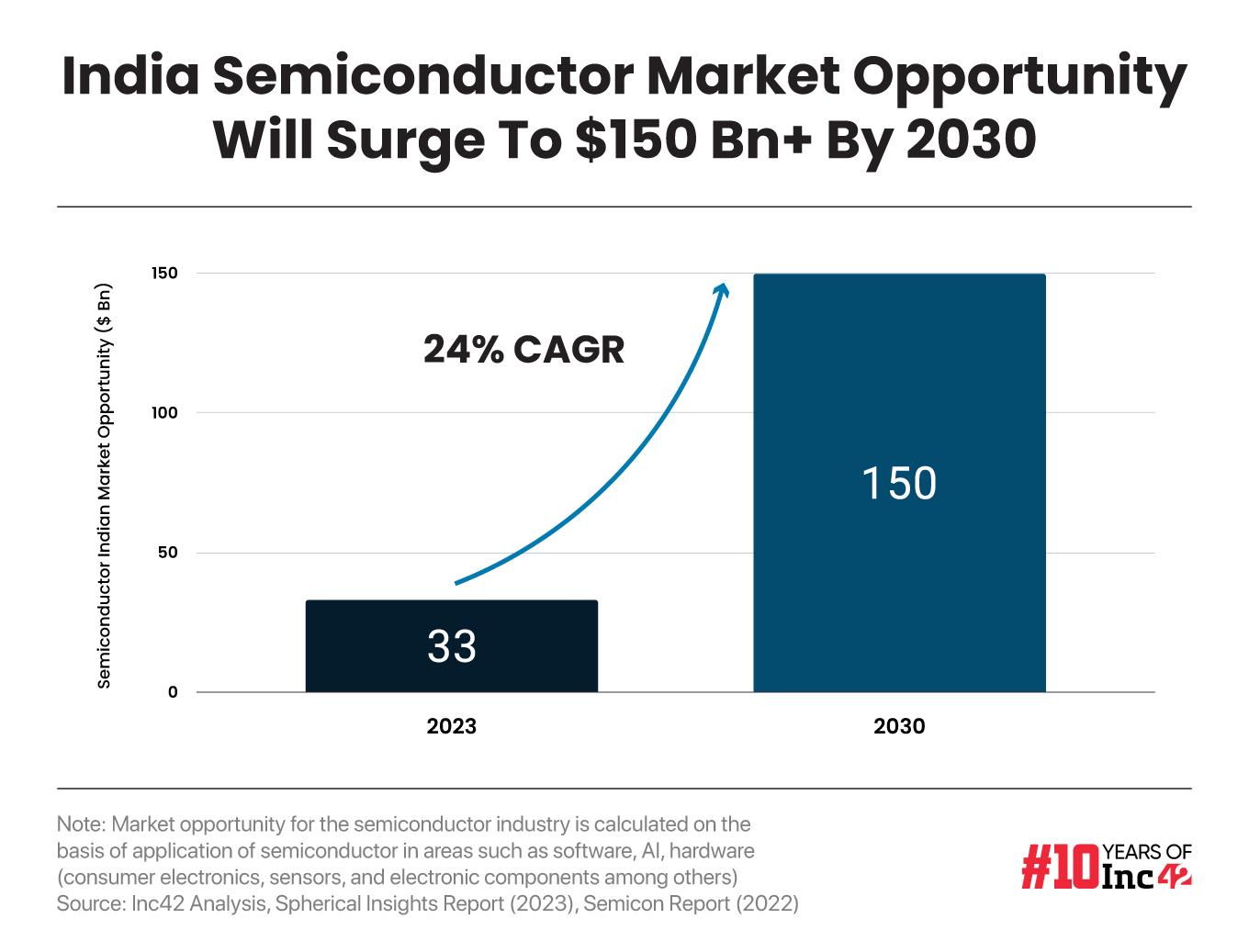

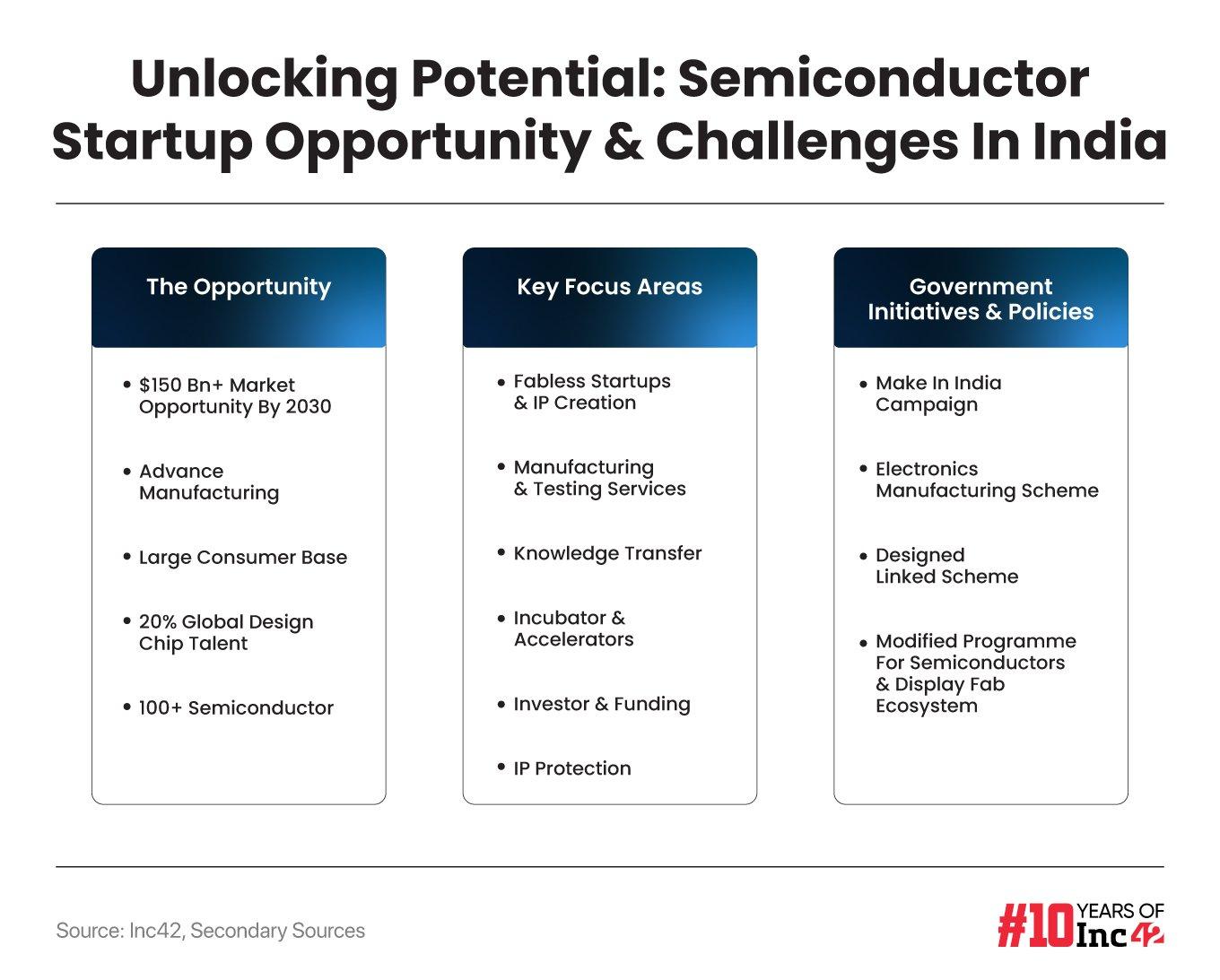

According to Inc42’s report, “The Rise Of India’s Semiconductor Startups Report 2024”, the country’s semiconductor market will witness an impressive CAGR of 24% during 2023-2030

