Introduced in 2021, the RBI’s Recurring Payments Guidelines continue to disrupt the ease of doing business in India as all payment stakeholders are yet to seamlessly integrate the framework

Inc42 spoke to over a dozen founders to find out whether they have ever exercised their e-mandate on the SiHub or MandateHQ platforms, a whopping 80% of them said they haven’t

Fintech and subscription economy players believe the guidelines have been poorly executed and that the RBI needs to must make it mandatory for all banks to join the framework

On October 1, 2021, the Reserve Bank Of India (RBI) introduced the Recurring Payments Guidelines and later card tokenisation frameworks to help customers end unwanted subscriptions and secure their financial data. At the time, many suggested that the framework would be a highly disruptive intervention and 20 months on, it’s looking exactly like that.

It’s June 2023, and subscribers and platforms continue to face issues while making recurring payments via cards, the guidelines seem to have caused more pain than they solved. Messages such as the ones produced below have become all too common.

Not just that, the RBI’s Recurring Payments Guidelines have severely impacted SMEs and startups offering monthly or annual subscription-based services, OTT platforms, and international giants offering services in India, thereby impacting the overall Indian subscription economy, which boomed during the pandemic.

Speaking to Inc42, Nikhil Pahwa, founder and CEO of Medianama, averred, “Both as a consumer and as a business user of global digital services, I’ve found that recurring transactions fail often. We’ve also had situations where some global services no longer accept Indian credit cards, post the RBI guidelines related to recurring payments, as well as the tokenisation guidelines. As a consumer, I have had to re-enter my credit card details and enable payments for a few Indian services as well, and that’s an inconvenience I wish I didn’t have to deal with.”

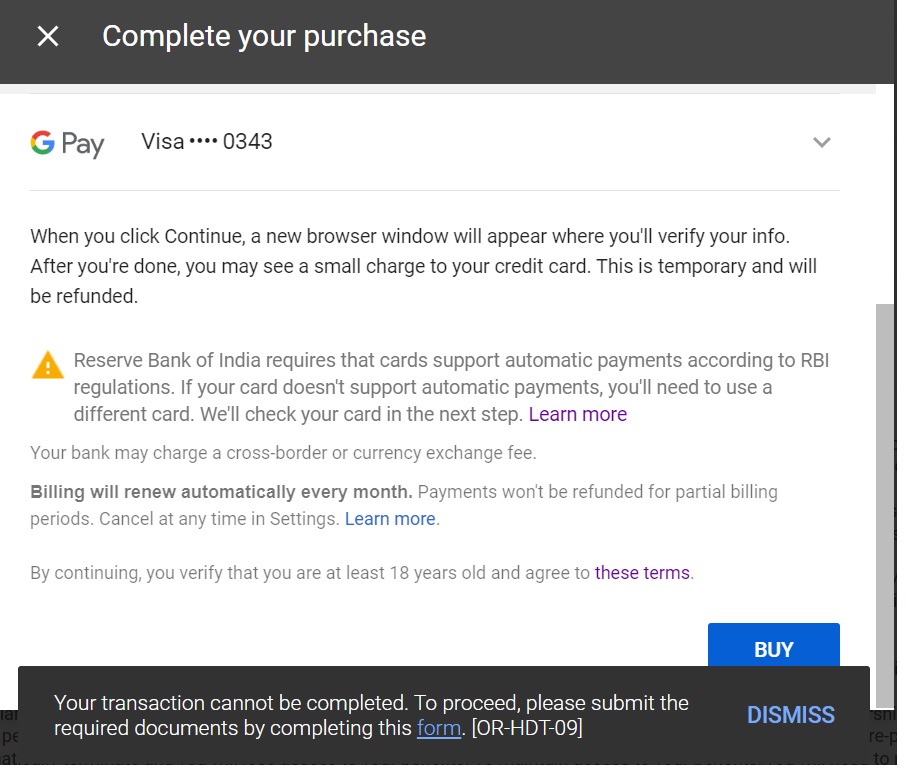

Even a company like Google is not able to deal with the mess.

Whether it is Google Cloud or Workspace or other services by the global tech giant, customers are grappling with payment hurdles. “Google repeatedly declines the cards, despite the cards being fully active,” a founder running a stealth-mode SaaS startup told us.

“Since Google does not accept debit cards or UPI for recurring payments, I had to borrow a card from someone else just to make the Google payments,” the founder added.

