[Note: This article is part of The Junction Series. We will be covering the HealthTech sector in detail at The Junction 2017 in Jaipur. Learn more about The Junction here!]

The Indian healthcare sector is vastly unorganised and unevenly distributed. Documentation and medical history are still largely non-existent, especially in Tier II and Tier III towns and cities. Higher patient to doctor ratio, treatment cost variations, lack of medical awareness, the need for faster diagnosis and treatment have all contributed to building untenable pressure on the system.

In its recent assessment of the Indian economy, the Organisation for Economic Co-operation and Development (OECD) identified India’s poor health outcomes as one of its major developmental challenges. India is a laggard in health outcomes not just by OECD standards, but also by the standards of the developing world.

A key reason behind the poor health of the average Indian is the low level of public investments in preventive health facilities and medical care facilities. Even when public health facilities are available, they are often of poor quality.

This gap has led to a surge in consumer-driven healthtech startups, and it seems Indian tech entrepreneurs have taken up the gauntlet to solve the complex healthcare problem in India.

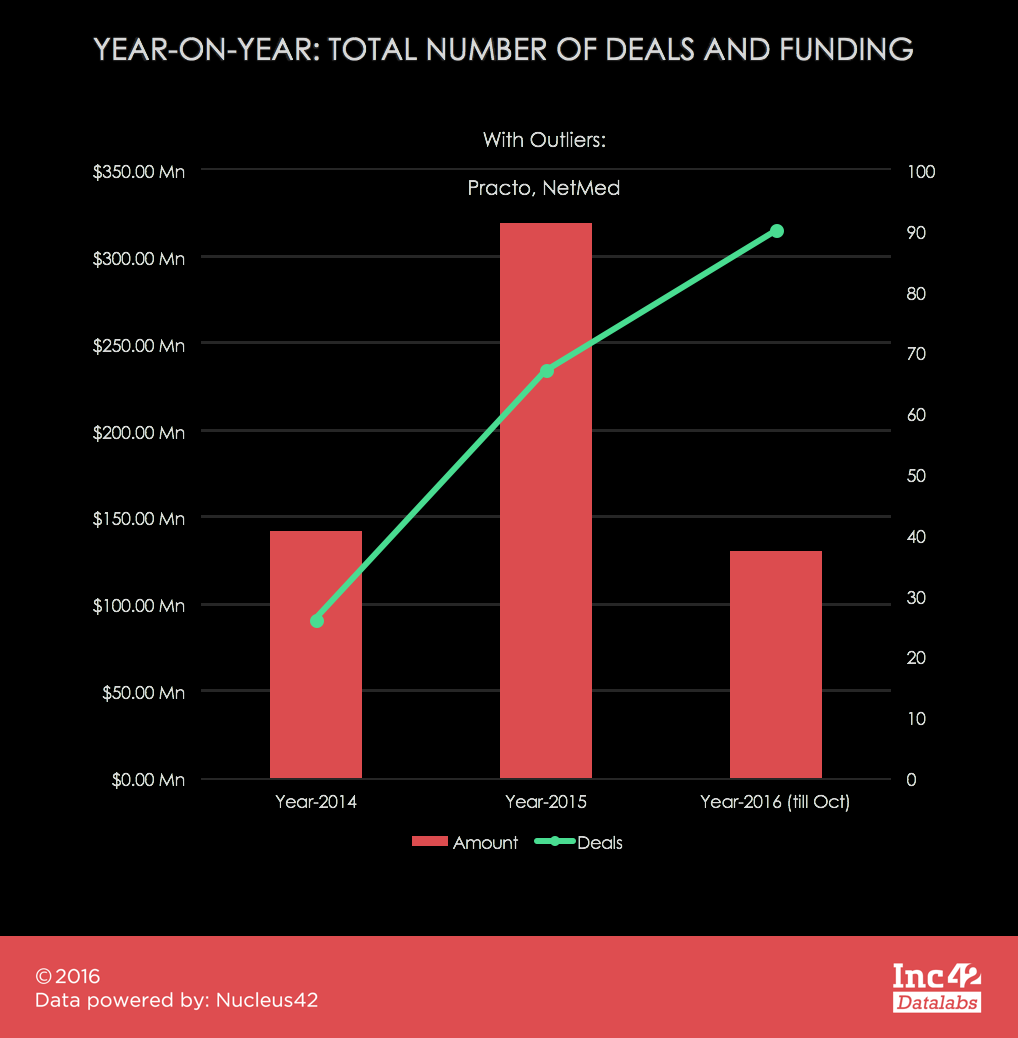

As per Inc42 datalabs, 183 healthcare startups have been funded in the period of 2014-2016 (till October 2016). With the sector seeing an infusion of around $600 Mn investment, we felt it was time to deep dive into the nuances of healthtech startups in India over the last three years.