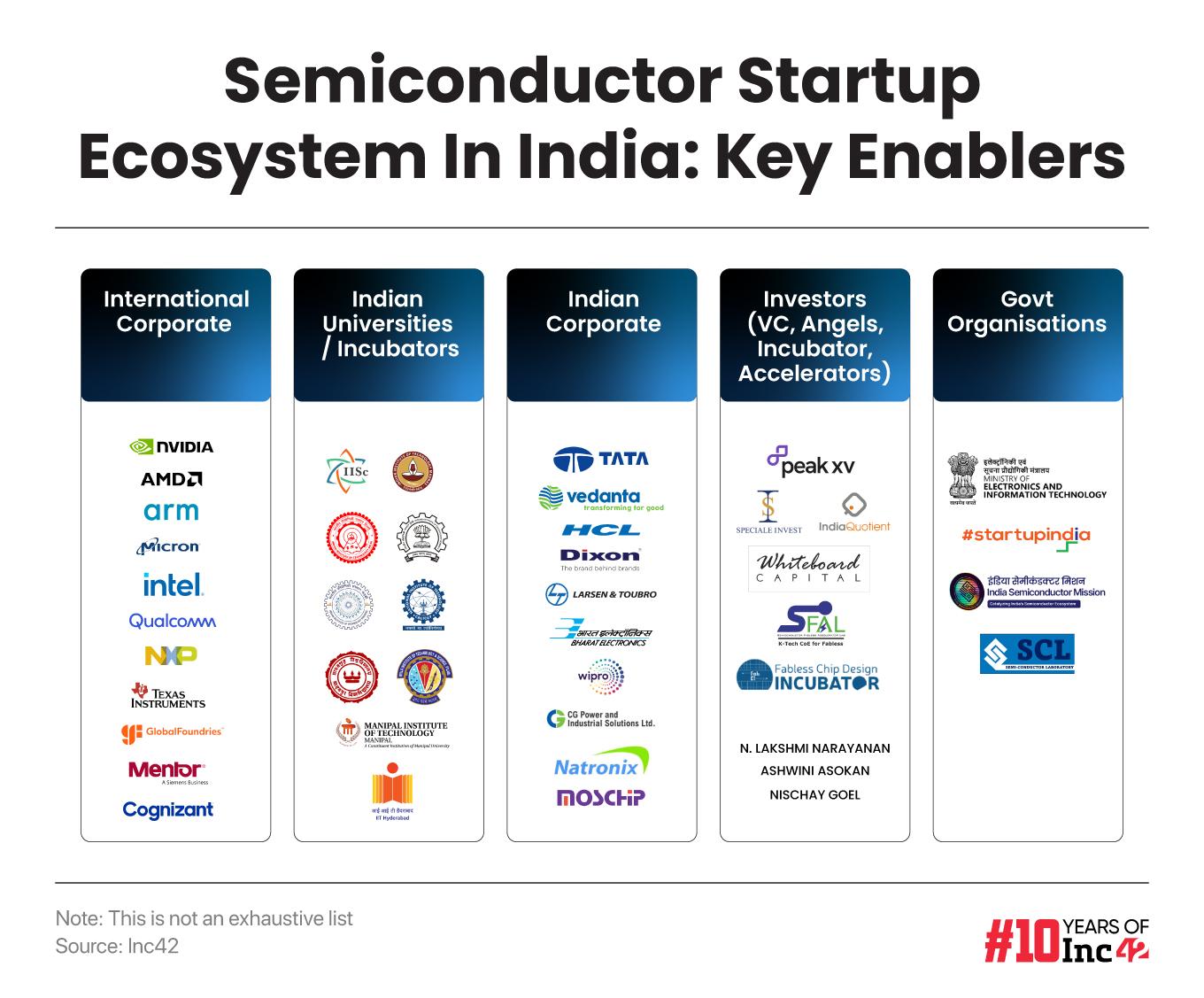

The ecosystem has seen the rise of 100+ startups across the stages and in critical domains, including AI semiconductors, industrial automation, consumer electronics, automotive, telecom and wireless communication

