DealShare was valued at $1.7 Bn in January 2022, but like many other Indian unicorns, its bloated valuation is finally being questioned

The exit of CEO Vineet Rao comes amid several challenges for DealShare which has scaled back operations in major states and laid off more employees, as per sources

DealShare‘s latest focus is on a DMart-like hybrid retail model, where it will utilise its cash reserves to set up brand-owned stores across India

January 2022: DealShare

Turns Unicorn With $165 Mn Funding Led By Tiger Global

February 2022: DealShare Raises $45 Mn In Series E At $1.7 Bn Valuation

April 2022: DealShare Aims For $3 Bn GMV By March 2023

May 2022: DealShare Plans To Add 1,500 Employees, Acquire 10 Businesses In Expansion Spree

November 2022: DealShare To Invest INR 500 Cr In Next 2-3 Years In Private Label Brands

December 2022: DealShare Customer Base Touches 20 Mn

January 2023: DealShare Lays Off 100 Employees, 6% Of The Workforce

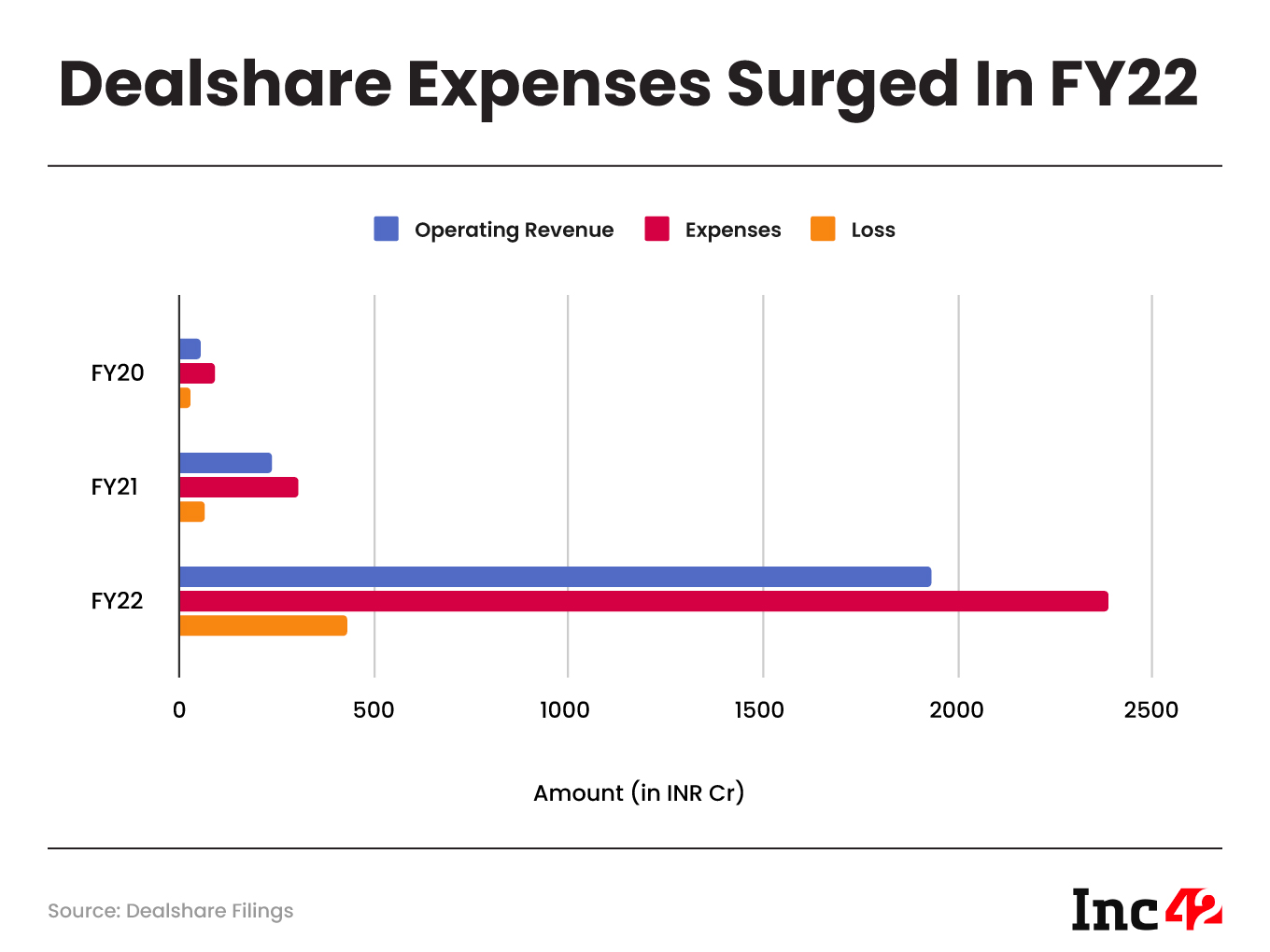

January 2023: DealShare’s FY22 Loss Balloons 543% YoY To INR 431 Cr

June 2023: DealShare To Invest INR 1,000 Cr In 5 Years To Help MSMEs Scale Up

July 2023: DealShare Without A CEO As Vineet Rao Steps Down

We have to give DealShare credit where it’s due. Despite the mega losses in FY22, layoffs earlier this year, the exit of a CEO, and the rapidly-changing competitive landscape, the Tiger Global-backed unicorn is not lacking any optimism.

Even its press release about cofounder Vineet Rao stepping down as the CEO was buried under a couple of paragraphs of what can only be described as bluster about a ‘strong balance sheet’ and a ‘quest towards profitable growth’.

The ecommerce unicorn was valued at $1.7 Bn at the time of its last fundraise in January 2022, but like in many other Indian unicorns, the bloated valuations are finally deflating and finding their ground.

But again, DealShare’s bullishness makes it hard to pin down the company’s many challenges. For one, even as its primary social commerce model has faded, the startup has not had any qualms in talking about the opportunity in private labels, MSMEs and all the tried-and-tested buzzwords that ecommerce companies turn to when things aren’t going so well.

DealShare: Scaling Down Like A Unicorn

The CEO’s departure comes at a time when the startup is moving to a hybrid online and offline model.

In a statement, the startup said that Rao would support the board to help identify the new CEO. However, it didn’t disclose the reason behind his resignation. As such, Rao’s decision to step down abruptly without securing a replacement is bound to raise many questions. Rao continues to hold more than 10% stake in the company.

