How The Consumer Lending Startup Is Working To Solve The Problem Of Poverty Premium In A Credit Starved Country

From an IIT Madras engineering student to a Silicon Valley-based entrepreneur to a VC in Bengaluru, the journey of Bala Parthasarathy has been an exhilarating tale of ambition, resourcefulness and ingenuity. The high points of his career have been many, including the time he sold Snapfish to Hewlett Packard for a whopping $300 Mn as well as the year he spent volunteering at UIDAI under the Government of India. His stint as an investor, however, didn’t last long. Ensnared by the allure of entrepreneurship, Bala ventured into the promising world of fintech with MoneyTap, a consumer lending startup that was launched last September.

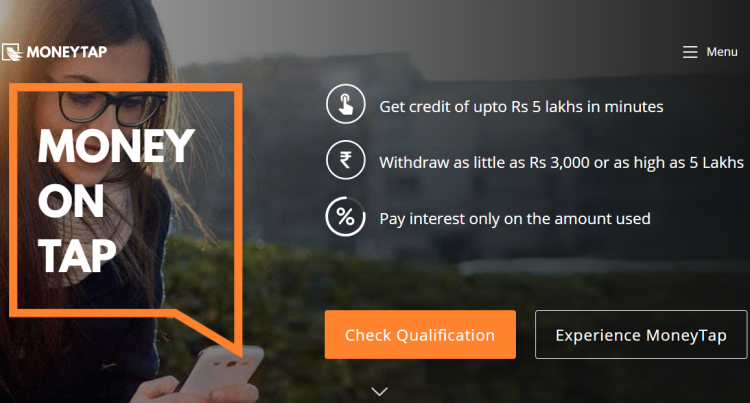

Touted as India’s first app-based credit line, the fintech startup is working to democratise credit in a country where 19% of the total population is still unbanked. So, what exactly is a line of credit (LOC)?

Think of it as having a personal cash reserve at your disposal. You can take money out whenever you want with just a tap of your finger, without having to go to a bank or filling out unnecessary forms. The credit line, Bala claims, is an innovative product that offers consumers flexibility not only in ticket size, but also in terms of payback duration. Once the borrowed amount is paid back, the money gets immediately replenished in the user’s account, no questions asked!

Since its launch in September 2016, MoneyTap has undergone substantial growth. Let’s look at some of its achievements over the last eight months:

The Story Of A Serial Entrepreneur: From Snapfish To MoneyTap

Bala has been part of over 20 startups in his career, most notably Snapfish which he co-founded along with Rajil Kapoor, Suneet Wadhwa, and Shripati Acharya. Started during the late dot-com era. The web-based photo sharing and printing service was sold to HP in 2005 for a staggering $300 Mn. Today, the site caters to more than 103 Mn users globally, has generated upwards of $900 Mn in revenue since its inception.

For Bala Parthasarathy, however, the thrill of starting up is akin to the euphoria of homecoming.

He also co-founded iSelect and Wyatt River Software, which was later acquired by SafeNet. Following the path that few NRIs have taken before him, Bala returned to India soon afterwards to start a Seed stage investment firm, Prime Venture Partners in 2014 (formerly known as AngelPrime), along with Sanjay Swamy and Shripati Acharya. The VC firm has invested in startups across diverse verticals, including HackerEarth, Nimble Wireless, digital payments solution provider Ezetap, and Happay.

For Bala Parthasarathy, however, the thrill of starting up is akin to the euphoria of homecoming. After two years at Prime Venture Partners, Bala returned to entrepreneurship once again, and this time with fellow techies, Kunal Verma and Anuj Kacker. And this is where MoneyTap’s journey began. Interestingly, Kunal and Anuj co-founded TapStart, a job discovery platform for consumers back in 2013. The duo managed to scale the company to over 300,000 users, before selling off their stake in the venture in September 2015.

“The reason we started MoneyTap was that we wanted to solve the problem of consumer credit. Clearly, India is very credit starved. Less than 1% of Indian consumers have access to any form of unsecured credit from a bank or any financial institution. Most people, whether it’s from middle class or lower middle class, need credit, but they have to use informal methods,” explains Bala.

MoneyTap Looks To Solve The Problem Of Insufficient Consumer Lending In India

During his stint at UIDAI, Bala Parthasarathy talked to a number of bankers and over 1,000 consumers in Mumbai about their experiences. He recalls, “Most of them did not even consider banks as a go-to option when they needed additional funds. Cumbersome processes, rigid products and complete lack of transparency were their main reasons to avoid banks completely. This was strange in some ways since banks are one of the most trusted brands in the country; after all, we trust them with all our savings.”

