Despite contributing more than 37.5% of India’s GDP, MSMEs face significant challenges when it comes to borrowing cash from legacy FIs

Lendingkart uses more than 5,000 data points to increase the scope of creditworthiness for small businesses

The company has also built multiple E2E solutions for banks and NBFCs to help them extend credit lines to MSMEs

Inc42 & WebEngage present, the second edition of “Decoding Hypergrowth”, a series capturing stories of successful businesses, the importance of intelligent engagement and their approach to creating the same.

The biggest dilemma for micro, small and medium enterprises (MSMEs) is knowing when is the right time to look for credit, what the right amount is and how fast they can raise the money to meet operational requirements. India is home to nearly 6.3 Cr MSMEs, accounting for almost 37.5% of the GDP. But most of them lack a well-structured credit financing strategy that can see them through difficult times.

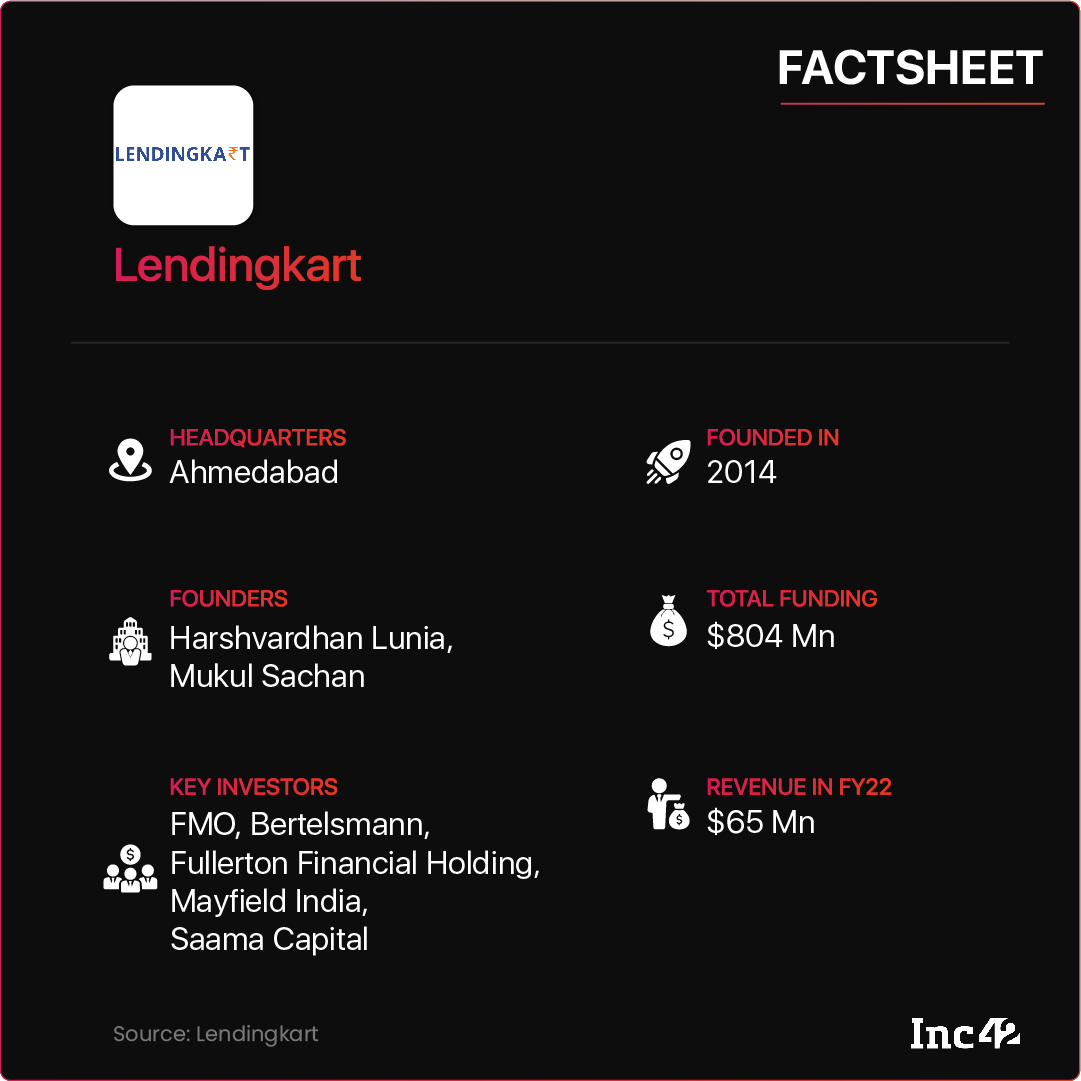

Ahmedabad-based Harshvardhan Lunia had seen this too often when he grew up. His father was a business owner residing in the city, and the family had to cope with similar challenges. However, he had pursued a career in finance, working with the likes of HDFC Bank, Standard Chartered Bank and the ICICI Bank for a decade or so. His work helped him understand why and how small businesses struggled to raise business loans. It also motivated him to develop a tech-driven credit system different from legacy banks, traditional NBFCs or other financial institutions (FIs).

Keen to pursue his passion without further delay, Lunia (CEO), along with Mukul Sachan (the COO left the company in 2019), set up Lendingkart in 2014 to offer collateral-free, short-term loans to MSMEs. But it was easier said than done, as the startup realised from its extensive conversations with many small business owners.

For starters, MSMEs come with their unique set of challenges as these are more susceptible to market volatility, and even small dips in sales can affect their revenue flow. Second, many lack the credit history or formal financial data needed to assess their creditworthiness. Plus, there is the massive paperwork required by FIs to process loan applications and the long turnaround time for loan disbursements. As most MSMEs are regional entities located away from the Tier 1 business hubs, FIs often find it geographically constraining to approve such loan applications. Businesses, too, struggle to navigate complicated documents in English/Hindi as most of them speak regional languages. The lack of collaterals/guarantees and high-interest rates charged by the grey market operators also throw a spanner in the works.