It must be noted that DealShare has made several key appointments over the last few months. In July, it appointed former Tata CLiQ Saurabh Kishore as its chief technology officer. Prior to Kishore’s appointment, DealShare didn’t have a CTO, and cofounder Rajat Shikhar, who has led product teams previously, largely handled the CTO responsibilities.

Besides this, in December last year, DealShare also appointed former Big Bazaar chief executive Kamaldeep Singh as the president of the retail business. This came soon after the company said it would invest INR 500 Cr in the private label business.

Further, the company claimed this year that it would invest INR 1,000 Cr to target MSMEs in India over the next five years. Despite its bullishness, DealShare has not exactly outlined how these investments will bolster its revenue or bottom line.

Over the course of the past couple of months, Inc42 has spoken to a number of former employees and investors in the ecommerce and B2B commerce space about where DealShare is heading and the picture painted is definitely less rosy than the most recent headlines about the company.

Amid bearish market conditions, DealShare is facing a series of challenges, including shuttering warehouses, implementing layoffs, scaling down operations in various states, and the CEO’s resignation at a critical time.

As per sources close to the company, it completely shut down operations in Maharashtra in late June. DealShare primarily had warehouses in Mumbai and Pune for B2C and B2B verticals, with nearly a dozen warehouses in Pune being shut. The company has also shut operations in Hyderabad, with Gujarat next on the chopping block, as per sources.

Employees in these states were told to resign in June due to a supposed fund crunch and were given two months of salaries in compensation. Over 400 employees have been let go in the past four months.

The thin margins across its many products mean that the company is seemingly solely relying on VC funds to grow and scale.

Questions sent to DealShare cofounder and co-CEO Sourjyendu Medda about the exits, layoffs, downturn in business and challenges in scaling up the hybrid retail business were not answered.

After pulling back from some states, the Tiger Global-backed unicorn will focus largely on Delhi NCR and Rajasthan, where it sees most business. DealShare is said to be doubling down on these two particular regions and scaling back from other hubs, as reported by Inc42 earlier this year.

