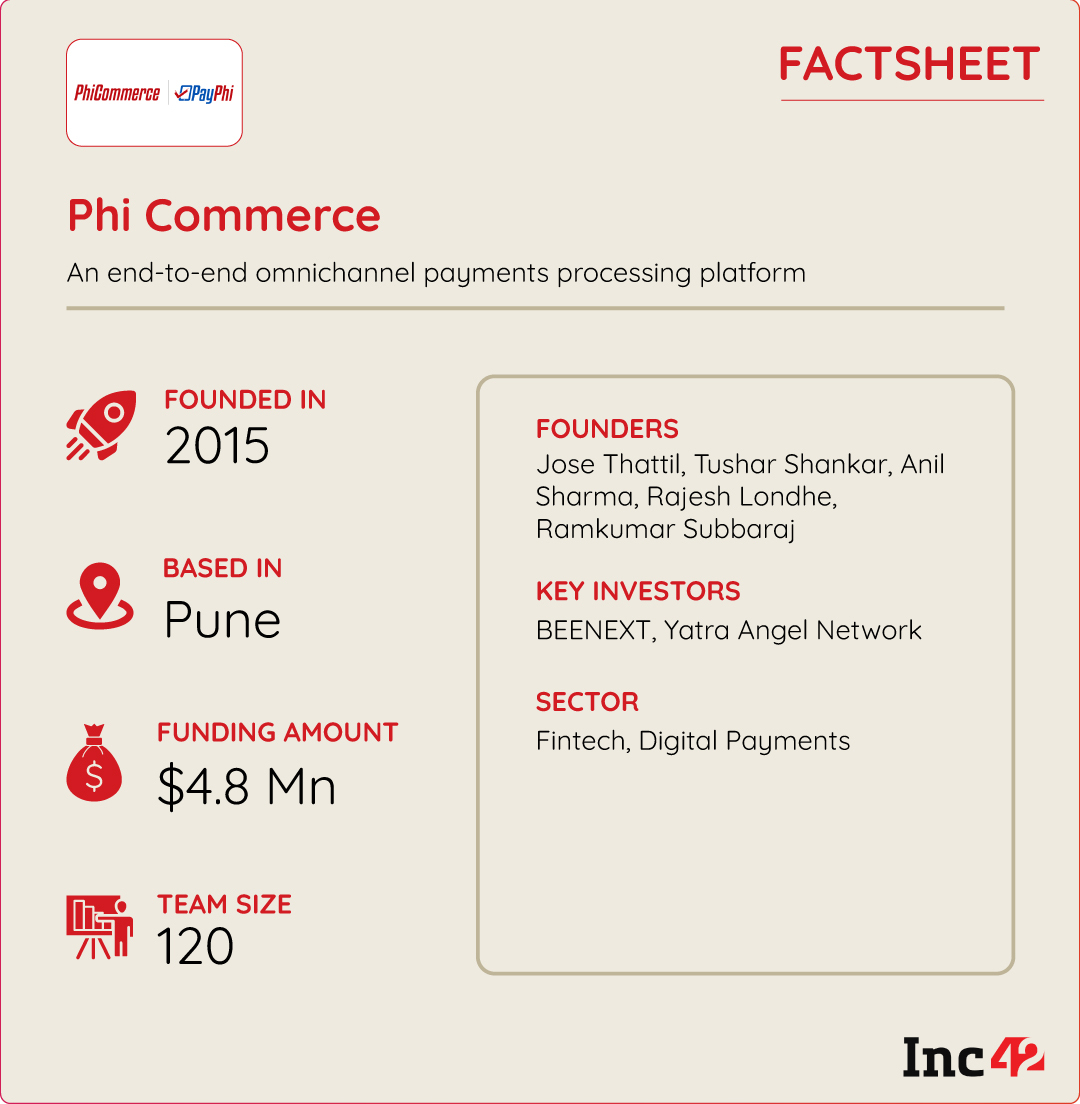

Seven years old Phi Commerce aims to tap India’s $10 Tn digital payment industry by helping enterprises keep track of multiple payment touchpoints and locations via a single dashboard

The platform has so far onboarded close to 1,200 mid to large institutions, which has helped it to build a network of 16K merchants and facilitate 4 Bn transactions

Phi Commerce plans to expand globally in the next two to three years, starting with Southeast Asia and eventually moving to the Middle East and the EU

It was early 2015 when Mastercard acquired ElectraCard Services, a global payment solutions firm based in Pune. The takeover also prompted five senior employees of ElectraCard to quit their corporate jobs and venture into the world of entrepreneurship. India was already flooded with creative startups.

