Catering to only members, CRED Scan & Pay does not seem to compete with apps like PhonePe and Gpay rather aims to increase the level of engagement for existing users

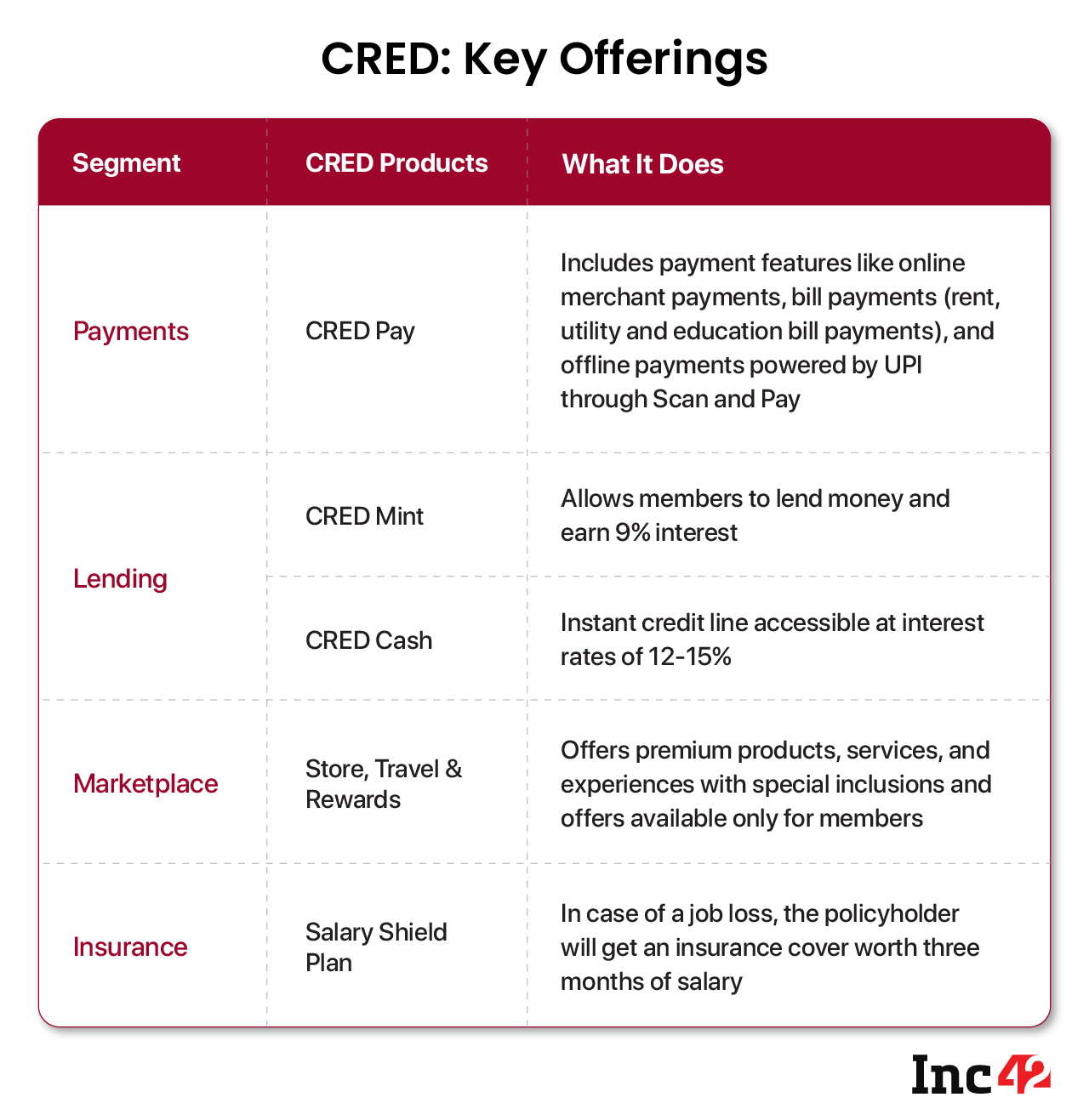

With Mint, Cash and Salary Shield features, the company has already entered into the lending and insurance space

The company’s revenue has increased from INR 18 Cr in FY20 to INR 95.5 Cr in FY21 while the total loss too increased from INR 361 Cr to INR 524 Cr during the same periods

Even as questions persist about its current business model and revenue track record, Bengaluru-based Cred![]()

![]() has now launched a new product in the hope of driving engagement and boosting transactions per user.

has now launched a new product in the hope of driving engagement and boosting transactions per user.