So, what exactly went wrong for DealShare that the unicorn has had to bite the bullet and call off its expansion spree?

How DealShare Fell Into The Red

Founded in September 2018 by Sourjyendu Medda, Vineet Rao, Sankar Bora, and Rajat Shikhar and Rishav Dev, DealShare began life as a social commerce marketplace which looked to target new online shoppers through affiliate links shared on messaging and social apps.

Dev exited the company in 2019 and is currently a cofounder of a fashion brand, however, the other four cofounders have key roles. While Rao was the CEO till this week, Medda is currently still the co-CEO (despite no actual CEO). Bora is the COO at the company, while Shikhar is the CPO at DealShare.

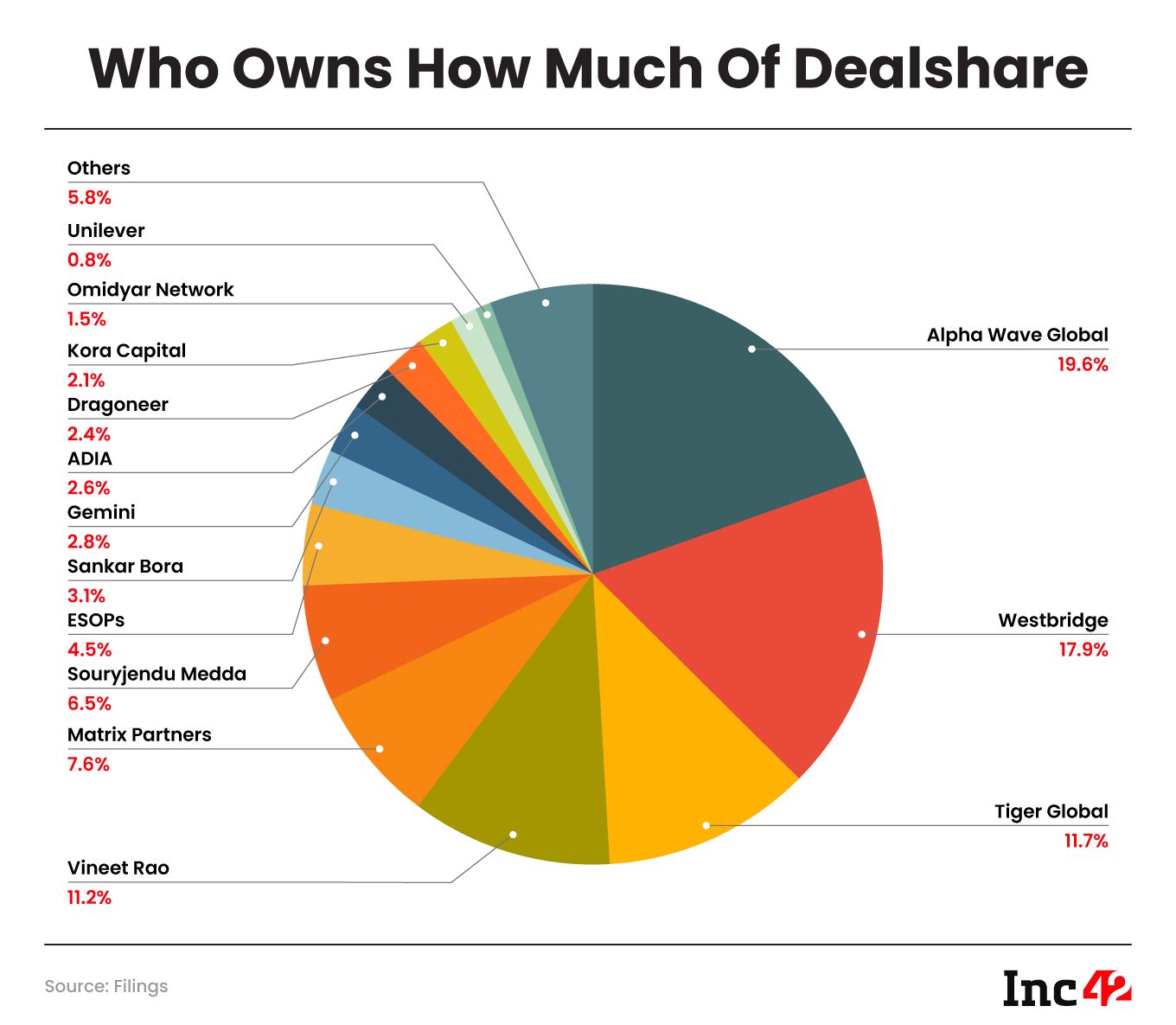

To date, it has raised close to $400 Mn from investors such as Tiger Global, Matrix Partners, Alpha Wave Global, Westbridge, ADIA, Unilever Ventures and others.

The company started out by allowing consumers to get discounts on products for buying in groups. Before launching its app, the company offered products through WhatsApp, which is where its social commerce credentials were honed.

DealShare’s idea was similar to a number of other startups such as Meesho, Trell, GlowRoad, CityMall, SimSim, Bulbul, and others. Essentially, these apps brought the affiliate marketing model to smartphone apps such as Instagram or WhatsApp where individuals can share links and earn money for conversions through those links.

But social commerce, which boomed during Covid and the height of TikTok mania in India failed to move the revenue needle for these players.

Rivals such as Meesho, GlowRoad, Trell and others have pivoted to other segments and models due to mounting losses. Bulbul was acquired by the Good Glamm Group in March 2023 in what we described as a puzzling acquisition at the time.

Essentially, social commerce was a thesis that never panned out. But DealShare had at least convinced investors about the model’s potential.

The startup entered the coveted unicorn club in January 2022 after it bagged $165 Mn in Series E round and followed this up with a $45 Mn round led by ADIA, which catapulted its valuation to over $1.7 Bn.