Poor infrastructure, delayed tech adaptation, low demand, lack of high-quality talent and lack of capital were some of the major challenges the Indian semiconductor industry had faced

In 1999, the Tata group considered selling its car business to Ford. The latter dismissed the idea, saying it would be doing the Indian conglomerate “a favour” by purchasing the business. The Tatas called off the deal but in 2008, acquired Jaguar Land Rover from the iconic automaker for $2.3 Bn, elevating India’s position in the global market.

More than a decade later, India once again witnessed the corporate house making a firm stride to lift the country’s semiconductor industry.

On March 22, 2024, the Tata group announced setting up a semiconductor ATMP (a combination of assembly, testing, marking and packaging) worth INR 27K Cr in March 2024 Assam. In February, Tata Electronics (TEPL) also received approval to build India’s first AI-enabled semiconductor fabrication facility in Gujarat’s Dholera.

TEPL is developing the project in collaboration with Powerchip Semiconductor Manufacturing Corporation of Taiwan (officially, the Republic of China), investing about INR 91K Cr in the fab and creating more than 20K jobs.

However, the Tata group is one of many players in the semiconductor space. The Vedanta Group is also building a chip foundry in Dholera and India-based SaaS MNC Zoho recently announced its plans to launch a commercial semiconductor manufacturing unit in Tamil Nadu. In early 2023, the US-headquartered Micron Technology said it would build an INR 22K Cr semiconductor testing and packaging plant in Sanand, Gujarat.

The list gets longer. However, global automotive giant Tesla’s strategic pact with TEPL for sourcing semiconductor chips has positioned the country as an emerging force to reckon with. But the question is: Why are domestic and international players bullish on India’s semiconductor story, a sector largely monopolised by Taiwan, Japan, the US and South Korea? This is all the more pertinent as India was a laggard here long after its independence.

Simply put, it is about finding capable industry players who can meet the growing demand in a global market.

According to a March 2024 report by Visual Capitalist, Taiwan had a 68% share in 2023, followed by South Korea (12%), the US (12%), and China (8%) in advanced foundry capacity (manufacturing of semiconductor chips). Whereas India’s share was miniscule in comparison.

However, Taiwan’s dominance is expected to shrink by 2027, with countries like the US and Japan investing more in domestic fabrication. Besides, global companies are also planning to fund semiconductor fabs, making it a $1 Tn opportunity by 2030. The shift in global sentiment and investment patterns may bring new opportunities to India as it tries to establish itself as a significant player.

Inc42’s report, “The Rise Of India’s Semiconductor Startups Report 2024” estimates that India’s semiconductor market will reach $150 Bn by 2030, up from $33 Bn in 2023, witnessing an impressive CAGR of 24%.

“There has always been a talent advantage for India on the global stage, whether in design or engineering. This advantage, honed in the software industry, can now be leveraged in the semiconductor sector. Therefore, there is substantial potential for Indian startups to capitalise on,” Haresh Abhichandani, managing director at Millennium Semiconductors told Inc42.

The Making Of An Indian Chip: A Saga Of Five Decades

India formally entered the semiconductor space in the mid-70s when the Union Cabinet, chaired by then Prime Minister Indira Gandhi, approved a proposal to set up the Semi-Conductor Laboratory (SCL), an autonomous body currently operating under the ministry of electronics and information technology (MeitY). However, Continental Device India (CDIL) is the country’s first private-sector semiconductor manufacturer.

It was launched in 1964, collaborating with Continental Device Corp. of Hawthorne, California. Around the same time, Bharat Electronics (BEL), a public sector undertaking under the ministry of defence, started developing semiconductor devices.