He calls this the “poverty premium”, which refers to the peculiar problem wherein those who earn less seem to pay a higher fee for accessing certain financial services, though they may be more creditworthy than the rich. Based on his interactions, he concluded that there are four main reasons behind this pervasive inadequacy of consumer credit in the country:

- Historical baggage/legacy

- Lack of data

- High overhead in small-ticket loans

- Finally, the emergence of a new class of demanding consumers

Between 2003 and 2007, a number of banks in India were issuing loans without doing any detailed checked. At the time, there was no credit bureaus or Aadhaar. Even PAN was not widely used. When the subprime crisis hit in 2008, all these banks got burned. In the period prior to that, around 24 Mn credit cards were sanctioned in India, of which nearly 10 Mn crashed.

In the aftermath of the collapse, banks became very conservative, making the process of procuring loans all the more difficult. Even getting credit cards became challenging. Although the sector has witnessed impressive growth in the decade since the financial crisis, this historical baggage, Bala Parthasarathy believes, this continues to be one of the main reasons for the lack of sufficient consumer credit in the country till date.

During the financial crisis of 2007-08, subprime lending was often supported by very little verifiable documentation and credit checks. The originators of the subprime mortgages served only intermediaries that did not have any “skin in the game”. Lenders, on the other hand, had to rely on third-party credit ratings and assessment that were at times unreliable. In India, the lack of verifiable data about loan seekers, such as employment status, income, a company’s debt-to-equity ratio, etc. continues to handicap the banking sector.

In a country with a population of over 1.31 Bn, only 220 Mn people have PAN cards. Other forms of KYC (know your customer), including voter ID, Aadhaar and ration cards are not considered as the sole identity proof, especially when it comes to financial activities. Credit information companies (CIC) – such as TransUnion Credit Information Bureau Ltd. (CIBIL), Experian India and Equifax India – still do not have records of a large section of the country’s banked populace.

The third reason is more fundamental and has to do with the process of loan disbursal itself. As per Bala Parthasarathy, the cost of evaluating and issuing a credit line/loan/credit card for a bank is extremely high and thus they prefer to give big-ticket loans to few people rather than small ticket loans for a large group of people. The average loan ticket size in this country is between $4,629 – $7,715 (INR 3 Lakh-INR 5 Lakh). At such a high level, the overhead is still bearable for the banks.

If you think of India as a pyramid in terms of the net worth of people, all these banks focus on only around 12 to 15 Mn customers at the top of the pyramid because they are capable of applying for a loan worth $4,629 to $7,715. The problem, according to him, arises when someone wants a $463 (INR 30,000) loan because the overhead, in this case, is too high for the bank to make any profit.

With the arrival of big consumer companies like Flipkart, Amazon and Reliance Retail in recent years, the consumer has also become more demanding. While the banks have become more conservative, consumer expectation has skyrocketed. People today expect ultimate flexibility and stellar customer service. For a product like money, customers demand even more flexibility, which has inadvertently made the availability of easy consumer credit line more difficult. This, Bala believes, is the fourth reason behind the acute shortage of consumer lending.

Developing A Technology That Provides Hassle Free Personal Credit Line

MoneyTap’s proprietary technology strives to solve this problem of insufficient consumer credit line by targeting the country’s fast-growing middle-income group who needs money for shopping, paying school fees, rent, weddings, birth and death, medical emergencies, sending money to family and so on.

The consumer lending startup claims to currently cater to customers with monthly income ranging between $308-$1,080 (INR 20,000-INR 70,000). Parthasarathy adds, “Someone who is earning that kind of money and living in any one of the 14 cities that we operate in is actually always short of money.”

When it comes to the unsecured credit line, Bala believes, there are three primary things the consumer wants. Firstly, there is convenience and ease of use. Secondly, flexibility in ticket size is equally important and can be as low as $46. Lastly, customers want flexibility when it comes to payback as well, be it two, four or six months. Bala Parthasarathy goes on to add, “They don’t want to get locked into a long-term loan, which is something the bank typically does. That’s why we came up with the idea of credit line. Credit line is a super flexible product.”

