors Should You Speak With?

Of course, there’s no exact number of VCs you should meet — these are simply guidelines. For simplicity, I’ll assume you’ve raised some money from angels or seed investors and you’re either raising an A round or a B round of venture capital.

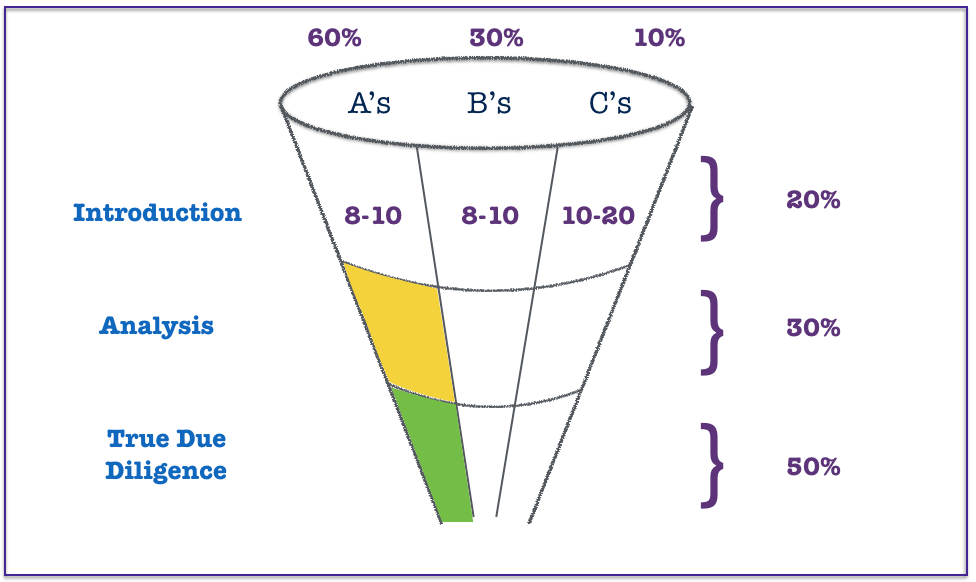

I like to start with a list of approximately 40 qualified investors. If you don’t know what is “qualified” please read my fund-raising planning post but assume they’re all the right: Size, geography, industry focus, capacity available and they themselves have raised a new fund in the last 3–4 years so you know they have dry powder.

If you’re raising a round where a new lead investor would invest $5 Mn the VC fund must have no less than $100 million and if you’re looking for them to write $15–20 Mn as the lead their fund realistically should be at least $400 Mn.

If you think you’ll have shared leads obviously fund-sizes can be slightly smaller but as a rough guideline assume most Seed/A/B VC funds wouldn’t allocate more than 5% of their fund to a first-time investment.

In terms of stack ranking I recommend you force yourself to have no more than 8–10 “A’s,” 8–10 “B’s” and the balance 20–24 should be “C’s.” An “A” is somebody who would be likely to invest in a company like yours and if chosen is somebody you’d be interested in working with.

If you’re not likely to get Sequoia then just because they’re an amazing firm doesn’t mean they go on your A list. If in high school you got a 3.6 GPA you might WANT to go Stanford but it isn’t likely so you spend more energy on schools you’re more likely to get into. Same with VC.

The A’s are the firms you’re going to work hardest to research, hardest to find high-quality introductions to and make the most effort to engage with. To be clear — your list never stays static. If you have a mediocre meeting with a high-quality prospect and you don’t think they’re likely to lean in they drop to a B or C. Likewise if a firm that you don’t think is your top pick suddenly starts engaging and doing work and showing you the love you might put them as an A because having an offer is important.

Should You Start with Your “Safety Schools”?

There is some debate about whether you should “test drive” with a few firms before a wider process or whether you just begin the process. People who believe the former believe that you should see the market demand before too many people know you’re “in market.”

I think there’s some truth in this. It’s such a small industry that if you talk with too many investors people will hear that you’re in market and quickly know who has passed.

My personal advice is that you first take 2 meetings with “safety schools” meaning somebody on your B list and somebody on your C list unless you already have a very strong relationship with somebody on your A list. This gives you good practice for your A meetings and you will have a sense of some likely questions, comments and concerns.

Then begin your process in earnest with up to 8–10 firms. These are the ones that you really want and that you also have a realistic possibility of landing. Keeping it to 8–10 helps you manage the public information flow that will be broader if you see 20 firms and also help you prioritize resources. You can hit a broader group in a few weeks once you know how you did with your initial meetings or perhaps of you did really well you can keep your aperture narrow.

Why 8–10 and not just 3–4?

One of the most important aims of a fund-raising process is to keep similar firms at the same stage of your process. If you’re talking with too small of a set and one leans in early and offers you a term sheet and you’re not sure that it’s the firm you really wanted to work with it is incredibly difficult to slow them down and say, “we really need to finish our process” as you run the risk that they feel played.