Together, these factors have a massive credit gap. According to Research and Markets, the credit demand in the MSME space is $490 Bn as per the RBI data, while the overall supply from formal sources stands at $192 Bn, underlining how this sector remains underserved even today.

Lunia concurred. “Even today, the credit process in traditional FIs takes months as credit evaluations are hampered due to the absence of crucial data points. When we started in 2014, MSMEs had very few resources, and the ones that existed should have done some hand-holding for business owners due to the complicated nature of these transactions. But no one did it,” he said.

Lendingkart: The Take-Off And The USP

Funding ‘repeatable growth’ across a wide range of MSMEs (Lendingkart is sector-agnostic) called for eliminating all human biases from the assessment system and required a streamlined procedure that would cover every single step, from application filling to online loan disbursal. It further needed effective customer experience management to ensure a seamless and hassle-free MSME journey (more on that later). So, Lendingkart doubled down on developing its tech-powered lending platform and further procured an NBFC licence in 2014 for disbursing an INR 50K-10 Lakh collateral-free loan for a period of 12-36 months. Later on, the upper limit was pushed to INR 2 Cr.

However, at the core of its lending ecosystem lies a proprietary underwriting mechanism that uses big data and machine learning AI to consider more than 5,000 data points crucial for MSME evaluation. After inputting all essential information such as the current financial year’s cash flow (an estimate of net balance of cash moving into and out of a business), GST records and more, each applicant’s data is run past this system to classify it under one of the five risk categories and determine the loan amount accordingly.

It has also dealt with a few critical issues. For instance, filling a loan application does not take more than 15 minutes now, and loans are approved and disbursed within 72 hours. The platform is currently available in seven regional languages to make it more inclusive and functional.

