SUMMARY

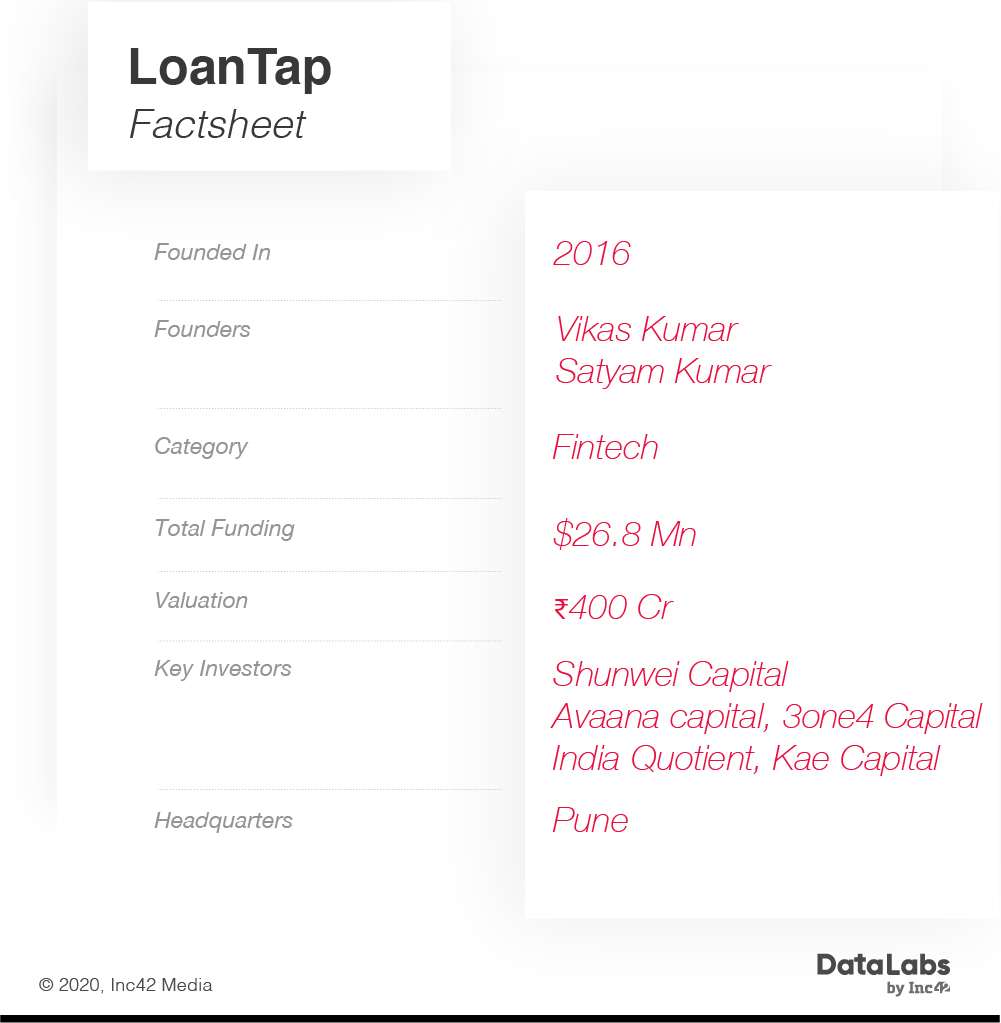

LoanTap was launched in 2016 with an aim to revolutionise personal loan segment by solving the friction points for consumers

The company claims to be profitable with 4X revenue growth in the last fiscal with massive traction in metro cities

Five years from now, founders foresee deeper presence in Tier 2 and 3 cities and beyond

“As someone who has been in the banking industry for more than 15 years, I have been familiar with the shortcomings in the traditional lending sector. So, there isn’t one but multiple experiences that urged us to launch LoanTap.” Satyam Kumar, cofounder and CEO, LoanTap.

The first signs of change in the Indian payment ecosystem appeared on the scene post the formal commencement of operations of the National Payment Corporation of India (NPCI) in 2009. Fast forward to 2015, the average Indian consumer was aware of digital payments and a small fraction of users had started utilising digital payment instruments like credit/debit cards, IMPS, USSD, RTGS, NEFT, and digital wallets.

Once payments went digital after 2016, entrepreneurs started looking for gaps and shortcomings in other areas of financial services, marking lending another sector ripe for disruption. The traditional financial institutions (FIs), with its own limitations, were not an easy place to borrow credit.

Consumers had to jump through several hoops — from documentation hassles to assessment of creditworthiness to long turnaround times, which made it impossible to get loans in an emergency. And when you did get them, they were vanilla personal loans — one size fits all — no matter the specific need. These several gaps meant lending startups could find a niche by solving for one or many problems.

“Our market research also pointed out that a majority of barriers to credit penetration could be easily countered by leveraging an array of technologies and non-conventional data repositories, especially with reference to salaried professionals,” said Kumar.

Although we have a plethora of lending players now in both business and consumer segment, considering the period between 2015-2016, this was a significant opportunity to pursue.

“We wanted to redefine the retail asset distribution model by eliminating the information gap between lender and consumer. So, we integrated our respective specializations in retail loans and technology domains to create a consumer-friendly credit facility in the competitive fintech space and hence LoanTap was established,” he added.

LoanTap: Key Products And Growth So Far

LoanTap has customer-centric products such as rental deposit loans, EMI free loans, salary advance and a personal overdraft. These products are designed to meet different life needs of the customer.

It also offers a differentiated product stack of end-use based products such as wedding loans, holiday loan, rental deposit loan as well as flexible loans like personal overdraft, credit card takeover loan, which gives more financial control in the hands of the borrower.