But the five of them – Jose Thattil, Tushar Shankar, Anil Sharma, Rajesh Londhe and Ramkumar Subbaraj – decided to explore the fintech space further and came up with Phi Commerce to democratise digital payments and make them seamlessly accessible across the country.

It was a bold step, as India was still a robust cash-based economy, and neither ‘demonetisation’ nor the subsequent influx of digital payments had swept the country at the time. But during their 15-year stint with ElectraCard, the founders deployed digital payment solutions to as many as 23 countries and knew that Indians would soon follow suit.

“We also realised that payment platforms and payment processors continue to work in silos almost everywhere. There was no one-stop solution for organisations to process, reconcile or track payment transactions from multiple channels,” said Thattil.

Identifying The Pain Points Of India’s Digital Payment Ecosystem

India’s digital payment industry is estimated to become a $10 Tn opportunity by 2026, according to a joint report by the Boston Consulting Group (BCG) and PhonePe. From prepaid instruments and credit/debit cards to NEFT/IMPS/RTGS, UPI, QR code, PoS and Aadhaar-based payments – more than 15 digital payment systems are now active in India, as per the RBI’s 2022-23 annual report. These systems allow businesses to receive payments through multiple channels, be it online, mobile or in-store transactions.

By and large, such diverse payment options have benefited both customers and businesses. But enterprises are still struggling to incorporate and integrate all available payment options in a simplified, cost-effective way.

Moreover, businesses today are increasingly adopting an omnichannel approach (an online-offline hybrid model) to maximise their reach and RoI, while tech-savvy customers are leveraging the same to cash in on best deals and other benefits. However, keeping track of multiple payment touchpoints and locations via a single dashboard remains a key pain point, especially for mid-to-large enterprises without any core expertise in digital payment technologies.

“No business can become big by solely focussing on the developed cities, particularly in India. They must go across the length and breadth of the country, serving a wide range of customers. And digital payments will be the backbone for such seamless operations,” emphasised Thattil.

Pune-based Phi Commerce aims to solve these glitches with its end-to-end digital payment processing platform and full-stack omnichannel solutions for businesses, banks and payment networks like Visa, Mastercard and UPI. It currently caters to more than 10 industry sectors, including fuel, telecom, utilities, real estate, education, retail, ecommerce, logistics and travel, among others.

In simple terms, Phi Commerce aggregates all payment systems available in India and provides access to merchants across sectors, with several value additions.

The platform has so far onboarded close to 1,200 mid to large institutions, which has helped the company to build a network of 16K merchants and facilitate 4 Bn transactions. Thattil also claims that the startup has partnered with the top three private sector banks in India and recently bagged a contract from the Bengaluru airport. Phi Commerce will manage the payment operations of all airport businesses as part of its integration and deployment services.

Finding A Blue Ocean For Go-To-Market

When Phi Commerce was launched in late 2015, Thattil knew that building an omnichannel payment stack for enterprises would take at least four to five years.

“But we could not wait that long as the opportunity cost was too high. So, we decided to find a blue ocean for our go-to-market strategy. To be precise, it was cash on delivery (CoD),” he chuckled.

At the time, more than 80% were CoD orders on major ecommerce platforms, and customers were paying in cash after doorstep deliveries. Again, companies like Amway, specialising in direct sales and multi-level marketing or MLM, were bound to accept cash payments. Overall, it was quite chaotic, and for months, the founders travelled with sales and delivery executives across cities to understand the key issues enterprises faced while handling CoD orders.

“A key issue was the non-availability of customers who should be present to pay for their CoD orders. Sometimes, people forgot to keep the money at home as orders were expected later. Others forgot their credit/debit card PINs even when delivery executives had card machines with them for convenience. In most of these cases, orders were returned to the companies concerned,” explained Thattil.

It turned out to be a golden opportunity for Phi Commerce.

