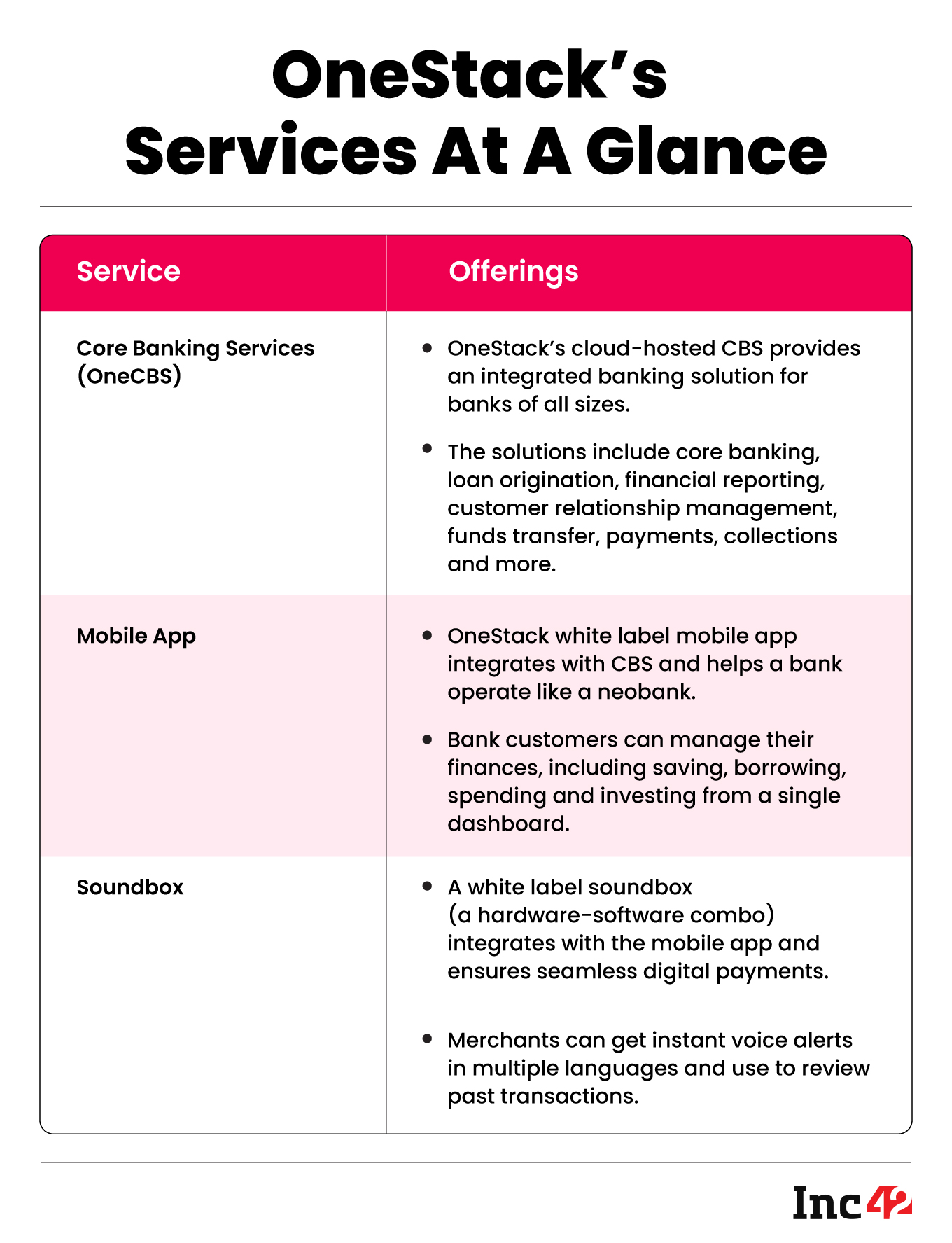

The platform offers core banking solutions as well as a white-label mobile app and a soundbox

The Venture Catalysts++ -backed startup also provides a wide range of value-added services including UPI, QR code, BBPS, insurance, investment, co-branded cards and more

OneStack is working with 100 plus cooperative banks and financial institutions and in the next two years it aims to cater to a big chunk of the bankable population

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

India’s push towards digital transformation in the banking and financial sectors has seen the rise of a new-age citizenry seeking technology-driven services for enhanced customer experience. However, not all Indian banks have invested heavily in tech adoption to improve their offerings and attract a larger customer base.