Overview

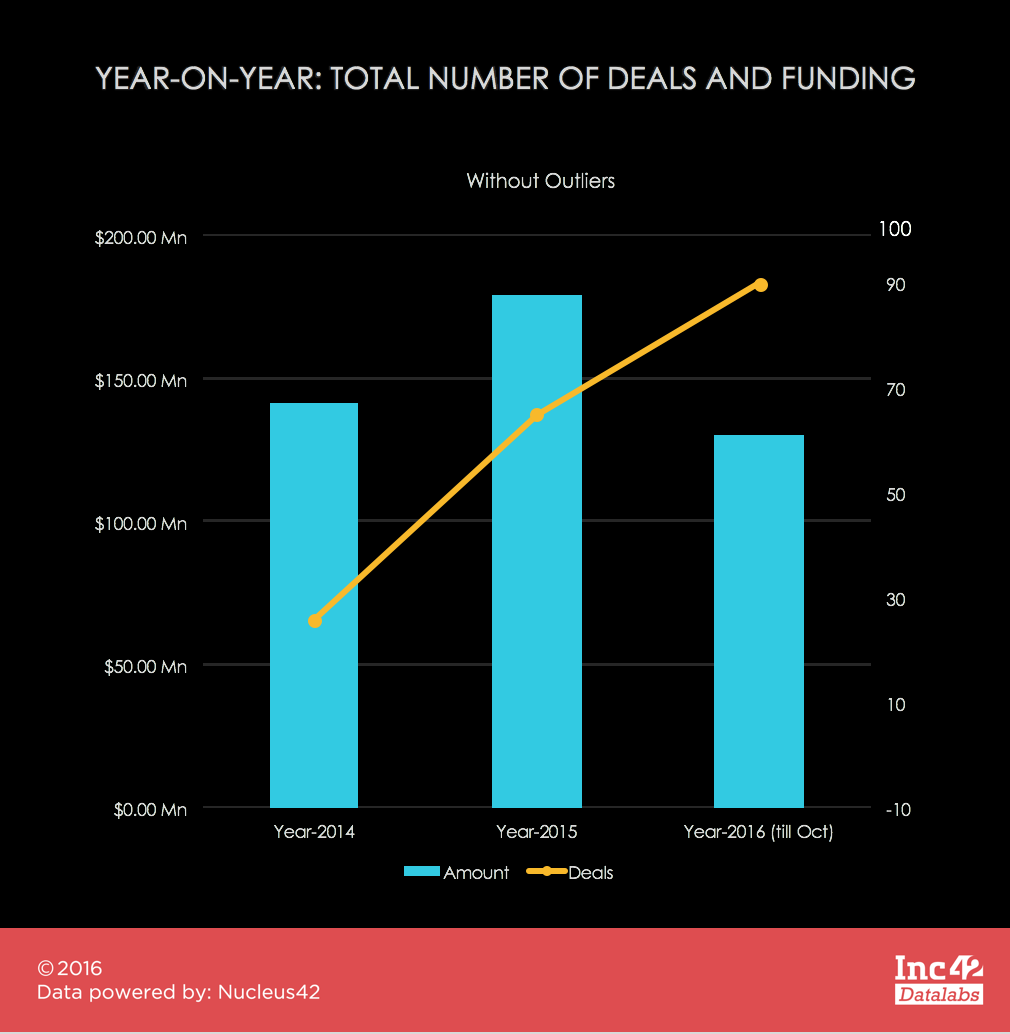

The year-on-year plot for the total number of deals shows a steady growth, but the total amount of funding seems explosively high for 2015. A better representation comes up when we exclude the outlier funding amounts like the $90 Mn Series C funding of Practo and $50 Mn Series A funding for NetMeds.