This is undoubtedly not the ease of doing business that the Indian government has been touting for the past few years. And, in fact, a complete contrast from the fintech and payments reputation that India holds today.

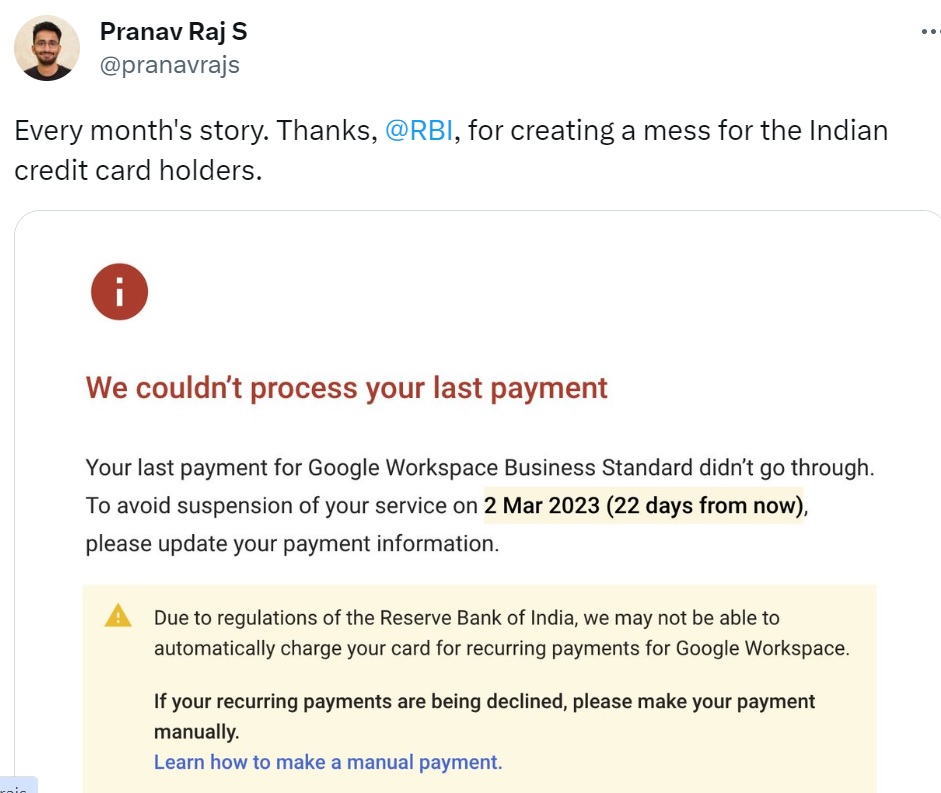

For instance, Pranav Raj, cofounder and CEO of YC-backed open-source omnichannel customer engagement suite Chatwoot tweeted in frustration on February 8, 2023.

Pranay Kotasthane, deputy director at Takshshila Institution, wrote, “I’m genuinely surprised that this isn’t a big deal. The RBI increased transaction costs for people and small businesses. More than a year later, it’s still a problem. I spend the first day of every month just coordinating all subscription payments.”

There are multiple reasons behind the recurring payments failures, argues Pushpa Marwal, an analyst at Forrester Research.

“In the ever-evolving landscape of recurring transactions, it is imperative for banks to put the customer at the centre of their strategies…Banks must prioritize two factors. First, they need to focus on customer education and awareness. In this way, banks can build trust, empower consumers, and build lasting relationships. Secondly, they need to put the customer at the centre and adopt a unified channel approach that provides better insight into subscriptions. This will really help banks achieve sustainable growth in the subscription business,” Marwal told Inc42.

These guidelines have definitely impacted subscription businesses.

