Acquiring businesses like Happay and Kuvera helps expand CRED’s product portfolio in the long run and enables it to acquire customers beyond the ‘exclusive’ CRED Club

Currently 11 Mn CRED members use the platform for the monthly card bill payments and UPI payments while over 4 Mn vehicles are parked on CRED Garage, which was launched just last year

To mitigate the risk of market saturation and high CAC, CRED is working on five key areas to diversify its revenue channels, attain sustainability

The number of credit cards reached 100 Mn in 2024, a 400% jump from 20 Mn in 2014 to over 102 Mn by April 2024.

Despite a remarkable rise in UPI payments due to the digital payment platform’s speed and convenience, India’s credit card market has not taken much of a hit. For instance, the total number of credit cards rose to 10.18 Cr in FY24, compared to 8.53 Cr in the previous financial year (a 19% jump), according to the RBI.

Similarly, YoY credit card spending in FY24 surged by 27% to reach INR 18.26 Lakh Cr compared to nearly INR 14 Lakh Cr in the previous financial year. The reason: The growing adoption of digital payments across Bharat since the Covid-19 pandemic and rise in discretionary spending in metros and beyond.

Given these trends, credit cards remain a small but premium and most lucrative segment to cater to. However, in a seemingly counterintuitive approach, most Indian banks and NBFCs continue to focus on the lending market for two primary reasons.

First, the loan market (both secured and unsecured) is much bigger. Second and more important, credit cards incur high operational costs involving reward programmes, fraud protection, customer services and more. Also, small sellers are unwilling to accept payments via credit cards as they are liable to pay a merchant discount rate (MDR) amounting to 1-3% of the transaction value.

The small percentage of credit card users in India poses another hurdle. According to the Federal Reserve data, 82% of U.S. adults had credit cards in 2022. In contrast, 5.5% of Indians hold credit cards, according to latest industry estimates.

On the other hand, popular loan products like personal loans or even very short-term loans (think of payday loans) for emergencies are quite straightforward in structure and operational costs are typically less. Therefore, most fintechs partner with banks and NBFCs to cater to the loan market. However, with the RBI keeping a strict vigil on lending norms, KYC and advanced security measures, many are now compelled to look beyond lending.

To be sure, a few fintech platforms have entered the credit card market with co-branded cards, BNPL (buy now, pay later) offerings and hassle-free credit card bill payments. But none managed to stand out except the fintech unicorn CRED, a member-only app that exclusively services credit card holders with a credit score of minimum of 750.

Set up in 2018 by Kunal Shah, Cred![]()

![]() aims to provide a premium experience to credit card users through a range of exclusive products and services. Not Everyone Gets It, says its tagline, amply illustrating the unique concept driving its business vision.

aims to provide a premium experience to credit card users through a range of exclusive products and services. Not Everyone Gets It, says its tagline, amply illustrating the unique concept driving its business vision.