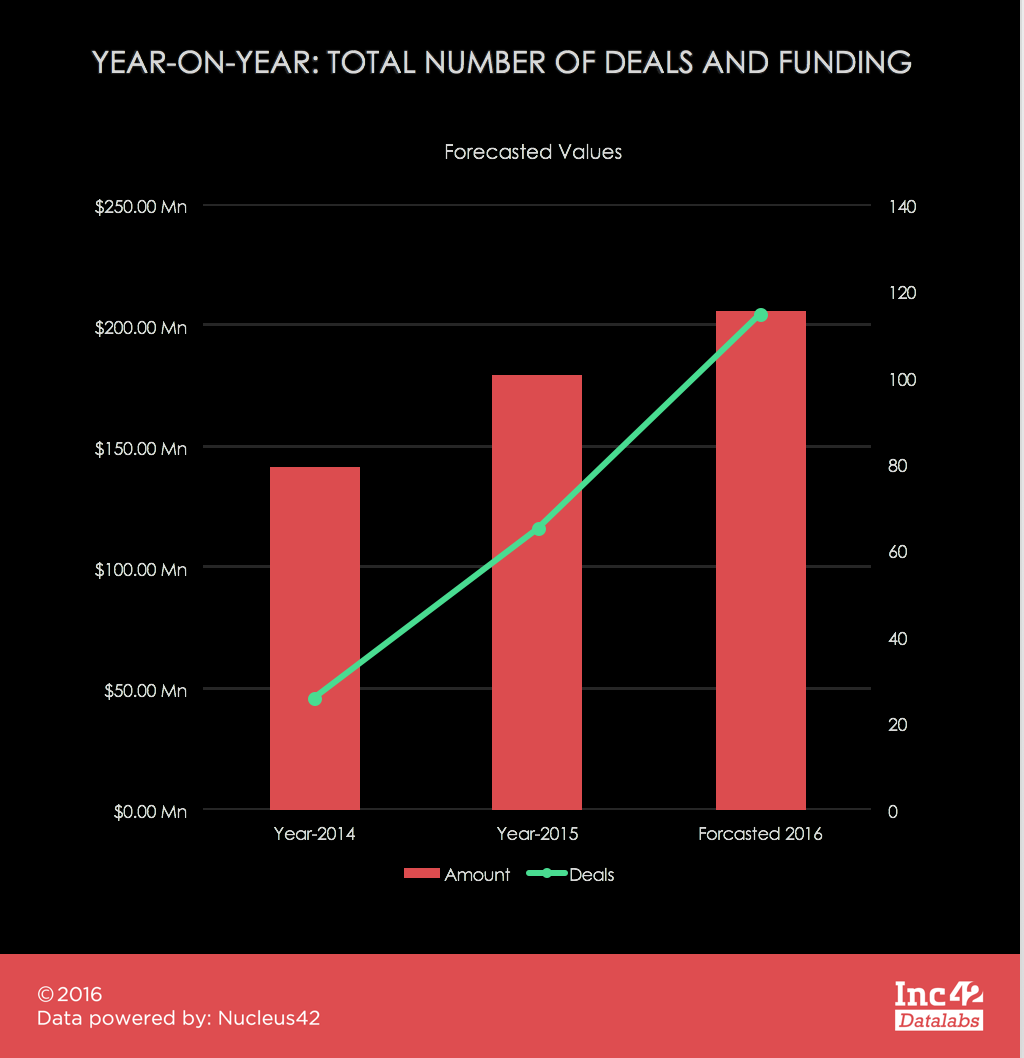

Now, forecasting the fourth quarter of 2016 gives us a complete overview of the investment in healthtech in India in the period of 2014 to 2016.

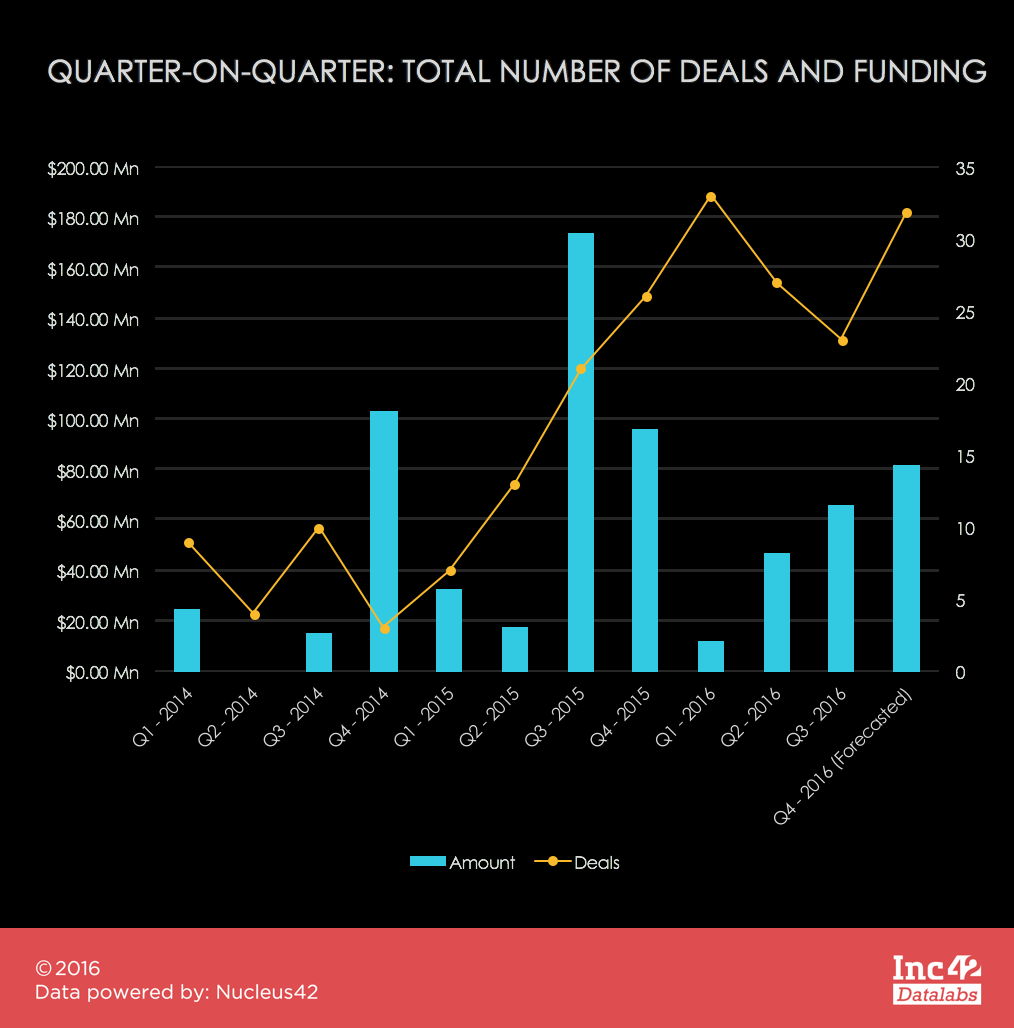

Although the year-on-year plot gives us a happy picture of an improving market for healthtech startups, the quarterly plotting shows a different scenario. The number of deals kept falling since the first quarter to the third of 2016. Whether, the real scenario meets the projections for the fourth quarter is yet to be seen.