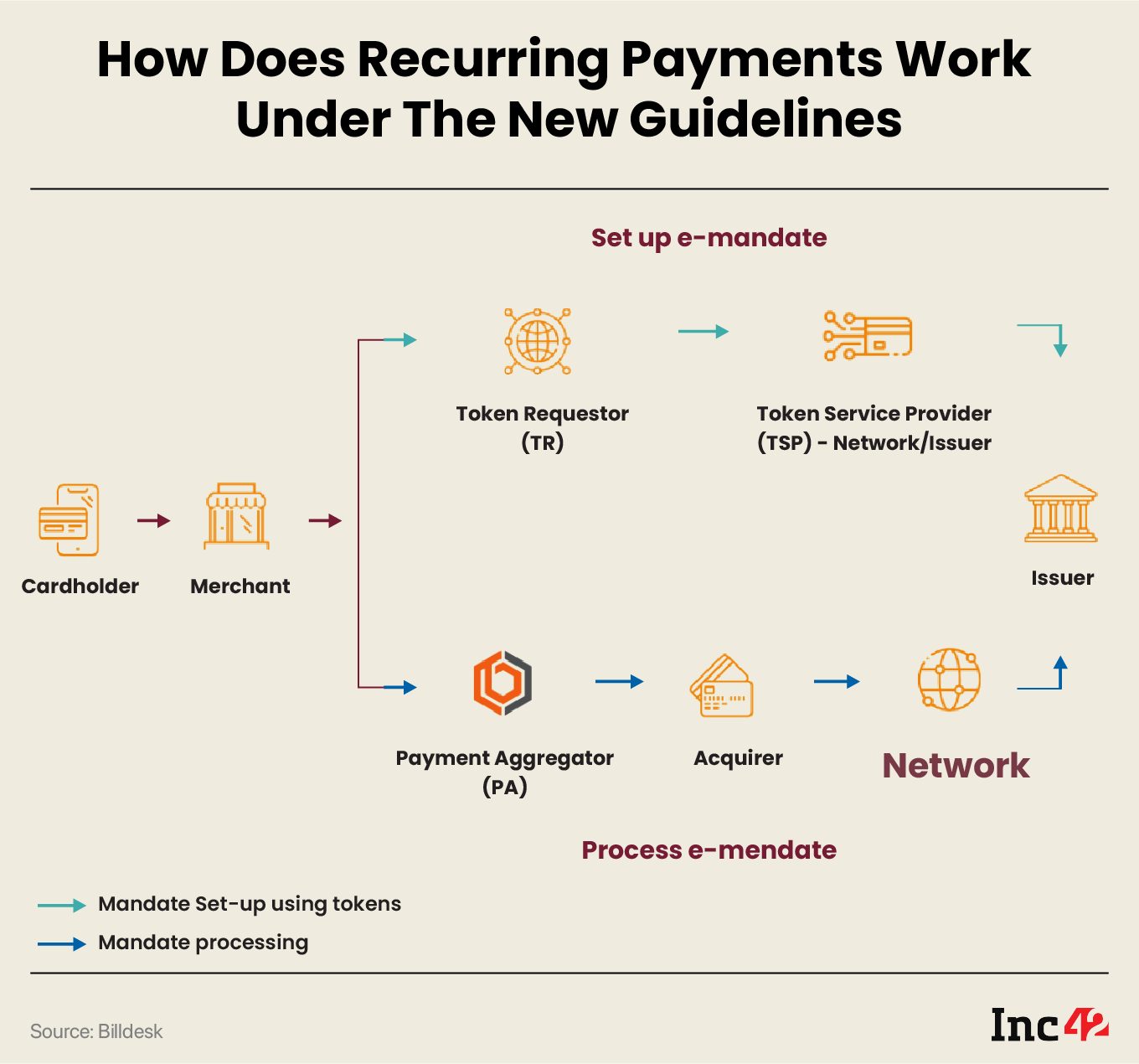

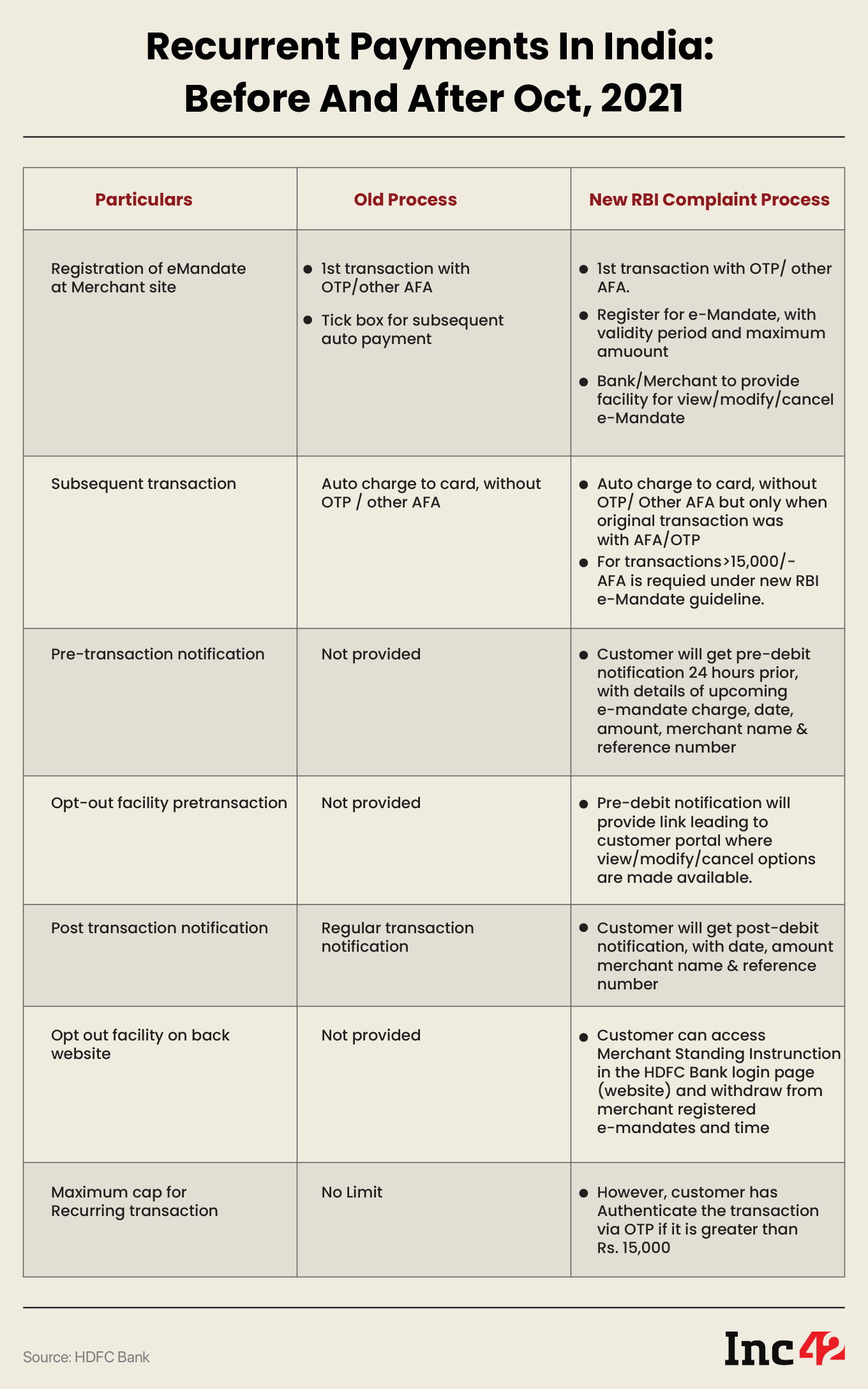

Simply put, the RBI wanted to introduce e-mandate guidelines, including additional security measures for recurring payments on India-issued credit and debit cards. UPI Autopay and NPCI eNACH were not impacted by these changes.

These measures say:

- Banks need to register cardholders and create an e-mandate through a one-time process, using additional factor authentication (AFA)

- Banks must alert cardholders at least 24 hours before charges take place and give them the ability to opt out of transactions

- Recurring transactions over INR 15,000 must go through AFA each time

What Changed After The Guidelines

In addition to this, the RBI also directed that from January 2022, no entity in the card payments chain other than card issuers or card networks will be allowed to store the actual card data. The central bank directed all entities, such as merchants, payment gateways, and PPIs to purge all the previously stored card data.

How The Well-Intentioned Move Backfired

The RBI’s Recurring Payments Guidelines and tokenisation move solved two big problems.

Firstly, they made online transactions a lot safer. In January 2021, it was widely reported that the card details of 10 Cr Indians were being sold on the dark web. The data was allegedly leaked from a compromised server of Juspay, the Bengaluru-based digital payments gateway. The tokenisation meant credit card data was no longer available with fintechs. Fintechs only had card details in an encrypted format that was unlocked for every transaction with a unique token.

Secondly, the RBI guaranteed that control remained with consumers. The AFA features, for instance, ensured no recurring payment transaction was happening without user consent. The guidelines put users at the helm, and in control of their future recurring payments. At any point in time they could cancel or edit their recurring payments. They no longer needed to reach out to each and every subscription platform for cancellations or modifications.

However, implementing the RBI’s guidelines had unintended consequences and backfired. The subscription market, which had been flourishing since the onset of the Covid pandemic, suffered immediate setbacks, with approximately 70% of recurring payments being declined, the very next month, as per reports and data that Inc42 has found.

