Lendingkart is one of the few companies who have not been affected much by the NBFC crisis of 2018

Lendingkart has disbursed more than 76K loans to more than 64K MSMEs so far

The company is further utilising its tech capabilities to penetrate deeper into tier 3 and tier 4 cities

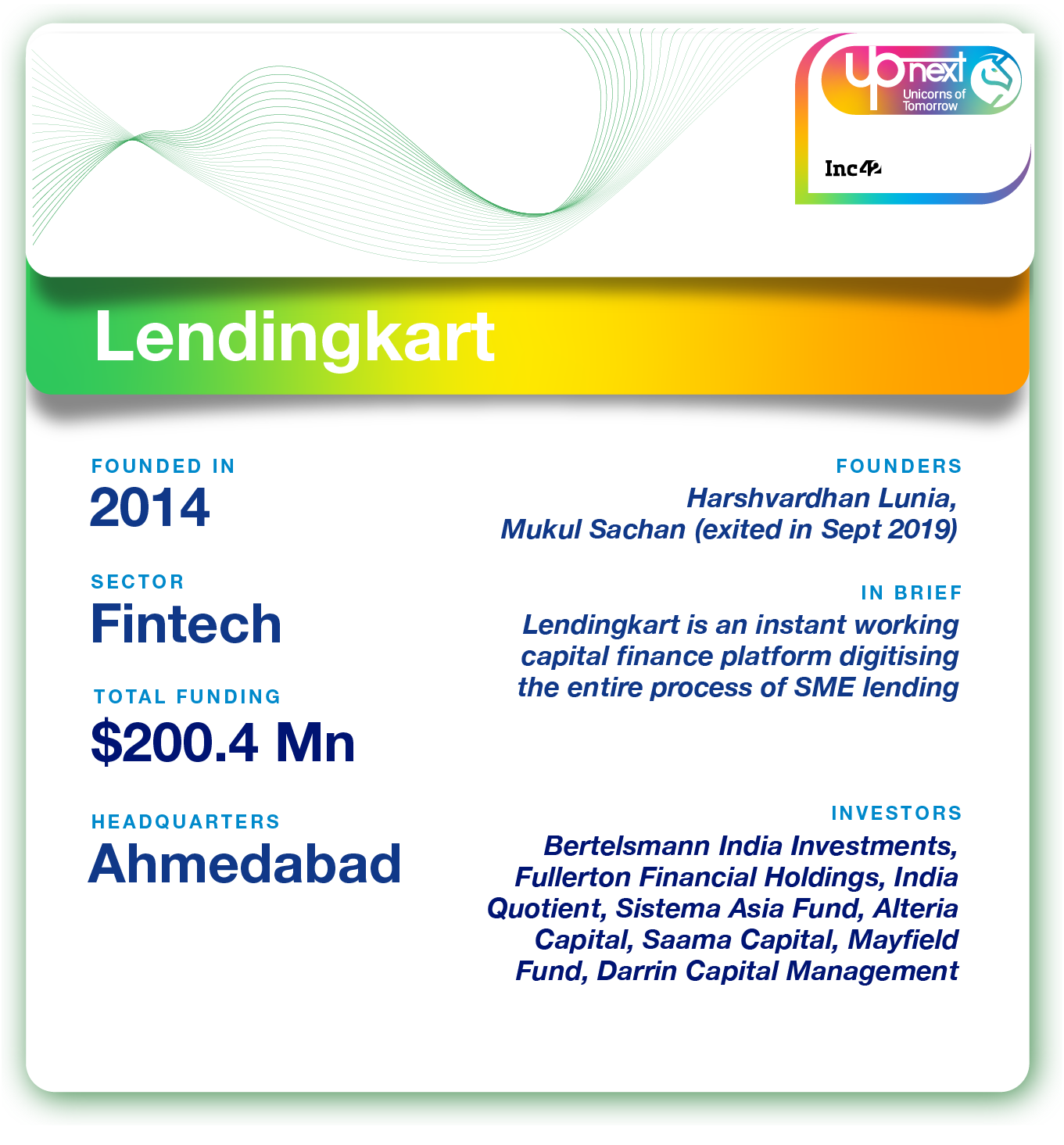

To celebrate India’s rising startups, Inc42 is profiling a new soonicorn every Friday in the Inc42 UpNext: Unicorns Of Tomorrow series. For the next few months, we will be speaking to founders and cofounders at these potential unicorns and shining light on their journeys and growth stories. We begin the series with a look at B2B lending tech platform Lendingkart.