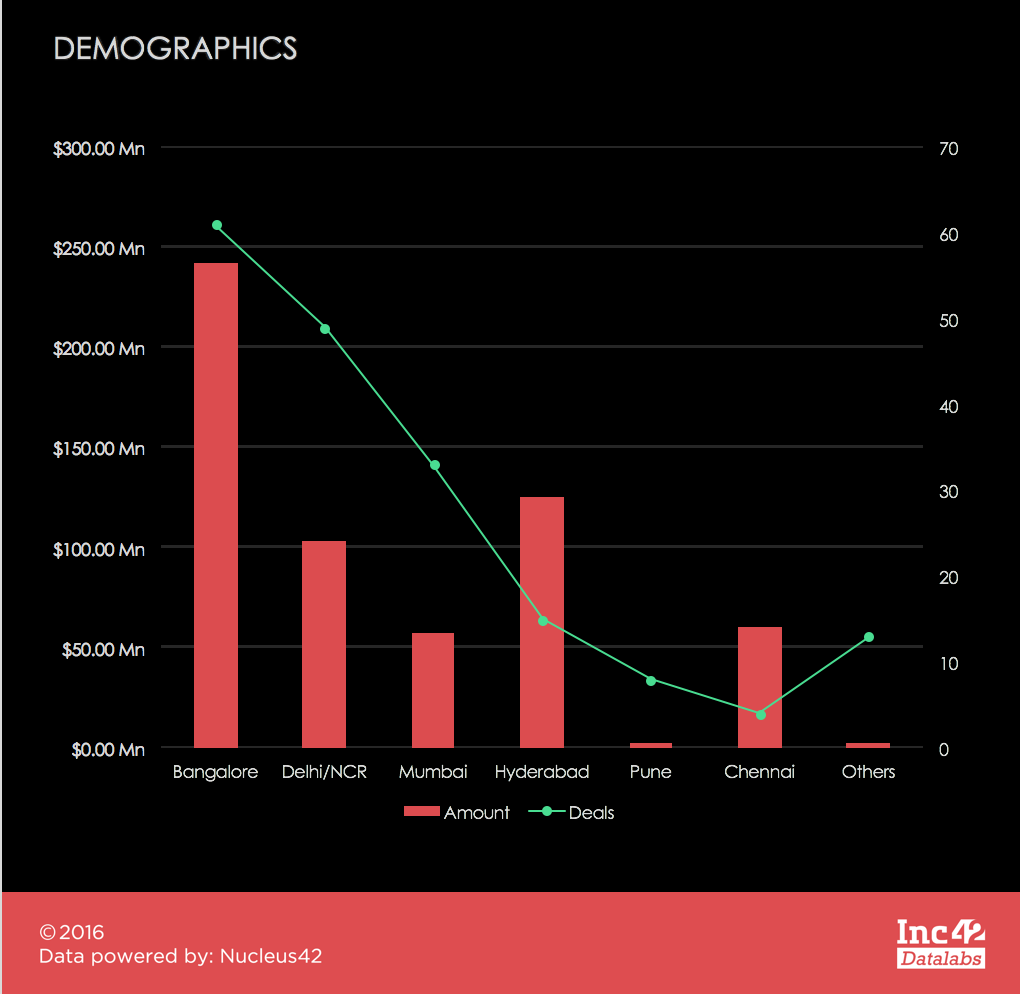

Demographics: Bengaluru Takes The Crown

Among the Tier I cities, Bengaluru has almost one-third of the total number of healthtech startups. Bengaluru being close to Chennai, the “Medical hub”of India, has greatly boosted healthtech market of the city.

Hyderabad, Pune, and Chennai are the upcoming Tier II cities for healthtech market.