An investor who doesn’t feel like there is a two-way commitment will eventually walk and look for deals they perceive as a better two-way fit.

As a VC I, of course, want you to come see only me because that means I have no competition and have time to properly get to know you. But honestly, you should do this before you’re actually raising, which was the basis of my “Lines, not Dots” essay. If we feel a mutual connection then my goal is to make your life easier by offering you a term sheet before you’re even raising and I’ll spend the time and effort trying to prove that it isn’t worth running a process. This is the exception, rather than the rule.

How Do You Know if a VC is Engaged?

The first meeting is usually with 1–2 people within the VC firm. You might start with a partner in the meeting or it might be a principal or associate. In any event this is a “screening meeting” or as I’ve called on my graphics an “introduction” to the firm. It’s hard but not that hard to get a first meeting for talented teams who hustle.

It’s infinitely harder to get a prompt* second meeting due to rigorous time management on behalf of a VCs. (* VCs will often grant you a second meeting in 9–12 months to hear a progress update).

Many VCs will appear to be super friendly in a first-meeting because they are there to learn and get to know you and there’s no upside to being an asshole (Yes, I know some VCs are assholes anyway. Remember, I was an entrepreneur for 10 years before a VC).

The warmest, friendliest and yet most direct VC on why he wasn’t going to invest in my company was Gus Tai at Trinity . Even though I got a “no” he helped me understand why I wasn’t a fit for him and that always set the bar for how I wanted to treat entrepreneurs — friendly, but direct in my thoughts.

I point out that VCs are often friendly in the first meeting because I’ve heard hundreds of founders tell me their first meeting was great only to feel ghosted when there is limited engagement following this meeting. There is a super simple way to know if a VC is engaged. If you get a second meeting, a follow-up phone call or you know they’re doing actual work then they’re engaged. No VC spends more time evaluating your company unless they know that they at least have some interest.

This is a sales process and your job is to look for “buying signals” — remember: Qualify, qualify, qualify.

Other signs of engagement are: they ask you to meet with portfolio companies (they want feedback on your product and you), they ask you to meet a colleague, they set up a call to go through a product demo / financial walk-through, they ask to speak with customers, etc.

It is NOT necessarily engagement if they ask you to send a bunch of financial information under the guise of “doing analysis on your firm.” It drives me nuts but many VCs ask for all of this because they figure more data is better than less and they might as well have insight into how your numbers look. This goes into the heart of my controversial blog post (coming soon! it’s item 7 on this series) “Why You Should Never Have a Data Room.” Come back to this blog over the next 2 weeks and I’ll explain.

But the previous is that I wouldn’t send your data lightly. I’d ask that you have a second meeting in order to walk through your data or maybe ask to walk through it with an associate. If they won’t spend time going through it with you then they’re more likely just shopping you for data.

The best test of engagement is time so I like to ask people to let me walk them through the data and then I’ll send it to them afterwards — even if it’s just a web conference call walk through. Your job in the sales process is to test engagement so you can figure out how to allocate your time better. It’s also true that the more time you have engaging with an investor the more you remind them why they loved you in the first place.

If a VC “ghosts you” (i.e. they told you it was a great meeting but then they don’t respond to emails) DO NOT ASSUME it means they’re not engaged. I wrote about it here. Sometimes — best will in the world — people just get busy. Your job is to push politely until you either get a “soft no” or more engagement.

If you fold simply because they haven’t responded to your last two emails you won’t have success in business development, sales, press, recruiting … anything. Every important person with whom you want to do business will at times go dark on you as self-preservation for other tasks they’re trying to complete.

How Do You Work the “Bottom End of the Funnel?”

Most entrepreneurs make the mistake of allocating too much time to taking new meetings or to spending time on the wrong investors simply because they’ll keep meeting with you. Don’t. Keep your eye focused first and foremost on any VCs that are A’s and are in your “analysis” or “due diligence” phases. This is the green and yellow portions of my graphic above which I’ve highlighted specifically as a reminder to you. Most entrepreneurs don’t put enough effort into these phases.

Sometimes engagement at the later stages seems to go dry. They haven’t said “no” but they don’t seem to be spending a lot of time thinking about whether to progress. It should be obvious to you. At the end of the process is when they really need to decide not only whether they want to invest $5–10 Mn in your company and take the personal risk of being wrong, but they’re also voting on how they might spend a considerable amount of their personal time for the next 5–10 years and nobody smart does this lightly.

Your job is to create reasons to spend more time with you and to draw them into engaging because the more time they’re doing work, thinking about you, spending time with you and getting their head around why this could be really exciting then the more likely they will bring you into a partner meeting or make a final commitment to you.