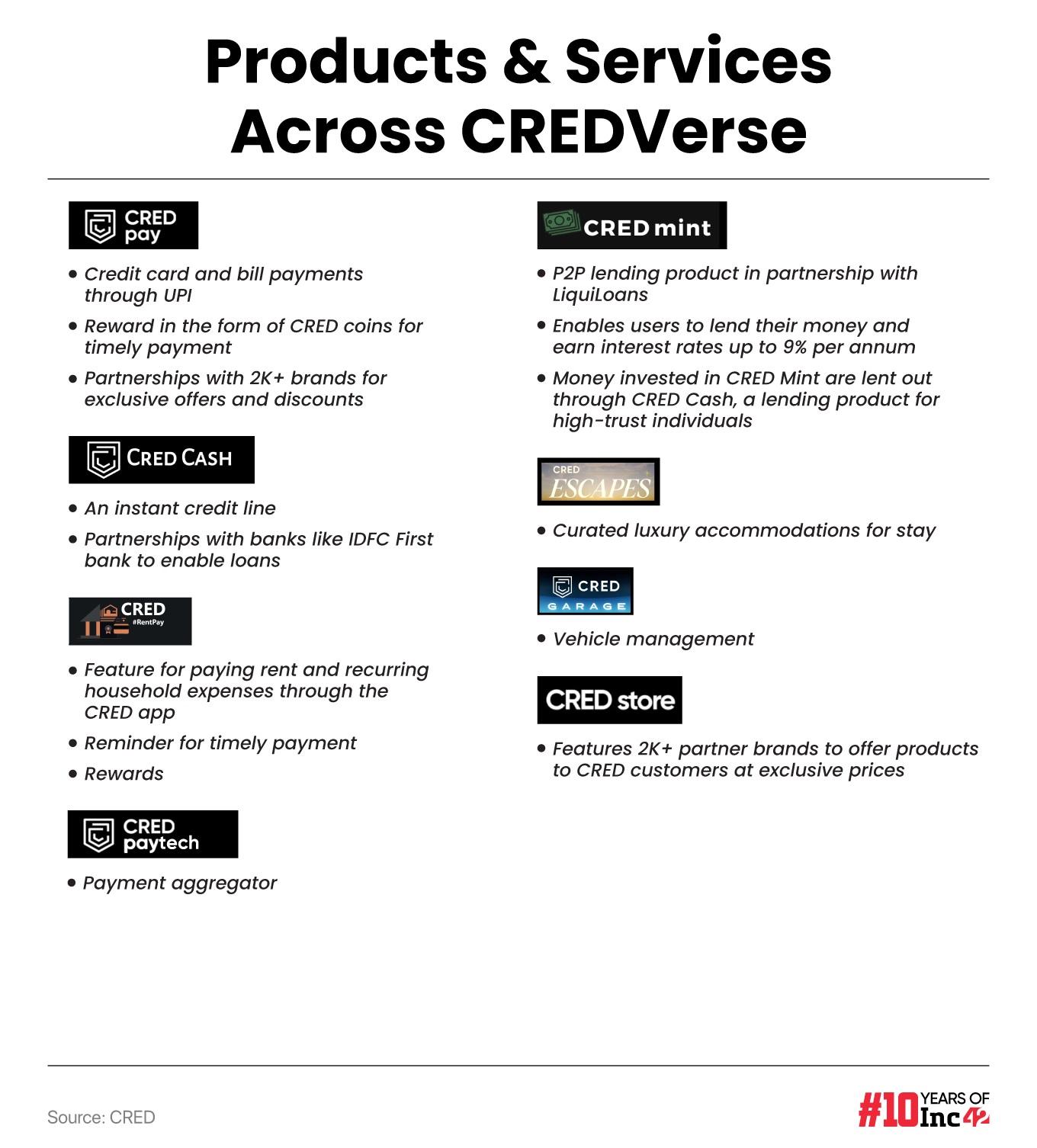

Besides its routine offerings, CRED has introduced a host of value-added services over the years, such as CRED Cash and CRED Mint, CRED UPI (integration with the UPI platform for secure transactions by generating UPI codes), Tap to Pay (NFC-enabled instant payment by tapping one’s smartphone on a merchant’s PoS device) without requiring any physical card and CRED RentPay, with provision for setting up auto-payment.

The platform has recently launched a bouquet of services such as Garage, a vehicle management platform to keep track of car spending and enable Fastag recharge for toll payments, and Escapes, a selection of curated accommodations for specific destinations, diverging from its pure-play financial offerings.

In 2023, CRED acquihired Spenny, a microsavings platform that helped people save and invest tiny amounts in mutual funds and digital gold. Earlier this year, it also acquired online wealth management platform Kuvera in a cash-and-stock deal. Additionally, the fintech platform has obtained in-principal approval from the RBI to operate as a payment aggregator. It has also set up a Dreamplug AA Tech Solutions subsidiary and intends to acquire an account aggregator licence.