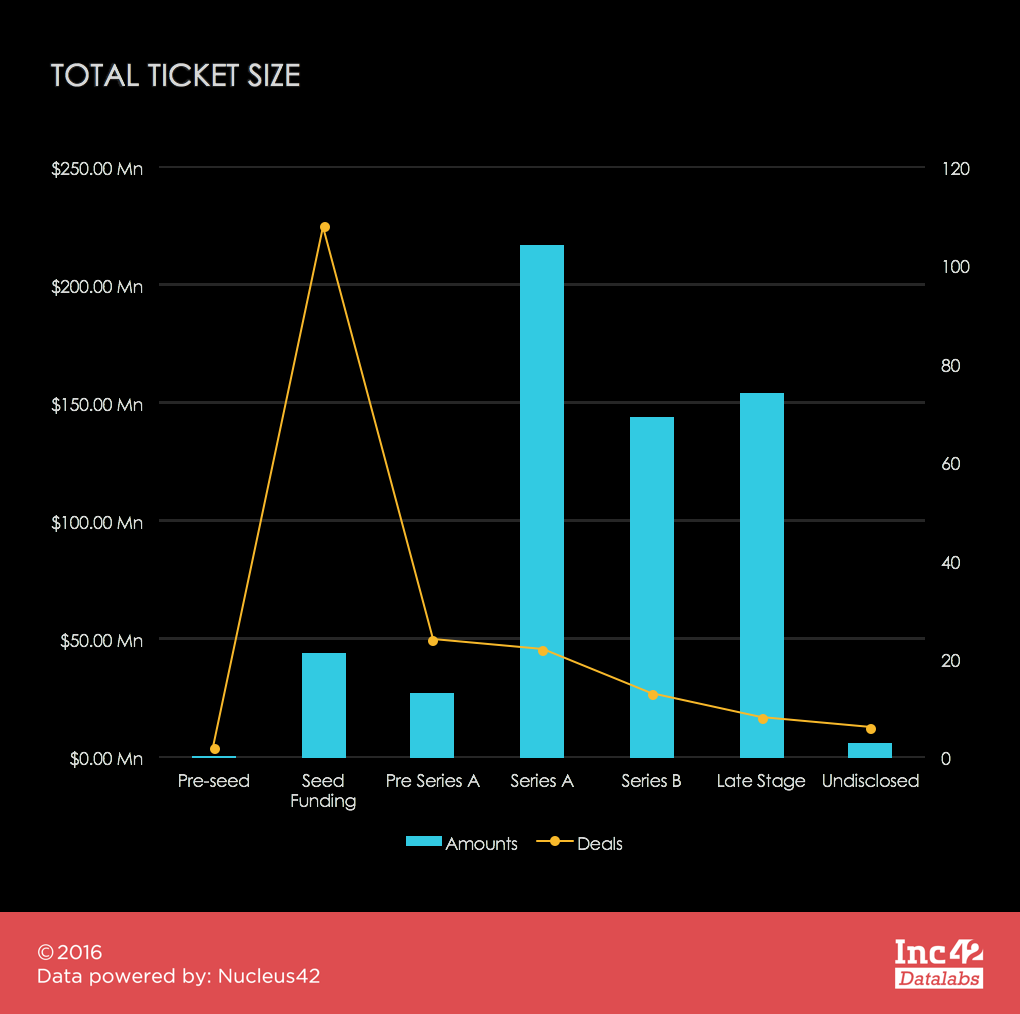

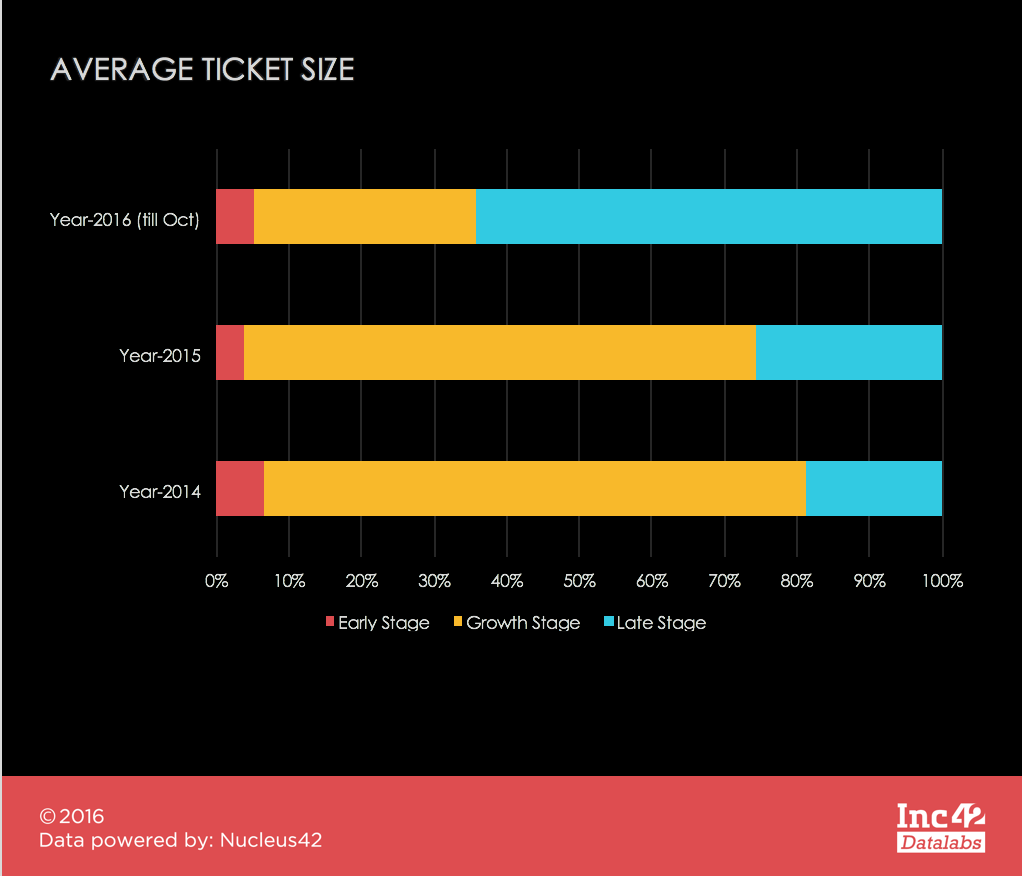

Stages Of Funding: Seed Funds Versus Series A

The distribution of deals and total funding in different stages remain as usual. 60% of deals were Seed funds bearing only 7% of the investment, while 37% of the investment were in Series A rounds.