On the MoneyTap platform, consumers can borrow anywhere between $46-$7,715 (INR 3,000 to INR 5 Lakh) with an option to choose the repayment duration from as little as two months up to three years. When a user downloads the app and applies for a loan with one of the company’s banking partners, he/she gets assigned credit limit, depending on the eligibility criteria. The consumer lending startup’s main selling point, according to Bala, is that it provides consumers with a personal line of credit to be used whenever and however they want. If they don’t use up the specified limit, users don’t pay any interest.

Real-Time Credit Assessment In Under 15 Minutes

Once a user downloads the app, after answering the set of questions to a chatbot, the user is informed upfront whether he/she is eligible for a credit line. “But if you are eligible, we evaluate your creditworthiness by collecting a bunch of information like your salary, employment status, etc. We also do a credit bureau check. In some cases, we pull your bank statement to understand what your track record is,” answers Parthasarathy on the topic of credit assessment.

He further claims that the entire process of credit evaluation takes around 3 to 7 minutes, depending on how fast the customer types. Unlike other consumer lending platforms, credit assessment on MoneyTap happens in real time.

The loan agreement is finally reviewed by the bank that has partnered with MoneyTap. The consumer lending company is currently working with seven banking/NBFC partners at different stages of integration, including the RBL Bank. Once the bank gives its approval, the credit line is set up almost immediately in the name of the customer. Although real-time credit assessment sounds a bit too risky, Parthasarathy maintains that the platform’s average default rate is much below 1%.

As revealed by the founding team, the platform differs from the competition on another count as well. Bala states, “The essence of the product lies in the one-time credit assessment. So once your profile is approved, your loan requests are approved automatically. It is a one-time process via the app. After that, the money is yours. If you don’t use it, you don’t pay any interest rate. When you do need the money, all you need to do is press the button on the app and the amount will be transferred within 15 seconds.”

At present, MoneyTap charges a one-time setup and origination fee of $7.7 (INR 499) plus tax. Repayment on the platform is done through EMIs. So once the credit is availed, the “meter” starts ticking. The next month, the customer gets a bill for the EMI. When the amount is repaid, the user’s credit limit is raised again.

Why MoneyTap Chose To Partner With Banks & NBFCs

Compared to credit card interest rates which typically range somewhere between 3% and 4% per month, the interest rates charged by the MoneyTap app are just over 1.5%. According to Bala, there are two reasons the consumer lending platform manages to offer low-interest rates. The first reason has to do with the fact that the cost of capital for a bank is the cheapest in the country.

Bala adds, “This is the fundamental difference between P2P lending companies and MoneyTap. Because we have partnered with banks, we have access to cheap capital. If you are partnering with individual lenders as is the case with P2P lending companies, the investors will likely demand interest rates between 18% and 20%. The platform itself has to ask for higher rates because of all the costs of KYC, origination etc. So, the reason for our low-interest rates lies not with us but in our partnerships.”

Secondly, Aadhaar has helped bring down the compliance costs of fintech and consumer lending companies in India to a great extent. The launch of the digital stack, as well as demonetisation, has made KYC much easier and more transparent. Parthasarathy states, “Overall, the emergence of the digital stack and demonetisation helped greatly in increasing the awareness of digital payments as well as lending/borrowing.”

From Zero To 300K Users In Less Than Eight Months

Since its launch in September 2016, MoneyTap has grown by leaps and bounds. In less than eight months, the platform has gone from zero to 300K registered users across 14 cities in India. While a certain percentage of the growth has come organically, the company currently relies on several marketing channels at present, including Google, social media and content marketing, to onboard new customers.

With a small office in Mumbai and a head office in Bengaluru, MoneyTap’s present workforce comprises 30 people. The number, the founders believe, will likely double in the next year or so. They state, “Our plan is to expand in a tech-enabled way, which means we don’t need to have more footfalls in the street or for that matter, more offices. The “feet on the street” is required only for two things: collection and KYC, both of which in our case the banking partners handle. We will be operationally present in 100 cities, but physically we are likely to be present in a lot of cities.”

In June 2017, MoneyTap raised $12.3 Mn in a round led by Sequoia India, New Enterprise Associates and Prime Venture Partners to drive the expansion of its app-based consumer credit line in India. The funding, as stated by Bala, has also helped strengthen the leadership position of the consumer lending firm by improving credit accessibility for other segments of customers.