For context, PAs are third-party service providers enabling customers and businesses to make and receive payments online. On the other hand, account aggregators (AAs) are RBI-regulated intermediaries with NBFC-AA licences, enabling financial data-sharing between financial information providers (FIPs) and financial information users (FIUs) within the AA network.

For instance, the AA ecosystem can help a lending bank (FIU, in this case) access the financial data of a potential borrower from another bank where the person has an account (here, the bank where the borrower has an account is the FIP). All data is accessed and shared securely and digitally, but no data-sharing is possible without the account holder’s digital consent (more on CRED’s role as a PA and a potential AA later).

Talking of numbers, currently 11 Mn use the platform for the monthly bill payments of their credit cards and UPI payments. Over 4 Mn vehicles are parked on CRED Garage, which was launched just last year.

A Close Look At CRED’s Design Thinking For Product Development

Considered quite a business buzzword nowadays, design thinking is all about an iterative process that dives deep into customer requirements, goes beyond conventional assumptions and comes up with innovative solutions.

When quizzed about CRED’s design thinking approach, a former senior executive explained it candidly. “Take a look at Microsoft. Its operating system is hugely popular, commanding 72% of the [laptop] OS market, while Apple’s macOS accounts for 14.73%. Similarly, Google’s Android OS dominates the mobile space with more than 70% of the market share compared to Apple’s 28%. Yet, Apple’s revenue surpasses Google’s parent Alphabet and Microsoft by 40% and 120%, respectively. That’s because Apple has better identified their potential consumers and focuses on offering experience, while others focus on products.”

According to the former exec, Shah is pursuing a similar approach for CRED.

The company has identified its user base — affluent and trustworthy Indian consumers. The design thinking is to enable financial progress for the trustworthy with products that improve their lives and lifestyles.

And, perceiving credit cards and credit scores — a metric for trust — CRED launched the first product as credit card bill payment. This included reminders to pay bills on time, insights into their card usage patterns.

Further to reward financial prudence, CRED came up with a host of instant gratification instruments including coins, cashback, merchant offers, vouchers for bill payment, as well as access to a curated selection of premium experiences across lifestyle products and travel. CRED Escapes and Store have been further designed to drive engagement and reward members for financial prudence with unique offers.

Garage has similarly been launched to serve their members’ vehicle-related needs. A platform where members could pay challans, recharge FAStag, and renew insurance policies, all on CRED.

CRED has its challenges, though, including market saturation and increasing customer acquisition cost (CAC). Consider this. According to the CRIF High Mark report, among credit card holders in the youngest age bracket of 18-25 years, 81% have one credit card, 12% have two cards, 3.6% have three cards, and 2.4% have more than three cards. Hence the total number of credit card holders indeed is less than 100 Mn.

Now CRED has already acquired over 11 Mn users and given its credit score cut off 750 (significantly higher than 650, minimum to have to qualify for credit cards), bringing the rest to its fold could be a near-impossible task. Even if it is theoretically possible, one simply can not afford to spend a huge amount on customer acquisition to capture the market.

To mitigate such risks and overcome other business hurdles while aiming to attain long term sustainability, CRED has been working on five areas mentioned below:

- Building a unique portfolio of products: Instead of creating entirely new products, CRED aims to offer unique experiences by enhancing existing ones. Take, for example, the design makeover of CRED UPI during this cricket season. The cricket edition flaunted a rhodium-toned interactive skin, resembling the look and feel of a premium credit card or a designer wallet. Along with that came mega rewards for consecutive transactions and luxury drops at select locations across India to ensure that such lifestyle upgrades become valued experiences which go beyond transactions. Garage and Escapes are other additions to its benefit-first product portfolio.