“With changing times and changing needs of customers, there is a demand for customised products for end-use ranging from holiday, buying a luxury bike or wedding. Thus, there are different factors affecting loan origination and therefore their repayment cycle should also be different,” said Kumar.

Technology At Play At LoanTap

In India, one of the major challenges is the evolving regulatory situation and this is true for lending too as it is for other fintech models. “Besides this, in the last 12-15 months, India and specifically its NBFC sector have seen unprecedented levels of liquidity squeeze, which has separated the boys from men,” said Kumar.

This requires companies to build their processes in a manner that they can smoothly accommodate the new changes. A major role here is thus played by the technology-induced at the backend processes.

As claimed by Kumar, LoanTap has maximised the use of technology to enhance all processes, from credit origination to the final loan disbursal, thereby ensuring that a loan reaches every applicant within 24-36 hours of the initial loan application.

“We use technology to deliver smart and innovative products for millennials. Our flagship product – EMI Free Loan provides the flexibility of payment to customers along with 40% lower monthly instalments as compared to regular personal loans,” he added.

LoanTap has also developed an in-house lead origination and loan management system called Finsome. This software ensures seamless data flow from lead origination, customer set management and lead processing, loan management, credit processing, disbursement to post disbursement care.

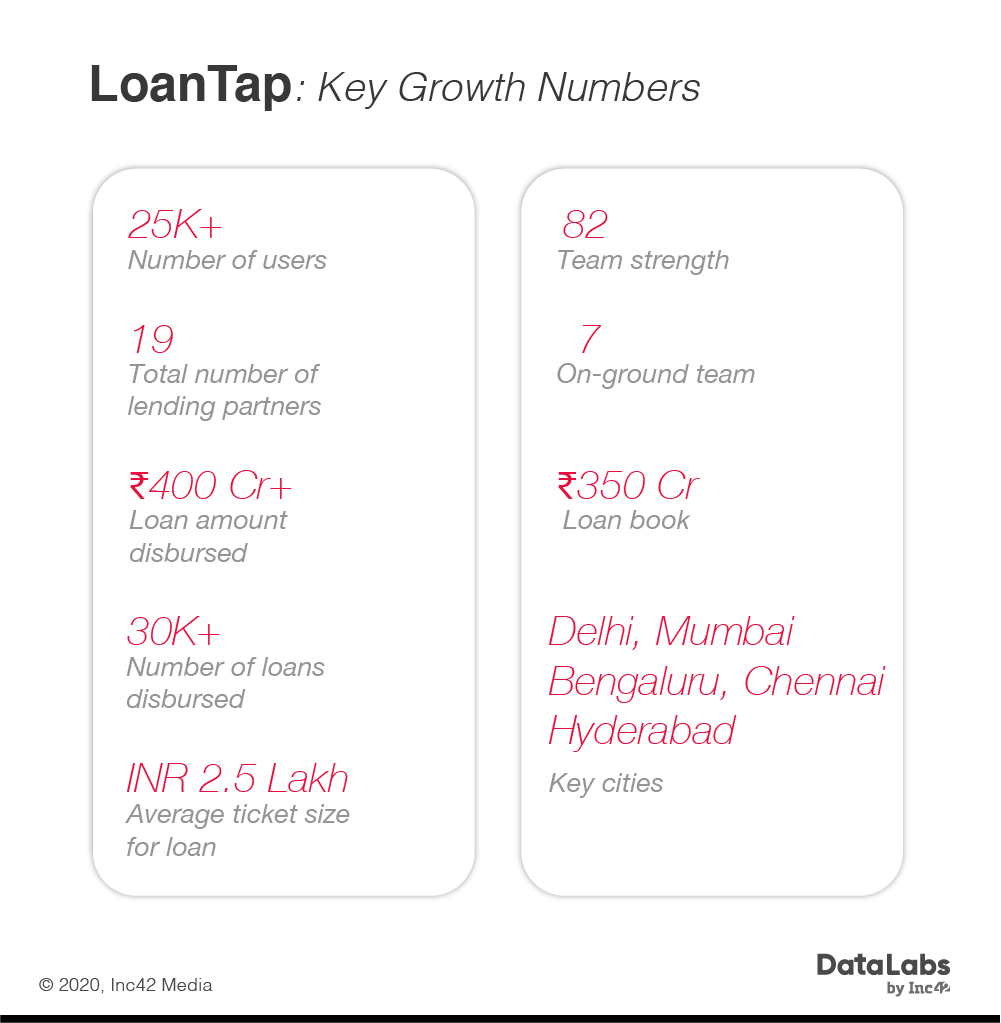

“Till date, we have serviced more than 25000 + customers and have received high appreciation for our services,” boasted Kumar.

Personal Loans: A $1 Tn Opportunity To Tap

The personal loan market is expected to reach a size of $1 Tn by 2025. However, as large is the opportunity, so is the players tapping for a significant share. This includes both the deep-pocketed players like MoneyTap, CreditVidya, PayMeIndia, Capital Float, ZestMoney, IndiaLends, Incred, MoneyTap, PaisaBazaar and the new age players like Earlysalary, Finzy, Shubhloans among others.

A lot of players are now also moving towards the tier 2 and tier audience, while further diversifying their offerings in a relative manner. LoanTap is no different.

Although, the company is currently focussed on the urban demand coming from salaried professionals with its business footprint across 20 cities in India. “Five years from now, we can see ourselves making deeper inroads into tier2 and tier 3 markets and diversify our loan offerings based on customer requirements,” said Kumar.