Despite the RBI issuing these guidelines in 2019 and extending the implementation deadline by several months till October 2021, the banking and financial institutions as a whole were ill-prepared for the changes.

Unlike the NPCI’s eNACH, one recurring payments solution for all the member banks, under the RBI’s guidelines, the e-mandate was provided to individual banks separately. And, it is becoming more cumbersome to have a seamless experience when it comes to recurring payments.

Apart from SiHub, a platform co-developed by BillDesk and Visa Card that successfully onboarded leading banks like HDFC and SBI, most other banks and payment aggregators failed to comply with the guidelines, even six months after their release.

Razorpay and Mastercard attempted to address the situation by launching MandateHQ, another platform for e-mandates. However, it had limited participation from banks.

On October 1, 2021, Shashank Kumar, CTO of Razorpay, acknowledged the challenges in a tweet, stating that it would take three to six months for banks to integrate with MandateHQ and provide support for recurring payments to their consumers. While some banks managed to go live, others still required additional time.

Despite nearly two years to fix the problems, a significant number of subscribers continue to struggle with recurring payment options, especially when it comes to international platforms. For instance, Google, which offers various subscription services such as Google Cloud, YouTube Premium, and Google Workspace, does not offer auto-debit options for UPI and debit cards.

Gautam Pradhan, cofounder of Earthmetry, a data analytics firm, criticised the RBI’s move, describing it as “When you want to go from 0.0002% fraud to 0% and decide to upset 100% of the people.”

The guidelines originally intended to give consumers control and choice over their payments. However, the implementation has inadvertently restricted consumer choice and hindered payment flexibility.

Bharath Reddy, program manager of the Graduate Certificate in Public Policy (GCPP), at Takshashila Institution, highlighted the numerous challenges the RBI’s move created for businesses and customers. The most significant impact was the disruption in subscription revenue, particularly for media companies, OTT platforms, non-profits, and other entities that rely on monthly or periodic payments.

Reddy further noted that many companies, especially those without a substantial Indian customer base, have yet to comply with the guidelines. Most international merchants accept payments through credit cards or PayPal, neither of which is compatible with Indian credit cards. Consequently, Indian customers are limited in their payment options, resulting in a loss of choice for accessing certain products and services.

In summary, implementing the RBI’s guidelines had unintended consequences, leading to declined recurring payments in the subscription market. The lack of readiness among banks and financial institutions, along with limited compliance, has hindered consumers’ payment options and caused disruptions in subscription revenue for various industries.

Additionally, international platforms and companies without a significant Indian customer base have faced challenges in complying with the guidelines, limiting choices for Indian customers.

“The problem I have with the Reserve Bank of India is that they don’t appear to take into consideration the impact of their regressive regulations on merchants and consumers, and the increasing inconvenience this leads to. There was no impact assessment, no public consultation: just a diktat with a deadline, which eventually got pushed repeatedly because of lack of feasibility,” Pahwa said.

“We also have to take into account that the RBI has enforced these guidelines on credit cards, which have better customer service, fraud detection and accountability, and yet they’ve failed to do anything to enforce accountability in case of UPI, especially in terms of fraud detection and prevention. There’s a saying “if it ain’t broke, don’t fix it.” In case of the RBI, they broke something that was working — credit card payments — and have failed to fix something that is crying out loud for regulatory intervention — UPI,” he further elaborated.

Understanding The Indian Subscription Market

The subscription market in India encompasses various sectors, with utility subscriptions such as electricity, gas, cable, and internet being prominent. Additionally, there is a significant presence of B2B SaaS subscriptions, IT tools subscriptions, and subscriptions related to the media industry, including both print and digital media. Non-profit organisations like Alt News, Internet Freedom Foundation, and The Wire heavily rely on recurring transactions for their monthly or annual donations.

Regarding utility subscriptions, it is argued that the impact of the RBI guidelines was not substantial for the common man. According to the RBI, individuals in the lower-middle-income category in India pay an average of 42 utility bills per year, of which only three are typically paid online.

But India’s media and entertainment (M&E) market experienced grave challenges in its growth rate. The M&E sector includes segments such as OTT platforms, television, podcasts, online gaming, and digital media subscriptions.