A year-on-year observation suggests the same trend. However, comparing the ticket size of the stages over the three years gives us an interesting observation.

We describe “Early-Stage” as a combination of Pre-Seed, Seed, and Pre-Series A, “Growth-Stage” as a combination of Series A and Series B while the later stages have been clubbed into “Late Stage.” It is observed that the “Early-Stage”and “Growth -stage” ticket size has fallen down while the “Late Stage” ticket size has drastically increased.

This suggests that, in 2016, investors have been cautious in early-stage funding, given the market being spammed by too many “me-too” startups.

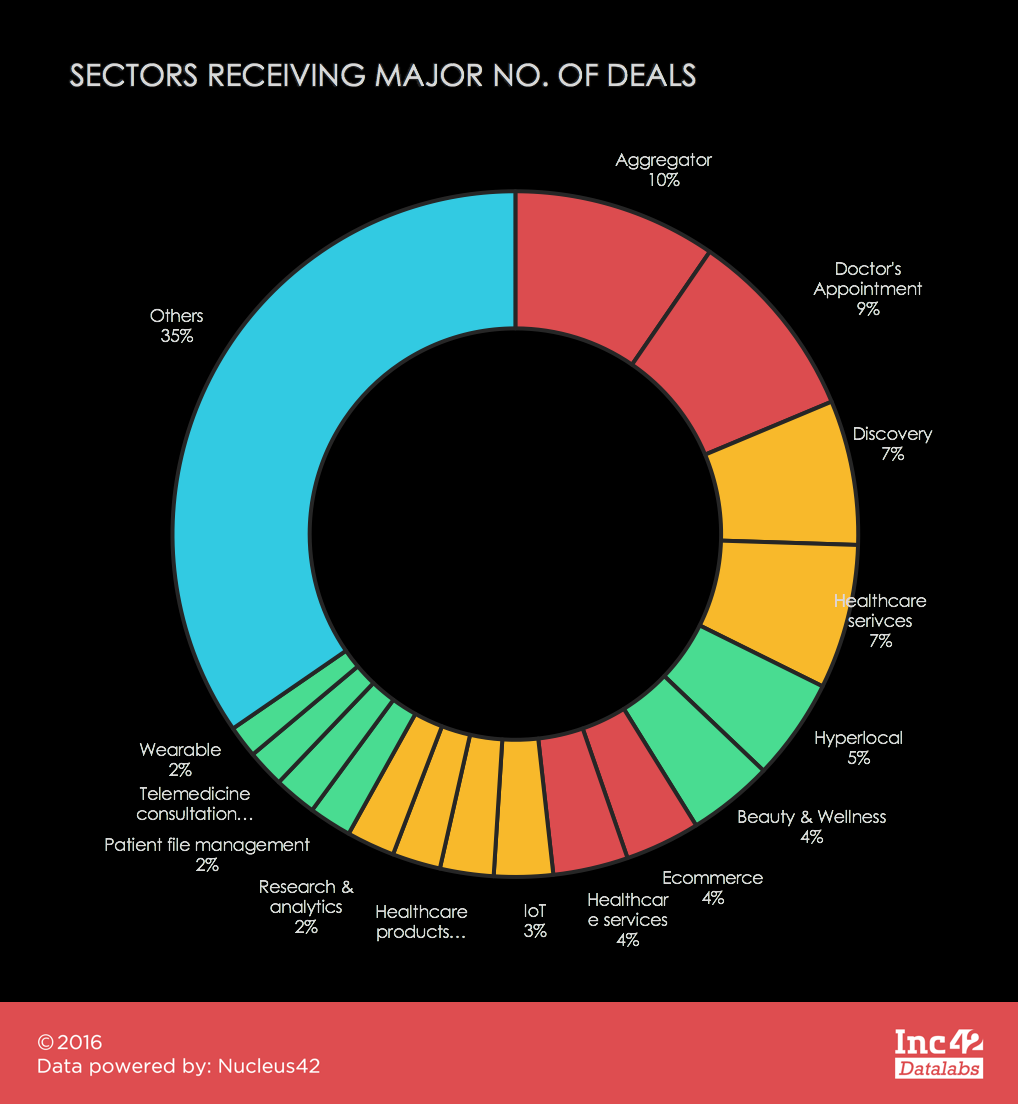

Market: Healthtech Saw 25% Investment

It could be fairly concluded in the case of B2C that entrepreneurs see the aggregation of services to be the solution to the unorganised nature of the market. About 25% of investment was made in this sector.

Major startups are focussed in aggregating doctor’s appointment, healthcare services, chat, discovery, patient file management, diagnostic labs.