DealShare had major plans to expand and scale up with this funding. The startup’s statement said that it would invest in technology and data science, and target a ten-fold expansion in its logistics infrastructure to increase geographic reach. In addition, it also said it would establish a sizable offline store franchise network.

But instead, DealShare has scaled back and the promise of social commerce is all but dead. Besides offering a digital B2B wholesale platform for kirana stores and retailers, DealShare operates an online grocery store for consumers as well. Its earlier social commerce play has more or less been retired now with a focus on B2C and B2B2C ecommerce.

In July, the company claimed to have over 1 Cr customers, with 1.5 lakh daily orders fulfilled. In its private label business, DealShare said it has eight brands across 16 categories, besides connecting 500 other brands to 1,000+ retailers in India.

It’s perhaps fortunate that DealShare managed to secure a funding round at the time it did. Since March 2022, valuations have become fickle and VCs are not shy about calling out the need for correction. Revenue projections, which were once rather ambitions, have also sobered down.

Losses Grow, Users Decline

Even before it turned a unicorn, DealShare has been ultra-bullish about its revenue projections. In July 2021 (FY22), after the startup raised $144 Mn, cofounder Medda said DealShare was on track to hit “$1 Bn gross merchandise value run rate by the end of the year and is very close to breaking even.”

As we now know, DealShare saw losses grow by nearly 7X in FY22 to INR 431 Cr, far from breaking even. The company primarily earned revenue from sale of goods, as a result its expenses leaned heavily towards purchase of stock in trade. It purchased stock worth INR 2,088 Cr in FY22 and earned INR 1,925 Cr in the year from sale of products.

Losses are not alien to the ecommerce sector, of course. While no one expects an ecommerce company to become profitable in its first few years — even Flipkart is in the red and Meesho’s FY22 loss stood at a staggering $500 Mn — there needs to be some justification for the fundraise, which usually depends on scale and revenue rate.

Let’s understand whether DealShare has the scale and engagement to justify the valuation and show that it can potentially accrue enough revenue from this scale to break even.