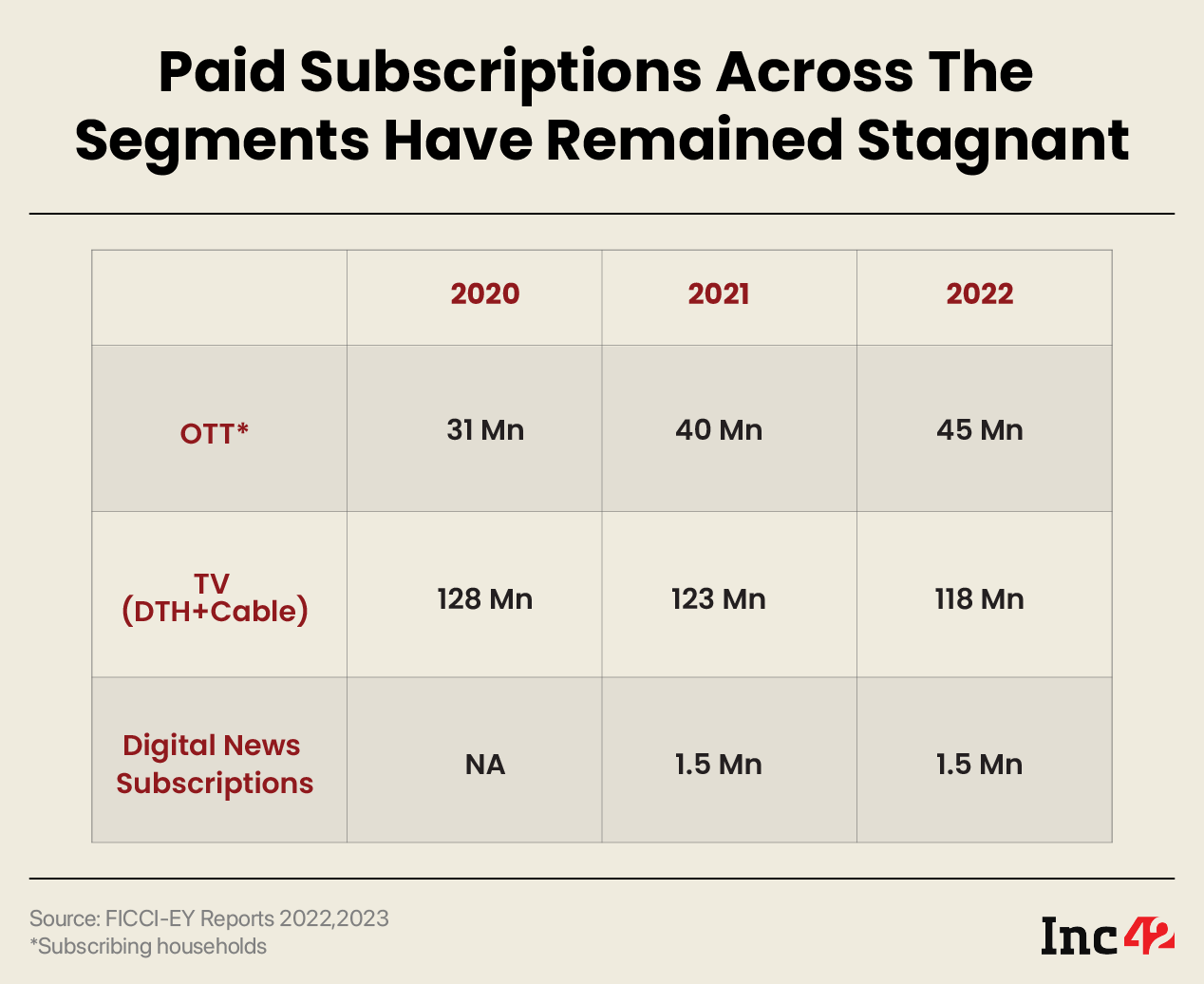

As a result of the guidelines, there was a reduction of around 5 Mn TV subscriptions as per data sourced by Inc42, and the growth rate of OTT subscriptions slowed down.

FICCI-EY, in its 2022 report, initially projected a Compound Annual Growth Rate (CAGR) of 24% for digital subscriptions until 2024. However, this has now been trimmed to 11% CAGR until 2025. Similarly, the estimated number of OTT subscribing households has been adjusted from 60 Mn in 2024 to 52 Mn in 2025.

While various factors could contribute to these figures, analysts believe that recurring payment issues are one of the key reasons behind the lacklustre numbers.

In the case of B2B subscriptions, although the overall businesses may not have been impacted due to the essential nature of their services, payment failures have become a major concern for both buyers and sellers.