India has a vast network of more than 1 Lakh urban and rural co-operative banks and societies, according to industry experts, serving middle- and low-income customers and micro -small-to-medium businesses. Besides, numerous niche credit societies cater to small borrowers from the unbanked/underbanked population. Many of these financial institutions still leverage outdated tech tools and safety/compliance-deficient processes without full-stack core banking solutions (CBS) and easy-to-use mobile banking apps. This has led to a loss of customers, as people today want banks to digitalise fast and excel in every service area, be it transactions, saving, lending, insurance or wealth creation.

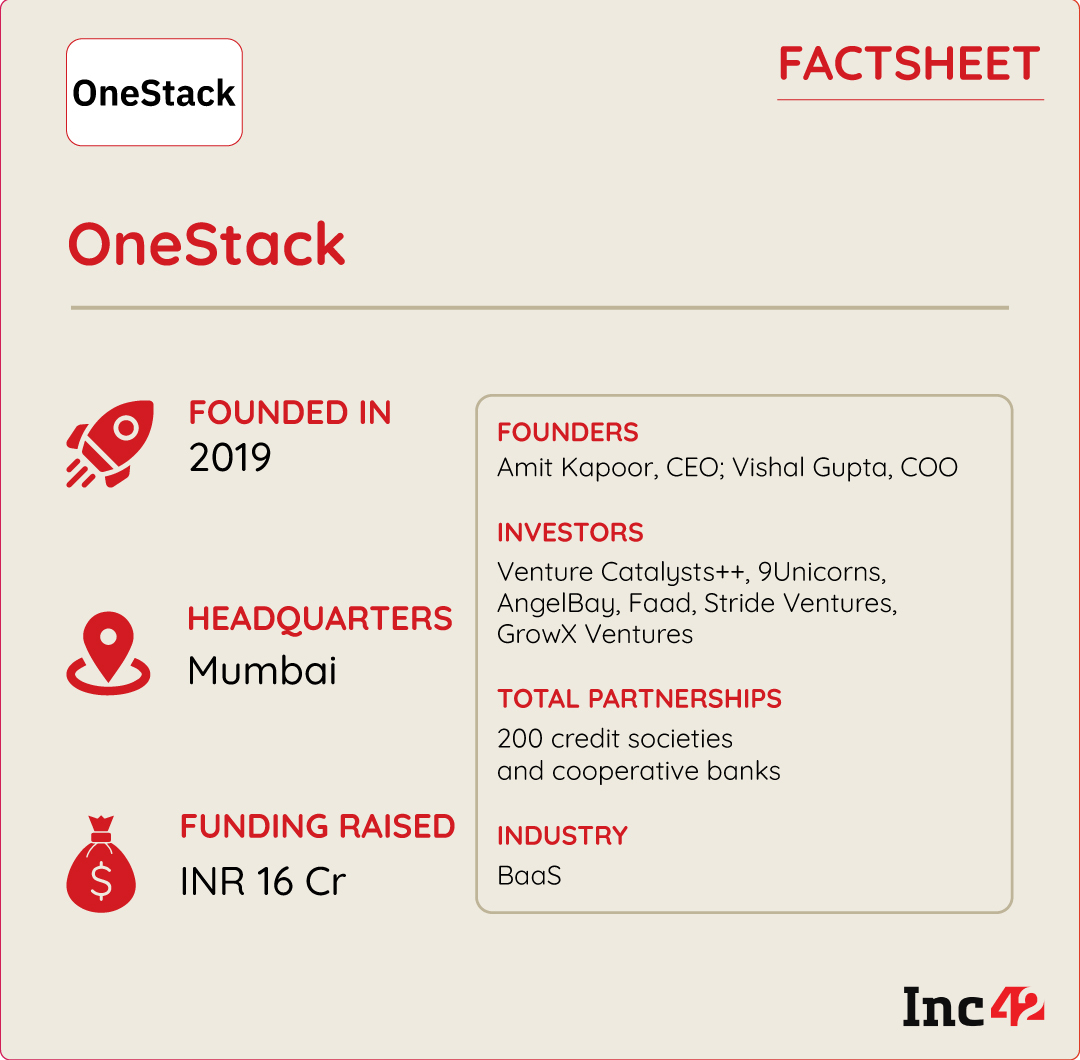

Set up by Amit Kapoor and Vishal Gupta, Mumbai-based BaaS (banking as a service) startup OneStack is a technology service provider (TSP) that helps co-operative banks and credit societies to digitise and enhance their digital capabilities. The B2B2C platform has developed easy-to-use APIs to offer a wide range of core banking solutions or CBS, enabling FIs of all sizes to provide top-end services in sync with evolving requirements.

It has also created a white-label mobile app that can be branded and customised by a bank to help its customers carry out key financial activities. The app features a unified dashboard, providing a consolidated view of the bank’s products and services and enabling its customers to track their assets, liabilities and cost-to-income ratio to determine their financial health.

The platform’s CBS stack is in the cloud and is integrated with its mobile app for seamless operations. The aim is to ensure that all ‘Bharat’ banks will have the technology edge on a par with digital-first neobanks, which are becoming increasingly popular for their agility, versatility and customer engagement.

OneStack’s CBS (OneCBS) helps build, customise and launch full-stack banking services, including KYC and customer onboarding, account opening, bill payment, fund transfer, card management, CRM, financial reporting and more. While its QR and UPI services (payment issuance and acceptance) have driven partner banks’ CASA growth, the platform has also entered the micro-lending space using OCEN, a cluster of APIs seamlessly connecting borrowers and lenders.

Besides, it uses AI/ML solutions to analyse bank customers’ data and deliver recommendations for insurance and investment products to improve their financial health.

“Our CBS empowers banks to streamline their operations and enhance customer service efficiently, along with helping them to be completely regulatory compliant to compliance,” said founder and CEO Amit Kapoor.