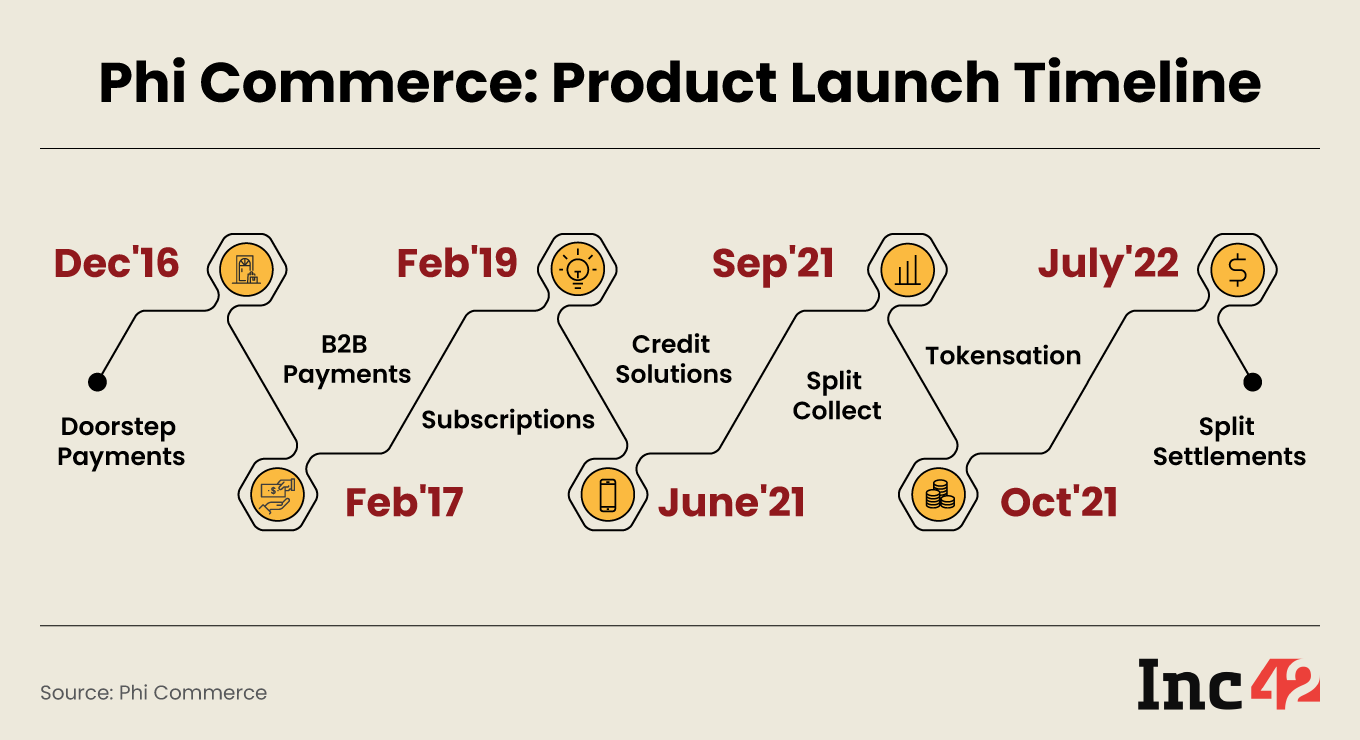

By December 2016, the team introduced PayPhi Doorstep Payments and empowered delivery executives with a software kit that allowed them to generate payment links even at locations with no mobile internet connectivity.

Subsequently, the PayPhi platform was enhanced to cater to other payment methods like wallets, credit and debit cards, dynamic UPI QR codes, biometric, netbanking, IMPS, RTGS and NACH for a truly seamless experience. For the first time, all fragmented payment options were consolidated into a convenient, user-friendly interface.

With the UPI rollout in 2016 and the demonetisation drive in November of that year, the module was further improved, and another API was added to generate dynamic QR codes. This allows delivery executives to collect doorstep payments digitally without an internet connection.

Fast forward to 2023, and one will find more feathers in Phi’s cap. It has now expanded to a 120-strong team and rolled out seven products for the doorstep and B2B payments, subscription, lending, tokenisation, split collect, split settlement and more.

In FY22, the startup clocked an operating revenue of INR 27.54 Cr, more than a 5x rise from INR 4.28 Cr in the previous financial year, according to company filings. Phi Commerce has not filed its FY23 financials yet.

