A look at the quarter-on-quarter numbers for Paytm vis-a-vis its merchants business indicates that a major problem is brewing for Paytm

The company saw a decline in loan value and the number of merchant transactions in Q4 FY24, and recovery is highly dependent on how the company restores the confidence of lending partners

Experts also believe that Paytm needs a leadership rejig to salvage its hot merchants loan business and get out of the cycle of degrowth

Paytm![]()

![]() is on the cusp of losing its lead in the merchant payments and lending business. Even though it has over 40 Mn merchants registered on its platform at the end of FY24, the company has seen a drop in the number of transactions, the merchant loan business and is at risk of losing out to the likes of PhonePe, BharatPe, Google Pay and others in this space.

is on the cusp of losing its lead in the merchant payments and lending business. Even though it has over 40 Mn merchants registered on its platform at the end of FY24, the company has seen a drop in the number of transactions, the merchant loan business and is at risk of losing out to the likes of PhonePe, BharatPe, Google Pay and others in this space.

A look at the quarter-on-quarter numbers for Paytm vis-a-vis its merchants’ business indicates that a major problem is brewing for the Vijay Shekhar Sharma-led company.

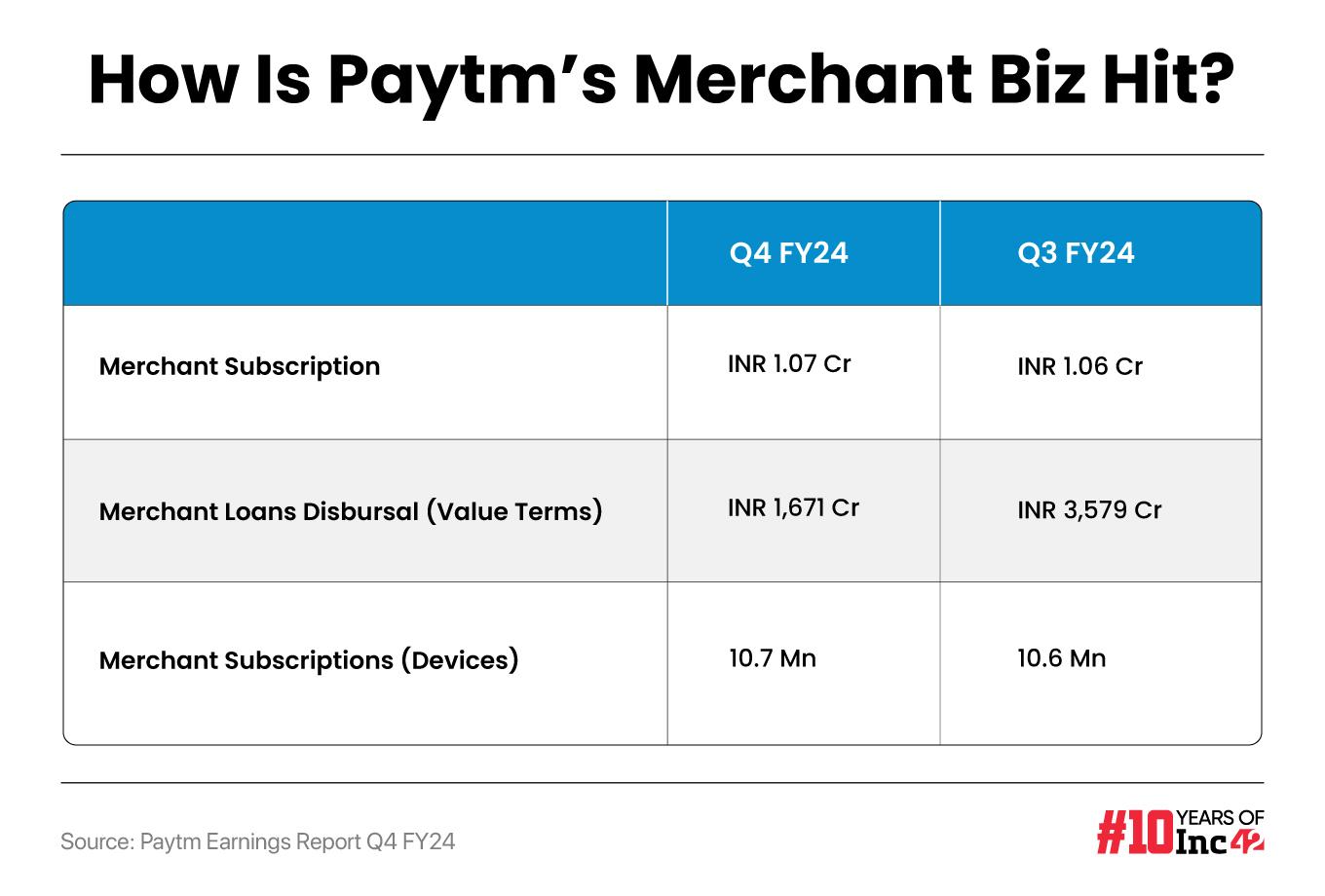

The number of merchants only grew marginally by 3%, the lowest sequential growth in all of FY24. Plus, the value of loans disbursed fell by 63% QoQ and 58% YoY, along with a 4% drop in merchant transactions. Further, the active device (PoS machines, soundboxes) base fell by 1 Mn in Q4.

And all the while, competition is snapping at the heels to grab market share at Paytm’s expense.

The numbers make for bad reading, but analysts told us that Paytm can expect several quarters of tepid growth even in FY25. Winning back merchants and most importantly the confidence of lending partners will be critical for Paytm’s merchant business to get back on track.

Losing A Major Advantage

“Without Paytm Payments Bank by his side, VSS has lost a significant advantage in this battle. It was vital for merchant retention since many of them had savings accounts with the payments bank, thereby allowing the company to more easily upsell loans and other products,” a former business head at an NBFC lending to Paytm told us.

The person added that while Paytm transitioned merchants to other banks in the past two months, this was enough time for rivals to poach some of these merchants for their own subscription services and devices.