Speaking to Inc42, Prithvideep Singh, general manager at CDIL, said that India was home to many semiconductor companies until the mid-90s. Additionally, the country boasted a robust ecosystem of electronic equipment manufacturers, with companies like Onida, Videocon and BPL emerging as front-runners.

The global landscape changed when the World Trade Organization’s (WTO) Information Technology Agreement (ITA-1) came into force. The agreement eliminated all import duties and other charges on IT and semiconductor products, compelling India and other nations to compete globally rather than regionally.

Again, other nations typically provided massive subsidies and grants to bolster their semicon ventures. But that kind of state capitalism was not practised in India until the government introduced the India Semiconductor Mission (ISM) in 2021 as a nodal agency, with an outlay of INR 76K Cr to revitalise the semiconductor ecosystem.

In addition, the government has set aside INR 1K Cr to fund semiconductor design startups, and states are likely to contribute substantially. The government has also committed $30 Bn in electronics and semiconductors, of which $10 Bn would be allocated for semiconductor manufacturing research and design.

MeitY also introduced a design-Linked incentive (DLI) scheme in December 2021 to support domestic companies, startups and MSMEs at various stages of semiconductor design, including integrated circuits (ICs), chipsets, systems on chips (SoCs), systems and IP cores, and semiconductor-linked designs.

To encourage local production of semiconductors, the government has further waived the basic customs duty (BCD) on certain types of capital goods, machinery, electrical equipment and other instruments and their parts. However, this exemption does not cover populated printed circuit boards used in semiconductor wafers and liquid crystal displays (LCDs).

However, India’s recent proposal to the WTO about not extending customs duty moratorium on electronic transmissions will hinder local design companies working for global partners. Designing chips often require frequent data exchange across locations, within the country and outside. But taxing that data is bound to throw a spanner in fast and seamless operations.

A close look at the last five decades underscores the challenges the industry has long faced, including inadequate infrastructure, sluggish technology adoption, subdued demand, a shortage of top-tier talent and financial constraints.

Download The Free ReportShashwath T R, cofounder and CEO of Chennai-based Mindgrove Technologies, noted that the semiconductor business is capital-intensive, so much so that setting up a single outsourced semiconductor assembly and test (OSAT) plant can cost more than $500 Mn. Even in the design space, a successful fabless enterprise may require tens of millions of dollars before becoming profitable.

“Such capital was scarce earlier. But now, with the government’s support, it is available both as equity and debt,” he added.

What Pushed Indian Policymakers & Startups To ‘Chip Up’

Traditionally, the semiconductor landscape at home has been dominated by global giants like Intel, Nvidia, Micron, NXP and Qualcomm. Government entities like DRDO (Defence Research and Development Organisation) also play a significant role in this domain.

Although the foundation was there, and R&D into advanced semiconductor material and device technologies was ongoing, India did not make significant strides towards design and fabrication goals for decades due to huge expenses and the intricacies of the processes involved. But when the Covid-19 pandemic broke out in 2020, it brought a host of challenges, including a complete breakdown in the global supply chain and a subsequent shortage of microchips.

The massive shortage deeply impacted several industries, especially electronics and automotive, as these chips are essential components of many digital consumer products (more on their functions later). Additionally, their demand skyrocketed as consumer and industrial requirements increased during months-long lockdowns for containing the pandemic.

India, too, faced the impact. A 2019-20 report by the ministry of statistics, planning and implementation (MoSPI) estimated supply deficiency in major sectors such as education, health, transportation, communication, entertainment and certain household gadgets using chips-based devices.

A dearth of merchandise depleted nearly 50% of average consumer spending across these categories, thus affecting the companies and the overall economy. On the other hand, a long-term supply crunch pushed the prices up and saw an inevitable demand dip. Not exactly a healthy scenario in post-Covid times when every industry and every country tried to regain pre-pandemic growth rates.