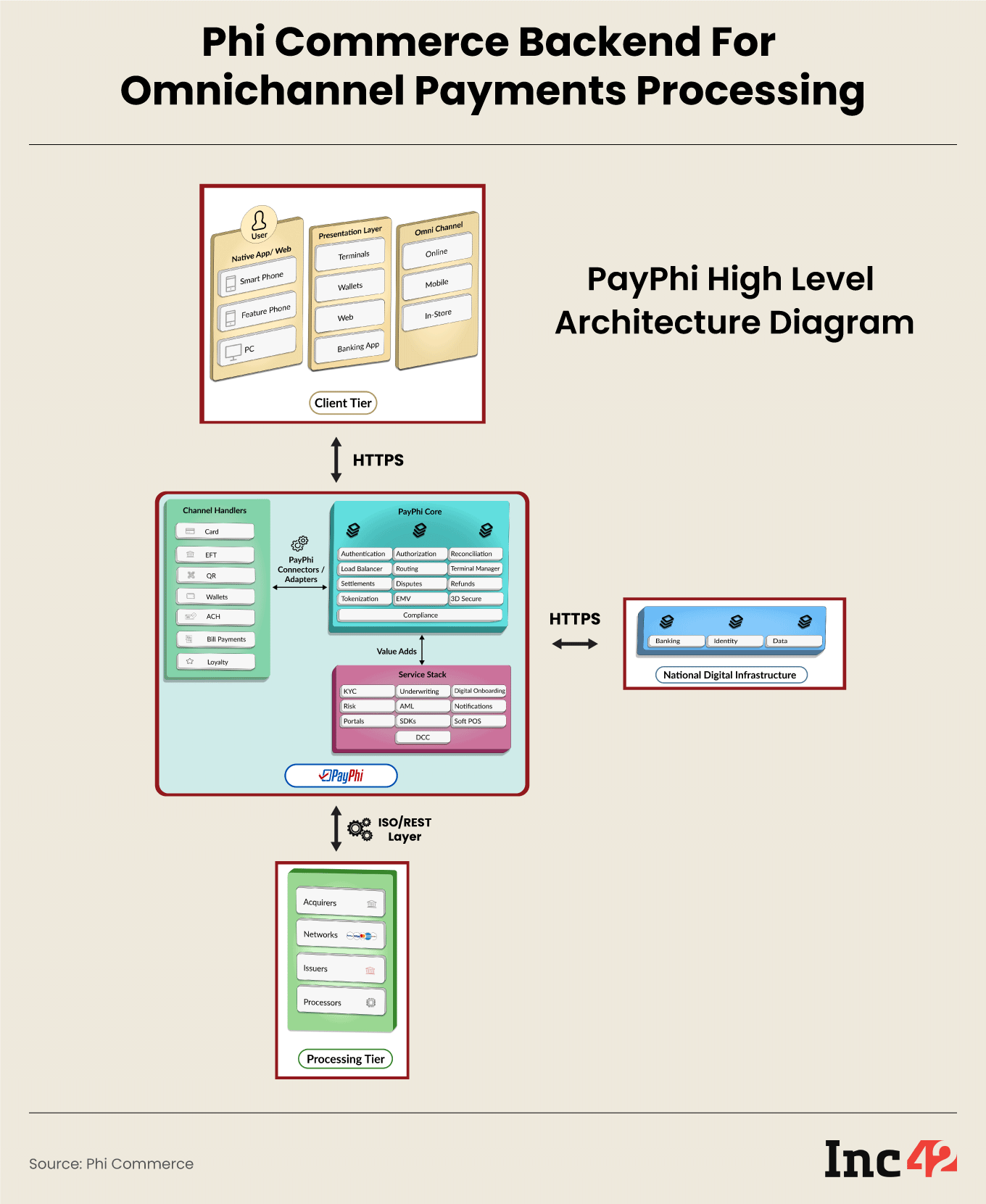

How The Payment Platform Of Phi Commerce Works

The fintech startup’s payment platform helps enterprises in three major areas: Payment collection across online and offline channels, payouts and reconciliation. As most businesses have adopted an omnichannel approach, they need to manage and monitor online and offline payments around the clock. To ensure a seamless experience across channels, payment options must be consistent across all channels and implemented appropriately. It will be unfair if online shoppers have exclusive access to BNPL/EMI options, but in-store customers fail to benefit from these schemes.