Tackling A Myriad Of Challenges From Acquiring Capital To Appeasing Demanding Customers

According to Bala Parthasarathy, the most challenging thing in the consumer lending business is acquiring capital at low costs. Players in this sector have a couple of options. They can either lend from a P2P network, raise debt or equity for a company, lend one’s own money or lend the bank’s money.

The MoneyTap co-founder explains, “From a borrower point of view, P2P is not viable because of its high-interest rates. Raising equity capital, on the other hand, is not very scalable either because you can only raise so much before diluting the company. The third option is to raise debt, which is mainly for established entities and not for startups. This means that the money has to come from a bank or an NBFC. And working with a bank or an NBFC is not easy because you have to comply with their rules and regulations.”

Banks are conservative, but also have the most money in the country. Finding a balance in the relationship, Bala claims, has been quite taxing. The other challenge has been working with demanding customers. Consumers today want stellar experience, in terms of speed, flexibility and reliability. To meet the customer’s demands while working within the strict structure set by the banks is extremely difficult, especially for new startups. The funding, Bala adds, was raised to develop solutions geared towards bridging the gap between these two ends of the spectrum.

Future Plans: Hitting Unit Economics Profitability In 12 Months And More

The consumer lending startup is aiming to disburse credit line worth about $46.2 Mn (INR 300 Cr) by the end of the current fiscal year. While hitting profitability is not one of the company’s main goals at the moment, Bala is more focused on touching unit economics break-even by March 2018. He adds, “We’ll hit unit economics profitability by July 2018. We are not shooting for company profitability right now. Our concern is to make sure our product is profitable in the unit economics metrics.”

Although there are many players in the field, competition, Bala claims, is not something MoneyTap is too concerned about. He goes on to say, “Our focus, therefore, is not on thwarting competition, but on growth and integration. Our goal is to hit unit economics profitability within the next six to 12 months. There is no question of whether there is a market or not. The challenge is acquiring capital, for which the banks are the best sources. And the banks are very eager to work with us because they are also looking to deploy capital at a low price. We give the tech facility to banks. Our biggest selling point is our product.”

The credit line, Bala Parthasarathy believes, is fairly significant technology in itself. The frontend of the app is only a small portion that customers can see. The backend, data compliance system, integration with the banks are all driven by advanced, highly-specialised technologies. As revealed by Parthasarathy, MoneyTap has already filed patents for five of its proprietary technologies.

Armed with a powerful technology-enabled system, the team at MoneyTap is gearing up to lend more than $1 Bn worth of credit line in the coming three years. Additionally, the consumer lending company is looking to expand operations across 100 cities within the next two to three years. The immediate goal is to reach 30 new cities in 12 months. On the topic of acquisition, Bala answers, “We might acquire companies that share our values. But, we are not actively looking for acquisitions. The way we look at it is that there are a billion consumers in the country, 1% of whom we serve. If we can double that to 2%, we have a huge win.”

Editor’s note

According to Bala Parthasarathy, when studying the consumer lending market in India, one needs to look at the markets in China and the US, respectively. The market in the US is very unlike India. The US is very saturated in terms of consumer credit. China, on the other hand, is a P2P lending paradise. The scenario in that country is a bit different. “What usually happens in China is that there is wild growth initially, but they crash very quickly and drastically, as can be seen with the P2P model,” adds Bala.

India lies midway between these extremes. Although relatively young, the fintech market is undergoing a phase of rapid growth and is forecasted to cross $2.4 Bn by 2020, as per reports by KPMG India and NASSCOM. India is currently home to more than 500 fintech startups. According to Inc42 Data labs report, alternative consumer lending startups have already attracted $220.66 Mn in funding between 2015 and 2017, which accounts for around 2.5% percentage of the overall fintech funding of $2 Bn during the said period. The growth has been, in part, the result of the launch of India’s digital stack – Aadhaar, eKYC and digital payment services (including UPI and BHIM), demonetisation as well as favourable government policies.

Despite the sector’s phenomenal growth, unsecured personal loans currently constitute only 4% of all loans in India, as per a Reuters report. Although technological advances have managed to bring down loan delinquencies to a great extent, the risk has not been entirely eliminated. In addition to the risk of default, consumer lending startups like Bala Parthasarathy co-founded MoneyTap have to tackle the dichotomous relationship with banks. For MoneyTap, the challenge, therefore, lies in ensuring stellar customer experience as well as protecting the bank’s money, while at the same time thwarting competition from a growing class of alternative lending platforms such as Lendingkart, Capital Float, Rubique, Innoviti and Indifi, among others.