Some easy hacks to get in front of a VC again if your process stalls

- Have them meet key team members they haven’t yet met — particularly if these are people whom the VC would want to know regardless of whether or not they fund your company

- Show demo’s of product that is yet to be released. This requires you to be disciplined and not sure it early in the process but a quick message to a VC that says, “I’d love to show you some really cool new features we’ve built in that we haven’t shown the market yet — can I get 20 minutes to swing by” is a good way to engage.

- Sometimes I encourage teams to create new analysis on cohorts, future revenue projections, competitor reviews, pricing studies, etc. Any information that creates a compelling next meeting is worth doing. With some pre-planning you might even know what information you show in your first or second meeting and what fragments you save for a follow-on meeting.

- Another idea I use is to encourage entrepreneurs to ask whether it’s ok to meet another team member of that VC in a 1–1 session to also show them your product. You can’t ask for a generic person — it must be a named individual that has some reason for you to meet. But that’s a chance for you to “land and expand” and build more fans inside the VC firm. It doesn’t have to be a partner — every advocate on the inside if valuable.

Due diligence meetings are the hardest to secure because VCs of course know that these follow-up meetings create obligations for them and if they’re balancing five potential deals and haven’t decided whether or not you’re a fit yet then they don’t meet again easily.

As a result, many entrepreneurs take the easy route of taking new first meetings because they’re easier to get, easier to prepare for (you already have a deck) and the feel like progress. Frankly, this is like running a sales campaign and when the last big push to persuade four disparate departments to back you and it starts feeling difficult, you instead start working on selling to different customers.

As dumb as it sounds, this is a very common playbook for entrepreneurs. The bottom end of the funnel is hard. Damn hard. But I’d rather see your time and energy go into creating new artifacts to share with your prospective VCs in the bottom of the funnel than just purely taking too many new meetings.

Why Marketing Helps

In the earliest stages of this post, I mentioned that fund-raising is a “sales & marketing” process but I’ve only spoken about sales. Marketing support is as critical in a fund-raising process as it is in a sales campaign. If you’re ever been involved with enterprise marketing you know how important it is to have marketing collateral and to have email drip campaigns and to drive re-marketing campaigns to prospects who showed interest but didn’t convert and to run PR so that you stay top of mind.

If you accept that these marketing techniques are critical in enterprise sales then please understand that they are no less critical in fund raising. When you plan out your fund-raising process you should dedicate some tasks on your GANTT chart to marketing.

When VCs are thinking about whether to take a second, third or fourth meeting it doesn’t hurt that they saw an article about you in the WSJ, Recode or TechCrunch. If you have a friend of the VC who is a customer of your product or an existing investor in your company and they share news of your company in their social feeds it helps to remind the VC that they need to engage.

Every VC just like every consumer of any product likes to think that we aren’t at all influenced by marketing but of course any behavioral economist can prove to you that we are. As a founder, use this basic knowledge to your advantage.

Why You Need to Keep Feeding the “Top of Funnel”

Having pleaded with you to put more time into the bottom end of the funnel, I do want to encourage you not to completely ignore the top end of the funnel.

In some cases, VCs lean into a deal, do tons of work and seemingly get so interested that they seen about to submit a term sheet only to have them say “no” at the last minute. Your lead on the deal was likely sincere in his or her interest in you but possibly got shut down when seeking approval.

The problem with putting all of your eggs into this one basket is that if you do get a “no” then you don’t have a well established pipeline of other prospects who have already gotten through a meeting or two and you end up having to go back to square one and you lose 6–8 weeks, which can be existential for some startups.

It seems obvious that you shouldn’t count on one VC whose process seems to be going well but I’ve seen so many entrepreneurs do this that I want to highlight it and remind you not to let this happen. Even if you are certain that you’re about to get a term sheet you need to keep working a few names in the top end of the funnel all of the way through a signed term sheet.

Never just assume that this will come through. I know you’re likely tired at the end of a process but it’s important to sprint through the finish line. Even if you DO get a term sheet there’s no saying you’re going to like the terms and with no pipeline behind you you’ll likely feel pressured to just say “yes.”

Summary

Fund-raising is a sales & marketing process in which the buyer is a VC and the product is equity in your company.

Any great sales & marketing campaign begins with methodical planning and any great process is run with rigorous time allocation on the most important prospects.

Because many startup founders view “running the business” as their only job and view fund-raising as something that they’re forced to do every 18 months it often doesn’t get the time, attention and resources it deserves. It’s true that fund-raising in its own right won’t make you successful, but being successful at fund-raising can give you a distinct advantage in the market against your competitors who aren’t as good at getting financed as you or have to spend more time in the market.

Plan accordingly. Fund-raising is a year-round activity and never ends. Place a small amount of your monthly time allocation to this task. Outside of fund-raising periods it should still be at least 15% of your time. It’s a large part of the job of a successful CEO.

[This post by mark Suster appeared first on bothsidesofthetable and has been reproduced with permission.]