Prashant Ganti, head of product management for Zoho Finance and Operations Suite told Inc42, “Most of Zoho’s monthly plans fall within this limit, so our customers on monthly subscriptions were not affected. For customers who exceed this limit, we offer them the option to prepay for a specific period upfront.”

The company also sent email notifications and personally followed up with customers as their subscriptions neared the expiry date. This approach helped it retain customers, Ganti claimed.

The RBI’s Take

Rebutting the criticism around the recurring payments guidelines, RBI Governor Shaktikant Das said in June 2022 that the rules prioritise user convenience, safety, and security. This was when the recurring payments limit was enhanced from INR 5,000 to INR 15,000 per transaction.

“Under this framework, over 6.25 crore mandates have been registered in favour of a large number of domestic and over 3,400 international merchants,” he said.

In December 2022, the RBI extended the scope of the Bharat Bill Payment System (BBPS), an ‘anytime anywhere’ bill payments platform, to include all categories of payments and collections, both recurring and non-recurring. It also brought in support for inbound cross-border bill payments.

BBPS has onboarded over 20,500 billers and processes over 9.8 Cr transactions monthly.

In January 2023, RBI Deputy Governor T Rabi Shankar highlighted that financial entities traditionally subject to regulation understand that regulation serves the larger objective of systemic stability and development. Entities outside the financial space are still learning to adapt to a regulated environment. Their initial reaction to regulation is often objectionable, even creating a narrative of customer inconvenience, sometimes echoed by industry bodies.

Shankar added, “The norms prescribed for recurring payments were criticised as inconvenient to customers until a survey revealed that more than 80% of customers welcomed the move. RBI’s approach to regulatory aversion is to patiently ease in regulations, allowing the ecosystem adequate time to adjust.”

Ram Rastogi, former head of products at NPCI, also acknowledged that there were some issues initially. However, with the revised system now in place, including card tokens and banks periodically sending the required messages, the guidelines are being perfectly followed.

“Various forums exist where grievances can be communicated with the RBI… The RBI is very open to industry feedback. I haven’t seen any other regulator being so receptive to criticism worldwide,” said Rastogi

What’s The Way Forward

While the RBI has been firm about its stand on the Recurring Payment Guidelines, Takshashila Institution’s Reddy believes that there is no data that these guidelines have benefited customers.

“We hear about a lot of people who have been inconvenienced by it, and it is not due to a lack of awareness. There are still a host of issues that need to be sorted before a seamless experience can be offered to the end users,” Reddy said.

Other industry players also chimed in with the major pain points:

- The guidelines have been very poorly executed, without RBI supervision. The central bank needs to ensure the guidelines be properly followed and communicated with consumers

- To streamline, all stakeholders involved such as payment gateways, card networks, and banks must support the capabilities required to enable additional authorisation for recurring transactions

- More power to consumers allowing them to select which transactions need to be automated and which needs to be monitored manually

- Lower-cost interventions, such as requiring banks to provide consumers with the ability to view and manage their subscriptions, might have also addressed the issue without as many disruptions

- Most of the banks’ websites do not show the e-mandate option prominently. Whether it is available for all their credit and debit cards as well as for the internet banking. This needs to change

“The RBI could also consider providing customers with more control over how their money is being collected. For example, allowing them to configure the terms of auto-debit transactions like setting the transaction limits for each vendor, and selecting which subscriptions can renew automatically without manual intervention,” added Zoho’s Ganti.

He believes this would not only provide customers with greater control but also reduce the need for manual follow-ups and minimise involuntary churn for businesses.

The global subscription ecommerce market value is expected to reach $904.2 Bn by 2026. Businesses have started recognising the value of establishing long-term customer relationships as this is the most sustainable way to ensure steady revenue.

“Since we will see more businesses adopting recurring revenue models, the RBI can listen to their feedback and explore opportunities that improve the ease of doing business while keeping customer security and our financial system at the core. By having the right system in place, businesses can achieve compliance and improve customer experience,” Ganti added.

Inc42 spoke to over a dozen founders to find out whether they have ever exercised their e-mandate on the SiHub or MandateHQ platforms. A whopping 80% of them said they haven’t.

Clearly, there is a greater need to sensitise the ecosystem and the fintech industry when it comes to the guidelines. But so far, with the disconnect between banks, tech giants and subscription economy platforms, consumers are still feeling the pain.