Given these ground realities, India saw an opportunity to establish itself as an up-and-coming semiconductor hub to meet the increasing global and local demand. It also coincided with the surge in the startup ecosystem and the rise of aspiring entrepreneurs making forays into trending technology segments.

“In the past decade, the demand for semiconductor chips has grown significantly, while India is boosting its manufacturing in key sectors for exports. Therefore, investments in the semiconductor space and related electronics businesses seem feasible now,” said Shashwath.

Chips, Chips Everywhere, But What Do They Do?

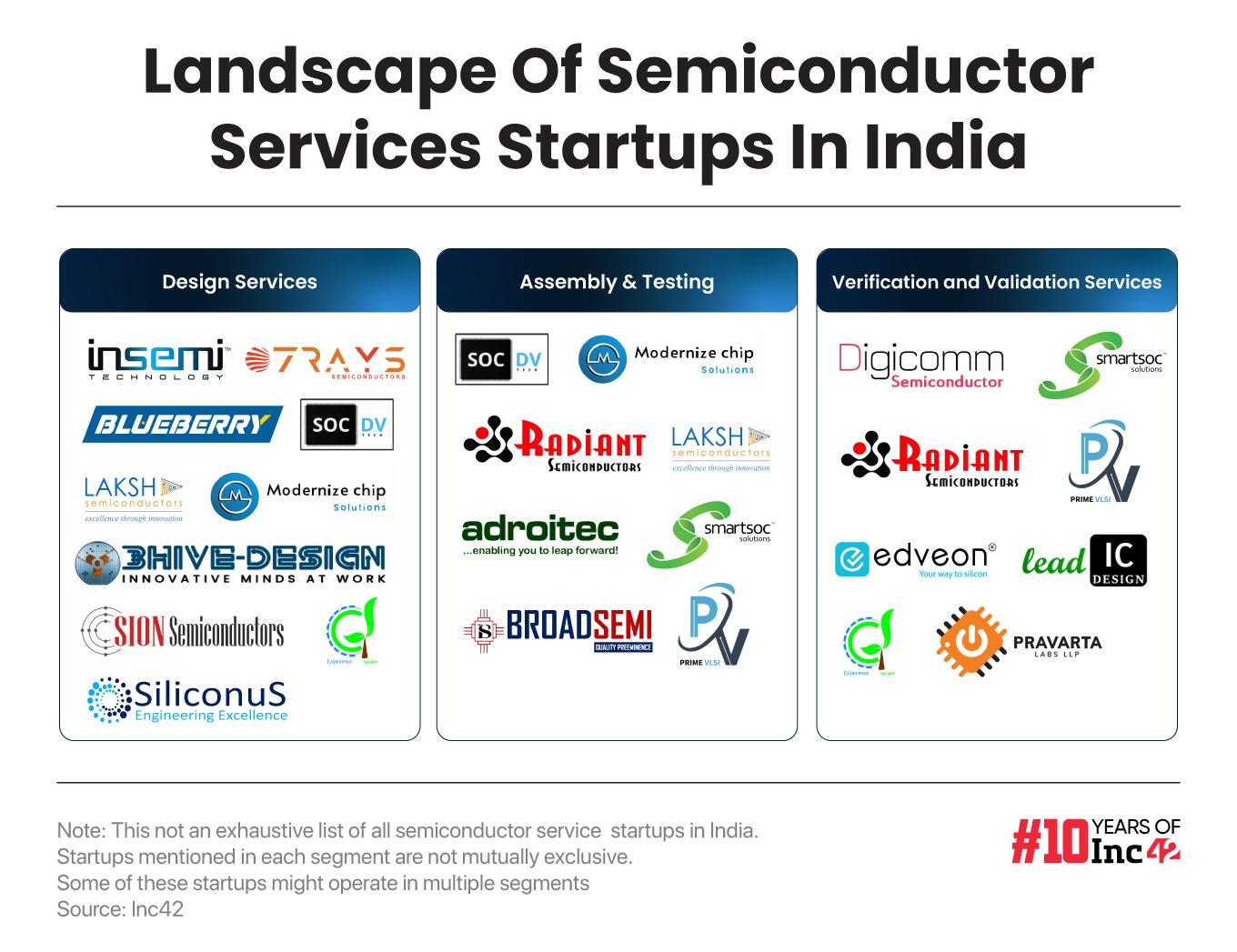

According to the Inc42 report, more than 100 startups are functioning across the value chain, specialising in R&D, design, assembly, verification and validation. In fact, the widespread demand for semiconductor chips will continue to rise for powering everything electronic and digital and building an IoT/IIoT ecosystem of smart devices and systems, which require sensors and integrated electronic circuits/chips for receiving inputs and executing actions based on logic.

In essence, chips are the brains and building blocks of all things tech – from video games, cars and supercomputers to precision farming and weaponry. These electronic circuits are embedded in tiny wafers made from semiconductor materials (like silicon) and contain multi-layered lattice works interconnected electronic components called transistors for transmitting signals.

Also, the smaller the size of an individual transistor (there can be a million or a billion in a chip), the more can be packed tightly, making a chip more powerful. Chips are measured in nanometres (nm), referring to the size of an individual transistor and equalling a millionth of a millimetre.

Nowadays, the ‘nano scale’ generally indicates a chip’s overall performance rather than the exact size of the transistor. But true to the original quality parameter, most advanced chips remain the tiniest on the nm scale, ensuring fast processing, less power consumption and less heat generation.

However, these require a high level of technical sophistication, component purity and stringent quality control implemented by very few global companies. Even a state-of-the-art chip manufacturer like the Taiwan Semiconductor Manufacturing took three decades to reduce the chip size from 3 micrometres to 3 nanometres (1 micrometre is equal to 1K nm).