- Developing multiple revenue streams: As per FY23 financials, currently 90% of its revenues come from Cred Cash or personal loans, utility bill payments, Cred Max and insurance services. The company hopes to channel new avenues of income through businesses acquired by CRED but run independently (like Kuvera), as well as from PA fees.

- Reducing costs: CRED constantly evaluates its operating expenses to keep tabs on cash flow and stay cost-efficient. It has also handed out pink slips multiple times despite a 3.5x rise in revenue to INR 1400 Cr in FY23. Access to a PA licence will further help reduce costs.

- Building compliance and long-term trust: CRED aims to build a trusted ecosystem by obtaining licences from major regulatory bodies like the RBI, SEBI and IRDAI and strictly adhering to all compliance norms.

- Working on IPO plans: CRED is reportedly accelerating its IPO plans and may file the DRHP as soon as it reaches breakeven. An initial public offering is the best way to raise funds to reduce debt burdens, acquire target companies and pursue long-term goals. Again, a publicly traded company is trusted more by all stakeholders. However, the IPO exercise will be more challenging than it seems initially; the devil is in the details.

CRED’s Kuvera Move Will Drive Horizontal & Vertical Growth

As the UPI ecosystem evolves, fintech companies seek to generate multiple revenue streams through cross-selling. Whether it is Paytm, Google Pay, PhonePe or Amazon Pay, cross-selling has become the critical focus of these apps, leading to stiff competition.

With a vast UPI consumer base on board, every fintech platform wants to get into lending and investments to increase its revenue. But now that the RBI is zealously monitoring all lending operations, UPI platforms tend to focus on wealth management. CRED is also moving into this space, but with a difference.

“CRED faces limited competition compared to Paytm Money, PhonePe and Groww, as it aims to monetise a high-quality customer base and emulate the profitability achieved by wealth management platforms like Zerodha and Groww,” said Ankur Bansal, cofounder and director of Blacksoil Capital, a Mumbai-based financial services provider.

The acquisition of the wealth management platform Kuvera syncs well with this purpose.

Kuvera, with assets worth $1.4 Bn+ under management for its 300K users, has become a preferred platform among India’s affluent investors. The average SIP size on Kuvera has reached INR 5K, twice the industry average, while total mutual investment amounts exceed INR 12 Lakh ($14,450), five times higher than the norm.

Kuvera, thus, fits into the CREDverse in terms of target customers and value creation. The acquisition also aims to fulfil the following short-term and long-term goals.

- Customer acquisition beyond CRED: According to a CRED statement, Kuvera will continue to operate independently and serve beyond CRED members.

- Vertical integration: CRED needs to cater to its users’ wealth management needs. Kuvera, with SEBI’s Investment Advisor (IA) licence, offers the opportunity to enter this segment.

- Speed up operations: Acquiring a licensed entity eliminates the need to meet compliance requirements and undergo long waiting periods.

While the acquisitions of Kuvera and Spenny add to CRED’s curated user base, there are more advantages.

“The existing user base, which manages their credit cards and expenses via the CRED platform, may prefer to consolidate their financial activities under one roof, thereby allowing CRED to gain some mileage and catch up with Zerodha and Groww,” observed Kalindhi Bhatia, partner at BTG Advaya, a leading transactional law firm based in Mumbai.

But there is another glitch. By acquiring licensed entities, CRED may have avoided the extensive scrutiny and long wait periods involved in setting up these businesses. However, from an ongoing compliance standpoint, the platform has to follow various sector-specific regulations. For instance, SEBI regulations are there for stocks, mutual funds and financial advisory; IRDAI looks after insurance, and the RBI monitors payment aggregation, KYC and more. So, it can still be an uphill task for CRED to comply with multiple requirements from the get-go, added Bhatia.

How CRED’s PA Licence Will Bring Value, Increase Revenue

Third-party payment aggregators are costly affairs, to say the least. PAs usually charge 1.75%-4% per transaction as processing fees, in addition to set-up costs and annual maintenance fees.