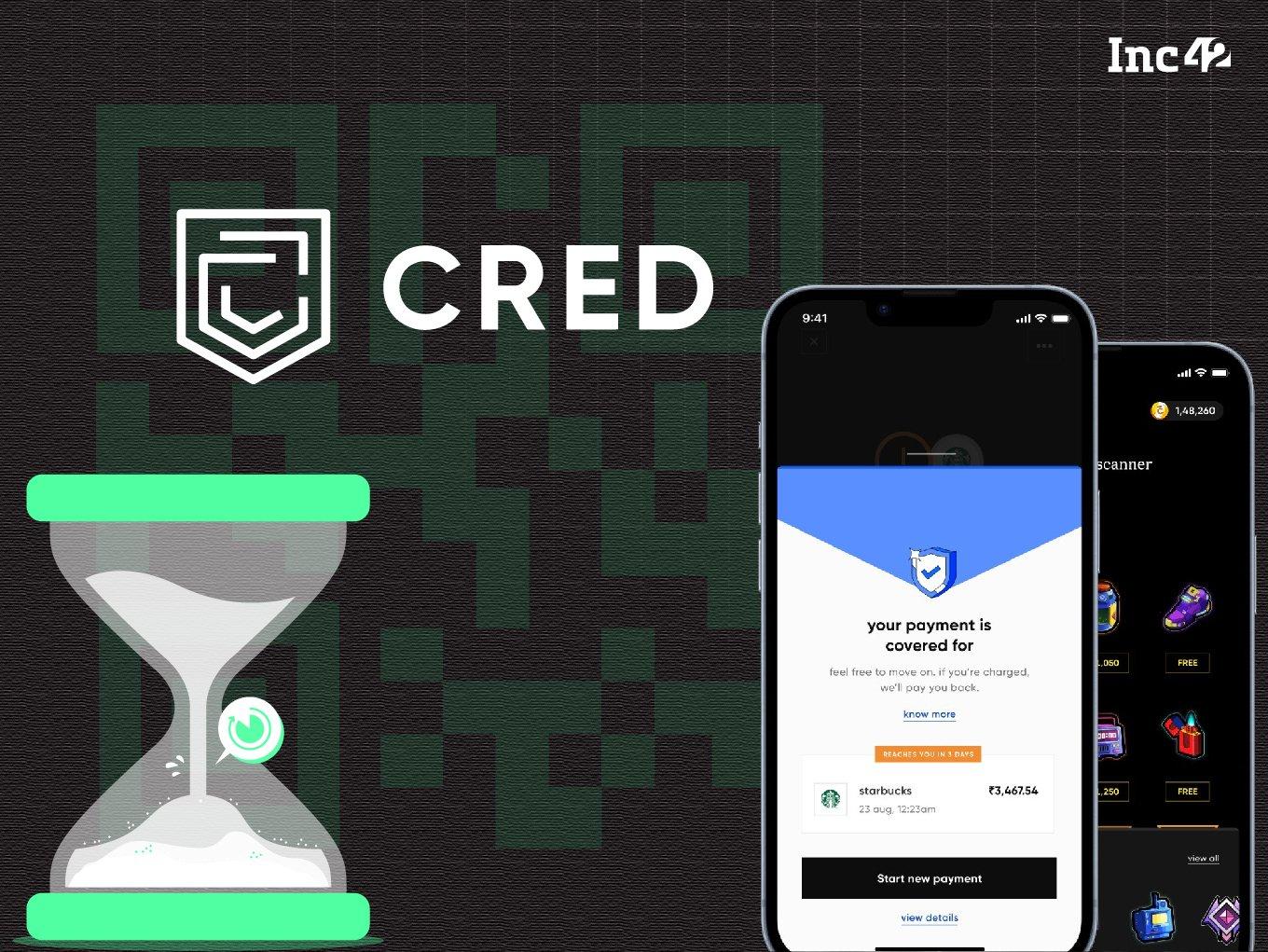

The Scan and Pay feature launched by Kunal Shah-led CRED is the latest to join the stable.

What started as a credit card bill payments app in 2018 has expanded to CRED Pay for making utility bills, CRED Mint for P2P lending, CRED Store, CRED Cash for loans and now Scan-and-Pay for UPI.

Founded by Kunal Shah, CRED has been one of the fastest-growing unicorns in India. It has raised over $800 Mn including the latest Series F Funding in June this year. The company claims to have 9 Mn active users, who are primarily credit card holders that sign up to the app to make card payments and other utility bill payments.

Speaking at the launch this week, CRED founder Kunal Shah said that the company has evolved as a great platform for brands, financial institutions, merchants, partners to come on board and offer great ecosystem benefits for each party. “And obviously, our intent is to constantly create more value for everybody in the system. Starting from CRED Pay to Bill Payments and now Scan & Pay, the intent is to constantly keep the transactions rewarding and delightful,” Shah added.

But how relevant is another UPI product in India at a time when there are half a dozen leading apps and bank apps that support UPI? Is CRED large enough to bank on UPI for growth? These are some of the major questions.

Scan & Pay: Just Another UPI Payments Or It’s Different?