When it comes to collecting payments from distributors or dealers, enterprises deal with the added complexity of split payments and matching with against invoices, among other activities.

“Tracking and reconciling payments is a big pain point for businesses. That’s why we wanted to create a platform which would be flexible enough to not only cover all payment modes and channels but also provide value adds like APIs for accounting thereby creating huge efficiencies for our customers” said Thattil.

Service-oriented framework: The team has built the platform aligned to a service-oriented framework. Thus, instead of hard-coding the application and feature set for each payment mode, services can be configured across payment flows to ensure uniformity in solution offering across channels and payment instruments, without impacting the platform’s core code base.

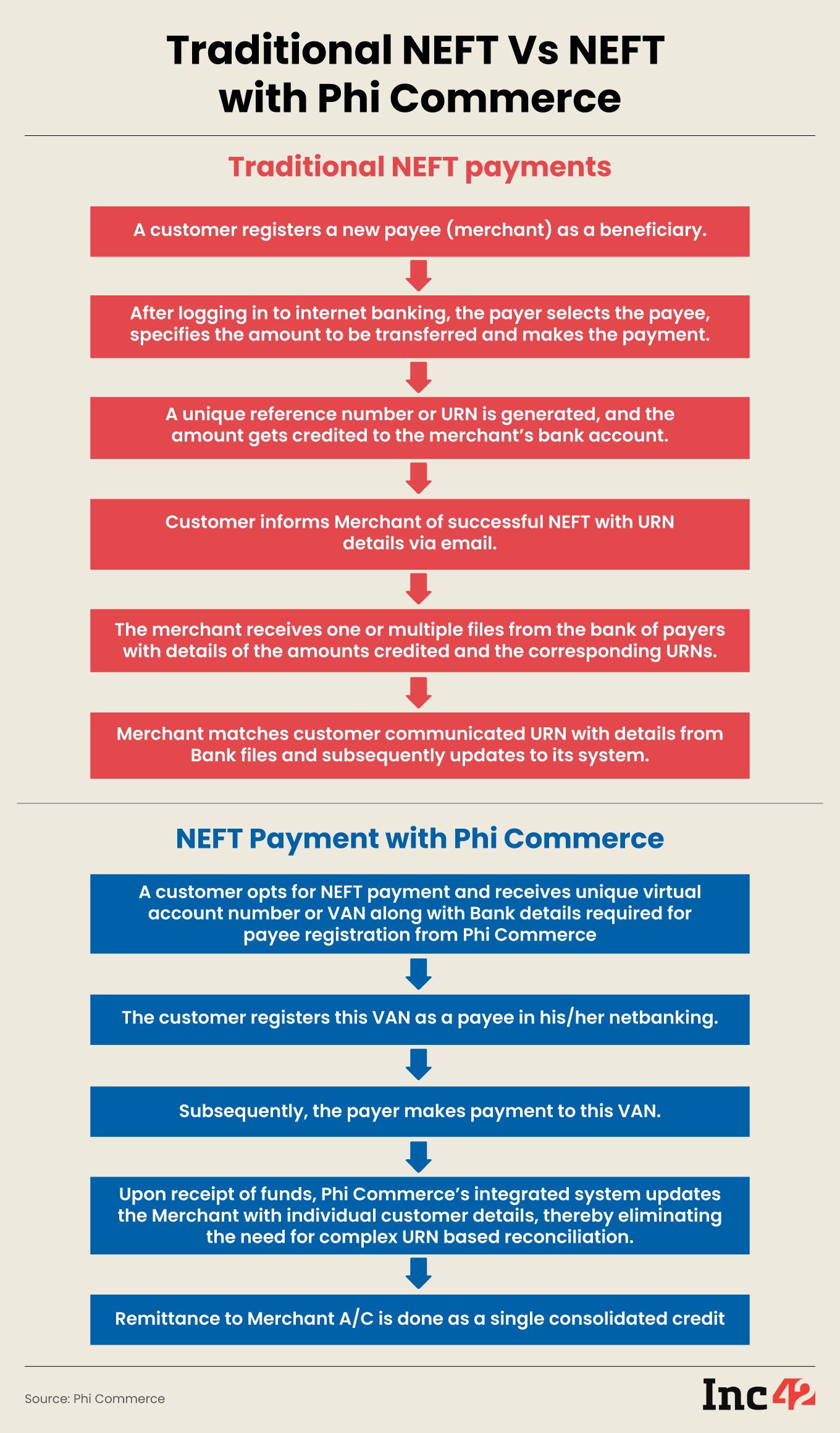

Payment reconciliation via Phi Commerce NEFT: National Electronic Funds Transfer (NEFT) is a popular mode of online transfer introduced in November 2005. But Thattil identified a critical information gap as payee names, purpose of payment and other details are rarely available when merchants receive the money via NEFT.