Semicon chips can be analogue, digital or mixed, with different functionalities – namely, logic chip, memory chip, ASIC (application-specific integrated chip) and SoC (system on a chip).

Although experts are already debating the ‘Beyond CMOS’ concept that surpasses traditional digital logic, the current technology has ushered in ingenious products such as power-over-ethernet (PoE) standards for connected lighting, MOSFET (metal-oxide-semiconductor field-effect transistor) signal switchers and signal amplifiers for the telecom sector and the insulated gate bipolar transistor (IGBT) devices, which guarantee low power losses and are widely used in automotive, consumer electronics, IT and communications, healthcare, aerospace and defence.

Download The Free ReportHow Indian Startups Are Seizing The Newfound Opportunity

Although India might not be looking at fabricating 2-3 nm chips right now, larger design features below 200 nm work well for automotives, audio chips and display drivers and account for a substantial market. Additionally, the country’s growing focus on developing networking devices and telecom equipment, coupled with the rapid adoption of artificial intelligence (AI) and 5G, will help drive the domestic market.

As Shashwath of Mindgrove points out, the multiple usage and fast evolution of the semiconductor technology are creating new opportunities for Indian startups, which are rapidly building the expertise and the resources to design (and fabricate) widely used microchips, as well as more complex ones required for AI applications. In fact, it is one of the most promising sub-sectors within the semiconductor space.

At present, the tech clusters of Bengaluru remain the most active semiconductor startup hub, housing 63.7% of the ventures. It is followed by Delhi NCR (9.9%), Hyderabad (5.5%) and Chennai (4.4%).

A few startups in the semiconductor space have also attracted investor interest and raised early stage funding, although the ticket sizes are pretty small. Among these are InCore Semiconductors ($3 Mn), a processor design startup; Mindgrove Technologies ($2.32 Mn), specialising in RISC-V-based SoC designing, and AGNIT Semiconductors ($1.37 Mn), a designer and manufacturer of GaN (gallium nitride) components used for defence and telecommunications.