“The payment aggregator licence will allow CRED to leverage its payment processing services for partner brands and third-party merchants. Of course, the play here lacks clarity as the PA sector is now saturated. But it will help CRED reduce external costs incurred by relying on third-party PAs as and when required,” said Bhatia.

Currently, CRED’s partner brands are responsible for paying the PA charges, as the fintech platform does not offer these services or cover these costs.

Now that CRED’s wholly owned subsidiary Dreamplug Paytech Services has been granted in-principal approval for the PA licence from the RBI, merchandise costs may likely to go down and the platform can leverage a brand new revenue channel.

“A PA licence enables direct payment processing, enhancing the platform’s offerings like CRED Pay and CRED RentPay. However, it comes with regulatory challenges, including strict monitoring and compliance, similar to what Paytm has undergone. In case restrictions are slapped on a business, they can impact innovations and product scope,” said Abhinav Paliwal, cofounder and CEO of PayNet Systems, a white-label neobanking software platform catering to new-age fintechs.

Nevertheless, the PA licence will be instrumental in trust-building, user base expansion and brand positioning. There can also be a possible shift in branding – from ‘exclusive’ to ‘more inclusive’ – while retaining the premium service aspects, he added.

Account Aggregator Licence For Seamless Operations

To break new ground, CRED reportedly had plans to obtain an account aggregator (AA) licence via Dreamplug AA Tech Solutions. As explained, the AA framework helps simplify financial services like loans and credit facilities by providing a fast, comprehensive and transparent way to share verified financial data among regulated entities.

According to sources close to the development, the company has not applied for the AA license yet. “Our approach to licences is to apply for those that will enable us to provide a better member experience while remaining compliant with the letter and spirit of regulations,” said a company official without wanting to be named.

As CRED is now involved in business operations regulated by the RBI, SEBI and IRDAI, acquiring an AA licence is required to ensure a seamless experience across its products and services. In simple terms, an AA licence will enable CRED users to consent to data sharing without investing time and effort to provide all essential details whenever the need arises.

“Instead, CRED’s subsidiary will enable secure financial data sharing and boost capabilities in service areas like CRED Mint,” said Paliwal of PayNet.

Pratekk Agarwaal, founder and general partner at GrowthCap Ventures, a Mumbai-based early stage VC firm, noted that obtaining these licences would strengthen CRED’s fintech portfolio and regulatory compliance. However, exploring synergies and optimising customer journeys to enhance user engagement would be essential, given its reliance on partner channels.

Bhatia of BTG Advaya underscores yet another point. With these licences in its kitty, it looks like CRED intends to validate a user’s financial credentials internally rather than relying on external agencies. Since the platform enables lending services and payment gateways, it can carry out stipulated KYC verifications and assess a user’s financial rating pretty swiftly.

CRED Is Building The Top 1% Club; Here’s A Glimpse Of What To Expect

Popular opinions and market research data often highlight that the larger the TAM (total addressable market), the bigger the growth opportunity. However, CRED has changed tack. Instead of exploring the untapped market for humungous growth, it has been focussing on members’ requirements to build new value propositions for its curated community.

A former CRED executive, quoted earlier in this article, concurred.

“Take Garage, for instance. More than 70% of CRED members might own vehicles. Hence, they must analyse and understand what they spend on their vehicles. CRED has made it extremely convenient by putting all relevant data in one place. Your FASTag payments are here. You get to know the last servicing cost and how much you spend on your vehicle every month. Is your car leaking money? This is crucial as you no longer have to feed the data separately to manage your vehicle expenditure,” he added.

Similarly, there is Escapes, another feature to help members with their travel plans. Almost all CRED members travel at least twice a year. Of course, critics may say that the fintech is deviating from its business model but that is not the case. CRED is simply catering to what its members like to have on the platform, the executive said.

However, cross-selling does not always work.