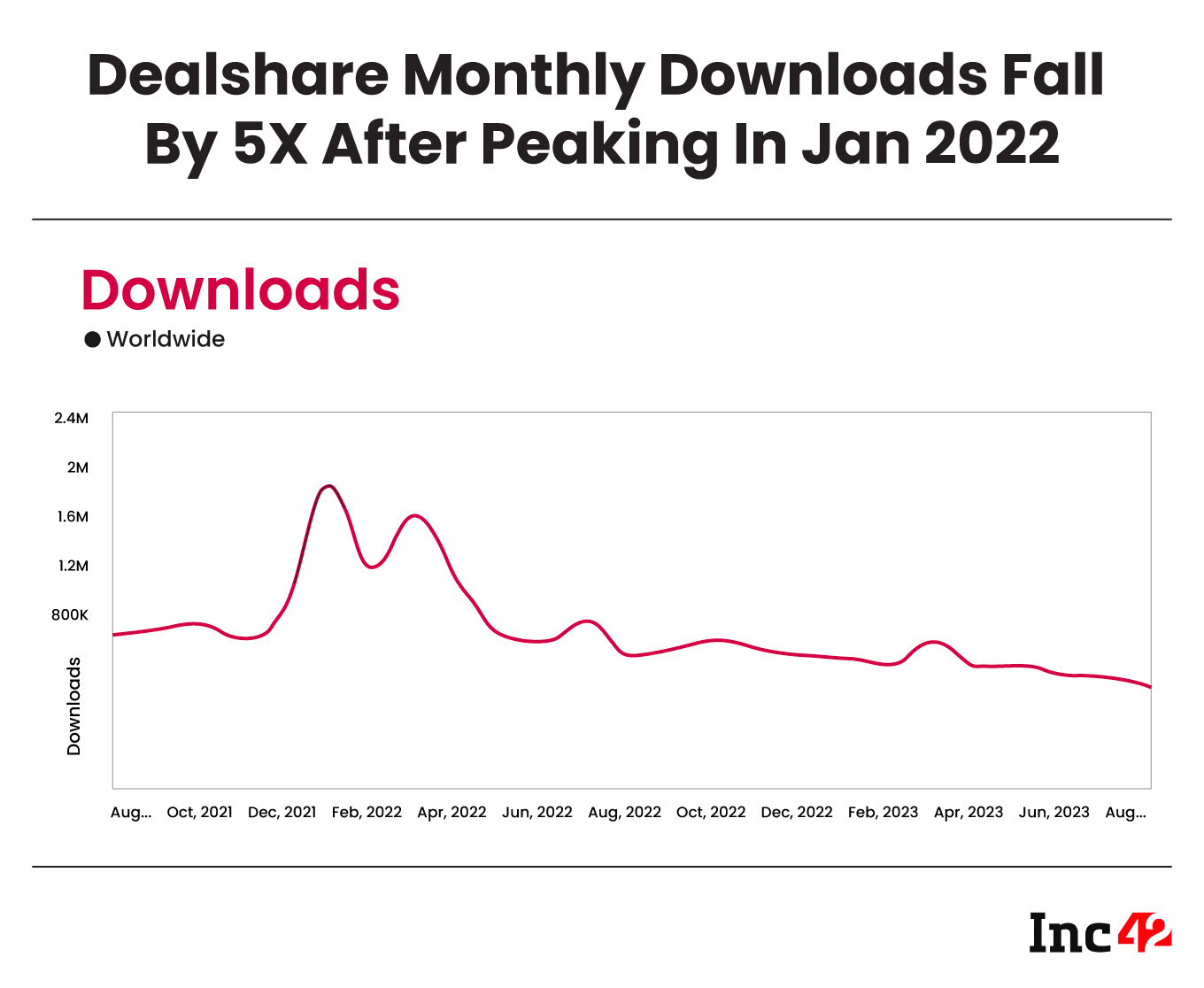

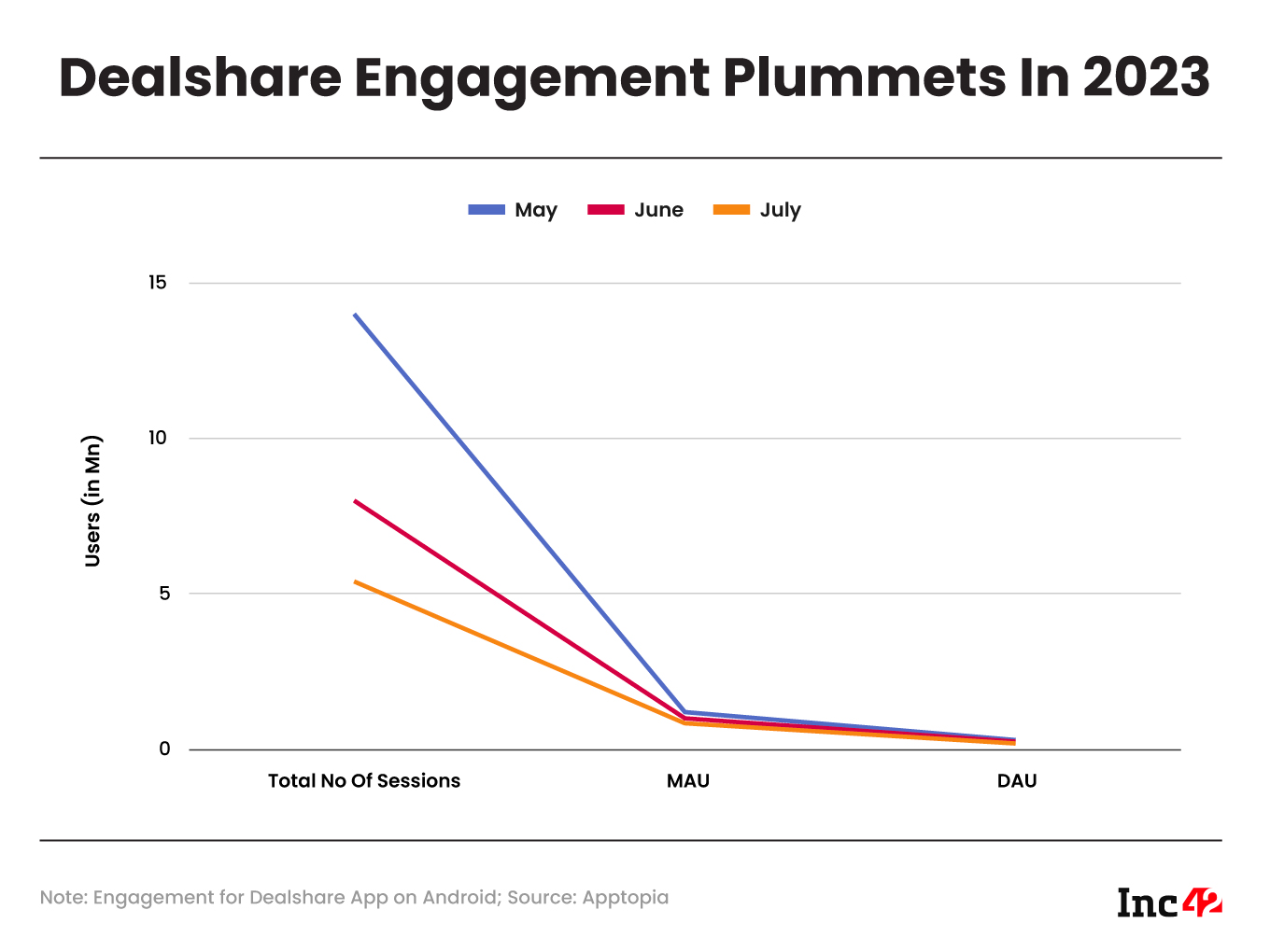

As we can see in the below charts, DealShare’s engagement (monthly and daily active users) and downloads have declined drastically, according to data sourced through Apptopia.

Unsurprisingly, downloads peaked to around 2 Mn per month just before DealShare’s unicorn round in January 2022 when it raised $165 Mn and since then monthly downloads have not cracked the 500K mark in the past 15 months.

Even though these numbers pertain to the Android app only, DealShare recently claimed that 99% of its volume comes from this channel.

The daily active user count has not been higher than 420K per month for the past three months. It’s not clear how the company plans to drive engagement and the downloads without raising fresh funds to fuel marketing and promotions.

Users are also fed up with DealShare’s tech and delivery issues.

Multiple social media posts, such as this one, point to the company automatically cancelling orders, delivering tampered packages and not refunding the amount for cancelled orders to customers.

Many customers told Inc42 that the company cancels orders without notice and does not refund the money to the source of payments. Instead, the amount is deposited to a DealShare Wallet, which has a one-year expiry period for fund deposits.