Among its value-added services is the soundbox, a seamless digital payment solution for merchants, which can be deployed through co-operative banks and credit societies. These smart devices instantly announce payment alerts in Hindi, English and other regional languages, while customers can pay through UPI and other channels (more on that later).

The startup claims to have onboarded more than 200 co-operative banks and credit societies. It also secured $2 Mn in a pre-Series A round in July 2023 from Venture Catalysts++, growX Ventures, Stride Ventures, 9Unicorns, Sunil Kulkarni and other existing investors.

Tapping Into Remote Areas Is Tough; Here’s How OneStack’s Marketing Works

By the time Kapoor started his entrepreneurial journey in 2012 with Airpay (an omnichannel payment platform), he had actively collaborated with the BFSI sector and worked on critical fintech solutions such as payment gateways and the PoS (point of sale) ecosystem. He also engaged with co-operative banks and realised how their inability to provide essential digital solutions hindered customer service.

It was a eureka moment for Kapoor when he saw the massive potential. OneStack was launched in 2019 to digitise the co-operative banking industry. Four years later, Vishal Gupta joined the startup as a co-founder. Gupta and Kapoor have known each other since 2012 when they pursued business studies together at INSEAD (Institut Européen d’Administration des Affaires).

The first major hurdle was a connectivity challenge that very few had anticipated. Most credit societies (and some rural co-operative banks) were located in such remote areas that OneStack’s sales team had to travel for a few days to reach their destinations. These long journeys ate into the startup’s time and resources, and the young company was compelled to rethink its marketing and sales.

OneStack operated in western and northern India then and onboarded two of the three banks in Mizoram. However, it implemented a two-pronged marketing strategy to grow its customer base substantially. The platform opted for B2B promotion to resonate with the specific regional requirements of the co-operative sector. Therefore, its vernacular muscle/regional language services came into play.

The other strategy was word-of-mouth promotion, helping the startup gain visibility. Initially, this meant tapping into the founder’s networks and connections. However, after experiencing OneStack’s offerings, user banks spoke highly of its services and recommended its use, thus amplifying its reach across Indian states.

Besides, the startup received immense support from its investor Venture Catalysts++.

“Initially, I had shared a concept of OneStack on a preliminary deck and the investors believed in us since the first day,” said Kapoor, emphasising how proactively the VC firm supported him.