“This can be confusing, especially when you receive several NEFT payments every day. Most merchants use a manual reconciliation process, which is often error-prone and time-consuming,” said Thattil.

Phi Commerce launched its unique virtual account number (VAN) solution to address this problem and ease out operations and reporting challenges for such transactions.

As the VPN generated is unique for each customer, the startup can automatically track and update all related payments in real time due to its seamless integration with merchant systems. This eliminates the need for manual payment reconciliation, while customers/payers are no longer required to provide their unique reference numbers (URNs) as proof of payment. Phi Commerce also provides summary settlement reports, which can be used to reconcile payments.

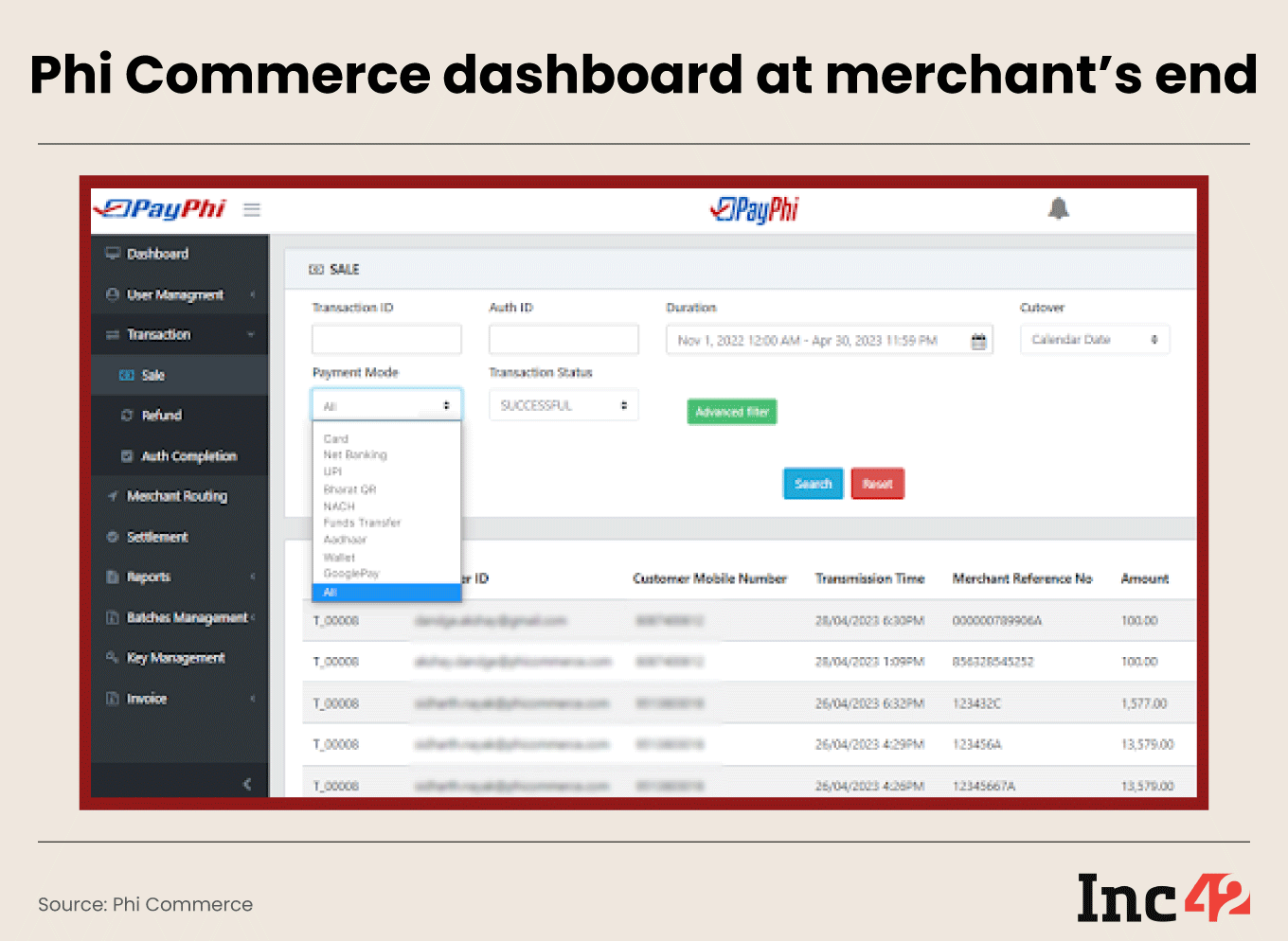

With built-in dashboards offered by Phi Commerce, merchants can also easily and efficiently track settlements.

On the revenue front, it follows a typical payment aggregator model, with the merchant discount rate (MDR) serving as the primary source of revenue. Additionally, its platform technology is deployed to businesses as a white-label solution, and Phi Commerce charges an annual subscription for the same.

Can Phi Commerce Outshine Competition, Iron Out Regulatory Glitches?

The fintech’s closest competitor is Razorpay, which provides a similar suite of enterprise payment solutions. However, several other players like Lyra.com, MONEI, Fiserv, Pinelabs, FSS Tech, Airpay, Cashfree, CCAvenue and Instamojo also offer a few services, which match some of Phi’s offerings.

Nevertheless, Thattil is confident about the fintech’s cutting-edge offerings.

Phi Commerce has strategically designed its platform architecture to offer cost-effective solutions, adding significant value to existing payment systems and helping resolve the challenges many businesses face today.

For instance, it will soon introduce Soft PoS, allowing merchants to use their mobile phones as PoS devices.

“Usually, merchants have to pay a monthly rent of INR 500-600 for a PoS terminal. Therefore, this all-new feature [soft PoS] is bound to disrupt the digital payments space, particularly in Tier II and III locations,” said Thattil.

Phi Commerce plans to expand globally in two to three years, starting with Southeast Asia and eventually moving to the Middle East and the EU. The fintech aims to process 5 Bn transactions via its platform in FY24 and triple the value of transactions from the previous year.