According to Bansal of Blacksoil Capital, a consumer’s preference will be the deciding factor here. For example, most users are accustomed to using traditional OTAs like MakeMyTrip or EaseMyTrip, and many will be using corresponding co-branded credit cards. In such a scenario, CRED may not expect significant cross-selling on Escapes, at least not initially. But even a small income will keep the vertical sustainable, as CRED will not acquire physical assets (like hotels) to keep it going. Instead, the platform hopes to drive Escapes engagements with rewards, vouchers and the luxury experiences it offers.

Paliwal from PayNet assumes that CRED may attempt to cross-sell its new products to existing users and ensure that its acquired customer base uses its current offerings. (Data usage in such cases must comply with applicable privacy laws.) Presumably, the idea is to emerge as a one-stop shop for all things finance, from managing expenses to making payments to wealth management and more.

All these are for the top 1%, of course. But there could be exceptions.

Although the platform has set ‘Brand CRED’ apart as exclusive, it is now allowing certain acquisitions to run independently and making their offerings more inclusive to drive customer acquisition and build a large consumer base.

Interestingly, CRED struggled initially for keeping its offerings too limited, which did not resonate well with early users. Soon, however, it learnt to broaden its service horizon and introduced more substantial offerings, such as managing one’s entire bunch of bills more efficiently without missing a single payment date. In other words, it turned to ‘convenience’ to carve its niche despite the ‘exclusivity’ tag. Now, standing at the crossroads, is it taking a page out of its old playbook again to sprint ahead?

“There seems to be a shift in the business approach compared to its original offering. Think of the first tagline – linked to a user’s creditworthiness. If CRED executes this phase well and becomes useful to customers [rather than being just another product in the market], its new tagline should be: Everyone must get it,” said Paliwal.

Will There Be Hurdles Ahead As CRED Expands?

Whether it is Happay (a corporate expense management platform), or Kuvera, CRED is not only diversifying its revenue streams through multiple offerings but also allowing other brands to grow independently. This further ensures risk diversification, a necessity in a post-pandemic landscape impacted by a prolonged funding winter.

Additionally, regulation and compliance issues continue to impact fintech platforms, and handling belligerent customers turns out to be difficult. Last year, when Happay corporate cards issued by SBM Bank (India) were unexpectedly blocked from the midnight of March 31, several users took to X (formerly Twitter) and criticised the business for its poor communication policy. However, the incident took place mainly because the bank failed to update its KYC details in sync with the RBI’s guidelines.

It did not impact Brand CRED, but it certainly revealed the kind of turbulence a fintech company might suddenly face.

Under regulatory scrutiny, it may not be a smooth journey ahead for CRED. However, analysts believe that CRED is better equipped to tackle regulatory hiccups than Paytm, which slipped on KYC compliance. In fact, it is the sheer volume that often makes the difference. Paytm faltered trying to manage more than 300 Mn users. But for CRED, it will be just 15 Mn, a more manageable number.

Considering the impact of regulatory challenges on fintechs like Instamojo, Paytm, Slice and many others, would it also be an issue for CRED?

Bansal thinks fintechs must be ready to plug every possible loophole. “While building a fintech brand, you can’t shy away from regulators for long. It will not help the brand grow. It is only natural for CRED to seek regulatory compliance to incorporate more products and services and build user trust. Razorpay has also gone through similar cycles. So, regulatory compliance will be part and parcel of a business if it wants to be part of a new asset class. However, CRED has acquired a fresh set of businesses and managing them is easier said than done.”

As CRED strives to balance exclusivity, a broader customer base and a diversified product portfolio through strategic acquisitions, it has positioned itself as a versatile fintech company. However, the real test lies in preserving its premium brand identity while navigating the intricacies of regulatory compliance and diverse market demands.

[Edited by Sanghamitra Mandal]

Update | May 29, 2024, 13.40

The total number of CRED members has been updated based on further input from the company.