Venture Catalysts’++ investment of INR 1.5 Cr in the startup’s seed round proved to be more than just financial backing. Its involvement in connecting the startup with key players and other investors in the ecosystem provided invaluable support that spurred its growth, said Kapoor.

“Meeting with Apoorva Sharma (co-founder of Venture Catalysts++ and 9Unicorns) is intense and very interactive. His clarity of thought and the ability to put the same in words are amazing. Every time I meet him, I get to learn more about my own business,” he added.

A bank’s journey with OneStack starts with a comprehensive onboarding process. The startup offers personalised support to every bank by assigning a dedicated account manager who assists the bank until its services are successfully launched post-API integration, which may take up to 15 days.

Its core offering is the cloud-based OneCBS, which provides integrated banking solutions such as payments and fund transfers, collections, loan assessment and approval (auto, home, and SME loans, as well as pre-sanctioned credit lines through UPI), customer relationship management, and submission of multiple audits/reports to the RBI and other regulatory bodies. Together, this service cluster helps banks run their operations more efficiently, reduce risks, and develop tailored solutions/financial products for their customers based on the extensive data analytics capabilities built into the system.

Additionally, there is a user-facing white-label app so that bank customers can easily manage their finances, including saving, borrowing, spending, and investing, from a single dashboard. As the app generates accurate financial snapshots, banking customers can analyse the same to make informed decisions, while co-operative banks get a competitive edge over their mainstream peers.

Talking about OneStack’s UPI/QR payment solution, he said its (merchant-focussed) B2B approach differentiates the service from the rest as established players like Paytm and PhonePe target the consumer side (B2C) of the payment business. On the other hand, the startup provides audio-enabled soundboxes (a hardware-software combo) as a white-label solution so that these smart devices can be branded as banks’ own and delivered to their merchants to ensure seamless digital payments.

A merchant can receive a soundbox from a bank (supplied by OneStack) by paying INR 1 per month. As soon as payments are received, they get instant voice alerts in multiple languages to keep them updated. The device can also be used to review past transactions, and its functionalities can be integrated with mobile apps for quick and hassle-free usage.

Payments collected through soundboxes go directly to the merchant accounts held at co-operative banks, claims Kapoor. This simplifies financial transactions for micro-sellers while reinforcing banks’ branding against leading fintech players.

Revenue is generated through BaaS subscriptions (payments for the OneCBS stack), white-label solutions, and value-added services, or VaS, many of which are work in progress. However, the platform will soon roll out various value-added services, including insurance, investment products, co-branded cards, and more. Earnings from these channels will complement the income generated by OneStack’s core offerings.

BaaS Is Brilliant, But Will There Be Indian Takers?

OneStack’s genesis lies in open banking, which has surpassed pure-play BaaS and aims to transform the narrow domain of legacy banking. It may sound too forward-thinking, but Kapoor pointed out that 380 Mn Indians currently account for 50% of the bankable population across metros and Tier II and III cities. In essence, the need for agile banking solutions is growing exponentially. But a mammoth increase in infrastructure and operational costs will be unviable, given the macroeconomic headwinds and the threat of a global slowdown.

Considering these, the OneStack founder wants to extend core banking services to the remaining bankable population in the next two years by adding neobanking capabilities to 150 more co-operative banks. Its growth plan involves expanding pan-India and raising another round of funding by FY25.

OneStack’s endeavour to cover the total addressable market (TAM) within the co-operative banking sector will further reinforce the promise of broadening financial inclusion. In fact, the growing impact of Indian BaaS startups, such as OneStack, Setu and Zeta, has created a paradigm shift, meeting end-to-end customer requirements and improving customer experience as never before.

Globally, the BaaS market is expected to reach $11.6 Bn by 2028 from an estimated $4.4 Bn in 2023, growing at a CAGR of 26.60%, a thumping rise that augurs well for industry players. No doubt there had been initial hesitation closer home regarding compliance and data security, to say nothing about the tech overhaul needed to maximise BaaS benefits. But the Lego-like API block-building and financial service sachetisation will be a win-win for incumbent banks and FIs, new-age fintech providers and TSPs like OneStack as it will put customers at the centre and help grow the banking ecosystem to the back of beyond.

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.