As the world marches towards a less-cash society, payment rails will be pivotal in driving innovative enterprise solutions and widespread financial inclusion. The ultimate in this value chain could be the blockchain technology and decentralised finance (DeFi), guaranteeing data fidelity and secure operations.

But this is easier said than achieved as the sector struggles to cope with regulatory compliance and funding crunch. According to Inc42’s Fintech Report (Q2 2023), payments startups raised $213 Mn or 25.4% of the $838 Mn funding in fintechs in Q2 2023, while lendingtech startups bagged the most – 67.1% or $562 Mn, to be precise.

Moreover, the RBI introduced a series of stringent measures for prepaid and credit card players, and nearly every fintech sub-sector has been under its scanner ever since. Not without reasons, though. According to the central bank’s 2022-23 annual report, Indian banks saw the highest number of fraudulent transactions in the digital payment space in FY23.

Additionally, the rollout of a government-backed digital currency (CBDC) instead of validating in-circulation private cryptos or the growing popularity of neobanks with advanced technology features may force payments startups to rework their playbooks to avoid roadblocks.

Although Phi Commerce aims to lead India’s digital payment revolution, ever-growing regulatory challenges can be a big hurdle going forward.

It is pertinent to note here that the company burnt its fingers in 2022 when it was about to go live with a large business prospect. The RBI had then introduced a new policy mandating all payment data to necessarily reside within the country, giving Phi Commerce a surprising blow and putting its plans on the back foot.

“One of our partners was a multinational company, which processed payments from its data-centre in Europe. Just a week before the big launch, we went back to our customer, took him into confidence and we were able to convince them to push the launch by a month to enable compliance with the mandate. Our transparency with our customer ensured that our relationship, built on this foundation of mutual trust, prospered in the years to come,” recalled Thattil.

Thattil is optimistic, though, about the road ahead. After all, a vast segment of India’s 1.4 Bn population remains outside the digital realm, although individuals and businesses in this space must be empowered with secure and efficient tech solutions. But given the size of this still untapped market, no single player can capture it all, and there will be enough growth opportunities for Phi Commerce and its ilk.