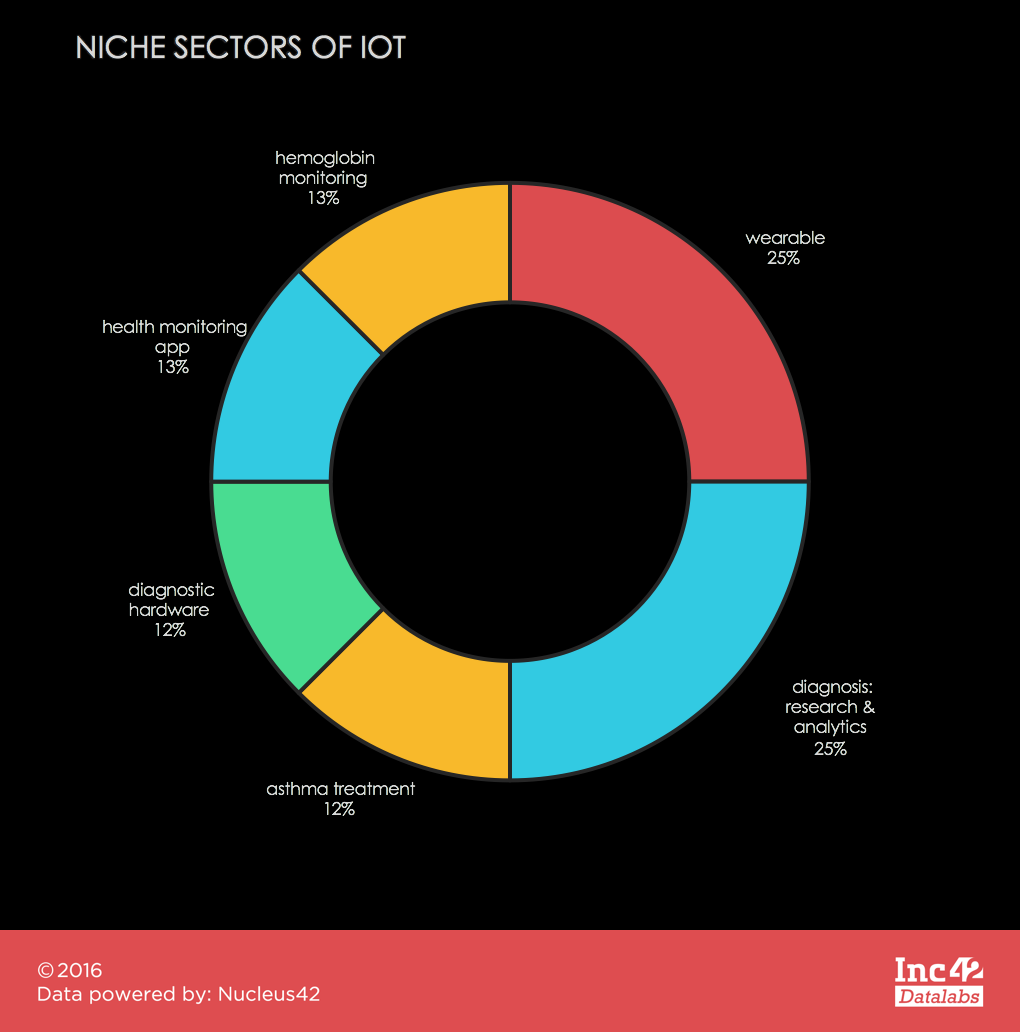

Although the number of startups is less and with only a few known players, IoT is becoming prominent in the healthcare sector. Following is a split of IoT startups working in various sectors of healthtech.