The funding landscape may soon change, given the global trends. According to a recent report by Moody’s Analytics, Asia will continue to lead in chips and electronics production in the foreseeable future as innovation leaders across the globe work with top manufacturers from Taiwan and South Korea to keep the formidable cost of chip production as competitive as possible.

With India focussing on both fab and non-fab expertise, tech companies are bound to explore yet another emerging hub. Of late, a few investments in the semiconductor industry seem to be moving away from China, yet another reason why investors may turn towards India. The growing ecosystem of startup enablers within the country’s semiconductor industry will further fuel growth and funding potential.

The infographic below features some key startups in India’s semiconductor services landscape. Also, there is a rising wave of semiconductor startups catering to specific verticals such as AI, industrial automation, consumer electronics, automotives (including EVs and autonomous vehicles), and telecom and wireless communication.

Among the leaders are Ola Krutrim, Semiconsoul, Signalchip, Cientra, Wafer Space (now ACL Digital), Saankhya Labs, AGNIT, InCore and Sensesemi Technologies, among others. Located in Bengaluru, the fabless chip design venture Sensesemi develops SoCs for the Internet of Medical Things (IoMT) and other IoT devices. On the other hand, Krutrim is pioneering a unique chiplet architecture for system-in-package solutions, targeting Indian companies specialising in Edge computing and automotive products.

Can India Emerge As The Next Big Chip-Maker?

India aims to become a chip-making superpower, propelled by robust government support and a burgeoning startup ecosystem. But the path ahead is fraught with challenges. The lack of fabrication facilities and manufacturing experience, along with heavy dependence on procuring raw materials from global suppliers, can limit a country’s capabilities.

Next comes the most pertinent question: Has India got talent for chip design and fabrication? A Q4 CY23 report by Zinnov-NASSCOM estimates 50K+ specialised workforce catering to more than 55 semiconductor GCCs (global capability centres) across the country, underlining there is no dearth of engineering talent in India. However, there is a shortage of service and maintenance experts and a lack of individuals well-versed in the fundamentals of semiconductor equipment.

“These things accumulate over time, leading to inventory pile-up, longer lead times and higher freight costs,” observed Singh of CDIL.

Shashwath of Mindgrove also pointed out the competitive landscape, emphasising that Indian chips are frequently compared to those from industry giants like Texas Instruments and NXP, which have established relationships with OEMs. This makes it exceedingly difficult to penetrate the global market.

On the flip side, there is growing optimism among stakeholders due to robust government support and the upcoming launch of quite a few top-grade semiconductor plants. In many cases local and global leaders are working in collaboration (think of the tie-up between Tata Electronics and Taiwan’s PSMC) for the best possible output, which will put all doubts about quality at rest.

The government’s plan to establish a graphics processing unit (GPU) cluster to support startups specialising in AI model training also aligns with the INR 1,100-1,200 Cr design-linked incentive scheme. For certain fabrications, ATMP and OSAT units, the government will provide 50% of the project cost/capital expenditure to eligible applicants on a pari-passu basis, an incentive driving many companies to set up semiconductor units across the value chain.

In line with an earlier analysis by McKinsey & Company, Inc42’s latest semiconductor report projects that the global AI semiconductor market will reach $190 Bn by 2030, with India poised to account for $21 Bn. This growth is attributed to the country’s ambitious smart city projects, infrastructural development and the increasing popularity of AI-powered consumer devices like smart home appliances and gadgets.

Given these developments, there will be opportunities galore for startups in the semiconductor space, whether they ensure a steady supply of bespoke ingredients to fab and fabless units, double down on intricate designs or do the final magic and make the chips. Also, the co-location of suppliers, designers and manufacturers will help fulfil every activity of the value chain, eventually unlocking new product potential.

Meanwhile, India must overcome a few practical difficulties (meet the expenses, for starters, and access the latest know-how) and gear up for global competition to ensure that these Make-In-India deeptech projects will finally take off.

[Edited by Sanghamitra Mandal]

Download The Free Report