Given that orders are automatically cancelled at times, users find it complicated to utilise their wallet balance as highlighted by tweets as late as July 2023. Besides this, the platform is inundated with complaints about delays in deliveries for products such as flour, rice and other staples.

Cracking The Retail Game

The primary problem for DealShare today are the executional issues in its distribution and warehousing operations. The layoffs earlier this year have further dented the operations in certain regions.

B2B wholesale distribution is a complicated beast due to the competition and the aggressive margin play involved.

Warehousing and distribution are said to be the biggest success factors in online B2B wholesale commerce, and challenges in this regard can hamper margins in the long run. This is the area that the likes of JioMart, Udaan, Jumbotail, Shopkirana and others have looked to grow in the past few years.

Even at the best of times, the margins are low because distributing to stores is fraught with logistics challenges. Startups compete by building warehouses and customising their supply chain for manufacturers and kiranas, and offer perks such as upfront payments to manufacturers to get longer contracts.

Competing in this segment requires not just extensive experience to build distribution networks but also financial flexibility to discount certain orders. Companies have struggled with razor thin margins due to the high competition from traditional B2B wholesalers.

Udaan was founded in 2016, two years before DealShare, but its losses in FY22 surged 1.2X to INR 3,075.80 Cr compared to INR 2,503.30 Cr in the previous year. This was on a revenue base of INR 9,880 Cr. In the year, Udaan spent INR 9,415 Cr in purchase of stock. Even at that scale, breakeven remains elusive. DealShare has a long way to go before catching up.

In early August, a report by The Arc claimed that despite having cash reserves of $150 Mn, the management is not allowed to access this cash for day-to-day affairs. The publication claimed DealShare management requires investor approval to access these reserves.

The company also said it would be focussing heavily on a hybrid approach with branded offline stores backing up the B2C and B2B2C ecommerce operations.

DealShare Vs Udaan, JioMart & Co

The pandemic more or less forced retailers and kiranas to use digital platforms to order directly from manufacturers. It not only widened the opportunity for Udaan, Peel-works’ Taikee, Shopkirana and others but also compelled giants such as Jio and Tata (armed with BigBasket) to enter the fray.

New-age companies such as Udaan, JioMart and DealShare offer a convenient way for retailers to buy products at wholesale prices, but DealShare is not in the position to dictate pricing to manufacturers just yet.

Even Udaan struggled with this issue and took FMCG giant Parle to the Competition Commission of India. Udaan had alleged that Parle was deliberately blocking supply of certain products to the startup, which forced the company to buy from the open market and thereby compromise on the margins.

Such scenarios are not uncommon in the B2B space. Besides Parle, even Amul stopped supplying products to Udaan.

Reliance Retail’s JioMart seems to have made a huge leap by adding Metro Cash & Carry to its bucket. JioMart’s entry has already made life difficult for the likes of Udaan, and DealShare will have to contend with this major headwind as well.

Even Flipkart has jumped in with both feet and is banking on a healthy mix of product categories to get higher margins on average. But in the B2B segment too, Flipkart has considerable losses.

However, it must be noted that DealShare has the backing from Unilever Ventures, which is the venture capital and private equity arm of global FMCG giant Unilever. It’s not clear how much of DealShare’s business comes from Unilever and Hindustan Unilever-owned brands. The latter operates over 65 brands in India across categories.

Given that the competition DealShare is perhaps stepping into this space a little too late and on the backfoot. Its extended focus on loss-making social commerce and B2C business may prove to be a dead-weight for the startup.

Revenue has to outpace costs of purchase of stock, as highlighted by Udaan’s financials and to get there, DealShare has to get the right margins from its network consistently over many quarters.

While DealShare says it would be setting up retail stores to back ecommerce operations, this hybrid play will also require significant investments, and it’s not likely to deliver profits in the short term.

If it is looking to scale up and expand its geographical reach, DealShare has to seek sustainability by charging higher margins than players such as JioMart or Udaan. This may make the company less appealing to manufacturers as a whole, especially if DealShare is not able to sign up more retailers to buy this stock at wholesale.

This is where the challenge lies for DealShare. Even at its optimistic best, the company cannot deny that B2B ecommerce and scaling up the retail play will have several unit economics challenges. The exit of the cofounder and CEO at this juncture makes this journey that much harder.