A look at its client base further confirms breaking down silos in the MSME lending space. Geographical diversification has gotten a boost — Lendingkart’s first loan went to a small business in Guwahati, 2,000 km away from the company’s headquarters. Around 81% of the companies come from Tier 2 cities and beyond, and 20% had no prior credit history.

More Solutions For MSME–Focussed FIs

Besides the in-house credit platform Lendingkart has developed three major financial products for banks and NBFCs.

Data Analytics Through Cred8: Launched in September 2021, this credit intelligence platform provides MSME credit scores based on Lendingkart’s underwriting model. As part of the company’s enterprise-to-enterprise (E2E) offerings, Cred8 enables FIs to support small businesses previously considered ineligible for loans.

Platform Intelligence Through xlr8: Set up in January 2021, xlr8 is an omnichannel platform with an API tool for online partners and a SaaS solution for offline companies. This helps FIs map the real-time loan journey of companies to keep an eye out for payment delays and help borrowing companies optimise their advantages. The platform also offers a host of customisation tools to help partners build flexible and cost-sensitive loan options. For instance, a lender may use these filters to provide a lower interest rate or a flexible repayment plan for a long-term customer.

Loan Disbursal Through 2gthr: Introduced in November 2020, this E2E co-lending platform has adopted a SaaS model and helps banks and NBFCs in origination and disbursal of collateral-free loans to MSMEs. The 2gthr platform is a customisable solution that offers clients to both discover origination as well as allows the end customers in taking a faster digital lending journey.

How Marketing Automation Drives Lendingkart’s Journey

The burden on fintech firms varies based on what they are doing and for whom. For a technology-driven NBFC like Lendingkart with a lot of skin in the game (after all, it checks a borrower’s financial health in-house instead of doing it via third-party service providers), onboarding minimum-risk companies with strong cashflows is mandatory for growth. It also means creating the right kind of buzz around its products and services, a comprehensive solution for effective engagement.

For Lendingkart, there was a strong need for multichannel customer engagement to reach the businesses on their preferred platform. Further, MSME is a highly diverse business segment and to cater to the needs and requirements of every business, Lendingkart required tailormade marketing solutions for individual customers.

Watch Lunia talk about Lendingkart’s growth journey and its tech-driven credit model at play

After trying and testing different marketing strategies, the fintech company decided to tie up with Mumbai-based marketing automation platform WebEngage in 2018. The partnership has allowed Lendingkart to build an integrated database to capture the entire journey of the customers in a single view. It has also allowed Lendingkart in retrieving real-time analytics to decode campaign effectiveness, thus helping the fintech player make strategic decisions.

According to Lunia, the decision to collaborate with WebEngage came from the simplicity and intuitiveness of the platform, as well as its analytical capabilities.

“It is the ease of usage of several features that makes life easy for us. It’s quite important for startups operating with limited resources to make use of these features and services so that they can execute customer engagement campaigns without having to struggle much,” said Lunia.

Lendingkart’s digital solution to measure creditworthiness is critical for its success. “We actively train our credit scoring model to be as accurate as possible. The emphasis on accuracy has also translated into fairness across all the important and impactful dimensions,” Lunia added.

Keeping accuracy at its core, the company intends to expand its offering by delving deep into MSME business models.

The digital lending sector in India has played a key role in enabling financial inclusion. It has also been a crucial financial resource as less than 10% of India’s small and medium businesses have access to organised credit. As a result, the market is growing fast and is fore casted to be the highest penetration sector by digital channels in India by 2023, a KPMG report says.

According to Research and Markets, the total digital lending (B2B and B2C) market in India was valued at $110 Bn in 2019 and is expected to reach $350 Bn by 2023, growing at a CAGR of 33.56%. The total digital lending market share is also expected to improve from 23% to 48% by 2023.

With more than 63 Mn MSMEs currently operating in India, fintech firms with lending solutions are clearly tapping into a promising segment. However, digital lenders offering business loans need to understand better how small businesses work to develop the right loan products, leading to enhanced viability and mutual growth.