Not only was Paytm impacted because of merchant attrition, but it also had to migrate the auto-repayment or NACH mandates for merchants who were repaying loans through Paytm Payments Bank account.

This also led to some fear among Paytm’s lending partners who are said to have deployed their own collections and recovery teams. Notably, out of 30 million merchants base on the platform, around 60 Lakh merchants had savings accounts with PPBL.

Paytm Walks Away From Loan Recovery

Those familiar with Paytm’s merchant lending business claim NBFCs and banking partners were concerned about Paytm’s ability to recover or collect the loans adequately.

In fact, the consequences of this are already evident in Paytm’s Q4 disclosures. Paytm said that it has ended the collections side of lending for postpaid and personal loans verticals and is reassessing collections on the merchant loans business.

Instead, the company will focus only on loan distribution and is adding partners only for this model. Under this model, Paytm will not earn any collection or recovery fee but will also have to bear lower risk if there are any defaults.

In this case, the lender collects, and therefore, Paytm does not have to allocate capital for loan default guarantees.

Several industry executives we spoke with told us that merchant loan collections had slid before the RBI’s action on PPBL earlier this year, and with the suspension of the payments bank, a major channel of EMI collections has been blocked.

Thanks to the Paytm Payments Bank licence, Paytm could sign up merchants with an ACH mandate for its in-house bank. This helped it easily recover loans through auto repayment of EMIs by merchants.

Paytm Payments Bank had 0.83 Mn ACH debit transactions in September 2023, which fell to 0.64 Mn in December and then was at 0.66 Mn in January and February 2024, before disappearing from NPCI’s data.

According to industry experts, having its own payments bank was an advantage for Paytm, as it allowed it to bargain with lenders for higher collection commissions. But this advantage disappeared after February 2024.

So when Paytm hit a pause on its merchant lending business in February and March, its lending partners immediately deployed their own teams for EMI collections.

“It was not just about loan disbursals anymore. RBI had cautioned banks, NBFCs on asset quality deterioration in December and all lending partners were doubtful of Paytm resuming its loan business. So they activated their field collection teams. Even a two-month pause in lending has a substantial impact on their revenue,” a fintech focussed VC and a former NBFC top executive said.