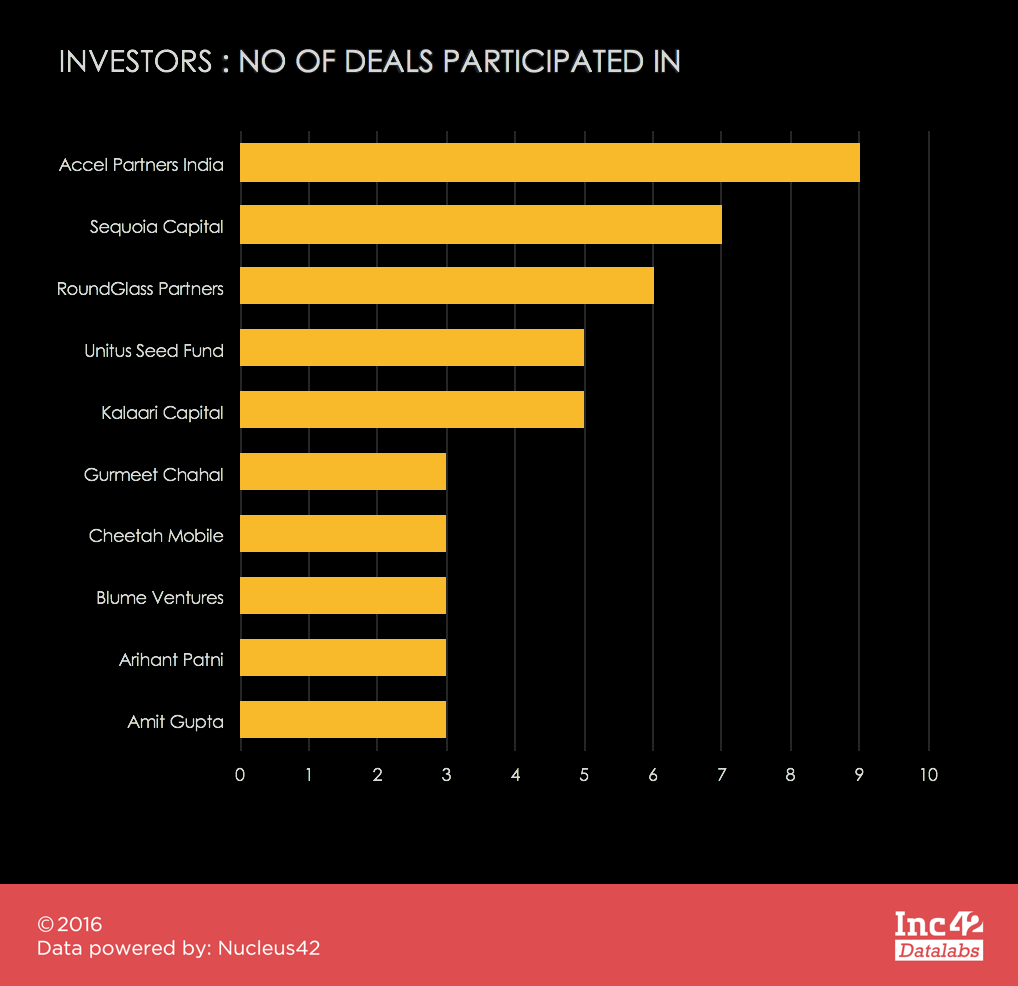

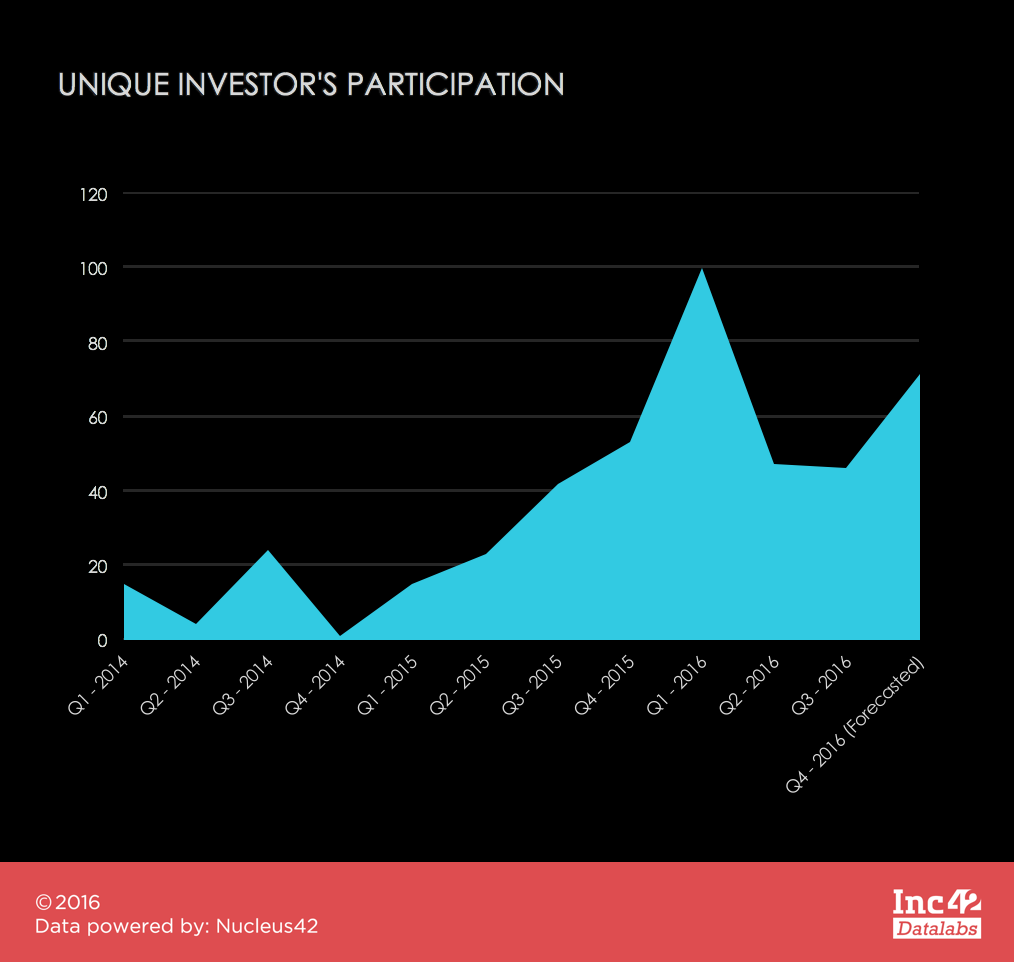

The major investors who participated in deals in healthtech are Accel Partners India, Sequoia Capital, RoundGlass Partners, Kalaari Capital and Unitus Seed Fund.

However, if we see the trend of investor participation in the funding rounds, the number has drastically fallen for 2016.

What’s Next

Although, the funding scenario and investor participation have fallen for healthtech the market is still unorganised and too large for it to be totally ignored. After the 2015 funding bubble burst, investors seem guarded to approach it with big tickets like for Practo, NetMeds and Portea. Although, 1mg secured $16 Mn in April 2016 but as compared to $90 Mn of Practo or $50 Mn for NetMed, the big tickets of 2016 have been too small and too scarce.

What’s next for healthtech, the direction it will take in 2017 and the moves that will be made by startups and investors alike is a wait-and-watch game for now.