Entrepreneurship in its true sense is about creating an impact on a large untouched segment. It is only then that an entrepreneur can validate the credibility of the business model. For Harshvardhan Lunia, the founder of Ahmedabad-based digital SME lending startup Lendingkart, the journey has been no different.

“Back in 2014 when we started, I still remember the very first loan we disbursed in Guwahati, 2000 kilometres away from our headquarters. That’s when we realised the potential of the platform we are building and the disruption we are set to initiate,” – Harshvardhan Lunia.

Ever since then, Lendingkart has been a part of many customer success stories and along the way, it has become part of the group of Indian companies heading for the coveted unicorn valuation by next year.

Helping MSMEs get access to credit right from Agartala to Surat and from Jammu to Kanyakumari, the company has become geographically agnostic. With offices in three cities (Ahmedabad, Bengaluru, and Mumbai), it has positively impacted small and medium businesses in more than 1300 cities across all 29 states and union territories of the nation, making it the NBFC with one of the largest geographical footprint in the country.

With more than $200 Mn raised so far from a club of investors such as Bertelsmann India Investments, Fullerton Financial Holdings, India Quotient, among others, the company is currently among a few fintech startups racing to become a unicorn soon.

How Did It All Begin?

During his stint with large private sector and multinational banks, Lunia experience first-hand how decisions were taken in the small loan divisions. “I realised how many small business owners were denied financing despite being creditworthy because they are unorganised and hardly maintain their books of accounts. Thus, in 2010, I returned to India after a successful stint in London with the aim to build a platform that makes Indian MSMEs bankable,” he added.

Initially, he started with an advisory business and realised the various inefficiencies that marred the MSME lending space in India. In India, formal sources only cater to 22% of the total MSME debt financing. Lack of credit history, collateral and accounting discipline further harm their capacity to procure funds from sources other than money lenders and friends and family.

Lunia wanted to solve these issues by bringing processes online and devise methods to create a credit score, he joined hands with Mukul, an ex-finance director and an old school friend to give shape to the business plan.

“In the beginning, we actively interacted with small business owners to understand their needs better. There was an unmet demand of short term (up to 36 months), small ticket size (INR 50K – INR 10 lakhs) loans for these MSMEs. We then ventured onto build a comprehensive online lending institution dedicated to helping MSMEs with working capital finance and that’s how Lendingkart came into existence,” Lunia recalled.

Here’s a timeline to showcase the key milestones achieved by Lendingkart so far.

Highlighting The Lendingkart Growth

Having evaluated around 6 Lakh applications and disbursed more than 76K loans to more than 64K MSMEs across 28 diverse business sectors, Lendingkart has a wealth of data about credit for small businesses. It told us 80% users are first-time unsecured business loan borrowers, leading to a 200% average year-on-year increase in the number of loans disbursed.

Here’s what Lendingkart has achieved over the last five years in terms of reach, credit evaluation and loan disbursements.

How Lendingkart Sets Course For The Unicorn Club

A strong foundation is a must to build any successful and sustainable business model in the long run. Lendingkart founders understood this a long while back. From adopting the latest technologies to product innovation and from scaling in the right direction to tackling failures in a right manner — Lendingkart has got all under its belt.

For instance, recently cofounder Sachan steppe down from his position of COO and left the company. According to Lunia, transparency in such matters is key in order to make sure all the stakeholders are aware and fully support the decision. “So, while this has been a shocker for others, we have been doubling our monthly run rates, our revenue and loan books have also been growing at approximately 3 times year-on-year,” chuckled Lunia.