Another Pune-based NBFC executive told us that the pause in merchant loans not only hit collections, but also made them rethink their business relationships with Paytm, which found itself on the wrong side of regulations

This means even as it resumes its merchant lending business, Paytm is likely to have to settle for lower commissions from banks and NBFCs even for the loan distribution. And it is also foregoing the additional revenue of commissions on the collections side.

A former Paytm senior employee claimed the company was being seen as having a very risky borrower base or low asset quality and this impacted negotiations on commission rates with lenders.

To its credit, Paytm claims in its Q4 disclosures that, “Asset quality for merchant loans has remained stable as GMV on these merchants was not impacted as they were our most engaged merchants, and we prioritised them for retention.”

But other experts believe banks were already in an advantageous position in these negotiations and companies like Paytm stand to lose any leverage they have if there are issues in their operations.

“The larger scrutiny by the RBI on digital unsecured loans may cast some impact on the margins earned by LSPs [such as Paytm] and this will also increase the competition among LSPs as the NBFCs and banks have incrementally reduced the growth into the digital loans segment after regulatory action of increase in risk weights on these loans” said Anil Gupta, senior VP and co group head for the financial sector at the credit ratings agency ICRA.

Decline In Merchant Devices

What worsens things for Paytm is that it is seeing a decline in the active device base i.e official QR codes, PoS devices and soundboxes. While Paytm was looking to transition many of the merchants using these devices to other banks, this also complicates the future growth of the merchant loans business.

A merchant with an active device linked to a Paytm Payments Bank account is not only a prospective loan customer for Paytm, but also is easier to lend to since recovery or collections happened through the same PPB account.

“Many lending platforms don’t consider the credit history of the merchant or the business when disbursing loans. Instead, they focus on the sales or transactions on the PoS devices. This also helps them recover loans more easily. Consequently, as the disruption happened across Paytm’s QR codes and PoS devices, this in turn impacted EMI repayments,” the analyst quoted above told us.

They added that with fewer active devices with a deep transaction history, the number of potential merchants that Paytm can lend to in the future also shrinks. We are yet to see the impact of this change and it will only be clear after the first two quarters of FY25.

Paytm’s Leadership Vacuum

What doesn’t help Paytm is that negotiations with banks and the growth of the merchant business were dependent on business leaders who quit the company in recent months.

Paytm has seen a spate of exits recently, which include Ajay Vikram Singh (CBO of user growth and UPI), Bipin Kaul (CBO of the offline payments business) and Sandeepan Kashyap (chief business officer of the consumer payments vertical) and most importantly Bhavesh Gupta who was the company’s COO.

Chairman and CEO Sharma who has taken a more central role in recent weeks has hinted at the appointment of top industry executives at leadership positions.

“The biggest thing that I’ve learned is that many times your teammate and adviser may not be getting it correct. And it is important for you, yourself to be taking care of it versus just letting a teammate or an adviser suggest what it should be,” Sharma said in March 2024 months after the RBI’s action on PPBL.

Experts feel Paytm needs to bring on board some credible names in the finance industry to help the company return to its growth trajectory, and most importantly rebuild relationships with banks, NBFCs.

“It cannot be denied that Bhavesh Gupta, in particular, was instrumental in helping Paytm secure major lender partnerships. Even though the company is trimming down its workforce now, it has to bring in a replacement who is a reputable name in financial services and brings his own individual credibility to Paytm,” another top executive at a Paytm lending partner said.

Paytm said its focus will be on corporate governance with the appointment of subject matter experts as advisors or independent directors to ensure the right leadership for corporate governance.

But the fresh leadership will also have quite a task on its hands even beyond governance. Paytm needs to win back the confidence of merchants, lenders and while it does so, the payments business has to pick up the slack. Here too, the company faces tough competition from well-entrenched players.

The super app formula will be critical for Paytm to improve its revenue mix and extract as much revenue as it can from each user, but the likes of PhonePe, Google Pay, Groww, CRED and others are also vying for the same piece. Can Paytm find its lost spark in FY25 and regain its lead in the fintech race?

[Edited by Nikhil Subramaniam]