Scan & Pay, a UPI payment feature, is made available to CRED members only. Member eligibility involves having a 750 Experian score, so despite being UPI at the core, CRED’s Scan & Pay feature does not really compete with other UPI apps. Those work for anyone and everyone who owns a mobile phone.

Recently, there has been an increasing trend of shifting from card transactions to UPI in India. Since 2016, if cards have grown by 1.6x, UPI payments have grown nearly 60x. Clearly, cardholders have started making a significant portion of their transactions in UPI. In order to keep up with this, CRED had no option but to launch the UPI payments for their members, said an analyst who works with one of the Big Four companies and did not wish to be named.

Unlike other UPI payments features, the company claims to offer certain unique features such as payments protection, customisable experience and anonymous UPI. Besides providing the existing status of the transaction, CRED is claiming 100% protection on every payment in case of failures.

Further, it provides customisability through flairs that members can add to the scanner screen. These virtual accessories can be purchased by redeeming CRED coins.

These are all great features, but not really a value-add for customers to opt for CRED over Google Pay, Paytm or PhonePe, which have built a bigger ecosystem of partners within their apps.

In comparison, CRED is banking on the fact that its ecommerce operations opened up doorways to bring D2C brands that have omnichannel presence as retail partners for the Scan and Pay feature. The company claims to have onboarded approximately 2,200 merchants on its app so far. With Scan & Pay, the company expects these numbers to increase significantly.

The CRED Ecosystem

In the last four years, CRED has gradually taken baby steps into other fintech segments besides credit card payments, including lending, marketplace and insurance. The company has launched some introductory products in each of the segments.

Besides this, the company has also planned to become an account aggregator. In January 2020, a separate subsidiary company called Dreamplug AA Tech Solutions was incorporated. However, it is yet to get approval from the RBI in this regard.

In August 2022, it was reported that CRED is looking to acquire Smallcase, a wealth management company that focuses on equitable investing in India, but this acquisition has not gone through for various reasons. This might delay the company’s plans to enter the investments segment.

In the past, CRED acquired HipBar, an alcohol delivery app, which had an RBI-approved mobile wallet licence. It also acquired Happay which develops business expense management software.

It’s worth noting that the company’s revenue has increased from INR 18 Cr in FY20 to INR 95.5 Cr in FY21. However, total loss too increased from INR 361 Cr to INR 524 Cr during the same period.

Given that CRED continued to spend heavily on promotions in FY22 as well means we can expect the losses to continue. On the revenue front, the introduction of lending is likely to have boosted the income from operations in FY22. However, the financial performance of the company for the previous fiscal year is still not official.

Is UPI Enough For CRED?

With Scan and Pay, the company claimed it listened to what its users wanted when launching the feature. But even so, CRED’s user base is significantly lower than most UPI apps, and changing app habits is harder than it sounds.

Many of CRED’s users might themselves be so habituated to Paytm or Google Pay or PhonePe that the fact that CRED has a UPI feature might not register immediately. So CRED has to continuously push for engagement through marketing, notifications and more.

At the same time, the likes of Paytm, PhonePe, Amazon Pay and Google Pay already offer most features that CRED does, including credit card bill payments, lending and much more.

WhatsApp is also a factor here with its recent deal with Jio for ecommerce. Most of the existing UPI apps have much bigger access to the marketplace and merchant partners, an area where CRED is only getting started.

What Is CRED’s USP?

Despite only three out of every 100 Indians having a credit card, CRED has remained bullish about targeting the premium Indian consumer.

This naturally shrunk the addressable market for CRED in the very beginning and many commended this strategy since it was focussed and revenue-oriented. Even though CRED did not earn too much revenue in the early days, the idea was that it could bring new services to its most active users.

However, the limited target market also limits the potential revenue streams for CRED, and also pose questions of lack of scalability. “The idea is to increase the level of engagement and retain the members for a longer term, reducing the CAC and increasing the ARPU,” said a company spokesperson.

CRED claims to offer a delightful and rewarding experience to users, which it says is the USP. While other apps do offer similar rewards on every transaction, the term ‘delightful’ is subjective and does not necessarily mean deeper engagement from the customer.

For instance, Flipkart and Paytm have a loyalty programme that is similar to CRED Coins. But while Flipkart has 150 Mn products, CRED just has a few thousands in its catalogue. So the question is: Is the CRED store with its limited shopping experience actually delightful?

CRED’s rewards are more inspired by how banks offer rewards and cashback, and not how marketplaces attract users, said the analyst quoted above.

“The idea is to milk the most milkable instead of shooting in the dark and finding the milkable first, an idea that very much every VC likes,” said the analyst.

Where will CRED turn to next after UPI? And will the addition of these services actually bring in the revenue and profits that have become so paramount in 2022?

While VCs have shown patience with some startups such as CRED given the longer horizons of their vision, they are unlikely to ignore the specific challenges in CRED’s revenue track record for too long. And when it comes to the question of revenue, Kunal Shah and CRED still do not have a clear answer.