Further, SWOT analysis is a widely used analysis to help a growth stage company figure out upcoming opportunities and prepare for threats. Here’s one for Lendingkart to assess the direction the company is going in.

So how can Lendingkart tackle existing challenges and reap in the rewards of the opportunities ahead?

Product Innovation

Supply chain finance, term loans, line of credit are a few of the more popular products from Lendingkart. It has also incorporated WhatsApp chatbot for document collection, and introducing the website in 7 vernacular languages has further eased the language barrier among its customer base.

Reaching The Target Audience

Multiple online channels, active re-engagement, digital campaigns as well as SEO based searches are used to reach and engage the target audience. The company is also focussed on building a high content base in the form of blogs that are useful for self-employed individuals and entrepreneurs.

Utilisation Of Funds

The initial focus for the first few funding rounds at Lendingkart was towards building a strong team. The next phase was all about building its sourcing and credit underwriting capabilities. Later it turned its focus towards building a strong tech platform and analytics to ensure optimal reach. Through the last couple of funding rounds, however, it is working towards scaling the business and investing in performance marketing activities for scale.

Credit Risk Assessment

For assessing the creditworthiness of a borrower, it pulls data points from bank statements, VAT/GST returns, credit bureau reports, defaulters list, social media platforms, industry databases and other partners, which is collated in a proprietary credit analysis template.

“This template forms the base to assess the creditworthiness of borrowers, capturing over 10K variables using our machine learning algorithm,” explained Lunia.

Representatives then complete loan documentation and KYC, NACH mandate and post-dated cheques are also collected. The company also makes use of alternate data like transaction data, statutory compliance, family background, educational background, etc. to strengthen the credit analysis based on financial variables. Moreover, the self-learning algorithm improves with repayment, delays and delinquencies data making it more robust with every repayment collected.

Technological Capabilities

Lendingkart claims to be completely technology and analytics-driven with automated processes throughout the funnel – from lead sourcing and credit evaluation to underwriting and disbursal. Data infrastructure is further driven by AI which helps capture every interaction with the customer: call logs, call transcripts, SMSes, email, product interaction variables and social data, in addition to traditional LOS and LMS data. It also applies a significant amount of ML and AI to clean data.

Further, it uses the microservices architecture for scalability. The entire tech stack is hosted on AWS. And as Lunia said, “Using the right tool for the right job is very important, and that is how it works here.”

The Road Ahead

Lendingkart is one of the few companies who have not been affected much by the NBFC crisis of 2018. “Given our healthy unit economics and the huge market opportunity that lay ahead of us, we had a fair amount of traction from the investor community. Despite the fear of liquidity, the players in the fintech ecosystem have continued to raise large amounts of funds from corporate borrowers through NCDs and CPs and are growing undeterred,” said Lunia.

The company is further utilising its technology capabilities to continuously innovate and penetrate deeper into tier 3 and tier 4 cities. “For example, we are working on an NLP-based system that can convert SMS data into credit variables, and also plan to use similar techniques to convert voice transcripts from calls into decisioning variables,” added Lunia.

Hence, ML techniques combined with technology to collect data are enabling Lendingkart to:

- Approve customers that would not have been otherwise approved based on additional data

- Assess the risk and price customers appropriately

- Optimise marketing and operations cost, therefore leading to a better bottomline

Going ahead, it is also working to bring in alternative data-based credit model to serve MSMEs in diverse business sectors such as restaurants, online sellers, telecommunications among others using their transaction data instead of banking data to boost financial inclusion. It is also working on building propensity models that predict the probability of the platform in selling other loan products to an existing customer.

Lunia believes in better days ahead. The fintech startups of today are all exploring different ways to serve their existing customer base better. Digital lending and paperless personal loans will further evolve to help a large number of salaried and self-employed individuals in the country.

“We are hopeful that the coming years will further push us in our efforts to help MSMEs achieve financial mainstreaming. The rapid and healthy scale-up that Lendingkart has already begun to see, we are all set to double the book size within a year from now and continue to grow the business and remain a significant contributor to the fintech ecosystem.”